Result Review

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Download Full Report

CONTENTS 02 Unstoppable Corporate overview We have been persistent 02 Unstoppable in our aim to establishing 04 Chairman’s Message and maintaining market leadership to be able to achieve 06 Vice Chairman’s Message unprecedented growth for our 08 Board of Directors stakeholders. 10 Management Board 12 Key Performance Highlights 14 14 Integrated Report Integrated Report 28 Management Discussion & Analysis Apollo Tyres’ contribution 51 Sustainability Snapshot to social and economic development is critical to create and sustain an enabling environment for investment. This has enabled the Company’s positioning as a credible Statutory Reports stakeholder partner. 84 Board’s Report 95 Annual Report on CSR 28 102 Business Responsibility Report Management 126 Corporate Governance Report Discussion & Analysis Financial Statements 161 Standalone Financial Statements 223 Consolidated Financial Statements UNSTOPPABLE Since inception, we have worked towards establishing ourselves as a leading player in the sale and manufacture of tyres. We have been persistent in our aim to establishing and maintaining market leadership and be able to achieve unprecedented growth for our stakeholders. In FY2018-19 (FY2019), we continued to focus We are unstoppable in establishing our on our key revenue generating regions APMEA leadership across multiple segments. (Asia Pacific, Middle East and Africa, including Our consistently advancing product range coupled India) and Europe. We expanded our presence in with product innovations are enabling us to achieve Americas by added new territories and increasing the same. our value proposition. The APMEA operation continued its focus on consolidating its leadership We are unstoppable in working towards achieving and enhancing share in India through the cutting edge manufacturing capabilities and introduction of best in class and technologically world-class R&D. -

IN the BUSINESS of PROGRESS CONTENTS Apollo Tyres in Brief

Annual Report 2019-20 IN THE BUSINESS OF PROGRESS CONTENTS Apollo Tyres in brief 01-03 Apollo Tyres is one of the most trusted Corporate factsheet names in the manufacture and sale of tyres. The Company was founded in 1972 and is 04-13 headquartered in Gurugram, Haryana (India). Leadership and governance 06 Chairman’s message 08 Vice-Chairman’s message 10 Board of Directors Catering to all tyre segments 12 Management Team TRUCK AND BUS LIGHT TRUCK 14-77 Performance and progress 16 Key performance indicators 18 Know our capitals 20 Business model 22 Capital-wise information 36 Progress amidst volatility 38 Progress that is sustainable 40 Progress through people centricity 42 Value created for the stakeholders PASSENGER VEHICLES TWO-WHEELER 78-93 Management Discussion & Analysis 94-170 Statutory Reports 94 Board’s Report 107 Annual Report on CSR 113 Business Responsibility Report 138 Corporate Governance Report OFF-HIGHWAY 171-305 Financial Statements 171 Standalone 233 Consolidated Apollo Tyres’ success as a leading tyre such as: geo-political relations, economic manufacturer is inextricably linked with the growth, industry cyclicality, environmental progress of the people, the businesses we issues, technological innovation, safety and partner and the planet at large. We have consumer attitudes. Our FY20 performance is always persevered to exceed expectations, a reflection of the resulting uncertainties. It set new benchmarks and in some cases, is also a testament to our foundational values shape the future of the industry. and intrinsic strengths that have helped us navigate through these uncertainties. Our marquee brands, Apollo and Vredestein, enjoy premium positions in the commercial As we step into a new decade, replete with and passenger vehicle tyre segments in unexplored opportunities, we are keen on India and Europe, respectively. -

Annexure to the Board Report | L&T Annual Report 2019-20

Annexure ‘A’ to the Board Report and EnPI reduction of CG moulding energy consumption. Information as required to be given under Section 134(3) zz Implemented Smart COMM Energy Management (m) read with Rule 8(3) of the Companies (Accounts) system at ASW & Digital Dashboard. Rules, 2014. zz Replacement of conventional light fittings with [A] CONSERVATION OF ENERGY: Solar lighting system in SSII, Open yard-5 and (i) Steps taken or impact on conservation of Grit blasting & painting areas at Production/ energy: Utility areas at EWL Kancheepuram factory and Kansbahal works. zz Implementation of LED lights in HE-Hazira campus and other project sites and Solar Pipes in zz Replacement of conventional MH Lamps and SG fabrication area. fluorescent tube lights by LED lamps in working areas at office and projects as well as for street zz Installation of an Off Grid Mini-Solar Power Plant for meeting the energy requirement of site & lights. workmen habitats at Ranchi Smart City Project. zz Installation of energy efficient water coolers and submersible pumps zz Installed Local Pre/ Post Weld Heat Treatment (PWHT) using PID Technology which ensures zz Replacing existing aged inefficient Split AC units uniform heating and reduction in energy with energy efficient units wastage. zz Utilization of Chiller for HVAC System – Campus zz Implemented the use of Metal Halide (400 Watt) FMD initiated and control the chiller running EOT Crane under bay lights with LED Lights. hour for HVAC need during holidays and extended working hours. zz Installed Energy efficient burners for Furnaces and pre heating. zz Initiative has been taken for replacement of Air-Cooled Chiller with Water Cooled Chiller. -

