Indigo Paints Ltd

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Reconciliation of Share Capital for Quarter Ended June

a! INDIGO Be surprised! Date: July 12, 2021 TO), To BSE Limited National Stock Exchange of India Limited Corporate Relationship Department Exchange Plaza, Plot No. C-1, Block G, 25" Floor, Phiroze Jeejeebhoy Towers, Bandra Kurla Complex, Bandra (East) Dalal Street, Mumbai- 400001 Mumbai -400051 Scrip Code: 543258 NSE Symbol: INDIGOPNTS Sub: Submission of Reconciliation of Share Capital Audit Report under Regulation 76 of SEBI (Depositories and Participants) Regulations, 2018 for the quarter ended June 30, 2021. Dear Sir/Madam, Please find enclosed herewith Reconciliation of Share Capital Audit Report for the quarter ended June 30, 2021 as per Regulation 76 of The Securities and Exchange Board of India (Depositories and Participants) Regulations, 2018 for Indigo Paints Limited. Kindly acknowledge and take the same on record. Thanking You For Indigo Paints Limited Company Secretary & Comp e Officer Enel: As above Registered Office: INDIGO Paints Limited (Formerly INDIGO Paints Pvt Ltd), Indigo Tower, Street- 5, Pallod Farm - 2, Baner Road, Pune 411045, Maharashtra T: +91 20 6681 4300, Email: [email protected], Website: www.indigopaints.com, CIN: U24114PN2000PLCO14669 F7WNAWAUIUS N\A Lb f. BAPAT GAIKWAD AND ASSOCIATES COMPANY SECRETARIES To, The Board of Directors, Indigo Paints Limited Indigo Tower, Street-5, Pallod Farm-2, Baner Road Pune- 411045 CERTIFICATE We have examined the relevant books, documents, register of members, beneficiary details produced before us by the depositories and other records/documents maintained by Link Intime India Private Limited, having its registered office situated at C-101, 1st Floor, 247 Park, Lat Bahadur Shastri Marg, Vikhroli (West) Mumbai- 400083, Registrar and Share transfer agent of Indigo Paints Limited (‘The Company’), in respect of Reconciliation of Share Capital Audit as per Regulation 76 of the Securities and Exchange Board of India (Depositories and Participants) Regulations, 2018. -

Model Portfolio Update

Model Portfolio update January 21, 2016 LatestDeal Team Model – PortfolioAt Your Service Large cap Midcap Name of the company Weightage(%) Name of the company Weightage(%) Auto 14 Aviation 6 Tata Motor DVR 4 Interglobe Aviation 6 Bosch 3 Auto 6 Maruti 4 Bharat Forge 6 EICHER Motors 3 BFSI 6 BFSI 23 BjjFiBajaj Finserve 6 HDFC Bank 8 Capital Goods 6 Axis Bank 3 HDFC 8 Bharat Electronics 6 Bajaj Finance 4 Cement 6 Capital Goods 5 Ramco Cement 6 L & T 5 Consumer 24 Cement 3 Symphony 6 UltraTech Cement 3 Supreme Ind 6 FMCG/Consumer 14 Kansai Nerolac 6 ITC 7 Pidilite 6 United Spirits 2 FMCG 8 Asian Paints 5 Nestle 8 IT 21 Infrastructure 8 Infosys 10 NBCC 8 TCS 8 Oil & Gas 6 Wipro 3 Meida 2 CtlCastrol 6 Zee Entertainment 2 Logistics 6 Metal 2 Container Corporation of India 6 Tata Steel 2 Pharma 12 Oil & Gas 4 Natco Pharma 6 Reliance Industries 4 Torrent Pharma 6 Pharma 12 Textile 6 Lupin 5 Arvind 6 Dr Reddys 4 Total 100 Aurobindo Pharma 3 Total 100 • Exclusion - Eicher Motors, Bajaj Finance (transferred to large cap), PVR, • Exclusion- State Bank of India, Bharti Airtel and ONGC CARE, Cummins & Shree Cement • Inclusion – Eicher Motors, Bajaj Finance (transferred from midcap), Wipro, • Inclusion – Ramco Cement, Bajaj Finserv, Supreme Industries, Indigo, Reliance Industries & Aurobindo Pharma Pidilite, Bharat Electronics and Bharat Forge Source: Bloomberg, ICICIdirect.com Research *Diversified portfolio - Combination of 70% large cap and 30% midcap portfolio OutperformanceDeal Team – At continues Your Service across all portfolios… • Our indicative large cap equity model portfolio (“Quality -20”) has • In the large cap space we continue to remain positive on pharma & IT. -

