Panaust 2013 Annual Review

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Profitable and Untethered March to Global Resource Dominance!

Athens Journal of Business and Economics X Y GlencoreXstrata… The Profitable and Untethered March to Global Resource Dominance! By Nina Aversano Titos Ritsatos† Motivated by the economic causes and effects of their merger in 2013, we study the expansion strategy deployment of Glencore International plc. and Xstrata plc., before and after their merger. While both companies went through a series of international acquisitions during the last decade, their merger is strengthening effective vertical integration in critical resource and commodity markets, following Hymer’s theory of internationalization and Dunning’s theory of Eclectic Paradigm. Private existence of global dominant positioning in vital resource markets, posits economic sustainability and social fairness questions on an international scale. Glencore is alleged to have used unethical business tactics, increasing corruption, tax evasion and money laundering, while attracting the attention of human rights organizations. Since the announcement of their intended merger, the company’s market performance has been lower than its benchmark index. Glencore’s and Xstrata’s economic success came from operating effectively and efficiently in markets that scare off risk-averse companies. The new GlencoreXstrata is not the same company anymore. The Company’s new capital structure is characterized by controlling presence of institutional investors, creating adherence to corporate governance and increased monitoring and transparency. Furthermore, when multinational corporations like GlencoreXstrata increase in size attracting the attention of global regulation, they are forced by institutional monitoring to increase social consciousness. When ensuring full commitment to social consciousness acting with utmost concern with regard to their commitment by upholding rules and regulations of their home or host country, they have but to become “quasi-utilities” for the global industry. -

Mineral Facilities of Asia and the Pacific," 2007 (Open-File Report 2010-1254)

Table1.—Attribute data for the map "Mineral Facilities of Asia and the Pacific," 2007 (Open-File Report 2010-1254). [The United States Geological Survey (USGS) surveys international mineral industries to generate statistics on the global production, distribution, and resources of industrial minerals. This directory highlights the economically significant mineral facilities of Asia and the Pacific. Distribution of these facilities is shown on the accompanying map. Each record represents one commodity and one facility type for a single location. Facility types include mines, oil and gas fields, and processing plants such as refineries, smelters, and mills. Facility identification numbers (“Position”) are ordered alphabetically by country, followed by commodity, and then by capacity (descending). The “Year” field establishes the year for which the data were reported in Minerals Yearbook, Volume III – Area Reports: Mineral Industries of Asia and the Pacific. In the “DMS Latitiude” and “DMS Longitude” fields, coordinates are provided in degree-minute-second (DMS) format; “DD Latitude” and “DD Longitude” provide coordinates in decimal degrees (DD). Data were converted from DMS to DD. Coordinates reflect the most precise data available. Where necessary, coordinates are estimated using the nearest city or other administrative district.“Status” indicates the most recent operating status of the facility. Closed facilities are excluded from this report. In the “Notes” field, combined annual capacity represents the total of more facilities, plus additional -

Strategy Delivery Growth

Rio Tinto 2009 Annual report Rio Tinto Financial calendar Strategy 2010 14 January Fourth quarter 2009 operations review 11 February Announcement of results for 2009 24 February Rio Tinto plc and Rio Tinto Limited shares and Rio Tinto plc ADRs quoted “ex-dividend” for 2009 fi nal dividend Delivery 26 February Record date for 2009 fi nal dividend for Rio Tinto plc shares and ADRs 2 March Record date for 2009 fi nal dividend for Rio Tinto Limited shares 11 March Plan notice date for election under the dividend reinvestment plan for the 2009 fi nal dividend 1 April Payment date for 2009 fi nal dividend to holders of Ordinary shares and ADRs Growth 15 April Annual general meeting for Rio Tinto plc 15 April First quarter 2010 operations review 22 April Annual general meeting for Rio Tinto Limited A focused and 14 July Second quarter 2010 operations review 5 August Announcement of half year results for 2010 integrated strategy 11 August Rio Tinto plc and Rio Tinto Limited shares and Rio Tinto plc ADRs quoted “ex-dividend” for 2010 interim dividend 13 August Record date for 2010 interim dividend for Rio Tinto plc shares and ADRs 17 August Record date for 2010 interim dividend for Rio Tinto Limited shares Excellence in 18 August Plan notice date for election under the dividend reinvestment plan for the 2010 interim dividend 9 September Payment date for 2010 interim dividend to holders of Ordinary shares and ADRs operational delivery 14 October Third quarter 2010 operations review 2011 Positioned for growth January Fourth quarter 2010 operations review February Announcement of results for 2010 Useful information and contacts Registered offi ces Investor Centre Rio Tinto Limited Rio Tinto plc To fi nd out more about Investor Centre, go to Computershare Investor Services Pty Limited 2 Eastbourne Terrace www.investorcentre.co.uk/riotinto GPO Box 2975 London Holders of Rio Tinto American Melbourne W2 6LG Depositary Receipts (ADRs) Victoria 3001 Registered in England No. -

