Annexure to the Board Report | L&T Annual Report 2019-20

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Download Full Report

CONTENTS 02 Unstoppable Corporate overview We have been persistent 02 Unstoppable in our aim to establishing 04 Chairman’s Message and maintaining market leadership to be able to achieve 06 Vice Chairman’s Message unprecedented growth for our 08 Board of Directors stakeholders. 10 Management Board 12 Key Performance Highlights 14 14 Integrated Report Integrated Report 28 Management Discussion & Analysis Apollo Tyres’ contribution 51 Sustainability Snapshot to social and economic development is critical to create and sustain an enabling environment for investment. This has enabled the Company’s positioning as a credible Statutory Reports stakeholder partner. 84 Board’s Report 95 Annual Report on CSR 28 102 Business Responsibility Report Management 126 Corporate Governance Report Discussion & Analysis Financial Statements 161 Standalone Financial Statements 223 Consolidated Financial Statements UNSTOPPABLE Since inception, we have worked towards establishing ourselves as a leading player in the sale and manufacture of tyres. We have been persistent in our aim to establishing and maintaining market leadership and be able to achieve unprecedented growth for our stakeholders. In FY2018-19 (FY2019), we continued to focus We are unstoppable in establishing our on our key revenue generating regions APMEA leadership across multiple segments. (Asia Pacific, Middle East and Africa, including Our consistently advancing product range coupled India) and Europe. We expanded our presence in with product innovations are enabling us to achieve Americas by added new territories and increasing the same. our value proposition. The APMEA operation continued its focus on consolidating its leadership We are unstoppable in working towards achieving and enhancing share in India through the cutting edge manufacturing capabilities and introduction of best in class and technologically world-class R&D. -

IN the BUSINESS of PROGRESS CONTENTS Apollo Tyres in Brief

Annual Report 2019-20 IN THE BUSINESS OF PROGRESS CONTENTS Apollo Tyres in brief 01-03 Apollo Tyres is one of the most trusted Corporate factsheet names in the manufacture and sale of tyres. The Company was founded in 1972 and is 04-13 headquartered in Gurugram, Haryana (India). Leadership and governance 06 Chairman’s message 08 Vice-Chairman’s message 10 Board of Directors Catering to all tyre segments 12 Management Team TRUCK AND BUS LIGHT TRUCK 14-77 Performance and progress 16 Key performance indicators 18 Know our capitals 20 Business model 22 Capital-wise information 36 Progress amidst volatility 38 Progress that is sustainable 40 Progress through people centricity 42 Value created for the stakeholders PASSENGER VEHICLES TWO-WHEELER 78-93 Management Discussion & Analysis 94-170 Statutory Reports 94 Board’s Report 107 Annual Report on CSR 113 Business Responsibility Report 138 Corporate Governance Report OFF-HIGHWAY 171-305 Financial Statements 171 Standalone 233 Consolidated Apollo Tyres’ success as a leading tyre such as: geo-political relations, economic manufacturer is inextricably linked with the growth, industry cyclicality, environmental progress of the people, the businesses we issues, technological innovation, safety and partner and the planet at large. We have consumer attitudes. Our FY20 performance is always persevered to exceed expectations, a reflection of the resulting uncertainties. It set new benchmarks and in some cases, is also a testament to our foundational values shape the future of the industry. and intrinsic strengths that have helped us navigate through these uncertainties. Our marquee brands, Apollo and Vredestein, enjoy premium positions in the commercial As we step into a new decade, replete with and passenger vehicle tyre segments in unexplored opportunities, we are keen on India and Europe, respectively. -