Annexure to the Board Report | L&T Annual Report 2019-20

Annexure ‘A’ to the Board Report and EnPI reduction of CG moulding energy consumption. Information as required to be given under Section 134(3) zz Implemented Smart COMM Energy Management (m) read with Rule 8(3) of the Companies (Accounts) system at ASW & Digital Dashboard. Rules, 2014. zz Replacement of conventional light fittings with [A] CONSERVATION OF ENERGY: Solar lighting system in SSII, Open yard-5 and (i) Steps taken or impact on conservation of Grit blasting & painting areas at Production/ energy: Utility areas at EWL Kancheepuram factory and Kansbahal works. zz Implementation of LED lights in HE-Hazira campus and other project sites and Solar Pipes in zz Replacement of conventional MH Lamps and SG fabrication area. fluorescent tube lights by LED lamps in working areas at office and projects as well as for street zz Installation of an Off Grid Mini-Solar Power Plant for meeting the energy requirement of site & lights. workmen habitats at Ranchi Smart City Project. zz Installation of energy efficient water coolers and submersible pumps zz Installed Local Pre/ Post Weld Heat Treatment (PWHT) using PID Technology which ensures zz Replacing existing aged inefficient Split AC units uniform heating and reduction in energy with energy efficient units wastage. zz Utilization of Chiller for HVAC System – Campus zz Implemented the use of Metal Halide (400 Watt) FMD initiated and control the chiller running EOT Crane under bay lights with LED Lights. hour for HVAC need during holidays and extended working hours. zz Installed Energy efficient burners for Furnaces and pre heating. zz Initiative has been taken for replacement of Air-Cooled Chiller with Water Cooled Chiller. -

List of Nodal Officer

List of Nodal Officer Designa S.No tion of Phone (With Company Name EMAIL_ID_COMPANY FIRST_NAME MIDDLE_NAME LAST_NAME Line I Line II CITY PIN Code EMAIL_ID . Nodal STD/ISD) Officer 1 VIPUL LIMITED [email protected] PUNIT BERIWALA DIRT Vipul TechSquare, Golf Course Road, Sector-43, Gurgaon 122009 01244065500 [email protected] 2 ORIENT PAPER AND INDUSTRIES LTD. [email protected] RAM PRASAD DUTTA CSEC BIRLA BUILDING, 9TH FLOOR, 9/1, R. N. MUKHERJEE ROAD KOLKATA 700001 03340823700 [email protected] COAL INDIA LIMITED, Coal Bhawan, AF-III, 3rd Floor CORE-2,Action Area-1A, 3 COAL INDIA LTD GOVT OF INDIA UNDERTAKING [email protected] MAHADEVAN VISWANATHAN CSEC Rajarhat, Kolkata 700156 03323246526 [email protected] PREMISES NO-04-MAR New Town, MULTI COMMODITY EXCHANGE OF INDIA Exchange Square, Suren Road, 4 [email protected] AJAY PURI CSEC Multi Commodity Exchange of India Limited Mumbai 400093 0226718888 [email protected] LIMITED Chakala, Andheri (East), 5 ECOPLAST LIMITED [email protected] Antony Pius Alapat CSEC Ecoplast Ltd.,4 Magan Mahal 215, Sir M.V. Road, Andheri (E) Mumbai 400069 02226833452 [email protected] 6 ECOPLAST LIMITED [email protected] Antony Pius Alapat CSEC Ecoplast Ltd.,4 Magan Mahal 215, Sir M.V. Road, Andheri (E) Mumbai 400069 02226833452 [email protected] 7 NECTAR LIFE SCIENCES LIMITED [email protected] SUKRITI SAINI CSEC NECTAR LIFESCIENCES LIMITED SCO 38-39, SECTOR 9-D CHANDIGARH 160009 01723047759 [email protected] 8 ECOPLAST LIMITED [email protected] Antony Pius Alapat CSEC Ecoplast Ltd.,4 Magan Mahal 215, Sir M.V. Road, Andheri (E) Mumbai 400069 02226833452 [email protected] 9 SMIFS CAPITAL MARKETS LTD. -