The Indian Automotive Supplier Report Supplierbusiness

IHS AUTOMOTIVE The Indian Automotive Supplier Report SupplierBusiness 2015 edition supplierbusiness.com REGIONAL REPORT Indian Subcontinent SAMPLE IHS Automotive | Supplying Ford Contents Executive Summary 4 – Renault-Nissan third largest exporter 30 – Tata’s exports expected to decrease 30 Indian Economy and Business Environment 6 – Ford ups capacity in India to boost exports 30 Volatile GDP growth in BRICS 7 – Volkswagen increases exports from India 31 Per capita GDP seen rising 8 – Honda to grow exports from India 31 Inflation in check, for now 8 – GM to turn India into a global export hub 31 Consumer demand expected to improve 9 Foreign investments going up 9 Overview of Automotive Supplier Industry 32 Industrial production recovers 10 Speed bumps 33 Shrinking exports, a cause for concern 10 Positive sentiment returns 33 Indian currency expected to depreciate mildly in 2015, – Engine parts, the largest segment 33 2016 11 – AMT to gain traction 34 – Chassis production 35 The Indian Automotive Market 13 – Interiors production 35 – Maruti Suzuki boosts sales with new models 14 – Exteriors production 35 – Hyundai increases market share 15 – Thermal component production 35 – Mahindra stays leader of SUV segment 16 – Market share of HVAC systems suppliers 36 – Tata Motors plans to reclaim lost ground 16 – The proliferation of car security systems 36 – Honda strengthens position in India with diesel cars Top 10 automotive suppliers in India 36 17 – Motherson Sumi System Limited 37 Key trends in the Indian LV market 18 – Amtek Auto 37 – Hatchback -

Asian Daily EPS, TP and Rating Changes Top of the Pack

Thursday, 13 February 2014 (Global Edition) Asian Daily EPS, TP and Rating changes Top of the pack ... EPS TP (% change) T+1 T+2 Chg Up/Dn Rating Commonwealth Bank 3 2 0 0 U (U) Asia Equity Strategy Sakthi Siva (3) Australia New report: Cyclicals have outperformed defensives YTD. Continue? China Mengniu Dairy (6) (7) 20 25 O (O) PRADA S.p.A. (10) (12) (5) 29 O (O) India IT Services Sector Anantha Narayan (4) Apollo Tyres 8 2 10 22 O (O) Is it too crowded for further performance? Cipla Limited (6) 0 0 1 N (N) Jaiprakash Power Ventures (60) (17) (14) 107 O (O) Page Industries 3 3 2 13 O (O) Asia Technology Sector Keon Han (5) Perusahaan Gas Negara (1) 1 2 31 O (O) New report: LED—entering expansion phase Softbank 0 0 — R (R) UMW Oil & Gas 0 (7) 31 3 N (N) China Mengniu Dairy (2319.HK) – Maintain O Kevin Yin (6) Universal Robina Corp. 1 1 0 18 O (O) 2014 outlook: Should pass through 10% raw milk price inflation; EPS likely to grow 35.9% YoY Huaku Development (3) (1) (5) 32 O (O) Novatek Microelectronics 3 1 3 (18) U (U) CS pic of the day Sinopac Holdings 2 2 3 8 N (N) AIS PCL (4) (7) (4) 29 O (O) Global general lighting and LED lighting market size Siam City Cement 0 (2) (5) 0 U (U) The LED general lighting industry is now shifting from the initial penetration phase to a rapid expansionary TAC PCL 0 0 0 44 O (O) phase. -

