View Annual Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

PREFERENCE SHARES, NOMINAL VALUE of E2.24 PER SHARE, in the CAPITAL OF

11JUL200716232030 3JUL200720235794 11JUL200603145894 Public Offer by RFS Holdings B.V. FOR ALL OF THE ISSUED AND OUTSTANDING (FORMERLY CONVERTIBLE) PREFERENCE SHARES, NOMINAL VALUE OF e2.24 PER SHARE, IN THE CAPITAL OF ABN AMRO Holding N.V. Offer Memorandum and Offer Memorandum for ABN AMRO ordinary shares (incorporated by reference in this Offer Memorandum) 20 July 2007 This Preference Shares Offer expires at 15:00 hours, Amsterdam time, on 5 October 2007, unless extended. OFFER MEMORANDUM dated 20 July 2007 11JUL200716232030 3JUL200720235794 11JUL200603145894 PREFERENCE SHARES OFFER BY RFS HOLDINGS B.V. FOR ALL THE ISSUED AND OUTSTANDING PREFERENCE SHARES, NOMINAL VALUE OF e2.24 PER SHARE, IN THE CAPITAL OF ABN AMRO HOLDING N.V. RFS Holdings B.V. (‘‘RFS Holdings’’), a company formed by an affiliate of Fortis N.V. and Fortis SA/NV (Fortis N.V. and Fortis SA/ NV together ‘‘Fortis’’), The Royal Bank of Scotland Group plc (‘‘RBS’’) and an affiliate of Banco Santander Central Hispano, S.A. (‘‘Santander’’), is offering to acquire all of the issued and outstanding (formerly convertible) preference shares, nominal value e2.24 per share (‘‘ABN AMRO Preference Shares’’), of ABN AMRO Holding N.V. (‘‘ABN AMRO’’) on the terms and conditions set out in this document (the ‘‘Preference Shares Offer’’). In the Preference Shares Offer, RFS Holdings is offering to purchase each ABN AMRO Preference Share validly tendered and not properly withdrawn for e27.65 in cash. Assuming 44,988 issued and outstanding ABN AMRO Preference Shares outstanding as at 31 December 2006, the total value of the consideration being offered by RFS Holdings for the ABN AMRO Preference Shares is e1,243,918.20. -

Prospectus Tomtom Dated 1 July 2009

TomTom N.V. (a public company with limited liability, incorporated under Dutch law, having its corporate seat in Amsterdam, The Netherlands) Offering of 85,264,381 Ordinary Shares in a 5 for 8 rights offering at a price of €4.21 per Ordinary Share We are offering 85,264,381 new Ordinary Shares (as defined below) (the “Offer Shares”). The Offer Shares will initially be offered to eligible holders (“Shareholders”) of ordinary shares in our capital with a nominal value of €0.20 each (“Ordinary Shares”) pro rata to their shareholdings at an offer price of €4.21 each (the “Offer Price”), subject to applicable securities laws and on the terms set out in this document (the “Prospectus”) (the “Rights Offering”). For this purpose, and subject to applicable securities laws and the terms set out in this Prospectus, Shareholders as of the Record Date (as defined below) are being granted transferable subscription entitlements (“SETs”) that will entitle them to subscribe for Offer Shares at the Offer Price, provided that they are Eligible Persons (as defined below). Shareholders as of the Record Date (as defined below) and subsequent transferees of the SETs, in each case which are able to give the representations and warranties set out in “Selling and Transfer Restrictions”, are “Eligible Persons” with respect to the Rights Offering. Application has been made to admit the SETs to trading on Euronext Amsterdam by NYSE Euronext, a regulated market of Euronext Amsterdam N.V., (“Euronext Amsterdam”). Trading of the SETs on Euronext Amsterdam is expected to commence at 09:00 (Central European Time; “CET”) on 3 July 2009 and will continue until 13:00 (CET) on 13 July 2009, barring unforeseen circumstances. -

IRISH LIFE SCIENCES Directory ©Enterprise Ireland December ‘10 - (251R)

