El Título Va Aquí

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

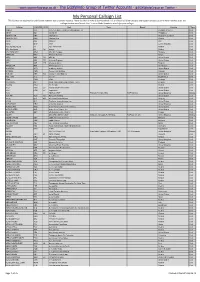

My Personal Callsign List This List Was Not Designed for Publication However Due to Several Requests I Have Decided to Make It Downloadable

- www.egxwinfogroup.co.uk - The EGXWinfo Group of Twitter Accounts - @EGXWinfoGroup on Twitter - My Personal Callsign List This list was not designed for publication however due to several requests I have decided to make it downloadable. It is a mixture of listed callsigns and logged callsigns so some have numbers after the callsign as they were heard. Use CTL+F in Adobe Reader to search for your callsign Callsign ICAO/PRI IATA Unit Type Based Country Type ABG AAB W9 Abelag Aviation Belgium Civil ARMYAIR AAC Army Air Corps United Kingdom Civil AgustaWestland Lynx AH.9A/AW159 Wildcat ARMYAIR 200# AAC 2Regt | AAC AH.1 AAC Middle Wallop United Kingdom Military ARMYAIR 300# AAC 3Regt | AAC AgustaWestland AH-64 Apache AH.1 RAF Wattisham United Kingdom Military ARMYAIR 400# AAC 4Regt | AAC AgustaWestland AH-64 Apache AH.1 RAF Wattisham United Kingdom Military ARMYAIR 500# AAC 5Regt AAC/RAF Britten-Norman Islander/Defender JHCFS Aldergrove United Kingdom Military ARMYAIR 600# AAC 657Sqn | JSFAW | AAC Various RAF Odiham United Kingdom Military Ambassador AAD Mann Air Ltd United Kingdom Civil AIGLE AZUR AAF ZI Aigle Azur France Civil ATLANTIC AAG KI Air Atlantique United Kingdom Civil ATLANTIC AAG Atlantic Flight Training United Kingdom Civil ALOHA AAH KH Aloha Air Cargo United States Civil BOREALIS AAI Air Aurora United States Civil ALFA SUDAN AAJ Alfa Airlines Sudan Civil ALASKA ISLAND AAK Alaska Island Air United States Civil AMERICAN AAL AA American Airlines United States Civil AM CORP AAM Aviation Management Corporation United States Civil -

Monthly OTP July 2019

Monthly OTP July 2019 ON-TIME PERFORMANCE AIRLINES Contents On-Time is percentage of flights that depart or arrive within 15 minutes of schedule. Global OTP rankings are only assigned to all Airlines/Airports where OAG has status coverage for at least 80% of the scheduled flights. Regional Airlines Status coverage will only be based on actual gate times rather than estimated times. This July result in some airlines / airports being excluded from this report. If you would like to review your flight status feed with OAG pleas [email protected] MAKE SMARTER MOVES Airline Monthly OTP – July 2019 Page 1 of 1 Home GLOBAL AIRLINES – TOP 50 AND BOTTOM 50 TOP AIRLINE ON-TIME FLIGHTS On-time performance BOTTOM AIRLINE ON-TIME FLIGHTS On-time performance Airline Arrivals Rank No. flights Size Airline Arrivals Rank No. flights Size SATA International-Azores GA Garuda Indonesia 93.9% 1 13,798 52 S4 30.8% 160 833 253 Airlines S.A. XL LATAM Airlines Ecuador 92.0% 2 954 246 ZI Aigle Azur 47.8% 159 1,431 215 HD AirDo 90.2% 3 1,806 200 OA Olympic Air 50.6% 158 7,338 92 3K Jetstar Asia 90.0% 4 2,514 168 JU Air Serbia 51.6% 157 3,302 152 CM Copa Airlines 90.0% 5 10,869 66 SP SATA Air Acores 51.8% 156 1,876 196 7G Star Flyer 89.8% 6 1,987 193 A3 Aegean Airlines 52.1% 155 5,446 114 BC Skymark Airlines 88.9% 7 4,917 122 WG Sunwing Airlines Inc. -

