1999 Annual Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Sweet and Chocolate Quiz

The Sweet and Chocolate Quiz Clue Answer 1. Sly giggles 2. High class thoroughfare 3. Money making royalty 4. Dark occult 5. Mother’s local 6. Clever folk 7. Various black items 8. Sport for Princes 9. Frankie Vaughan wanted it 10. Good children get these 11. Feline equipment 12. Garden flowers 13. Assorted girls 14. Dairy holder 15. Arrange marriage partners 16. Edible fasteners 17. Wobbly infants 18. Talk quietly 19. Big bus 20. Gem orchard 21. Spin around 22. Capital granite 23. Lorry driver’s snack Emaths.co.uk Emaths.co.uk Emaths.co.uk Emaths.co.uk Emaths.co.uk Emaths.co.uk Emaths.co.uk Emaths.co.uk 24. 100% Au 25. Istanbul harem 26. Out there (look up at night) 27. Even more out there! 28. Big cat’s pub 29. Noisy insect 30. One who wanders 31. Musical bard 32. Lots of parties 33. Outside meal 34. Easily blown 35. Locals from Malta 36. Reward 37. Ten cent pub 38. Toothless Drink 39. Lost them? 40. Sweet tooth cleaner 41. Pub pins Initials and Words Quiz Emaths.co.uk Question Answer 1. 26 = L of the A Letters of the alphabet 2. 7 = W of the A W 3. 1001 = A N 4. 12 = S of the Z 5. 54 = C in a D (including the J) 6. 9 = P in the S S 7. 88 = K on a P 8. 12 = D of C 9. 32 = D F at which W F 10. 18 = H on a G C 11. 90 = D in a R A 12. -

Charlie's Group Limited

Charlie’s Group Limited Independent Adviser’s Report On the full takeover offer from Asahi Beverages New Zealand Limited APPENDIX July 2011 024 Table of Contents Glossary Glossary..........................................................................................................................................................................................3 Glossary 1. Terms of the Asahi Offer ......................................................................................................................................................5 1.1 Background to the Offer ...............................................................................................................................................5 Term Definition 1.2 Details of the Asahi Offer...............................................................................................................................................6 90% Minimum Acceptance Condition A condition of the Asahi Offer that requires that Asahi receive acceptances to take its 1.3 Requirements of the Takeovers Code...........................................................................................................................7 shareholding to 90% or more of the Charlie’s Group shares on issue 2. Scope of the Report..............................................................................................................................................................8 2.1 Purpose of the Report ..................................................................................................................................................8 -

For Sale by Tender Sale

On Behalf of a Retained Client U CATALOGUE FOR SALE BY TENDER SALE Tenders Due 12:00pm BST on Wednesday 30th May 2018 to [email protected] Viewing: 25th May and 29th May 2018, 9:00am – 16:30pm Location: 11 Barnes Wallis Road Segensworth East Fareham PO15 5TT REGISTRATION FORM This form must be submitted with the tender catalogue. Name ...................................................................................................................... Company Name ..................................................................................................... Address .................................................................................................................. ................................................................................................................................ ................................................................................................................................ Postcode ................................................................................................................ Position in Company .............................................................................................. Office Tel No. ......................................................................................................... Mobile No. .............................................................................................................. Email Address ........................................................................................................ Signature -