Havells India (HAVIND)

Havells India (HAVIND) CMP: | 1031 Target: | 1215 (18%) Target Period: 12 months BUY May 22, 2021 Strong recovery across product segments... Havells continued its growth momentum in Q4FY21 with topline growth of 50% YoY in line with our estimate of 48%. The company witnessed strong Particulars revenue growth in all business verticals cables, switchgears, electrical Particular Amount consumer durable (ECD), Lloyd, lightings and others by 51%, 53%, 71%, Market Capitalization (| Cr) 64,324.1 29%, 40% and 71%, respectively. The management reiterated market share Total Debt (FY21) (| Cr) 393.7 gains, strong demand traction in rural helped drive sales recovery for Havells Cash and Inv (FY21) (| Cr) 1,931.0 India in Q4 and in FY21. The company reported ~11% topline growth in EV (| Cr) 62,786.7 FY21 despite a washout in Q1. The key takeaways from conference call are: 52 week H/L 1238 / 454 Equity capital (| Cr) 62.6 Update Result 1) strong sales traction in first two weeks of April 2021 before lockdown Face value (|) 1.0 sseSFsfsf imposed in many states, 2) May sales hit by lockdown across the country, 3) price hikes of 10% in fans and 45-50% in cable business to offset Price Performance sseSFsfsf inflationary pressure, 4) focus on capacity building of Lloyd (future launches in refrigerators and washing machines categories), 5) focus on tapping rural 1400 20000 1200 and semi urban markets for the long term. However, considering lockdowns 1000 15000 and higher input prices, we revise our FY22E revenue, PAT estimate 800 10000 downward by ~7%, 6%, respectively. 600 400 5000 200 Strong b/s helps navigate challenging scenario 0 0 Havells India reported revenue, PAT CAGR of ~13%, ~15%, respectively, in Oct-18 Apr-21 Jan-20 Jun-20 Dec-17 Nov-20 Aug-19 Mar-19 the last 10 years with EBITDA margin expansion of 200 bps YoY to 15%. -

Avenue Supermarts (DMART IN)

Avenue Supermarts (DMART IN) Rating: BUY | CMP: Rs3,378 | TP: Rs3,686 July 10, 2021 Rising Footfalls, Online scalability Positive Q1FY22 Result Update Quick Pointers: Change in Estimates | ☑ Target | Reco . Q1FY22 saw a stronger second wave resulting in loss of more days or higher restriction on number of hours of store operations. Change in Estimates Current Previous . No significant impact on supply chain during the quarter, Inventory moving FY22E FY23E FY22E FY23E Rating BUY BUY towards normal levels. Target Price 3,686 3,366 Sales (Rs. m) 2,89,846 4,08,606 2,89,846 4,08,606 D’Mart 1Q results depicted impact of a strong second wave with business % Chng. - - EBITDA (Rs. m) 23,781 37,290 23,781 37,290 loss of more days (versus last year) and higher restriction on operating hours % Chng. - - /non-essential sales. However, rising footfalls, vaccination drive, 203% sales EPS (Rs.) 22.5 36.0 22.5 36.0 % Chng. - - growth in D’Mart ready and work on new store openings is positive. Key Financials - Consolidated Despite near term challenges we remain optimistic about the long term Y/e Mar FY20 FY21 FY22E FY23E potential of D’Mart on back of 1) Increasing scale and scope D’Mart Ready 2) Sales (Rs. m) 2,48,702 2,41,431 2,89,846 4,08,606 Extending offerings on D’Mart ready app to include general merchandise, EBITDA (Rs. m) 21,284 17,431 23,781 37,290 fresh food and vegetable 3) Growth in General merchandise sales over lower Margin (%) 8.6 7.2 8.2 9.1 PAT (Rs. -