IMPORTANCIA DE LAS LÍNEAS AÉREAS EN EL SECTOR TURISMO DE MÉXICO Cecilia García Muñoz Aparicio1 Universidad Juárez Autónoma De Tabasco [email protected]

Journal of Tourism and Heritage Research (2019), vol , nº 1, pp. 220-234. García Muñoz C. “Importance of aerial lines in the México tourism sector” IMPORTANCIA DE LAS LÍNEAS AÉREAS EN EL SECTOR TURISMO DE MÉXICO Cecilia García Muñoz Aparicio1 Universidad Juárez Autónoma de Tabasco [email protected] Resumen El turismo hoy en día es una actividad que aporta al crecimiento económico ya que de acuerdo con la Cámara Nacional de Aerotransportes (2017) el número de pasajeros se incrementó 10.7%, pasando de 73.2 millones de pasajeros en 2015 a poco más de 82 millones de pasajeros en 2016, incremento que de acuerdo con la disminución de los precios de los boletos de avión. En México el transporte genera actividades como el traslado de personas, animales, mercancías y equipo. El objetivo del trabajo es conocer la importancia de las líneas aéreas en el desarrollo del Turismo. La metodología utilizada es de tipo descriptivo explicativo para medir el fenómeno a través de fuentes secundarias. Como resultado existen empresas de capital nacional posicionadas en el mercado como Aeroméxico, interjet, Viva Aerobús, Volaris, Aeromar, Mayair y TAR entre otras, mismas que contribuyen al desarrollo y crecimiento económico del país a través de la generación de más de un millón de empleos y su aportación al producto interno bruto. Palabras clave: empresa, líneas aéreas, turismo. 1 Universidad Juárez Autónoma de Tabasco, [email protected] 220 Journal of Tourism and Heritage Research (2019), vol , nº 1, pp. 220-234. García Muñoz C. “Importance of aerial lines in the México tourism sector” IMPORTANCE OF AERIAL LINES IN THE MEXICO TOURISM SECTOR Summary Tourism today is an activity that contributes to economic growth because according to the National Air Transportation Chamber (2017) the number of passengers increased 10.7%, from 73.2 million passengers in 2015 to just over 82 million passengers in 2016, increase that according to the decrease in the prices of airline tickets. -

World Airliner Census 2015

WORLD AIRLINER CENSUS EXPLANATORY NOTES This census data covers all commercial jet and parentheses in the right-hand column. excluded, unless a confirmed end-user is known – in turboprop-powered transport aircraft in service or on On the Ascend database, an airliner is defined as which case the aircraft is shown against the airline firm order with airlines worldwide, excluding aircraft being “in service” if it is “active” (in other words concerned. Operators’ fleets include leased aircraft. that carry fewer than 14 passengers or equivalent accumulating flying hours). An aircraft is classified as cargo. It records the fleets of Western, Chinese-built “parked” if it is known to be inactive – for example, if and Russia/CIS/Ukraine-built airliners. it is grounded because of airworthiness requirements The tables have been compiled by Flightglobal or in storage – and when flying hours for three Abbreviations Insight using Flightglobal’s Ascend Fleets database. consecutive months are reported as zero. Aircraft AR: advance range (Embraer 170/190/195) The information is correct up to July 2015 and undergoing maintenance or awaiting conversion are C: combi or convertible excludes non-airline operators, such as leasing also counted as being parked. ER: extended range companies and the military. Aircraft are listed in The region is dictated by operator base and does ERF: extended range freighter (747 and 767) alphabetical order, first by manufacturer and then type. not necessarily indicate the area of operation. F: freighter Operators are listed by region, with any aircraft variant Options and letters of intent (where a firm contract LR: long range in brackets next to the operator’s name. -