Model Portfolio Update

Model Portfolio update January 21, 2016 LatestDeal Team Model – PortfolioAt Your Service Large cap Midcap Name of the company Weightage(%) Name of the company Weightage(%) Auto 14 Aviation 6 Tata Motor DVR 4 Interglobe Aviation 6 Bosch 3 Auto 6 Maruti 4 Bharat Forge 6 EICHER Motors 3 BFSI 6 BFSI 23 BjjFiBajaj Finserve 6 HDFC Bank 8 Capital Goods 6 Axis Bank 3 HDFC 8 Bharat Electronics 6 Bajaj Finance 4 Cement 6 Capital Goods 5 Ramco Cement 6 L & T 5 Consumer 24 Cement 3 Symphony 6 UltraTech Cement 3 Supreme Ind 6 FMCG/Consumer 14 Kansai Nerolac 6 ITC 7 Pidilite 6 United Spirits 2 FMCG 8 Asian Paints 5 Nestle 8 IT 21 Infrastructure 8 Infosys 10 NBCC 8 TCS 8 Oil & Gas 6 Wipro 3 Meida 2 CtlCastrol 6 Zee Entertainment 2 Logistics 6 Metal 2 Container Corporation of India 6 Tata Steel 2 Pharma 12 Oil & Gas 4 Natco Pharma 6 Reliance Industries 4 Torrent Pharma 6 Pharma 12 Textile 6 Lupin 5 Arvind 6 Dr Reddys 4 Total 100 Aurobindo Pharma 3 Total 100 • Exclusion - Eicher Motors, Bajaj Finance (transferred to large cap), PVR, • Exclusion- State Bank of India, Bharti Airtel and ONGC CARE, Cummins & Shree Cement • Inclusion – Eicher Motors, Bajaj Finance (transferred from midcap), Wipro, • Inclusion – Ramco Cement, Bajaj Finserv, Supreme Industries, Indigo, Reliance Industries & Aurobindo Pharma Pidilite, Bharat Electronics and Bharat Forge Source: Bloomberg, ICICIdirect.com Research *Diversified portfolio - Combination of 70% large cap and 30% midcap portfolio OutperformanceDeal Team – At continues Your Service across all portfolios… • Our indicative large cap equity model portfolio (“Quality -20”) has • In the large cap space we continue to remain positive on pharma & IT. -

The Indian Automotive Supplier Report Supplierbusiness

IHS AUTOMOTIVE The Indian Automotive Supplier Report SupplierBusiness 2015 edition supplierbusiness.com REGIONAL REPORT Indian Subcontinent SAMPLE IHS Automotive | Supplying Ford Contents Executive Summary 4 – Renault-Nissan third largest exporter 30 – Tata’s exports expected to decrease 30 Indian Economy and Business Environment 6 – Ford ups capacity in India to boost exports 30 Volatile GDP growth in BRICS 7 – Volkswagen increases exports from India 31 Per capita GDP seen rising 8 – Honda to grow exports from India 31 Inflation in check, for now 8 – GM to turn India into a global export hub 31 Consumer demand expected to improve 9 Foreign investments going up 9 Overview of Automotive Supplier Industry 32 Industrial production recovers 10 Speed bumps 33 Shrinking exports, a cause for concern 10 Positive sentiment returns 33 Indian currency expected to depreciate mildly in 2015, – Engine parts, the largest segment 33 2016 11 – AMT to gain traction 34 – Chassis production 35 The Indian Automotive Market 13 – Interiors production 35 – Maruti Suzuki boosts sales with new models 14 – Exteriors production 35 – Hyundai increases market share 15 – Thermal component production 35 – Mahindra stays leader of SUV segment 16 – Market share of HVAC systems suppliers 36 – Tata Motors plans to reclaim lost ground 16 – The proliferation of car security systems 36 – Honda strengthens position in India with diesel cars Top 10 automotive suppliers in India 36 17 – Motherson Sumi System Limited 37 Key trends in the Indian LV market 18 – Amtek Auto 37 – Hatchback -

