In Re American Apparel, Inc. Shareholder Litigation 10-CV-06352-Consolidated Class Action Complaint for Violation of Federal

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Fear and Threat in Illegal America: Latinas/Os, Immigration, and Progressive Representation in Colorblind Times by Hannah Kathr

Fear and Threat in Illegal America: Latinas/os, Immigration, and Progressive Representation in Colorblind Times by Hannah Kathryn Noel A dissertation submitted in partial fulfillment of the requirements for the degree of Doctor of Philosophy (American Culture) in the University of Michigan 2014 Doctoral Committee: Associate Professor Evelyn A. Alsultany, Co-chair Associate Professor María E. Cotera, Co-chair Associate Professor María Elena Cepeda, Williams College Associate Professor Anthony P. Mora © Hannah Kathryn Noel DEDICATION for Mom & Dad ii ACKNOWLEGEMENTS I could not have accomplished this dissertation without the guidance of my co-chairs, and graduate and undergraduate mentors: Evelyn Alsultany, María Cotera, María Elena Cepeda, Mérida Rúa, Larry La Fountain-Stokes, Carmen Whalen, Ondine Chavoya, Amy Carroll, and Anthony Mora. Evelyn, thank you for the countless phone calls, comments on every page of my dissertation (and more), advice, guidance, kind gestures, and most of all your sensibilities. You truly went above and beyond in commenting and helping me grow as a teacher, scholar, and human. María, thank you for standing by my side in both turbulent, and joyous times; your insight and flair with words (and style) are beyond parallel. Maria Elena, thank you for your constant guidance and keen constructive criticism that has forced me to grow as an intellectual and teacher. I will never forget celebrating with you when I found out I got into Michigan, I am beyond honored and feel sincere privilege that I have been able to work and grow under your mentorship. Mérida, I would have never found my way to my life’s work if I had not walked into your class. -

UNIVERZITA KARLOVA V PRAZE Fotografické Strategie Společnosti

UNIVERZITA KARLOVA V PRAZE FAKULTA SOCIÁLNÍCH VĚD Institut komunikačních studií a žurnalistiky Katedra žurnalistiky Jan Červenka Fotografické strategie společnosti American Apparel Bakalářská práce Praha 2015 ‚ Autor práce: Jan Červenka Vedoucí práce: doc. MgA. Filip Láb, Ph.D. Oponent práce: Rok obhajoby: 2015 Hodnocení: ‚ Bibliografický záznam ČERVENKA, Jan. Fotografické strategie společnosti American Apparel, Praha, 2015. Počet s. 45 Bakalářská práce (Bc.) Univerzita Karlova, Fakulta sociálních věd, Institut komunikačních studií a žurnalistiky, Katedra žurnalistiky. Vedoucí bakalářské práce doc. MgA. Filip Láb, Ph.D. Abstrakt Předmětem práce je analyzovat fotografické strategie oděvní společnosti American Apparel v letech 2011 – 2015 a její současné reklamní strategie. V teoretické části práce se text zaměří na principy reklamní fotografie a popíše historii fotografie módní. Dále zmíní práce fotografů, kteří se ve svém životě věnovali atypickým reklamním strategiím. Obsahem další části práce je přehled vzniku a vývoje společnosti American Apparel a jejího zakladatele Dova Charneyho. Na základě textů teoretika obrazu Roland Barthese a metod popsaných v knize Metody výzkumu médií od Trampoty a Vojtěchovské, aplikuje autor práce své poznatky na kvantitativní i kvalitativní výzkum již zmíněných reklamních fotografií. Stěžejním výstupem práce je právě kvalitativní analýza, jejíž předlohou se stal Barthesův text Rétorika obrazu. Abstract The aim of this thesis is to analyse American Apparel’s photographical strategies and its advertising tendencies in the years 2011 – 2015. In the theoretical part of this thesis, the text will cover the principals of advertising photography and will briefly describe the history of fashion photography. Also it will mention the work of famous photographers who have worked with atypical visual methods in the past. -