367 Partenaires Trouvés. Vérifiez La Disponibilitédansvotre Marché

367 partenaires trouvés. Vérifiez la disponibilitédansvotre marché. Veuillez utiliser Quick Check sur www.hahnair.com/quickcheck avant d'émettre le billet P4 Air Peace BG Biman Bangladesh Airl… T3 Eastern Airways 7C Jeju Air HR-169 HC Air Senegal NT Binter Canarias MS Egypt Air JQ Jetstar Airways A3 Aegean Airlines JU Air Serbia 0B Blue Air LY EL AL Israel Airlines 3K Jetstar Asia EI Aer Lingus HM Air Seychelles BV Blue Panorama Airlines EK Emirates GK Jetstar Japan AR Aerolineas Argentinas VT Air Tahiti OB Boliviana de Aviación E7 Equaflight BL Jetstar Pacific Airlines VW Aeromar TN Air Tahiti Nui TF Braathens Regional Av… ET Ethiopian Airlines 3J Jubba Airways AM Aeromexico NF Air Vanuatu 1X Branson AirExpress EY Etihad Airways HO Juneyao Airlines AW Africa World Airlines UM Air Zimbabwe SN Brussels Airlines 9F Eurostar RQ Kam Air 8U Afriqiyah Airways SB Aircalin FB Bulgaria Air BR EVA Air KQ Kenya Airways AH Air Algerie TL Airnorth VR Cabo Verde Airlines FN fastjet KE Korean Air 3S Air Antilles AS Alaska Airlines MO Calm Air FJ Fiji Airways KU Kuwait Airways KC Air Astana AZ Alitalia QC Camair-Co AY Finnair B0 La Compagnie UU Air Austral NH All Nippon Airways KR Cambodia Airways FZ flydubai LQ Lanmei Airlines BT Air Baltic Corporation Z8 Amaszonas K6 Cambodia Angkor Air XY flynas QV Lao Airlines KF Air Belgium Z7 Amaszonas Uruguay 9K Cape Air 5F FlyOne LA LATAM Airlines BP Air Botswana IZ Arkia Israel Airlines BW Caribbean Airlines FA FlySafair JJ LATAM Airlines Brasil 2J Air Burkina OZ Asiana Airlines KA Cathay Dragon GA Garuda Indonesia -

The ANKER Report 67 (19 Apr 2021) (Pdf) Download

Issue 67 Monday 19 April 2021 www.anker-report.com Contents Q1 was bad, but COVID data trends 1 Q1 was a disaster, Q2 just as bad? 2 Analysis: April 2021 capacity 3 Trends: Europe-Morocco suggest Q2 may not be much better 4 Airline: Pegasus Airlines With a fairly disastrous Q1 out of the way, Europe’s airlines and Paris airports. One year on from the start of the pandemic it is 6 91 new European routes analysed airports are now facing up to the fact that Q2 is not going to be doubtful whether any airlines or airports in western Europe had 9 New airline: Flyr much better. The vaccine roll out across Europe has not gone as envisaged such an extreme scenario. 10 Country: Croatia quickly, or as smoothly, as hoped, with doubts being cast on The exceptions, as might be expected, were airports in Russia, 12 Mini airport profiles of Cluj-Napoca the safety of at least one of the vaccines, resulting in it being Turkey and Ukraine. Figures for Moscow’s main airports are not in Romania, Mineralnye Vody in withdrawn from some countries or from some age groups. yet available. However, in February, Sheremetyevo was at 40% Russia and Toulon in France UK leads way but May travel resumption still not confirmed of its 2020 demand, Vnukuvo was at over 70% and Domodedovo was at 80%. Thanks to a surge in Russian 13 Airport: Turin Somewhat unexpectedly, the UK appears to have benefitted domestic tourism, Sochi/Adler on the Black Sea even reported 14 North America and 100+ new routes from leaving the EU in this regard and is leading the way in vaccinations. -