The IRISH LIFE SCIENCES Directory ©Enterprise Ireland December ‘10 - (251R) The see map underneathπ IrIsh The LIfe scIences www.enterprise-ireland.com Irish Life Sciences Directory Ireland is a globally recognised centre of excellence in the Life Sciences industry. Directory This directory highlights the opportunities open to international companies to partner and do business with world-class Irish enterprises. Funded by the Irish Government under the National Development Plan, 2007-2013 see map overleaf ∏ Irish Life Sciences Companies Donegal Roscommon Itronik Interconnect Ltd. ANSAmed Moll Industries Ireland Ltd. Wiss Medi Teo. Westmeath Arran Chemical Co Ltd. Leitrim Cavan Univet Ltd. Mayo M&V Medical Devices Ltd. Vistamed Ltd. Louth LLR-G5 Ltd Mergon Healthcare AmRay Medical Ovagen Group Ltd. Technical Engineering Bellurgan Precision Engineering Ltd. Precision Wire Components & Tooling Services Ltd. ID Technology Ltd. Trend Technologies Mullingar Ltd. Millmount Healthcare Ltd. New Era Packaging Ltd. Sligo Ovelle Ltd. Arrotek Medical Ltd. Letterkenny Derry Uniblock Ltd. Avenue Mould Solutions Ltd. Donegal iNBLEX Plastics Ltd Donegal Northern Galway ProTek Medical Ltd. Aerogen Ltd. SL Controls Ltd. Ireland Belfast Longford Anecto Ltd. Socrates Finesse Medical Ltd. APOS TopChem Laboratories Ltd. Avonmed Healthcare Ltd. TopChem Pharmaceutcals Ltd. Bio Medical Research Enniskillen Monaghan Meath BSM Ireland Ltd. Leitrim Newry ArcRoyal Ltd. Cambus Medical Sligo Monaghan Ballina Sligo Kells Stainless Ltd. Cappella Medical Devices Ltd. Cavan Carrick-on-Shannon Novachem Corporation Ltd. Caragh Precision Dundalk Cavan Offaly Chanelle Medical Castlebar Louth Chanelle Pharamaceuticals Europharma Concepts Ltd. Mayo Roscommon Manufacturing Ltd. Westport Longford Drogheda Midland Bandages Ltd. Clada Medical Devices Roscommon Steripack Medical Packaging Longford Meath Complete Laboratory Solutions Contech Ireland Dublin Athlone Creagh Medical Limited Mullingar AGI Therapeutics Plc. -

The Deity's Beer List.Xls

Page 1 The Deity's Beer List.xls 1 #9 Not Quite Pale Ale Magic Hat Brewing Co Burlington, VT 2 1837 Unibroue Chambly,QC 7% 3 10th Anniversary Ale Granville Island Brewing Co. Vancouver,BC 5.5% 4 1664 de Kronenbourg Kronenbourg Brasseries Stasbourg,France 6% 5 16th Avenue Pilsner Big River Grille & Brewing Works Nashville, TN 6 1889 Lager Walkerville Brewing Co Windsor 5% 7 1892 Traditional Ale Quidi Vidi Brewing St. John,NF 5% 8 3 Monts St.Syvestre Cappel,France 8% 9 3 Peat Wheat Beer Hops Brewery Scottsdale, AZ 10 32 Inning Ale Uno Pizzeria Chicago 11 3C Extreme Double IPA Nodding Head Brewery Philadelphia, Pa. 12 46'er IPA Lake Placid Pub & Brewery Plattsburg , NY 13 55 Lager Beer Northern Breweries Ltd Sault Ste.Marie,ON 5% 14 60 Minute IPA Dogfishhead Brewing Lewes, DE 15 700 Level Beer Nodding Head Brewery Philadelphia, Pa. 16 8.6 Speciaal Bier BierBrouwerij Lieshout Statiegeld, Holland 8.6% 17 80 Shilling Ale Caledonian Brewing Edinburgh, Scotland 18 90 Minute IPA Dogfishhead Brewing Lewes, DE 19 Abbaye de Bonne-Esperance Brasserie Lefebvre SA Quenast,Belgium 8.3% 20 Abbaye de Leffe S.A. Interbrew Brussels, Belgium 6.5% 21 Abbaye de Leffe Blonde S.A. Interbrew Brussels, Belgium 6.6% 22 AbBIBCbKE Lvivske Premium Lager Lvivska Brewery, Ukraine 5.2% 23 Acadian Pilsener Acadian Brewing Co. LLC New Orleans, LA 24 Acme Brown Ale North Coast Brewing Co. Fort Bragg, CA 25 Actien~Alt-Dortmunder Actien Brauerei Dortmund,Germany 5.6% 26 Adnam's Bitter Sole Bay Brewery Southwold UK 27 Adnams Suffolk Strong Bitter (SSB) Sole Bay Brewery Southwold UK 28 Aecht Ochlenferla Rauchbier Brauerei Heller Bamberg Bamberg, Germany 4.5% 29 Aegean Hellas Beer Atalanti Brewery Atalanti,Greece 4.8% 30 Affligem Dobbel Abbey Ale N.V. -