Vat 7Anaaatauannnanry Ss

ay winiac Be surprised! Date: 14 May, 2021 To, To BSE Limited National Stock Exchange of India Limited Corporate Relationship Department Exchange Plaza, Plot No. C-1, Block G, 25" Floor, Phiroze Jeejeebhoy Towers, Bandra Kurla Complex, Bandra (East) Dalal Street, Mumbai- 400001 Mumbai -400051 Scrip Code: 543258 NSE Symbol: INDIGOPNTS Dear Sir, Sub: Press Release- Unaudited Financial Results of the Company along with the Limited Review Report thereon for the quarter and nine month ended on 3lst December, 2020. Pursuant to regulation 30 of Securities and Exchange Board of India (Listing Obligations and Disclosure Requirements) Regulations, 2015 (‘Listing Regulations’), we have attached herewith a copy of the Press Release that is being issued by the Company today, in connection with the above captioned subject. Please take the above information on record. Thanking you. Yours faithfully, For Indigo Paints Limit Company Secretary & Compliance Officer Encl — As above Registered Office: INDIGO Paints L i m i t e d (Formerly INDIGO P a i n t s P v t L t d ) , Indigo T o w e r , Street - 5 , Pallod F a r m- 2 , B a n e r R o a d , Pune 4 1 1 0 4 5 , Maharashtra T . + 9 1 20 6681 4 3 0 0 , Email: [email protected], Website: www.indigopaints.com, VAT 7ANAAATAUANNNANRY CIN: U24114PN2000PLCO SS 14669 Olyee a Press Release Financial Results for the quarter and nine month ended 31° December 2020. Highlights of the Results: a. Net Revenue from Operations for the quarter ended December 31, 2020 was Rs 209.64 crores as against Rs. -

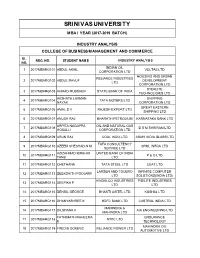

Srinivas University M Ba I Year (2017-2019 Batch)

SRINIVAS UNIVERSITY M BA I YEAR (2017-2019 BATCH) INDUSTRY ANALYSIS COLLEGE OF BUSINESS MANAGEMENT AND COMMERCE SL . REG. NO. STUDENT NAM E INDUSTRY ANALYSIS NO. INDIAN OIL 1 2017MBARG101 ABDUL AKHIL VOLTAS LTD CORPORATION LTD HOUSING AND URBAN RELIANCE INDUSTRIES 2 2017MBARG102 ABDUL RAVUF DEVELOPMENT LTD CORPORATION LTD STERLITE 3 2017MBARG103 AHMAD MUBSHER STATE BANK OF INDIA TECHNOLIGIES LTD AKSHATA LAXMAN SHIPPING 4 2017MBARG104 TATA MOTERS LTD NAYAK CORPORATION LTD GREAT EASTERN 5 2017MBARG105 AMAL S V RAJESH EXPORT LTD SHIPPING LTD 6 2017MBARG107 ANUSH RAJ BHARATH PETROLIUM KARNATAKA BANK LTD ARPITA NAGAPPA OIL AND NATURAL GAS 7 2017MBARG108 D S M SHRIRAM LTD HOSALLI CORPORATION LTD 8 2017MBARG109 ARUN RAJ COAL INDIA LTD ASAHI INDIA GLASS LTD TATA CONSULTENCY 9 2017MBARG110 AZEEM SHESHAD N M SPML INFRA LTD SERVICE LTD AZIZAHMAD IBRAHIM UNITED BANK OF INDIA 10 2017MBARG111 P & G LTD TANJI LTD 11 2017MBARG112 CHETHANA TATA STEEL LTD CEAT LTD LARSEN AND TOUBRO INFINITE COMPUTER 12 2017MBARG113 DEEKSHITH POOJARY LTD SOLUTIONS(INDIA LTD) HINDALCO INDUSTRIES PIDILITE INDUSTRIES 13 2017MBARG114 DEEPIKA P LTD LTD 14 2017MBARG115 DENSIL GEORGE BHARTI AIRTEL LTD KUSHAL LTD 15 2017MBARG116 DHANYASHREE K HDFC BANK LTD CASTROL INDIA LTD MAHINDRA & 16 2017MBARG117 DILSHANA K AIA ENGINEERING LTD MAHINDRA LTD FATHIMATH RAHEEMA ENDURANCE 17 2017MBARG118 NTPC LTD K TECHNOLOGY MAHINDRA CIE 18 2017MBARG119 FREDIN DOMINIC RELIANCE POWER LTD AUTOMOTIVE LTD GAYATRI GAJANANA RAYMOND COMPANY 19 2017MBARG120 INFOSYS LTD PAI LTD MARUTI SUZUKI INDIA AMARA -