BHP: Fine Words, Foul Play 23 September 2020 Introduction

BHP: fine words, foul play 23 September 2020 Introduction BHP presents itself, and is often considered by investors, as the very model of a modern mining company. Not only does it present itself as socially and environmentally responsible but now as indispensable in the efforts to save the world from climate catastrophe. Given the impacts and potential impacts of its Australian operations on Aboriginal sites and the furore over Rio Tinto’s destruction of the Juukan Gorge site earlier this year, perhaps BHP will begin to tread more carefully. It certainly needs to. This briefing summarises concerns around current and planned operations in which BHP is involved in Brazil, Chile, Colombia, Peru and the USA. LMN and our member groups work with communities or partner organisations in these five countries. Concerns include ecological and social impacts, violation of indigenous rights, mining waste disposal and the financing of clean- up. Other matters of current concern are briefly noted. At the end of the briefing are reports on three legacy cases - in Papua New Guinea, Indonesia and Colombia - where BHP pulled out, leaving others to deal with the environmental destruction and social dislocation caused by its operations. LMN exists to work in solidarity with communities harmed by companies linked to London, including BHP, the world’s largest mining corporation. This briefing is intended to encourage those who finance the company to use that finance to force change, and members of the public to join us in support of communities in the frontline of the struggle to defend their rights and the integrity of the planet’s ecosystems. -

Chapter 8: Colombia

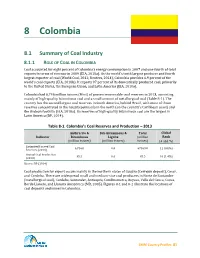

8 Colombia 8.1 Summary of Coal Industry 8.1.1 ROLE OF COAL IN COLOMBIA Coal accounted for eight percent of Colombia’s energy consumption in 2007 and one-fourth of total exports in terms of revenue in 2009 (EIA, 2010a). As the world’s tenth largest producer and fourth largest exporter of coal (World Coal, 2012; Reuters, 2014), Colombia provides 6.9 percent of the world’s coal exports (EIA, 2010b). It exports 97 percent of its domestically produced coal, primarily to the United States, the European Union, and Latin America (EIA, 2010a). Colombia had 6,746 million tonnes (Mmt) of proven recoverable coal reserves in 2013, consisting mainly of high-quality bituminous coal and a small amount of metallurgical coal (Table 8-1). The country has the second largest coal reserves in South America, behind Brazil, with most of those reserves concentrated in the Guajira peninsula in the north (on the country’s Caribbean coast) and the Andean foothills (EIA, 2010a). Its reserves of high-quality bituminous coal are the largest in Latin America (BP, 2014). Table 8-1. Colombia’s Coal Reserves and Production – 2013 Anthracite & Sub-bituminous & Total Global Indicator Bituminous Lignite (million Rank (million tonnes) (million tonnes) tonnes) (# and %) Estimated Proved Coal 6,746.0 0.0 67469.0 11 (0.8%) Reserves (2013) Annual Coal Production 85.5 0.0 85.5 10 (1.4%) (2013) Source: BP (2014) Coal production for export occurs mainly in the northern states of Guajira (Cerrejón deposit), Cesar, and Cordoba. There are widespread small and medium-size coal producers in Norte de Santander (metallurgical coal), Cordoba, Santander, Antioquia, Cundinamarca, Boyaca, Valle del Cauca, Cauca, Borde Llanero, and Llanura Amazónica (MB, 2005). -