White Wine Glass/Bottle

White Wine Glass/Bottle Goose Beret Sauvignon Blanc 2013 €8.00/ €31.00 Marlborough, New Zealand Tbursting with ripe tropical aromas of passion fruit and guava, while the palate is full and rich with intense gooseberry and citrus flavours leading to a crisp finish Domaine Sylvain Bailly Sancerre 2013 €43.00 Loire Valley, France Classic with intense but elegant herb-sprinkled, green fruit and brisk perky acidity. Mouth-watering and tangy. Chablis Domaine Simonnet-Febvre 2011 €44.00 France A fresh vivacious style with intense floral aromas. A perfect balance, combining full generous fruit flavours with finesse and elegance. Rose Cuna de Reyes Clarete Rosé, 2013 €7.50 €28.00 D.O Rioja, Spain This is a very elegant Rosé: smooth and bright with juicy strawberry and raspberry fruit, leading to a crisp, refreshing finish. Bar of the Year 2007 City Bar 2007 & 2008 Best Bar 2007, 2009, 2010 & 2011, 2014 Crozes -Hermitage, Arnoux et Fils , 2011 The Bank’s Cocktails Rhone, France €44.00 This is a classy syrah, with savoury aromas and perfumed, smoky blackcurrant fruit with liquorice notes and delicate peppery finish. Classics and On The Rocks Chateau La Fleur Picon 2009 €48.00 The Banks Bloody Mary €10.50 Morillon, St. Emilion Grand Cru Bordeaux, France House Vodka, Lemon Juice, Tabasco Sauce, Salt and Pepper, Worchester The 12 month aging in one and two year old barrels keeps the freshness which can be enjoyed after three years of cellaring. Showing richness and Sauce, Horseradish and Tomato Juice balance of fruit and the elegance of the merlot grape. -

Heineken Holding NV 2020 Annual Report

HEINEKEN HOLDING N.V. ANNUAL REPORT 2020 2A02n0nEstablished in Amsterdamu 2 Profile Heineken Holding N.V., which holds 50.005% of the issued share capital of Heineken N.V., heads the HEINEKEN group. The object of Heineken Holding N.V. pursuant to its Articles of Association is to manage or supervise the management of the HEINEKEN group and to provide services for Heineken N.V. It seeks to promote the continuity, independence and stability of the HEINEKEN group, thereby enabling Heineken N.V. to grow in a controlled and steady manner and to pursue its long-term policy in the interest of all stakeholders. Heineken Holding N.V. does not engage in operational activities itself. These have been assigned within the HEINEKEN group to Heineken N.V. and its subsidiaries and associated companies. Heineken Holding N.V.’s income consists exclusively of dividends received on its interest in Heineken N.V. Every Heineken N.V. share held by Heineken Holding N.V. is matched by one share issued at the level of Heineken Holding N.V. The dividend payable on the two shares is identical. Heineken Holding N.V. shares are listed on Euronext Amsterdam. Page 2 This Annual Report can be downloaded from www.heinekenholding.com Heineken Holding N.V. Annual Report 2020 3 Contents Shareholder Information Board of Directors Report of the Board of Directors Financial Statements 2020 Other Information Contents 2 Profile 01 Shareholder Information 02 Report of the Board of Directors 04 Other Information 5 Heineken Holding N.V. 10 Report of the Board of Directors 74 Other information 6 Heineken N.V. -