Dov Charney's American Dream Audio Part 3: Photos Https

Dov Charney’s American Dream Audio Part 3: Photos https://gimletmedia.com/episode/part-3-photos-season-4-episode-6/ Part 4: Boundaries https://gimletmedia.com/episode/part-4-boundaries-season-4-episode-7/ Part 5: Suits https://gimletmedia.com/episode/part-5-suits-season-4-episode-8/ Part 6: Anger https://gimletmedia.com/episode/part-6-anger-season-4-episode-9/ Part 7: MAGIC https://gimletmedia.com/episode/part-7-magic-season-4-episode-10/ Host: Lisa Chow Senior Producer: Kaitlin Roberts Producers: Bruce Wallace, Luke Malone, Molly Messick Associate Producer: Simone Polanen Editors: Alex Blumberg, Alexandra Johnes, Caitlin Kenney Audio Engineers: Andrew Dunn, David Herman, Martin Peralta, Dara Hersch 2 Episode Transcripts Part 3: Photos DOV: Look how cool that is, that metro thing. C’mon that is cool. Isn’t it? LISA: Oh yeah! There’s a metro stop right on a highway? DOV: Yeah, this is LA, dude. Get with the program. LISA: Hello. From Gimlet Media, this is StartUp. I'm Lisa Chow. And once again, I’m sitting in the car with the ex-CEO of American Apparel Dov Charney. And just a quick warning, there’s some swearing in this episode … and some sexual content. DOV: This is an interesting mural that I’m going to shoot now since we’re in traffic. That’s a good one. LISA: Dov’s taking photographs while driving. This happens all the time. Something catches his eye — a mural or an old sign or a storefront — and he has to get the shot. So he rolls down the window, grabs his phone, and stretches out both hands…and totally forgets about the steering wheel. -

BATTLE of the APPS Banana’S New Flagship Beauty-Booking Apps Are Quickly Overpopulating the Rapidly Expanding Mobile Universe in Cyberspace

ADIDAS KENDALL’S STEPS UP CALVINS KENDALL JENNER IS THE TOKYO TALES THE STRUGGLING GERMAN FACE OF THE LATEST AD MIUCCIA PRADA MINGLED WITH REI KAWAKUBO, ACTIVEWEAR BRAND OUTLINES AN CAMPAIGN FOR CALVIN RAF SIMONS AND MORE AT A MIU MIU EVENT AGGRESSIVE FIVE-YEAR PLAN TO KLEIN JEANS. PAGE 4 IN THE JAPANESE CAPITAL. PAGE 11 GET BACK TO GROWTH. PAGE 2 FROM DOV TO SEC No End To The Woes At American Apparel By EVAN CLARK AMERICAN APPAREL INC. is teetering on the edge of chaos. And if that in itself is nothing new, this time around the retailer’s facing an unusually thorny set of challenges on multiple fronts: ■ Ousted founder Dov Charney continues to stir up FRIDAY, MARCH 27, 2015 ■ $3.00 ■ WOMEN’S WEAR DAILY trouble, from agitating an already disgruntled work- WWD force to seeking a backer to buy the fi rm, moving ahead with arbitration and, tonight, appearing on ABC’s “20/20.” ■ Fourth-quarter losses widened as sales fell more than 9 percent and workers are being furloughed at the Los Angeles factory. ■ The brand is being reimagined with more of a social emphasis and some of the scantily clad sales associates long featured in its ads will be replaced with models. ■ Shareholders have sued the company, claiming it failed to maintain control of its colorful founder. Under Charney, American Apparel honed contro- versy to a high art and lurched from one loan with a sky- high interest rate to the next — always keeping just a step ahead of both the debt collector and Miss Manners. -