Guadalupe Gómez: Ejemplar Trayectoria En Marriott

ABR 05 2014 menos pág 20 y 21_FORMATO CORRECTO 31/03/14 08:11 Página 1 Guadalupe Gómez: Ejemplar Trayectoria en Marriott uadalupe Gómez, solamente brillante y eficiente, Directora Senior de la sino de tal constancia y Organización Global fidelidad a la compañía en que de Ventas de Marriott en labora desde hace 31 años, que México, es una ejecutiva no G VAYA A LA PAGINA 20 FUNDADOR DIRECTOR GERENTE FORTINO IBARRA EDGAR IBARRA SCHAUFELBERGER NUM. 1067 VOL. 70 AÑO 45 MÉXICO D.F. 5 DE ABRIL DE 2014 Ubicación Privilegiada de los Cinco Hoteles del Aeropuerto de la Ciudad de México o se encuentran en kilómetros de la Plaza del Constitución, 4,1 kilómetros Reforma, tampoco en Ejecutivo, 6,3 kilómetros del del Bosque de Aragón, 16,9 el centro de la ciudad Autodromo Hermanos kilómetros del Zoológico de ni en la creciente zona de Santa Rodríguez, 6,4 kilómetros del Chapultepec, 12,9 kilómetros NFe, sin embargo los cinco Palacio de los Deportes y el del World Trade Center, 16,6 hoteles del aeropuerto, por estar Foro Sol, 15 kilómetros de la kilómetros del Auditorio en donde están, ofrecen una Arena Ciudad de México, 20,2 Nacional, 13,9 kilómetros del ubicación privilegiada, kilómetros del Hipódromo de Ángel de la Independencia, excelente y de fácil acceso a las Américas, 20,2 kilómetros 30,7 kilómetros de Six Flags, muchos lugares de la gran del Estadio Azteca, 7,7 15,9 kilómetros de Coyoacán, capital mexicana. A 1,2 kilómetros de la Plaza de la 12,3 kilómetros de la Torre Latinoamericana, 18,4 kilómetros de Santa Fe y 23,8 Chic Outlet, Excelente Opción de Lupita Gómez, con más de 30 años en Marriott, es reconocida y kilómetros de Xochimilco. -

Analyzing the Online Reputation and Positioning of Airlines

sustainability Article Analyzing the Online Reputation and Positioning of Airlines Ayat Zaki Ahmed and Manuel Rodríguez-Díaz * Department of Economics and Business, University of Las Palmas de Gran Canaria, 35001 LasPalmas, Spain; [email protected] * Correspondence: [email protected]; Tel.: +34-928-452-805 Received: 18 December 2019; Accepted: 1 February 2020; Published: 6 February 2020 Abstract: The aim of this study is to propose a methodology to define the positioning of airlines in terms of their online reputation measured with quantitative variables and applied in the airline industry. Reviews shared on the Internet give key information about service quality and value as perceived by customers. To carry out the empirical study, we obtained the information available on TripAdvisor about airlines in Europe, the USA, Canada, and other countries in America, differentiating also between airlines that follow a low-cost strategy and those that do not apply it. The results show that there is a significant difference in key service quality variables between airlines in the different geographical areas studied on the one hand, and the low-cost strategy applied on the other. The variables to be used to conduct the positioning analysis in the airlines are determined. They also show that the methodology has relevant practical implications and provides tools to further develop research related to the online reputation and strategic positioning of airlines. Keywords: online reputation; airlines; market positioning; customer value; service quality; online customer review 1. Introduction Customers’ ratings of a product, service, or brand through different social media on the Internet constitute its online reputation [1–4]. -