Asian Daily EPS, TP and Rating Changes Top of the Pack

Thursday, 13 February 2014 (Global Edition) Asian Daily EPS, TP and Rating changes Top of the pack ... EPS TP (% change) T+1 T+2 Chg Up/Dn Rating Commonwealth Bank 3 2 0 0 U (U) Asia Equity Strategy Sakthi Siva (3) Australia New report: Cyclicals have outperformed defensives YTD. Continue? China Mengniu Dairy (6) (7) 20 25 O (O) PRADA S.p.A. (10) (12) (5) 29 O (O) India IT Services Sector Anantha Narayan (4) Apollo Tyres 8 2 10 22 O (O) Is it too crowded for further performance? Cipla Limited (6) 0 0 1 N (N) Jaiprakash Power Ventures (60) (17) (14) 107 O (O) Page Industries 3 3 2 13 O (O) Asia Technology Sector Keon Han (5) Perusahaan Gas Negara (1) 1 2 31 O (O) New report: LED—entering expansion phase Softbank 0 0 — R (R) UMW Oil & Gas 0 (7) 31 3 N (N) China Mengniu Dairy (2319.HK) – Maintain O Kevin Yin (6) Universal Robina Corp. 1 1 0 18 O (O) 2014 outlook: Should pass through 10% raw milk price inflation; EPS likely to grow 35.9% YoY Huaku Development (3) (1) (5) 32 O (O) Novatek Microelectronics 3 1 3 (18) U (U) CS pic of the day Sinopac Holdings 2 2 3 8 N (N) AIS PCL (4) (7) (4) 29 O (O) Global general lighting and LED lighting market size Siam City Cement 0 (2) (5) 0 U (U) The LED general lighting industry is now shifting from the initial penetration phase to a rapid expansionary TAC PCL 0 0 0 44 O (O) phase. -

List of Nodal Officer

List of Nodal Officer Designa S.No tion of Phone (With Company Name EMAIL_ID_COMPANY FIRST_NAME MIDDLE_NAME LAST_NAME Line I Line II CITY PIN Code EMAIL_ID . Nodal STD/ISD) Officer 1 VIPUL LIMITED [email protected] PUNIT BERIWALA DIRT Vipul TechSquare, Golf Course Road, Sector-43, Gurgaon 122009 01244065500 [email protected] 2 ORIENT PAPER AND INDUSTRIES LTD. [email protected] RAM PRASAD DUTTA CSEC BIRLA BUILDING, 9TH FLOOR, 9/1, R. N. MUKHERJEE ROAD KOLKATA 700001 03340823700 [email protected] COAL INDIA LIMITED, Coal Bhawan, AF-III, 3rd Floor CORE-2,Action Area-1A, 3 COAL INDIA LTD GOVT OF INDIA UNDERTAKING [email protected] MAHADEVAN VISWANATHAN CSEC Rajarhat, Kolkata 700156 03323246526 [email protected] PREMISES NO-04-MAR New Town, MULTI COMMODITY EXCHANGE OF INDIA Exchange Square, Suren Road, 4 [email protected] AJAY PURI CSEC Multi Commodity Exchange of India Limited Mumbai 400093 0226718888 [email protected] LIMITED Chakala, Andheri (East), 5 ECOPLAST LIMITED [email protected] Antony Pius Alapat CSEC Ecoplast Ltd.,4 Magan Mahal 215, Sir M.V. Road, Andheri (E) Mumbai 400069 02226833452 [email protected] 6 ECOPLAST LIMITED [email protected] Antony Pius Alapat CSEC Ecoplast Ltd.,4 Magan Mahal 215, Sir M.V. Road, Andheri (E) Mumbai 400069 02226833452 [email protected] 7 NECTAR LIFE SCIENCES LIMITED [email protected] SUKRITI SAINI CSEC NECTAR LIFESCIENCES LIMITED SCO 38-39, SECTOR 9-D CHANDIGARH 160009 01723047759 [email protected] 8 ECOPLAST LIMITED [email protected] Antony Pius Alapat CSEC Ecoplast Ltd.,4 Magan Mahal 215, Sir M.V. Road, Andheri (E) Mumbai 400069 02226833452 [email protected] 9 SMIFS CAPITAL MARKETS LTD. -

Havells India (HAVIND)