Sexual Harassment and Corporate Law

University of Chicago Law School Chicago Unbound Journal Articles Faculty Scholarship 2018 Sexual Harassment and Corporate Law Daniel Hemel Dorothy Shapiro Lund Follow this and additional works at: https://chicagounbound.uchicago.edu/journal_articles Part of the Law Commons Recommended Citation Daniel Hemel & Dorothy Shapiro Lund, "Sexual Harassment and Corporate Law," 118 Columbia Law Review 1583 (2018). This Article is brought to you for free and open access by the Faculty Scholarship at Chicago Unbound. It has been accepted for inclusion in Journal Articles by an authorized administrator of Chicago Unbound. For more information, please contact [email protected]. COLUMBIA LAW REVIEW VOL. 118 OCTOBER 2018 NO. 6 ARTICLES SEXUAL HARASSMENT AND CORPORATE LAW Daniel Hemel * & Dorothy S. Lund ** The #MeToo movement has shaken corporate America in recent months, leading to the departures of several high-profile executives as well as sharp stock price declines at a number of firms. Investors have taken notice and taken action: Shareholders at more than a half dozen publicly traded companies have filed lawsuits since the start of 2017 alleging that corporate fiduciaries breached state law duties or violated federal securities laws in connection with sexual harassment scandals. Additional suits are likely in the coming months. This Article examines the role of corporate and securities law in regulating and remedying workplace sexual misconduct. We specify the conditions under which corporate fiduciaries can be held liable under state law for perpetrating sexual misconduct or allowing it to occur. We also discuss the circumstances under which federal securities law requires issuers to disclose allegations against top executives and to reveal settlements of sexual misconduct claims. -

American Apparel Inc. and Latina Labor in Los Angeles

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by Via Sapientiae: The Institutional Repository at DePaul University Diálogo Volume 18 Number 2 Article 5 2015 Branding Guilt: American Apparel Inc. and Latina Labor in Los Angeles Hannah Noel Miami University, Oxford, Ohio Follow this and additional works at: https://via.library.depaul.edu/dialogo Part of the Latin American Languages and Societies Commons Recommended Citation Noel, Hannah (2015) "Branding Guilt: American Apparel Inc. and Latina Labor in Los Angeles," Diálogo: Vol. 18 : No. 2 , Article 5. Available at: https://via.library.depaul.edu/dialogo/vol18/iss2/5 This Article is brought to you for free and open access by the Center for Latino Research at Via Sapientiae. It has been accepted for inclusion in Diálogo by an authorized editor of Via Sapientiae. For more information, please contact [email protected]. Branding Guilt: American Apparel Inc. and Latina Labor in Los Angeles Hannah Noel Miami University, Oxford, Ohio Abstract: A study of the marketing strategies of the clothing enterprise, American Apparel, how it targets affluent, educated youth through socially conscious tactics, including a focus on pro-immigrant rights and Los Angeles-made, “sweatshop-free” advertising. The essay analyzes the ideologies and stances behind marketing materials that often contain images of Latinas/os as laborers, and white (European origin) population as consumers, and examines how U.S.-based ethical capitalism operates as a neoliberal form of social regulation to champion personal responsibility and individual freedom, in often hidden and inferentially racist and classist ways. -

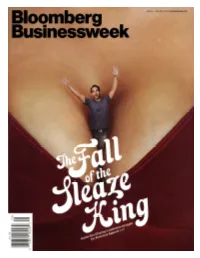

Dov Charney's Sleazy Struggle for Control of American Apparel July 9, 2014

Don Charney’s Sleazy Struggle for Control of American Apparel By Susan Berfield When I first reach Dov Charney on been in crisis as American Apparel 2011, Irene Morales, a sales associ- June 24, he’s scrambling to raise lost $270 million and came close to ate, accused Charney of using her as money, find a partner, try anything bankruptcy twice. But the board had a sex slave and sought damages of a to get his company back. His hand- stuck by him, sales had increased quarter-billion dollars. An arbitrator picked board of directors had ousted this spring, and summer promised to dismissed those claims but found the him from American Apparel six days be busier yet. Things were finally company “vicariously liable” for the earlier following an investigation looking up. conduct of another employee who that turned up several instances of had created a fake blog in Morales’s alleged misconduct. “They’re con- Charney packed samples, ordered an name. Then the employee posted cerned that an unconventional leader Uber car to get to LAX, and boarded erotic photos of Morales on it. Char- somehow damages the company’s a red-eye for New York. After he landed, he put on a suit and tie and, ney told some board members and chances of success. But a contrarian, wearing white American Apparel his lawyers that he had photos of alternative-thinking CEO can bring socks and Common Projects sneak- Morales and of others accusing him creative ideas that advance the com- ers, sauntered into the office of the of harassment that showed the wom- pany, even the industry,” he says. -