Randstad Annual Report 2019

annual report 2019 realizing true potential. contents randstad at a glance management report governance financial statements supplementary information contents. randstad at a glance financial statements 4 key figures 2019 135 contents financial statements 6 message from the CEO 136 consolidated financial statements 8 about randstad 140 main notes to the consolidated financial statements 14 our global presence 170 notes to the consolidated income statement 15 geographic spread 174 notes to the consolidated statement of financial 16 realizing true potential position 189 notes to the consolidated statement of management report cash flows 19 how we create value 193 other notes to the consolidated financial statements 24 integrated reporting framework 200 company financial statements 26 the world around us 202 notes to the company financial statements 31 our strategy and progress 206 other information 36 our value for clients and talent 41 our value for employees supplementary information 47 our value for investors 217 financial calendar 52 our value for society 218 ten years of randstad 58 sustainability basics 220 about this report 71 performance 222 sustainable development goals 88 risk & opportunity management 223 GRI content index 227 global compact index governance 228 sustainability and industry memberships and 102 executive board partnerships 104 supervisory board 229 certifications, rankings, and awards 106 report of the supervisory board 231 highest randstad positions in industry associations 115 remuneration report 232 glossary 128 corporate governance 238 history timeline annual report 2019 2 contents randstad at a glance management report governance financial statements supplementary information randstad at a glance. 4 key figures 2019 6 message from the CEO 8 about randstad 14 our global presence 15 geographic spread 16 realizing true potential annual report 2019 3 contents randstad at a glance management report governance financial statements supplementary information key figures 2019. -

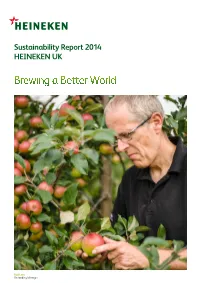

Brewing a Better World

Sustainability Report 2014 HEINEKEN UK Brewing a Better World Rod Lees Orcharding Manager Introduction The big picture Our focus areas Values and behaviours Going Forward Introduction The big picture Our focus areas Values and behaviours Going Forward Welcome to our 2014 Sustainability Report Our Values Our values represent what we stand for as a business and employer. They inspire us and are brought to life by our colleagues at every level and function and of our business. Our long-standing company values are: Jeremy Beadles Enjoyment Respect Quality Corporate Relations Director We’re committed to delighting We have respect for individuals, Our passion for quality is at the heart consumers, day in, day out, with society and the environment. of everything we do. perfect cider & beer experiences. HEINEKEN is the country’s leading cider and beer company and part of HEINEKEN N.V., the world’s most international brewer. Our brands Enjoyment Respect Quality Livingston We’re cFiorstm Pointm itted to delighting We have respect for individuals, Our passion for quaEdinbulity righs at the heart Broadway Park customer contact 342 Colleagues are known and loved across the UK and consumecentrers, day 192in C,olleagues day out, with society and the environment. of everything we dooffice. include Foster’s, Heineken®, Strongbow, perfLivingstonect cider & beer experiences. Edinburgh Caledonian Brewery Edinburgh 0.2mhl 46 Colleagues Caledonian Brewery Kronenbourg 1664, Desperados, John Smith’s Tadcaster Brewery 338 Colleagues 3.5mhl and Bulmers alongside -