Havells India (HAVIND) CMP: | 1031 Target: | 1215 (18%) Target Period: 12 months BUY May 22, 2021 Strong recovery across product segments... Havells continued its growth momentum in Q4FY21 with topline growth of 50% YoY in line with our estimate of 48%. The company witnessed strong Particulars revenue growth in all business verticals cables, switchgears, electrical Particular Amount consumer durable (ECD), Lloyd, lightings and others by 51%, 53%, 71%, Market Capitalization (| Cr) 64,324.1 29%, 40% and 71%, respectively. The management reiterated market share Total Debt (FY21) (| Cr) 393.7 gains, strong demand traction in rural helped drive sales recovery for Havells Cash and Inv (FY21) (| Cr) 1,931.0 India in Q4 and in FY21. The company reported ~11% topline growth in EV (| Cr) 62,786.7 FY21 despite a washout in Q1. The key takeaways from conference call are: 52 week H/L 1238 / 454 Equity capital (| Cr) 62.6 Update Result 1) strong sales traction in first two weeks of April 2021 before lockdown Face value (|) 1.0 sseSFsfsf imposed in many states, 2) May sales hit by lockdown across the country, 3) price hikes of 10% in fans and 45-50% in cable business to offset Price Performance sseSFsfsf inflationary pressure, 4) focus on capacity building of Lloyd (future launches in refrigerators and washing machines categories), 5) focus on tapping rural 1400 20000 1200 and semi urban markets for the long term. However, considering lockdowns 1000 15000 and higher input prices, we revise our FY22E revenue, PAT estimate 800 10000 downward by ~7%, 6%, respectively. 600 400 5000 200 Strong b/s helps navigate challenging scenario 0 0 Havells India reported revenue, PAT CAGR of ~13%, ~15%, respectively, in Oct-18 Apr-21 Jan-20 Jun-20 Dec-17 Nov-20 Aug-19 Mar-19 the last 10 years with EBITDA margin expansion of 200 bps YoY to 15%. -

Annual Report 2016-17

Annual Report 2016-17 apollotyres.com REACH Corporate Overview Introduction 1 Chairman’s Message 2 Vice Chairman’s Message 4 THE Board of Directors 6 Management Board 8 Performance Highlights 10 Management Discussion and 12 Analysis Report Sustainability Report 32 WORLD Statutory Reports Board’s Report 54 HIGHLIGHTS Annual Report on CSR 65 Business Responsibility Report 75 2016-17 Corporate Governance Report 98 Financial Statements `140.53 Bn Standalone Financial Statements 124 Gross Sales Consolidated Financial 194 Statements `39.02 Bn Capital Expenditure 15.8% ROE `10.99 Bn Net Profit `20.01 Bn EBITDA REACH india hungary WORLD where to next? At Apollo Tyres, we are building tyres for the future of transportation and mobility. As we do this, we are transforming ourselves both from a product and markets perspective. Building on our core competencies, strength and brand, we are aspiring to ‘Reach the World’, by manufacturing in different countries, expanding our distribution networks, and growing our brand associations. We are creating a distinctly ‘glocal’ culture in our organsiation, where we are thinking like a global organisation and yet, aligning ourselves to local needs in each geography we operate. At the same time, we are proud of being an Indian brand, and representing the best of technology, operations and thinking on the world stage. In FY17, we took many steps that furthered our aim of reaching the world. These include the inauguration of our Hungary plant and the Global R&D centre. These, however, are just stepping stones to achieving our cherished vision. As we do this, we are equally committed to ‘reach’ each of our stakeholders, and create value for them, in ways that are credible and meaningful. -

Avenue Supermarts (DMART IN)