Regional Ethics Bowl Cases

REGIONAL ETHICS BOWL CASES FALL 2011 Prepared by: Rhiannon D. Funke, Chair Editing Board: Adam Potthast Case Writers: Susanna Flavia Boxall Raquel Diaz-Sprague Michael B. Funke Gretchen A. Myers Association for Practical and Professional Ethics 2011 Editor’s Note: Please note that source materials cited may be used multiple times, but only identified once per case. Case #1: Transient Student Voting Rights New legislation introduced by New Hampshire State Representative Gregory Sorg, HB 176, specifically addresses the rights of students to vote. According to HB 176, ―The domicile for voting purposes of a person attending an institution of learning shall not be the place where the institution is located unless the person was domiciled in that place prior to matriculation.‖1 The force of HB 176 is to require that students vote in their hometowns and not the town in which they reside for educational purposes. The bill would not allow students to register to vote in the town in which they attend university unless they lived in that town prior to enrolling. Supporters of HB 176 include House Representative and University of New Hampshire student Michael Weeden. Weeden argues, ―each individual person should vote where [he or she] resides long-term, not just where [he or she] resides for a semester.‖2 The bill‘s sponsor, Gregory Sorg, defends the initiative saying, ―This is a reasonable classification to account for one demographic group that is unlike any other and threatens to overwhelm the legitimate residents of a town or city.‖3 House Speaker William O‘ Brien says, ―I look at towns like Plymouth and Keene and Hanover, and particularly Plymouth. -

Dov Charney: from American Apparel to Los Angeles Apparel by Deborah Belgum Senior Editor

NEWSPAPER 2ND CLASS $2.99 VOLUME 73, NUMBER 6 FEBRUARY 3–9, 2017 THE VOICE OF THE INDUSTRY FOR 72 YEARS Dov Charney: From American Apparel to Los Angeles Apparel By Deborah Belgum Senior Editor If the business plan sounds the same, it is. Dov Charney is more determined than ever to make his second stab at ap- parel manufacturing more successful than the first. Charney, who was fired at the end of 2014 from his American Apparel clothing company, is still stinging by the ouster and the loss of the company he founded. But he is determined to move forward and prove that you can manufacture clothing in Los Angeles, pay a fair wage and make money. “We are going to take over and be an important force in the apparel industry,” he said, speaking Feb. 2 at a creative services and artist-oriented event organized by Le Book at the Pacific Design Center in West Hollywood, Calif. On an outdoor patio with a clear view of the three col- orful buildings that make up the Pacific Design Center, a crowd of more than 100 people showed up to hear Char- ➥ Dov Charney page 6 TRADE SHOW REPORT Surf Industry—and More—Turn Out for Surf Expo By Alison A. Nieder Executive Editor Exhibitors were “stoked” and buyers were busy at the Jan. 26–28 run of Surf Expo at the Orange County Con- vention Center in Orlando, Fla. The surf-industry trade show drew a mix of core surf and swim stores from across the country, including Cali- fornia retailers Jack’s Surfboards, Surf Diva, Sun Diego and Hansen’s; East Coast retailers Ron Jon, Curl, Cin- namon Rainbows, Warm Winds and Brave New World; and Hawaiian retailers Hi Tech and Déjà Vu. -