Copper and Its Electrifying Future 19

SECTOR BRIEFING number DBS Asian Insights DBS Group61 Research • October 2018 Copper And Its Electrifying Future 19 DBS Asian Insights SECTOR BRIEFING 61 02 Copper And Its Electrifying Future Eun Young LEE Equity Analyst [email protected] Yi Seul SHIN Equity Analyst [email protected] Special thanks to Rachel Miu for her contribution to the report Produced by: Asian Insights Office • DBS Group Research go.dbs.com/research @dbsinsights [email protected] Goh Chien Yen Editor-in-Chief Martin Tacchi Art Editor 19 DBS Asian Insights SECTOR BRIEFING 61 03 04 Executive Summary 06 Introduction 12 Bullish on Long Term Copper Prices 18 Copper Demand’s New Growth Path Over the Next Decade 27 Electrifying Society: A Key Driver of Copper Demand 42 Copper Supply Lagging Demand 50 Appendix I Global Copper Sector Value Chain 52 Appendix II China Copper Sector Value Chain 53 Appendix III Top copper mines and refiners DBS Asian Insights SECTOR BRIEFING 61 04 Executive Summary opper is set for an electrifying future. Already the metal of choice wherever electricity is needed, copper is to experience demand at growth rates not seen in previous decades, as the world moves towards the electrification of energy. In particular, the Celectrification of transportation will be a mega-trend. Electric vehicles use copper more intensely than internal combustion engine vehicles (ICEVs) – a battery-powered electric vehicle contains four times as much copper as an ICEV (80kg versus 20kg). Renewable energy also uses significantly more copper per megawatt hour of power generated than for coal or nuclear power. With the electrification of energy, we expect demand for electricity to outstrip the growth in total primary energy demand going forward. -

Metals & Mining Sector Profile

Metals & Mining Sector Profile Overview The Metals & Mining sector is the largest industry sector by number of companies with over 650 involved in mineral exploration, development and production in over 100 countries. The sector comprises several of the world’s largest diversified resource companies, including global giants such as BHP Billiton and Rio Tinto, as well as a representation of potential future industry leaders in the mid-tier producers and junior miners. The sector has always been reliant on equity markets to provide the funding required for the capital intensive development of mineral projects or the funding of higher risk exploration to locate new deposits. Investors in the Australian market have supported over 290 new junior resource floats since 2009. Reasons to list Metals & Mining companies S&P/ASX 200 v S&P/ASX 300 Metals & Mining on ASX 175 • Access to capital: 150 – A global market with a wide range of institutional and retail investors 125 – Australia has the 6th largest pool of investment assets in the l world and the largest in Asia* 100 Leve • A natural destination for international mining capital - 75 a developed market in one of the world’s major mining regions Index 50 • Peer Group: list alongside key industry players • Opportunities for SMEs: a broad service offering for early 25 stage and mature companies 0 7 7 9 8 1 7 3 * Source: Austrade, Investment Company Institute, Worldwide Mutual Fund 4 Jul 1 Jul 1 Jul 1 Jul 15 Jul 12 Jul 16 Jul 1 Jul 10 Jan 11 Jul 0 Jul 0 Jan 17 Jan 13 Jan 15 Jul 0 Jan 12 Jan 16 Jan -

ETO Listing Dates As at 11 March 2009

LISTING DATES OF CLASSES 03 February 1976 BHP Limited (Calls only) CSR Limited (Calls only) Western Mining Corporation (Calls only) 16 February 1976 Woodside Petroleum Limited (Delisted 29/5/85) (Calls only) 22 November 1976 Bougainville Copper Limited (Delisted 30/8/90) (Calls only) 23 January 1978 Bank N.S.W. (Westpac Banking Corp) (Calls only) Woolworths Limited (Delisted 23/03/79) (Calls only) 21 December 1978 C.R.A. Limited (Calls only) 26 September 1980 MIM Holdings Limited (Calls only) (Terminated on 24/06/03) 24 April 1981 Energy Resources of Aust Ltd (Delisted 27/11/86) (Calls only) 26 June 1981 Santos Limited (Calls only) 29 January 1982 Australia and New Zealand Banking Group Limited (Calls only) 09 September 1982 BHP Limited (Puts only) 20 September 1982 Woodside Petroleum Limited (Delisted 29/5/85) (Puts only) 13 October 1982 Bougainville Copper Limited (Delisted 30/8/90) (Puts only) 22 October 1982 C.S.R. Limited (Puts only) 29 October 1982 MIM Holdings Limited (Puts only) Australia & New Zealand Banking Group Limited (Puts only) 05 November 1982 C.R.A. Limited (Puts only) 12 November 1982 Western Mining Corporation (Puts only) T:\REPORTSL\ETOLISTINGDATES Page 1. Westpac Banking Corporation (Puts only) 26 November 1982 Santos Limited (Puts only) Energy Resources of Aust Limited (Delisted 27/11/86) (Puts only) 17 December 1984 Elders IXL Limited (Changed name - Foster's Brewing Group Limited 6/12/90) 27 September 1985 Queensland Coal Trust (Changed name to QCT Resources Limited 21/6/89) 01 November 1985 National Australia -