¿Boxeo O Artes Marciales Mixtas? Boxing, Or

En portada: Ixtapa-Zihuatanejo Dirección General On the cover: Bernardo N. Illanez Cámara Ixtapa-Zihuatanejo Dirección Comercial Irma Sugey Hernández Torres Asistente Dirección General Luz Beatriz Huerta Quijano Contenido y Corrección Bernardo Illanez Solis Diseño Gráfico Andrea Rebeca Ontiveros González Traducción Aaron Covaliu Olechnowicz Colaboradores Levy Barragán Susana Pagano Agustín Zepeda Figueroa Bernardo Illanez Solis Club La Loma S.L.P. Dr. Roberto Carlos González García OCV Ixtapa Consejo Editorial Tar Rodrigo Vásquez Colmenares Guzmán Luis Eduardo Castellanos Aldana José Gil Calzadías Carvajal Denise Foulkes Pieck Star News es una revista de publicación mensual. Ésta se encuentra en todos los vuelos de “TAR Aerolíneas” quienes, hasta el día de hoy, atienden en promedio a más de 10,000 pasajeros por mes, en sus diversos destinos. Esto garantiza que la publicidad en la revista “Star News” es el mejor medio de difusión. Además de ser distribuida en los vuelos, Star News se encontrará en las varias agencias, aeropuertos y establecimientos en los que la aerolínea opera o tiene convenio. Ésta es una revista de lectura rápida, redactada en los idiomas español e ingles y que maneja contenido turístico, social, deportivo, entre otros. INDEX INDICE 06 28 50 EL REBOZO GOLF SALUD THE REBOZO HEALTH 10 32 54 TEATRO GENTE TAR CLUB CASABLANCA THEATRE TAR CREW 16 34 59 IXTAPA DESTINO ZIHUATANEJO MUJER DEPORTES DESTINATION WOMAN SPORTS 24 38 64 LITERATURA MUSICA DAVID BOWIE LITERATURE MUSIC 26 42 70 ODIN VINO CELEBRIDAD DUPEYRON UNAQ WINE CELEBRITY VENTAS: (442) 270 9040 Email: [email protected] starnewsmx www.starnews.mx La patita, con canasta y con rebozo de bolita. -

My Personal Callsign List This List Was Not Designed for Publication However Due to Several Requests I Have Decided to Make It Downloadable

- www.egxwinfogroup.co.uk - The EGXWinfo Group of Twitter Accounts - @EGXWinfoGroup on Twitter - My Personal Callsign List This list was not designed for publication however due to several requests I have decided to make it downloadable. It is a mixture of listed callsigns and logged callsigns so some have numbers after the callsign as they were heard. Use CTL+F in Adobe Reader to search for your callsign Callsign ICAO/PRI IATA Unit Type Based Country Type AASCO KAA Asia Aero Survey and Consulting Engineers Republic of Korea Civil ABAIR BOI Aboitiz Air Philippines Civil ABAKAN AIR NKP Abakan Air Russian Federation Civil ABAKAN-AVIA ABG Abakan-Avia Russia Civil ABAN ABE Aban Air Iran Civil ABAS MRP Abas Czech Republic Civil ABC AEROLINEAS AIJ ABC Aerolíneas Mexico Civil ABC Aerolineas AIJ 4O Interjet Mexico Civil ABC HUNGARY AHU ABC Air Hungary Hungary Civil ABERDAV BDV Aberdair Aviation Kenya Civil ABEX ABX GB ABX Air United States Civil ABEX ABX GB Airborne Express United States Civil ABG AAB W9 Abelag Aviation Belgium Civil ABSOLUTE AKZ AK Navigator LLC Kazakhstan Civil ACADEMY ACD Academy Airlines United States Civil ACCESS CMS Commercial Aviation Canada Civil ACE AIR AER KO Alaska Central Express United States Civil ACE TAXI ATZ Ace Air South Korea Civil ACEF CFM ACEF Portugal Civil ACEFORCE ALF Allied Command Europe (Mobile Force) Belgium Civil ACERO ARO Acero Taxi Mexico Civil ACEY ASQ EV Atlantic Southeast Airlines United States Civil ACEY ASQ EV ExpressJet United States Civil ACID 9(B)Sqn | RAF Panavia Tornado GR4 RAF Marham United Kingdom Military ACK AIR ACK DV Nantucket Airlines United States Civil ACLA QCL QD Air Class Líneas Aéreas Uruguay Civil ACOM ALC Southern Jersey Airways, Inc. -