Avenue Supermarts (DMART IN) Rating: BUY | CMP: Rs3,378 | TP: Rs3,686 July 10, 2021 Rising Footfalls, Online scalability Positive Q1FY22 Result Update Quick Pointers: Change in Estimates | ☑ Target | Reco . Q1FY22 saw a stronger second wave resulting in loss of more days or higher restriction on number of hours of store operations. Change in Estimates Current Previous . No significant impact on supply chain during the quarter, Inventory moving FY22E FY23E FY22E FY23E Rating BUY BUY towards normal levels. Target Price 3,686 3,366 Sales (Rs. m) 2,89,846 4,08,606 2,89,846 4,08,606 D’Mart 1Q results depicted impact of a strong second wave with business % Chng. - - EBITDA (Rs. m) 23,781 37,290 23,781 37,290 loss of more days (versus last year) and higher restriction on operating hours % Chng. - - /non-essential sales. However, rising footfalls, vaccination drive, 203% sales EPS (Rs.) 22.5 36.0 22.5 36.0 % Chng. - - growth in D’Mart ready and work on new store openings is positive. Key Financials - Consolidated Despite near term challenges we remain optimistic about the long term Y/e Mar FY20 FY21 FY22E FY23E potential of D’Mart on back of 1) Increasing scale and scope D’Mart Ready 2) Sales (Rs. m) 2,48,702 2,41,431 2,89,846 4,08,606 Extending offerings on D’Mart ready app to include general merchandise, EBITDA (Rs. m) 21,284 17,431 23,781 37,290 fresh food and vegetable 3) Growth in General merchandise sales over lower Margin (%) 8.6 7.2 8.2 9.1 PAT (Rs. -

Indigo Paints Ltd

Stock Idea Sector: Consumer Goods August 23, 2021 Indigo Paints Ltd Paint your portfolio bright Powered by Sharekhan’s 3R Research Philosophy Indigo Paints Ltd Paint your portfolio bright Stock Idea Stock Powered by the Sharekhan 3R Research Philosophy Consumer Goods Sharekhan code: INDIGOPNTS Initiating Coverage 3R MATRIX + = - Summary We initiate coverage on Indigo Paints Ltd (IPL) with a Buy and assign a target price of Rs. 3,305. Right Sector (RS) ü Differentiated business model, excellent return profile and strong structural growth outlook will keep valuation at a premium of 60x/44x its FY2023/24E earnings versus peers. Right Quality (RQ) ü With a differentiated product portfolio and bottom-up approach, IPL is emerging as one of India’s fastest growing paints companies. Revenues and PAT clocked a CAGR of 22% and 71% over FY2018-21. Right Valuation (RV) ü Gross margins are highest among peers at ~48% led by IPL’s locational advantage and healthy mix of revenues from differentiated products. + Positive = Neutral - Negative Better working capital management has kept net working capital cycle low at 13-14 days. Operating cash flows (OCF) improved from Rs. 42.8 crore to Rs. 101.4 crore over FY2019-21. Reco/View Indigo Paints Limited (IPL) is an emerging player, which has created a niche for itself in the highly competitive paints industry by launching differentiated products, creating brand equity through one prominent brand ‘Indigo’ and follow bottoms-up approach to expand its distribution in the Reco: Buy domestic market. It has market share of 2% but has strong potential to improve it in the coming years. -

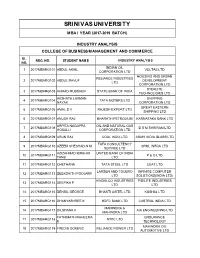

Srinivas University M Ba I Year (2017-2019 Batch)