The Resolution Copper Deposit, a Deep, High-Grade Porphyry Copper Deposit in the Superior District, Arizona

See discussions, stats, and author profiles for this publication at: https://www.researchgate.net/publication/283908508 THE RESOLUTION COPPER DEPOSIT, A DEEP, HIGH-GRADE PORPHYRY COPPER DEPOSIT IN THE SUPERIOR DISTRICT, ARIZONA Conference Paper · April 2003 CITATIONS READS 2 767 6 authors, including: Ken Krahulec Utah Geological Survey 20 PUBLICATIONS 15 CITATIONS SEE PROFILE All content following this page was uploaded by Ken Krahulec on 16 November 2015. SCAT001570 The user has requested enhancement of the downloaded file. THE RESOLUTION COPPER DEPOSIT, A DEEP, HIGH-GRADE PORPHYRY COPPER DEPOSIT IN THE SUPERIOR DISTRICT, ARIZONA Geoff Ballantyne, Tim Marsh, Carl Hehnke, Dave Andrews, Amy Eichenlaub & Ken Krahulec Kennecott Exploration Company THIS PAPER WAS PRESENTED AT THE MARCO T. EINAUDI SYMPOSIUM, SOCIETY OF ECONOMIC GEOLOGISTS STUDENT CHAPTER, COLORADO SCHOOL OF MINES, GOLDEN, CO; A CONFERENCE (MARCOFEST) HELD AT THE COLORADO SCHOOL OF MINES ON APRIL 3 AND 4, 2003. INTRODUCTION Manske and Paul (2002) described a recently discovered, deep, high-grade porphyry copper deposit in the Superior (Pioneer) district of Arizona. Their description, written after just five core holes had intersected an apparently coherent zone of >1% Cu mineralization, provides a remarkably complete picture of the upper parts of the mineralized system. Following initial drilling, which was carried out by Magma Copper Company and by BHP, Kennecott secured an option to earn a 55% interest in the copper deposit through further exploration expenditures. The deposit was named the Resolution deposit and a program of deep surface drilling commenced in July 2001. Since that time 17 additional deep core holes have been completed, most of them to depths of more than 2000m. -

Big Business in Twentieth-Century Australia

CENTRE FOR ECONOMIC HISTORY THE AUSTRALIAN NATIONAL UNIVERSITY SOURCE PAPER SERIES BIG BUSINESS IN TWENTIETH-CENTURY AUSTRALIA DAVID MERRETT UNIVERSITY OF MELBOURNE SIMON VILLE UNIVERSITY OF WOLLONGONG SOURCE PAPER NO. 21 APRIL 2016 THE AUSTRALIAN NATIONAL UNIVERSITY ACTON ACT 0200 AUSTRALIA T 61 2 6125 3590 F 61 2 6125 5124 E [email protected] https://www.rse.anu.edu.au/research/centres-projects/centre-for-economic-history/ Big Business in Twentieth-Century Australia David Merrett and Simon Ville Business history has for the most part been dominated by the study of large firms. Household names, often with preserved archives, have had their company stories written by academics, journalists, and former senior employees. Broader national studies have analysed the role that big business has played in a country’s economic development. While sometimes this work has alleged oppressive anti-competitive behaviour, much has been written from a more positive perspective. Business historians, influenced by the pioneering work of Alfred Chandler, have implicated the ‘visible hand’ of large scale enterprise in national economic development particularly through their competitive strategies and modernised governance structures, which have facilitated innovation, the integration of national markets, and the growth of professional bureaucracies. While our understanding of the role of big business has been enriched by an aggregation of case studies, some writers have sought to study its impact through economy-wide lenses. This has typically involved constructing sets of the largest 100 or 200 companies at periodic benchmark years through the twentieth century, and then analysing their characteristics – such as their size, industrial location, growth strategies, and market share - and how they changed over time. -