Presentación De Powerpoint

Second Quarter Results 2021 July 2021 This presentation may contain forward-looking information and statements Disclaimer Disclaimer 2 Table of Contents Company Overview About the Company | Value Proposition | Historical Performance | Corporate Governance | Shareholders' Structure | Sustainability | COVID-19 Impact Aeronautical Business (AR) Passenger Flow 6M21 | Passenger Traffic | Airline Participation 6M21 | Aeronautical Revenue 2Q21 Non-Aeronautical Business (NAR) Commercial Revenues 2Q21 | Diversification Revenues 2Q21 | Historical NAR Growth Financial Results Highlights 2Q21 | Cost & Efficiency | Balance Sheet | Profitability Indicators | Value Distribution MDP & Maximum Tariffs MDP Investments 2021-2025 | Airport Expansions | Maximum Tariffs Outlook & Industry Industry Trends | Airlines Fleet 3 About the Company 13 Airports in the central-north More than 1,000 employees Overview region of Mexico, serving 11 committed to providing Company million passenger in 2020. Ciudad Juárez (CJS) aeronautical, commercial and real state services of Aeronautical 2 Hotels: Chihuahua (CUU) excellence to our passengers (AR)Business • NH Collection Hotel in Terminal Monterrey (MTY) and clients. Torreón (TRC) Reynosa (REX) 2 of the Mexico City Airport. Aeronautical - Business (NAR) Business • Hilton Garden Inn at Monterrey Culiacán (CUL) Listed in BMV & NASDAQ Non Tampico (TAM) Airport. Mazatlán (MZT) since 2006. San Luis Potosí (SLP) Results Durango (DGO) Zacatecas (ZCL) • Part of the main index of the Financial 3 Bonded warehouses: BMV (IPC). Zihuatanejo -

Monthly OTP February 2019

Monthly OTP February 2019 ON-TIME PERFORMANCE AIRLINES Contents On-Time is percentage of flights that depart or arrive within 15 minutes of schedule. Global OTP rankings are only assigned to all Airlines/Airports where OAG has status coverage for at least 80% of the scheduled flights. Regional Airlines Status coverage will only be based on actual gate times rather than estimated times. This may result in some airlines / airports being excluded from this report. If you would like to review your flight status feed with OAG pleas [email protected] MAKE SMARTER MOVES Airline Monthly OTP – February 2019 Page 1 of 1 Home GLOBAL AIRLINES – TOP 50 AND BOTTOM 50 TOP AIRLINE ON-TIME FLIGHTS On-time performance BOTTOM AIRLINE ON-TIME FLIGHTS On-time performance Airline Arrivals Rank No. flights Size Airline Arrivals Rank No. flights Size FA Safair 96.0% 1 1,920 173 WO Swoop 28.8% 159 666 247 GA Garuda Indonesia 95.5% 2 12,621 45 3H Air Inuit 37.4% 158 1,376 202 CM Copa Airlines 94.6% 3 9,565 58 SY Sun Country Airlines 39.2% 157 1,907 174 BC Skymark Airlines 92.5% 4 4,158 110 WG Sunwing Airlines Inc. 44.5% 156 2,715 139 XQ SunExpress 92.1% 5 2,245 156 AC Air Canada 48.9% 155 43,851 7 JH Fuji Dream Airlines 91.1% 6 1,960 168 AI Air India 51.0% 154 15,414 37 7G Star Flyer 90.9% 7 1,848 176 5J Cebu Pacific Air 52.6% 153 8,601 71 JP Adria Airways 90.6% 8 1,273 206 RS Air Seoul, Inc 54.8% 152 986 222 XL LATAM Airlines Ecuador 90.4% 9 799 241 MS Egyptair 56.9% 151 6,292 88 SATA International-Azores LS Jet2.com 90.2% 10 2,905 136 S4 57.0% 150 396 276 Airlines S.A.