SRINIVAS UNIVERSITY M BA I YEAR (2017-2019 BATCH) INDUSTRY ANALYSIS COLLEGE OF BUSINESS MANAGEMENT AND COMMERCE SL . REG. NO. STUDENT NAM E INDUSTRY ANALYSIS NO. INDIAN OIL 1 2017MBARG101 ABDUL AKHIL VOLTAS LTD CORPORATION LTD HOUSING AND URBAN RELIANCE INDUSTRIES 2 2017MBARG102 ABDUL RAVUF DEVELOPMENT LTD CORPORATION LTD STERLITE 3 2017MBARG103 AHMAD MUBSHER STATE BANK OF INDIA TECHNOLIGIES LTD AKSHATA LAXMAN SHIPPING 4 2017MBARG104 TATA MOTERS LTD NAYAK CORPORATION LTD GREAT EASTERN 5 2017MBARG105 AMAL S V RAJESH EXPORT LTD SHIPPING LTD 6 2017MBARG107 ANUSH RAJ BHARATH PETROLIUM KARNATAKA BANK LTD ARPITA NAGAPPA OIL AND NATURAL GAS 7 2017MBARG108 D S M SHRIRAM LTD HOSALLI CORPORATION LTD 8 2017MBARG109 ARUN RAJ COAL INDIA LTD ASAHI INDIA GLASS LTD TATA CONSULTENCY 9 2017MBARG110 AZEEM SHESHAD N M SPML INFRA LTD SERVICE LTD AZIZAHMAD IBRAHIM UNITED BANK OF INDIA 10 2017MBARG111 P & G LTD TANJI LTD 11 2017MBARG112 CHETHANA TATA STEEL LTD CEAT LTD LARSEN AND TOUBRO INFINITE COMPUTER 12 2017MBARG113 DEEKSHITH POOJARY LTD SOLUTIONS(INDIA LTD) HINDALCO INDUSTRIES PIDILITE INDUSTRIES 13 2017MBARG114 DEEPIKA P LTD LTD 14 2017MBARG115 DENSIL GEORGE BHARTI AIRTEL LTD KUSHAL LTD 15 2017MBARG116 DHANYASHREE K HDFC BANK LTD CASTROL INDIA LTD MAHINDRA & 16 2017MBARG117 DILSHANA K AIA ENGINEERING LTD MAHINDRA LTD FATHIMATH RAHEEMA ENDURANCE 17 2017MBARG118 NTPC LTD K TECHNOLOGY MAHINDRA CIE 18 2017MBARG119 FREDIN DOMINIC RELIANCE POWER LTD AUTOMOTIVE LTD GAYATRI GAJANANA RAYMOND COMPANY 19 2017MBARG120 INFOSYS LTD PAI LTD MARUTI SUZUKI INDIA AMARA -

Sharekhan Special August 31, 2021

Sharekhan Special August 31, 2021 Index Q1FY2022 Results Review Automobiles • Capital Goods • Consumer Discretionary • Consumer Goods • Infrastructure/Cement/Logistics/Building Material • IT • Oil & Gas • Pharmaceuticals • Agri Inputs and Speciality Chemical • Miscellaneous • Visit us at www.sharekhan.com For Private Circulation only Q1FY2022 Results Review In-line quarter, healthy outlook Results Review Results Summary: After ending FY2021 on a strong note, Q1FY2022 earnings of broader indices showed a promising start (Nifty/ Sensex companies’ PAT rose 100%/66% y-o-y) in the new fiscal with strong growth momentum on low base. Management commentaries on earnings outlook remained positive, on improving economic activity post second COVID-19 wave and anticipation of strong demand revival. Demand recovery and ramp-up of vaccinations look encouraging. We expect economic activity to increase in the upcoming festive season. Nifty trades at 23x and 20x EPS based on FY2022E/FY2023E EPS, at a premium to mean average. Valuation gap between large and mid-caps has shrunk, we advise investors to focus on stocks with strong earnings growth potential with reasonable valuation. High-conviction investment ideas: o Large-caps: Infosys, ICICI Bank, M&M, L&T, UltraTech, SBI, HDFC Ltd, Godrej Consumer Products, Divis Labs and Titan. o Mid-caps: NAM India, BEL, Gland Pharma, Dalmia Bharat, Laurus Labs, Max Financial Services, LTI. o Small-caps: TCI Express, Kirloskar Oil, Suprajit Engineering, Repco Home Finance, PNC Infratech, Mahindra Lifespaces, Birlasoft. After ending FY2021 on a strong note, Q1FY2022 corporate earnings of broader indices showed a promising start with continued strong growth momentum on the low base of Q1FY2021, though it was along the expected lines.