Draught Lager

46 Lager Draught Lager PREMIUM DRAUGHT LAGER 4378 Asahi 5.0 11 Gall (S) CO2 6380 Hop House 13 5.0 30 Litre (A) CO2 1259 Birra Moretti 4.6 50 Litre (S) CO2 4332 Kaltenberg Royal 4.1 11 Gall (S) CO2 4222 Birra Poretti 4.8 30 Litre (S) CO2 4249 Kingfisher 4.3 30 Litre (S) CO2 4370 Bitburger Pils 4.8 11 Gall (G) CO2 4346 Kingfisher Premium 4.3 11 Gall (S) CO2 4201 Brahma 5.0 10 Gall (U) CO2 4799 Kirin Ichiban 4.6 11 Gall (S) CO2 4244 Budvar Budweiser 5.0 11 Gall (S) CO2 7003 Konig Pilsner 4.9 11 Gall (G) CO2 4420 Budweiser 4.5 11 Gall (G) CO2 4695 Kozel Czech 4.0 11 Gall (S) CO2 0333 Caledonian Coast To Coast 4.6 30 Litre (S) CO2 9736 Krombacher Pils 4.8 50 Litre (A) CO2 6661 Camden Hells Lager 4.6 30 Litre (A) CO2 4639 Kronenbourg 1664 5.0 22 Gall (S) CO2 4239 Carlsberg Export 5.0 30 Litre (S) CO2 4307 Kronenbourg 1664 5.0 11 Gall (S) CO2 4229 Carlsberg Export 5.0 11 Gall (S) CO2 4272 Leffe Blonde 6.6 20 Litre (S) CO2 4479 Chimay Gold 4.8 20 Litre (A) CO2 4216 Leffe Blonde 6.6 6 Litre (PD) CO2 4488 Cobra 4.3 11 Gall (G) CO2 4867 Löwenbrau 5.0 11 Gall (G) CO2 1352 Desperados 5.9 30 Litre (S) CO2 8199 Lucky Saint Unfiltered Lager LOW 0.5 30 Litre (S) CO2 4739 Dortmunder Pils 5.0 11 Gall (S) CO2 3603 Mahou 5.5 30 Litre (S) CO2 0445 Draught Master Angelo Poretti No9 5.9 20 Litre (DM) N/A 4223 Moretti 4.5 30 Litre (S) CO2 0449 Draught Master Brooklyn Lager 5.2 20 Litre (DM) N/A 4810 Moretti 'David' 4.6 20 Litre CO2 3209 Draught Master Carlsberg 3.8 20 Litre (DM) N/A 4524 Peroni Nastro Azzurro 5.2 11 Gall (S) CO2 0449 Draught Master Carlsberg Export -

2008 Bjcp Style Guidelines

2008 BJCP STYLE GUIDELINES Beer Judge Certification Program (BJCP) Style Guidelines for Beer, Mead and Cider 2008 Revision of the 2004 Guidelines Copyright © 2008, BJCP, Inc. The BJCP grants the right to make copies for use in BJCP-sanctioned competitions or for educational/judge training purposes. All other rights reserved. See our website www.bjcp.org for updates to these guidelines. 2003-2004 BJCP Beer Style Committee: Gordon Strong, Chairman Ron Bach Peter Garofalo Michael L. Hall Dave Houseman Mark Tumarkin 2008 Contributors: Jamil Zainasheff, Kristen England, Stan Hieronymus, Tom Fitzpatrick, George DePiro 2003-2004 Contributors: Jeff Sparrow, Alan McKay, Steve Hamburg, Roger Deschner, Ben Jankowski, Jeff Renner, Randy Mosher, Phil Sides, Jr., Dick Dunn, Joel Plutchak, A.J. Zanyk, Joe Workman, Dave Sapsis, Ed Westemeier, Ken Schramm 1998-1999 Beer Style Committee: Bruce Brode, Steve Casselman, Tim Dawson, Peter Garofalo, Bryan Gros, Bob Hall, David Houseman, Al Korzonas, Martin Lodahl, Craig Pepin, Bob Rogers 48 i ilSot...................................................17 Stout rial Impe Russian 13F. Sot..............................................................17 Stout American 13E. pdate.................................46 U 2008 T, CHAR STYLE BJCP 2004 tra Stout........................................................16 tra Ex Foreign 13D. N/A N/A N/A 5-12% 0.995-1.020 1.045-100 Perry or Cider Specialty Other D. y Cider/Perry...........................................45 y Specialt Other 28D. tu ................................................................16 Stout l Oatmea 13C. ine......................................................................44 Applew 28C. tu ....................................................................15 Stout Sweet 13B. N/A N/A N/A 9-12% 0.995-1.010 1.070-100 Wine Apple C. ie .....................................................................44 Cider Fruit 28B. 3.DySot.......................................................................15 Stout Dry 13A. N/A N/A N/A 5-9% 0.995-1.010 1.045-70 Cider Fruit B. -