Collection of the Center for the Study of Political Graphics

http://oac.cdlib.org/findaid/ark:/13030/c8959k7m No online items Collection of the Center for the Study of Political Graphics Center for the Study of Political Graphics 3916 Sepulveda Blvd. Suite 103 Culver City, California 90230 (310) 397-3100 [email protected] http://www.politicalgraphics.org/ 2020 Collection of the Center for the See Acquisition Information 1 Study of Political Graphics Descriptive Summary Title: Collection of the Center for the Study of Political Graphics Dates: 1900- ; bulk 1960- Collection Number: See Acquisition Information Creator/Collector: Multiple creators Extent: 330 flat files Repository: Center for the Study of Political Graphics Culver City, California 90230 Abstract: The collection of the Center for the Study of Political Graphics (CSPG) contains over 90,000 domestic and international political posters and prints relating to historical and contemporary movements for social change. The finding aid represents the collection in its entirety. Language of Material: English Access The CSPG collection is open for research by appointment only during the Center's operating hours. Publication Rights CSPG does not hold copyright for any items in the collection. CSPG provides access to the materials for educational and research purposes only. Users are responsible for obtaining all necessary permissions for use. Preferred Citation [Identification of item], Collection of the Center for the Study of Political Graphics (CSPG). Acquisition Information CSPG acquires 3,000 to 5,000 items annually, primarily through donations. Each acquisition is assigned a unique acquisition number and is written on individual items before these are sorted and filed by topic. Scope and Content of Collection The collection represents diverse social and political movements. -

Alternative Media at UCI Vol I Issue II

ALTERNATIVE MEDIA COLLECTIVE Volume I Issue II Spring quarter June 3rd, 2005 Cellador Irvine Progressive Statement of Purpose: The 2004-2005 school year was Statement of Purpose: The Irvine Progressive is a non-partisan pub- the first year Cellador was recognized as an Alternative lication dedicated to fostering political awareness and intelligent dis- Media publication. It was founded to showcase creative cussion. We seek to provide a forum chiefly for viewpoints associated works of UCI students. Cellador provides the UCI com- with the political left at the University of California, Irvine. munity with a publication that allows students of all disci- plines to share and network with other students through their creative expressions. By printing quarterly through- Contacts: Heidi Khaled ([email protected]), Gerald Tan (gtan@uci. out the academic year, Cellador provides a consistent op- edu), and Alexander Phillips ([email protected]) portunity for students to view the works of other students and submit their work for publication. Contacts: Christina Luiz ([email protected]), Zachary Horn ([email protected]) Jaded Statement of Purpose: Jaded magazine is a form of alternative media to encourage political, cultural, and personal discourse among UCI Irvine Review students. We celebrate and support the Asian Pacific Islander commu- nity through the retelling of the past, engaging of the present, and Statement of Purpose: The Irvine Review Foundation is a sharing a vision for the future. We hope to build connections and non-profit, non-partisan educational foundation estab- bridge gaps between people of different ethnicities and ways of think- lished to promote conservative ideas and enhance the qual- ing. -

Identity & Inspiration

NEWSPAPER 2ND CLASS $2.99 VOLUME 71, NUMBER 21 MAY 15–21, 2015 THE VOICE OF THE INDUSTRY FOR 70 YEARS FREIGHT & LOGISTICS How Apparel Importers Are Adjusting Their Strategies for the Next Big Shipping Season By Deborah Belgum Senior Editor Late last year, Ram Kundani waited as long as seven weeks to extract his cargo containers filled with printed dresses, lace tops and distressed denim pants from the con- gested ports of Los Angeles and Long Beach. Many of his apparel shipments didn’t make it in time for the make-or-break holiday season, costing his company more than $500,000 in lost sales. This year, hoping not to be burned again, he is bringing his apparel import in a little earlier than normal. “We used to add an extra three or four days for our mer- chandise to clear. Now we are adding up to 10 days to two weeks just in case,” said Kundani, executive vice president ➥ Freight page 9 The Point: New Retail Center Bows in LA County By Andrew Asch Retail Editor Planet Blue, Lucky Brand and Michael Stars are scheduled to open stores at The Point, Los Angeles Coun- ty’s newest retail center, which is scheduled to take a bow on July 30. Also scheduled to take a bow at The Point are boutiques for Prana; Lou & Grey, a new concept from Ann Taylor Loft; No Rest for Bridget, a fast-fashion chain; Athleta, Gap Inc.’s women’s fitness line; and Six:02, a women’s fitness apparel and footwear shop owned by Foot Locker Inc.