Curriculum Vitae

Career BIO - JOSE GORBEA Jose Gorbea joined HP in 2017 and is Head of HP Graphics Solutions for Brands in EMEA. Jose is a passionate marketing leader & keynote speaker with solid expertise & thought leadership across the marketing mix, coupled with a strong track record on revitalizing brands by inspiring teams to deliver breakthrough brand strategies & award-winning campaigns. He has led for nearly 20 years the overall marketing strategy & execution of well established brands such as Kit Kat, Crunch, Cadbury, Milka, Toblerone, belVita, Ritz, Philadelphia, Trident and Stimorol across numerous geographies such as Latam, Europe and Global. In his last role at Mondelez, he was the Head of Marketing & Digital Operations for Europe. Jose has helped shape the marketing culture in global organizations with a socially responsible, competitive & winning mindset by strengthening marketing capabilities in Nestle, Mondelez and HP. Jose holds a digital marketing certification from the Google Marketing Academy which makes him an asset for delivering brand solutions in a digital world. • Recognized by CNN's Grupo Expansion with a Marketing Monster Award in delivering one of the best performing marketing campaigns of 2010 in Mexico with the Nestle 'Carlos V' brand (Link → http://expansion.mx/monstruos- de-la-mercadotecnia-2010/2010/10/20/nestle-juega-y-reposiciona-a-carlos-v) • Recognized by Mondelez with the 'Best Brand Revitalization' Award in 2016 for successfully turning around the Stimorol chewing gum brand in Europe. SCHOLARSHIP / CERTIFICATIONS • IBEROAMERICANA UNIVERSITY – Mexico City - Business Management Bachelor Degree (1996-2000) / Marketing Specialty Degree (1999-2000) • GOOGLE DIGITAL ACADEMY – Europe - Squared Guru Certification – Digital Marketing (2017) PROFESSIONAL EXPERIENCE • MONDELEZ EUROPE – Zurich, Switzerland - Marketing & Digital Operations Head - Europe – (Feb’16 – Aug’17) - Gum Category Lead Europe – (Mar’14 – Jan’16) - Innovation Platform Lead – Toblerone, Cadbury and Milka – (Jan’11 – Mar’14) • NESTLE MEXICO - Sr. -

Mondelez International Announces $50 Million Investment Opportunity for UK Coffee Site

November 7, 2014 Mondelez International Announces $50 Million Investment Opportunity for UK Coffee Site - Proposal coincides with Banbury coffee plant's 50th anniversary - Planned investment highlights success of Tassimo single-serve beverage system - Part of a multi-year, $1.5 billion investment in European manufacturing BANBURY, England, Nov. 7, 2014 /PRNewswire/ -- Mondelez International, the world's pre-eminent maker of chocolate, biscuits, gum and candy as well as the second largest player in the global coffee market, today announced plans to invest $50 million (£30 million) in its Banbury, UK factory to build two new lines that will manufacture Tassimo beverage capsules. Tassimo is Europe's fastest growing single-serve system, brewing a wide variety of beverages including Jacobs and Costa coffees and Cadbury hot chocolate. The decision is part of Mondelez International's multi-year investment in European manufacturing, under which $1.5 billion has been invested since 2010. The planned investment will create close to 80 roles and coincides with the 50th anniversary of the Banbury factory, which produces coffee brands such as Kenco, Carte Noire and Maxwell House. The Tassimo capsules produced in Banbury will be exported to Western European coffee markets in France and Spain as well as distributed in the UK. "Tassimo is a key driver of growth for our European coffee business, so this $50 million opportunity is a great one for Banbury," said Phil Hodges, Senior Vice President, Integrated Supply Chain, Mondelez Europe. "Over the past 18 months, we've made similar investments in Bournville and Sheffield, underscoring our commitment to UK manufacturing. -