2016 Sustainability Report MULTI BINTANG INDONESIA

2016 Sustainability Report MULTI BINTANG INDONESIA 1 2 2016 Sustainability Report MULTI BINTANG INDONESIA 2016 Sustainability Report MULTI BINTANG INDONESIA 3 DAFTAR ISI Content Ikhtisar Profil perusahaan Laporan manajemen highlights company management profile report 06 Informasi bagi Pemegang 13 Visi dan Misi Kami 32 Surat dari Dewan Saham Our Vision and Mission Komisaris Information For Letter from the Board of 20 Sejarah Perusahaan Shareholders Commissioners Company Milestones 07 Kronologi Pencatatan 40 Profil Dewan Komisaris 22 Struktur Organisasi Saham Profil Board of Organization Structure Chronology of Share Commissioners Listing 25 Penghargaan 2016 48 Laporan Direksi Award Received in 2016 10 Ikhtisar Data Keuangan Report of the Board of Summary of Financial 28 Peristiwa Penting 2016 Directors Data 2016 Event Highlights 58 Profil Direksi Profile of the Board of Directors 4 2016 Sustainability Report MULTI BINTANG INDONESIA Analisa dan pembahasan manajemen Tata kelola perusahaan Laporan keuangan management's corporate financial discussion and governance statements analysis 65 Tinjauan Industri 110 Struktur Tata Kelola 140 Surat Pernyataan Anggota Industry Review GCG Structures Dewan Komisaris dan Direksi tentang Tanggung 66 Tinjauan Usaha 131 Sekretaris Perusahaan Jawab atas Laporan Tahunan Operational Review Corporate Secretary 2016 90 Tinjauan Keuangan 135 Manajemen Risiko Board of Directors and Board Financial Review Risk Management of Commissioners‘ Statement 98 Tanggung Jawab Sosial regarding the Responsibility Perusahaan -

Caracterização Da Empresa

Flávia Alexandra Pedro Fernandes Licenciada em Biologia Celular e Molecular Melhoria dos indicadores microbiológicos em linhas de enchimento de cerveja em barril Dissertação para obtenção do Grau de Mestre em Tecnologia e Segurança Alimentar – Ramo Qualidade Alimentar Orientador: Professora Doutora Ana Lúcia Leitão, FCT/UNL Co-Orientador: Doutor Pedro Vicente, SCC Juri: Presidente: Doutora Benilde Simões Mendes Vogais: Doutor José Fernando Gomes Requeijo Eng.ª Maria Dulce Brás Trindade da Silva Doutora Ana Lúcia Monteiro Durão Leitão Dr. Pedro Miguel dos Reis Vicente Março 2012 Melhoria dos indicadores microbiológicos em linhas de enchimento de cerveja em barril ii Melhoria dos indicadores microbiológicos em linhas de enchimento de cerveja em barril Flávia Alexandra Pedro Fernandes Melhoria dos indicadores microbiológicos em linhas de enchimento de cerveja em barril Março 2012 iii Melhoria dos indicadores microbiológicos em linhas de enchimento de cerveja em barril “Melhoria dos indicadores microbiológicos em linhas de enchimento de cerveja em barril” Copyright ©, Flávia Alexandra Pedro Fernandes, FCT/UNL e UNL. A Faculdade de Ciências e Tecnologia e a Universidade Nova de Lisboa têm o direito, perpétuo e sem limites geográficos, de arquivar e publicar esta dissertação através de exemplares impressos reproduzidos em papel ou de forma digital, ou por qualquer outro meio conhecido ou que venha a ser inventado, e de a divulgar através de repositórios científicos e de admitir a sua cópia e distribuição com objectivos educacionais ou de investigação, não comerciais, desde que seja dado crédito ao autor e editor. iv Melhoria dos indicadores microbiológicos em linhas de enchimento de cerveja em barril AGRADECIMENTOS Foram muitas as pessoas que me apoiaram na execução deste trabalho e a quem estou profundamente grata.