The Coming Copper Peak

NEWSNEWSFOCUSFOCUS on March 28, 2017 The Coming Copper Peak http://science.sciencemag.org/ Production of the vital metal will top out and decline within decades, according to a new model that may hold lessons for other resources IF ELECTRONS ARE THE LIFEBLOOD OF A even if copper is more abundant than most per from the earth has always come to the Downloaded from modern economy, copper makes up its blood geologists believe. That would drive prices rescue before, he notes, so he expects a much- vessels. In cables, wires, and contacts, cop- sky-high, trigger increased recycling, delayed peak that businesses and consumers per is at the core of the electrical distribu- and force inferior substitutes for copper will comfortably accommodate by recycling tion system, from power stations to the deli- on the marketplace. more copper and using copper substitutes. cate electronics that can display this page of Predicting when production of any nat- The copper debate could foreshadow Science. A small car has 20 kilograms of ural resource will peak is fraught with un- others. The team is applying its depletion copper in everything from its starter motor certainty. Witness the running debate over model to other mineral resources, from to the radiator; hybrid cars have twice that. when world oil production will peak (Science, oil to lithium, that also face exponentially But even in the face of exponentially rising 3 February 2012, p. 522). And the early recep- escalating demands on a depleting resource. consumption—reaching 17 million metric tion of the copper forecast is mixed. The work tons in 2012—miners have for 10,000 years gives “a pretty good idea that likely we’ll get So far, so good met the world’s demand for copper. -

Newcrest Mining Concise Annual Report 2007

Newcrest Mining Concise Annual Report 2007 Newcrest Mining Limited ABN 20 005 683 625 Concise Annual Report 2007 Corporate Directory Newcrest is a leading gold and copper producer. It provides investors with an exposure to large, low-cost, long life and Investor Information Share Registry Other Offi ces small, high margin gold and copper mines. Registered and Principal Offi ce Link Market Services Limited Brisbane Newcrest Mining Limited Level 9 Exploration Offi ce It aims to be in the lowest quartile for costs. Level 9 333 Collins Street Newcrest Mining Limited 600 St Kilda Road Melbourne, Victoria 3000 Level 2 Newcrest has technical skills and mining Melbourne, Victoria 3004 Australia 349 Coronation Drive Australia Postal Address Milton, Queensland 4064 Telephone: +61 (0)3 9522 5333 Locked Bag A14 Australia experience to deliver strong fi nancial returns Facsimile: +61 (0)3 9525 2996 Sydney South, New South Wales 1235 Telephone: +61 (0)7 3858 0858 Email: Australia Facsimile: +61 (0)7 3217 8233 and growth through exploration success. [email protected] Telephone: 1300 554 474 Internet: www.newcrest.com.au Perth +61 (0)2 8280 7111 Exploration Offi ce & Its vision is to be the ‘Miner of Choice’. Company Secretary Facsimile: +61 (0)2 9287 0303 Telfer Project Group Bernard Lavery +61 (0)2 9287 0309* Newcrest Mining Limited Level 9 *For faxing of Proxy Forms only. Hyatt Business Centre Social responsibility, safety and sustainability 600 St Kilda Road Email: Level 2 Melbourne, Victoria 3004 [email protected] 30 Terrace Road are the fundamental guideposts to that vision. Australia Internet: www.linkmarketservices.com.au East Perth, Western Australia 6004 Telephone: +61 (0)3 9522 5371 ADR Depositary Australia Facsimile: +61 (0)3 9521 3564 Telephone: +61 (0)8 9270 7070 Email: [email protected] BNY – Mellon Shareowner Services Investor Services Facsimile: +61 (0)8 9221 7340 Stock Exchange Listings P.O.