Indigo Paints Limited

January 18, 2021 IPO Note - SUBSCRIBE INDIGO PAINTS LIMITED Company Background Issue Details Incorporated in 2000, Indigo Paints Ltd (‘Indigo’) has rapidly scaled up its operations to become Fresh Issue of Equity Shares aggregating upto ₹ 300 Crore the fifth largest company in the Indian decorative paint industry in terms of revenues as on and Offer For Sale of 5,840,000 Equity Shares FY20. Indigo has created an extensive distribution network across 27 states and seven union territories. The company manufactures its products across three manufacturing facilities located Issue Highlights in Jodhpur (Rajasthan), Kochi (Kerala) and Pudukkottai (Tamil Nadu) with an aggregate estimated Net Issue Size: ₹ 1,168 – 1,169 Cr No. of Shares ('000): 7,856 – 7,853 installed production capacity of 101,903 kilo litres per annum (“KLPA”) for liquid paints and Face Value (₹): 10 93,118 metric tonnes per annum (“MTPA”) for putties and powder paints. The company has Employee Reservation: Upto 70,000 Equity Shares expanded its manufacturing capabilities to manufacture a complete range of decorative paints Price Band : ₹ 1,488 – 1,490 including emulsions, enamels, wood coatings, distempers, primers, putties and cement paints. Bid Lot: 10 Shares and in multiple thereof Indigo is the first company to manufacture and introduce certain differentiated products in Employee Discount: ₹ 148 /- per share the decorative paint market in India, which includes Metallic Emulsions, Tile Coat Emulsions, Issue Opens On: Wednesday, 20th Jan’2021 Bright Ceiling Coat Emulsions, Floor Coat Emulsions, Dirtproof & Waterproof Exterior Laminates, Issue Closes On: Friday, 22nd Jan’2021 Post Issue Implied Exterior and Interior Acrylic Laminates, and PU Super Gloss Enamel (together, “Indigo ₹ 7,079 – 7,088 Cr Market Cap Differentiated Products”). -

Sharekhan Special August 31, 2021

Sharekhan Special August 31, 2021 Index Q1FY2022 Results Review Automobiles • Capital Goods • Consumer Discretionary • Consumer Goods • Infrastructure/Cement/Logistics/Building Material • IT • Oil & Gas • Pharmaceuticals • Agri Inputs and Speciality Chemical • Miscellaneous • Visit us at www.sharekhan.com For Private Circulation only Q1FY2022 Results Review In-line quarter, healthy outlook Results Review Results Summary: After ending FY2021 on a strong note, Q1FY2022 earnings of broader indices showed a promising start (Nifty/ Sensex companies’ PAT rose 100%/66% y-o-y) in the new fiscal with strong growth momentum on low base. Management commentaries on earnings outlook remained positive, on improving economic activity post second COVID-19 wave and anticipation of strong demand revival. Demand recovery and ramp-up of vaccinations look encouraging. We expect economic activity to increase in the upcoming festive season. Nifty trades at 23x and 20x EPS based on FY2022E/FY2023E EPS, at a premium to mean average. Valuation gap between large and mid-caps has shrunk, we advise investors to focus on stocks with strong earnings growth potential with reasonable valuation. High-conviction investment ideas: o Large-caps: Infosys, ICICI Bank, M&M, L&T, UltraTech, SBI, HDFC Ltd, Godrej Consumer Products, Divis Labs and Titan. o Mid-caps: NAM India, BEL, Gland Pharma, Dalmia Bharat, Laurus Labs, Max Financial Services, LTI. o Small-caps: TCI Express, Kirloskar Oil, Suprajit Engineering, Repco Home Finance, PNC Infratech, Mahindra Lifespaces, Birlasoft. After ending FY2021 on a strong note, Q1FY2022 corporate earnings of broader indices showed a promising start with continued strong growth momentum on the low base of Q1FY2021, though it was along the expected lines. -