2020 Easter Candy

2020 EASTER CANDY BOOK 1 OF 2 Orders Due Back to URM no later than September 16th, 2019 The following items are the offerings for your 2020 Easter Candy. Hershey is offering an early ship on eight of their Easter items. These can be found at the beginning of Catalog 1 and will ship to stores 12/29/19. All other items will ship 2/9/20 All orders are due to URM by September 16th, 2019. Preferred Ordering Method: Online ordering is fast, efficient, and the preferred way to order. Detailed instructions for Online ordering can be found on the Portal under Retail Kiosk/Documents/User Guides. Please read the instructions and utilize the Online ordering. Alternate Ordering Methods: Complete the separate Easter Candy order guide then scan or email to Rena Goodwin at [email protected] If you cannot utilize the first two ordering methods: orders may be faxed ATTN: Rena Goodwin 509-467-2738 We reserve the right to change prices due to typographical errors or incorrect information from vendors JANUARY Item #389324-5 Line # 1 Item #389319-5 Line # 2 Item #389320-3 Line # 3 HRSH AST CNT GDS SHIPPER 432/ASST CADBURY CARAMEL EGG 288/1.2 OZ CADBURY CHOC CRM EGG 288/1.2 OZ Net Cost:$263.24 EA .61¢ SRP: .89¢/32% Net Cost:$182.98 EA .64¢ SRP: .95¢/33% Net Cost:$182.98 EA .64¢ SRP: .95¢/33% 72 MILK CHOC BUNNIES 1.2 OZ UPC: 34000-00687 UPC: 34000-00799 UPC: 34000-00712 72 ALMOND JOY EGGS 1.1 OZ UPC: 34000-00231 180 REESES PB EGGS 1.2 OZ UPC: 34000-00475 36 KIT KAT 1.55 OZ UPC: 34000-24659 36 REESE’S WHITE CHOC PB 1.2 O Z UPC: 34000-00692 36 REESES PIECES -

Kelly Promo's

1921 - 2021 Kelly Promo’s 1921 - 2021 Kelly Promo’s SeptemberSeptember 4th 4th to to October October 1st, 1st, 2021 2021 NEW - HALLOWEEN SEASONAL CANDY NOW ON SALE! Page 23 NEW - FOOD & SNACKS Page 16 Page Page Page Page Page 15 15 33 14 5 NEWWelch’s - FruitBEVERAGES & Yogurt Tubes NEW - CANDY Gondola Topper Rack 3 SKU’s Kit #400904 $15 Semi Annual Rack Payment Total Retail: $94.50 Average Cost: $57.50 Profit Dollars: $37.00 Product Turns: 4 Incremental Dollars: $148.00 Placement Item # Description Pack Size Shelf 1 517020 Welch's Fruit 'n Yogurt-Strawberry 10 1.8 oz Dimensions: 41”W x 8”D x 13”H Shelf 2 517020Page Welch's Fruit 'n Yogurt-Strawberry 10 1.8 oz Page Page Page Page Page Shelf 3 5170037 Welch's Fruit 'n Yogurt-Blueberry 10 1.8 oz 30 31 28 25 24 Shelf 4 517011 Welch's Fruit 'n Yogurt-Mango 10 1.8 oz Shelf 5 517011 Welch's Fruit 'n Yogurt-Mango 10 1.8 oz Rack 414760 Gondola Topper Rack 3 SKU's 1 Empty NEWHalls 9- box CCS Counter RACKS Rack | Kit #516678 NEW - HBA, TOBACCO & AUTO $20 Semi Annual Rack Payment Welch’s Fruit & Yogurt Tubes Gondola Topper Rack 3 SKU’s Total Retail: $311.19 Kit #400904 Average Cost: $192.94 Profit Dollars: $118.25 $15 Semi Annual Rack Payment Product Turns: 3 Incremental Dollars: $354.75 Total Retail: $94.50 Placement Item # Description Pack Size Average Cost: $57.50 1 508586 Halls Mini S/F Menthol-Lyptus 8 24 Profit Dollars: $37.00 Peg 2 508578 Halls Mini S/F Honey Lemon 8 24 Product Turns: 3 508560 Halls Mini S/F Cherry 8 24 4 1 69698 Halls Honey Lemon 20 9 Incremental Dollars: $148.00 1st Shelf -