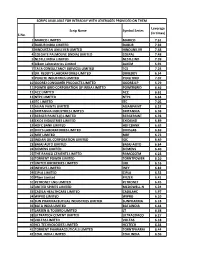

S.No. Scrip Name Symbol Series Leverage (In Times) 1 MARICO

SCRIPS AVAILABLE FOR INTRADAY WITH LEVERAGES PROVIDED ON THEM Leverage Scrip Name Symbol Series (in times) S.No. 1 MARICO LIMITED MARICO 7.61 2 DABUR INDIA LIMITED DABUR 7.92 3 HINDUSTAN UNILEVER LIMITED HINDUNILVR 7.48 4 COLGATE PALMOLIVE (INDIA) LIMITED COLPAL 7.48 5 NESTLE INDIA LIMITED NESTLEIND 7.39 6 Alkem Laboratories Limited ALKEM 6.91 7 TATA CONSULTANCY SERVICES LIMITED TCS 7.24 8 DR. REDDY'S LABORATORIES LIMITED DRREDDY 6.54 9 PIDILITE INDUSTRIES LIMITED PIDILITIND 7.07 10 GODREJ CONSUMER PRODUCTS LIMITED GODREJCP 5.79 11 POWER GRID CORPORATION OF INDIA LIMITED POWERGRID 6.46 12 ACC LIMITED ACC 6.61 13 NTPC LIMITED NTPC 6.64 14 ITC LIMITED ITC 7.05 15 ASIAN PAINTS LIMITED ASIANPAINT 6.52 16 BRITANNIA INDUSTRIES LIMITED BRITANNIA 6.98 17 BERGER PAINTS (I) LIMITED BERGEPAINT 6.78 18 EXIDE INDUSTRIES LIMITED EXIDEIND 6.89 19 HDFC BANK LIMITED HDFCBANK 6.63 20 DIVI'S LABORATORIES LIMITED DIVISLAB 6.69 21 MRF LIMITED MRF 6.73 22 INDIAN OIL CORPORATION LIMITED IOC 6.49 23 BAJAJ AUTO LIMITED BAJAJ-AUTO 6.64 24 SIEMENS LIMITED SIEMENS 6.40 25 THE RAMCO CEMENTS LIMITED RAMCOCEM 6.23 26 TORRENT POWER LIMITED TORNTPOWER 6.10 27 UNITED BREWERIES LIMITED UBL 6.16 28 INFOSYS LIMITED INFY 6.82 29 CIPLA LIMITED CIPLA 6.52 30 Pfizer Limited PFIZER 6.41 31 PETRONET LNG LIMITED PETRONET 6.45 32 UNITED SPIRITS LIMITED MCDOWELL-N 6.24 33 CADILA HEALTHCARE LIMITED CADILAHC 5.97 34 WIPRO LIMITED WIPRO 6.10 35 SUN PHARMACEUTICAL INDUSTRIES LIMITED SUNPHARMA 6.18 36 BATA INDIA LIMITED BATAINDIA 6.44 37 LARSEN & TOUBRO LIMITED LT 6.38 38 ULTRATECH CEMENT -

Consumer Durables22apr21

Consumer Durables Sector Update April 26, 2021 PLI to foster component ecosystem Government has approved the Production Linked Incentive (PLI) Scheme for Air Conditioners and LED Lights to be implemented over FY22 to FY29 with a PL Universe budgetary outlay of Rs62.4bn (4-6% incentive on incremental sales over base year FY20). Given the contours of the scheme, we believe this shall promote Companies Rating CMP (Rs) TP (Rs) onshore manufacturing of critical components like Compressors, Motors, PCBs, LED chips amongst others. We remain unsure on the participation of Bajaj Electricals BUY 1,135 1,033 CG Cons. Elec. BUY 354 447 local brands like Voltas, Havells etc. given the capital intensive nature and Havells India Hold 1,006 1,128 need of large economies of scale for these components. Nevertheless, Polycab India BUY 1,485 1,480 creation of a robust component ecosystem by ancillary entities remains a Voltas Hold 939 1,000 positive for brands as it shall help 1) accelerate import substitution and 2) Source: PL shrink lead times thereby reducing working capital requirements. We continue to maintain our positive stance on consumer durables space given huge penetration scope and market consolidation. Amongst our coverage universe, Voltas/ Lloyd (Havells) stand to benefit from AC PLI while Crompton, Havels, Bajaj and Polycab to benefit from the LED Lights PLI. Key Highlights of the Scheme: . To incentivize manufacturing of components of Air Conditioners and LED Lights over FY22-FY29 with a budgetary outlay of Rs62.4bn. Categories within Air Conditioner: . AC Components: High Value Intermediates or Low Value Intermediates or Sub-assemblies or a Combination thereof .