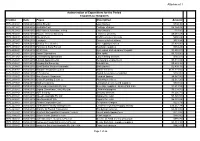

Creditor Date Payee Description Amount Authorisation Of

Authorisation of Expenditure for the Period 1/04/2015 to 30/04/2015 Creditor Date Payee Description Amount 1775.2008-01 01/04/2015 Alinta Energy Gas charges $704.30 1775.2019-01 01/04/2015 Australia Post Postage charges $5,154.29 1775.2033-01 01/04/2015 BOC Gases Australia Limited Gas charges $23.50 1775.2034-01 01/04/2015 Boyan Electrical Services Electrical services $8,681.48 1775.2049-01 01/04/2015 City Of Perth BA/DA archive retrievals $690.49 1775.2072-01 01/04/2015 Landgate Gross rental valuations $653.84 1775.2074-01 01/04/2015 Dickies Tree Service Tree lopping services $7,491.00 1775.2085-01 01/04/2015 Farinosi & Sons Pty Ltd Hardware supplies $334.22 1775.2096-01 01/04/2015 GYM Care Gym wipes and equipment repairs $1,450.91 1775.2110-01 01/04/2015 Jason Signmakers Bike racks $3,729.00 1775.2119-01 01/04/2015 Line Marking Specialists Line marking services $765.07 1775.2120-01 01/04/2015 LO-GO Appointments Temporary employment $3,318.89 1775.2126-01 01/04/2015 Mayday Earthmoving Bobcat hire $5,245.90 1775.2134-01 01/04/2015 Boral Bricks Western Australia Brick pavers $2,409.13 1775.2136-01 01/04/2015 Mindarie Regional Council Waste services $131,171.85 1775.2138-01 01/04/2015 C Economo Award for service recognition $150.00 1775.2158-01 01/04/2015 Non Organic Disposals Rubbish tipping $4,587.00 1775.2159-01 01/04/2015 Oasis Plumbing Services Plumbing services $6,517.20 1775.2189-01 01/04/2015 SAS Locksmiths Locksmith services and supplies $993.52 1775.2190-01 01/04/2015 Schweppes Australia Pty Ltd Beverage supplies - Beatty Park -

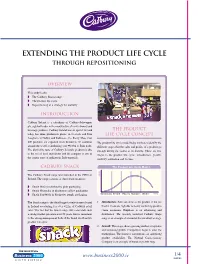

Extending the Product Life Cycle Through Repositioning

CADBURY V-5 9/8/05 1:38 PM Page 1 Extending the Product Life cycle through Repositioning Overview This study looks: ! The Cadbury Snack range ! The product life cycle ! Repositioning as a strategy for maturity introduction Cadbury Ireland is a subsidiary of Cadbury-Schweppes plc, a global leader in the manufacture of confectionery and beverage products. Cadbury Ireland was set up in 1932 and The Product today has three production plants, in Coolock and Dun Life Cycle concept Laoghaire in Dublin and Rathmore, Co. Kerry. More than 200 products are exported from Ireland to 30 countries The product life cycle model helps marketers identify the ! around the world, contributing over 110m to Irish trade. different stages that the sales and profits of a product go The distinctive taste of Cadbury Ireland’s products is due through during the course of its lifetime. There are five to the use of local ingredients and the company is one of stages to the product life cycle: introduction, growth, the largest users of indigenous Irish materials. maturity, saturation and decline. Cadbury Snack The Product Life Cycle Model The Cadbury Snack range was launched in the 1950s in SALES Ireland. The range consists of three main products: ! Snack Wafer in distinctive pink packaging ! Snack Shortcake in distinctive yellow packaging ! Snack Sandwich in distinctive purple packaging Introduction Growth Maturity Saturation Decline TIME The Snack range is the third biggest confectionery brand 1. Introduction: Sales are slow as the product is not yet in Ireland accounting for over !22m of Cadbury retail known. Costs are high due to heavy marketing spend to sales. -

Filed by Kraft Foods Inc. Pursuant to Rule 425 Under the Securities Act of 1933

Filed by Kraft Foods Inc. Pursuant to Rule 425 Under the Securities Act of 1933 Subject Company: Cadbury plc Commission File No.: 333-06444 The following information was made available by Kraft Foods Inc. to employees on February 3, 2010. Client: Cadburys BT Transcription Ref: K9081050 Date: 3rd February 2010 @ 14.00 1 Forward-looking statements This document contains forward-looking statements regarding Kraft Food’s combination with Cadbury. Such statements include, but are not limited to, statements about the benefits of the combination and other such statements that are not historical facts, which are or may be based on Kraft Foods’ plans, estimates and projections. These forward-looking statements are subject to a number of risks and uncertainties, many of which are beyond Kraft Foods’ control, that could cause Kraft Foods’ actual results to differ materially from those indicated in any such forward-looking statements. Such factors include, but are not limited to, the risk factors, as they may be amended from time to time, set forth in Kraft Foods’ filings with the US Securities and Exchange Commission (“SEC”), including the registration statement on Form S-4, as amended from time to time, filed by Kraft Foods in connection with the offer, Kraft Foods’ most recently filed Annual Report on Form 10-K and subsequent reports on Forms 10-Q and 8-K. Kraft Foods disclaims and does not undertake any obligation to update or revise any forward-looking statement in this document, except as required by applicable law or regulation. Additional US-related information This document is provided for informational purposes only and is neither an offer to purchase nor a solicitation of an offer to sell shares of Cadbury or Kraft Foods. -

Mondelez International Joins Chocolate Industry's 'Cocoaaction' Through World Cocoa Foundation

May 23, 2014 Mondelez International Joins Chocolate Industry's 'CocoaAction' Through World Cocoa Foundation - Coordinates Support from 12 Largest Global Cocoa Companies - Focuses on Boosting Supply Chain Productivity and Community Development - Complements Mondelez International's $400 Million Cocoa Life Sustainability Initiative DEERFIELD, Ill., May 23, 2014 /PRNewswire/ -- Mondelez International, the world's largest chocolate company and a proud member of the World Cocoa Foundation since 2004, is lending its support for the chocolate industry's "CocoaAction" sustainability strategy announced earlier this week during the visit by its board of directors in West Africa. CocoaAction brings together 12 of the largest companies in the cocoa industry under the World Cocoa Foundation to voluntarily coordinate and align their sustainability efforts, boost their impact and contribute to building a rejuvenated and economically viable cocoa sector. "As a founding member of the World Cocoa Foundation, we're proud to have played an active role in shaping CocoaAction," said Bharat Puri, President, Global Chocolate, Gum and Candy. "We believe in the power of major chocolate and cocoa companies working together to maximize the industry's ability to create thriving cocoa communities and help secure the future of the cocoa industry. We're pleased our signature Cocoa Life program, launched in 2012, aligns with the CocoaAction strategy, and we welcome the support from the governments of Ghana and Cote d'Ivoire for CocoaAction." Mondelez International will continue to expand its Cocoa Life sustainability program, a $400 million, 10-year effort plan based on its successful Cadbury Cocoa Partnership in Ghana, which has promoted gender equality in cocoa production since 2008. -

Portland Daily Press: July 13,1892

PORTLAND DAILY PRESS. ESTABLISHED JUNE 23, 1862—VOL. 31. PORTLAND, MAINE, WEDNESDAY MORNING, JULY 13, 1892. PRICE THREE CENTS. NEWS. MISCELLANEOUS. THIS MORNING’S bill that was every presented and hunt- ing of Messrs. Craw did O’Donnell, Coon, A TEMPERANCE TALK. ing up some who not care to make ford, Scliuckman and 1. out Clifford, represent- AWAKENED TO DIE. Page any bill, thus proving that he be- ing the Amalgamated Association advi- lieved in with Weather indications. dealing squarely all. To- sory committee and the citizens. Mr. the was Seneral Telegraphic news. day elephant captured and Coon was the spokesman. He stated hitched but when he he a. got ready, again that lie represented the association and Page the started, fastenings being insecure. the citizens. On their part he welcomed Seneral sporting news. Mr. Tells the Senate About the Again he has been found and is Frye enjoying the troops to the town and offered the co Tourists at St. Gervais news. himself in a as he would Crushed Telegraphic swamp in his operation of the citizens i n or- 3. native It is not preserving Page Maine Law. jungle. known what der. Beneath a course he will now pursue but one Glacier. History of the Pinkertons. thing General Snowden said: “I thank yov is has a live Maine towns. sure, Bucksport elephant on Provost Patrol in Place of for the welcome, but do not need its hands. y’oui Heavy warships of today. co-operation, The only way good citizen* can with' us is to Page 4. MR.