List of Nodal Officer

List of Nodal Officer Designa S.No tion of Phone (With Company Name EMAIL_ID_COMPANY FIRST_NAME MIDDLE_NAME LAST_NAME Line I Line II CITY PIN Code EMAIL_ID . Nodal STD/ISD) Officer 1 VIPUL LIMITED [email protected] PUNIT BERIWALA DIRT Vipul TechSquare, Golf Course Road, Sector-43, Gurgaon 122009 01244065500 [email protected] 2 ORIENT PAPER AND INDUSTRIES LTD. [email protected] RAM PRASAD DUTTA CSEC BIRLA BUILDING, 9TH FLOOR, 9/1, R. N. MUKHERJEE ROAD KOLKATA 700001 03340823700 [email protected] COAL INDIA LIMITED, Coal Bhawan, AF-III, 3rd Floor CORE-2,Action Area-1A, 3 COAL INDIA LTD GOVT OF INDIA UNDERTAKING [email protected] MAHADEVAN VISWANATHAN CSEC Rajarhat, Kolkata 700156 03323246526 [email protected] PREMISES NO-04-MAR New Town, MULTI COMMODITY EXCHANGE OF INDIA Exchange Square, Suren Road, 4 [email protected] AJAY PURI CSEC Multi Commodity Exchange of India Limited Mumbai 400093 0226718888 [email protected] LIMITED Chakala, Andheri (East), 5 ECOPLAST LIMITED [email protected] Antony Pius Alapat CSEC Ecoplast Ltd.,4 Magan Mahal 215, Sir M.V. Road, Andheri (E) Mumbai 400069 02226833452 [email protected] 6 ECOPLAST LIMITED [email protected] Antony Pius Alapat CSEC Ecoplast Ltd.,4 Magan Mahal 215, Sir M.V. Road, Andheri (E) Mumbai 400069 02226833452 [email protected] 7 NECTAR LIFE SCIENCES LIMITED [email protected] SUKRITI SAINI CSEC NECTAR LIFESCIENCES LIMITED SCO 38-39, SECTOR 9-D CHANDIGARH 160009 01723047759 [email protected] 8 ECOPLAST LIMITED [email protected] Antony Pius Alapat CSEC Ecoplast Ltd.,4 Magan Mahal 215, Sir M.V. Road, Andheri (E) Mumbai 400069 02226833452 [email protected] 9 SMIFS CAPITAL MARKETS LTD. -

Annual Report 2016-17

Annual Report 2016-17 apollotyres.com REACH Corporate Overview Introduction 1 Chairman’s Message 2 Vice Chairman’s Message 4 THE Board of Directors 6 Management Board 8 Performance Highlights 10 Management Discussion and 12 Analysis Report Sustainability Report 32 WORLD Statutory Reports Board’s Report 54 HIGHLIGHTS Annual Report on CSR 65 Business Responsibility Report 75 2016-17 Corporate Governance Report 98 Financial Statements `140.53 Bn Standalone Financial Statements 124 Gross Sales Consolidated Financial 194 Statements `39.02 Bn Capital Expenditure 15.8% ROE `10.99 Bn Net Profit `20.01 Bn EBITDA REACH india hungary WORLD where to next? At Apollo Tyres, we are building tyres for the future of transportation and mobility. As we do this, we are transforming ourselves both from a product and markets perspective. Building on our core competencies, strength and brand, we are aspiring to ‘Reach the World’, by manufacturing in different countries, expanding our distribution networks, and growing our brand associations. We are creating a distinctly ‘glocal’ culture in our organsiation, where we are thinking like a global organisation and yet, aligning ourselves to local needs in each geography we operate. At the same time, we are proud of being an Indian brand, and representing the best of technology, operations and thinking on the world stage. In FY17, we took many steps that furthered our aim of reaching the world. These include the inauguration of our Hungary plant and the Global R&D centre. These, however, are just stepping stones to achieving our cherished vision. As we do this, we are equally committed to ‘reach’ each of our stakeholders, and create value for them, in ways that are credible and meaningful. -

Sharekhan Special August 31, 2021

Sharekhan Special August 31, 2021 Index Q1FY2022 Results Review Automobiles • Capital Goods • Consumer Discretionary • Consumer Goods • Infrastructure/Cement/Logistics/Building Material • IT • Oil & Gas • Pharmaceuticals • Agri Inputs and Speciality Chemical • Miscellaneous • Visit us at www.sharekhan.com For Private Circulation only Q1FY2022 Results Review In-line quarter, healthy outlook Results Review Results Summary: After ending FY2021 on a strong note, Q1FY2022 earnings of broader indices showed a promising start (Nifty/ Sensex companies’ PAT rose 100%/66% y-o-y) in the new fiscal with strong growth momentum on low base. Management commentaries on earnings outlook remained positive, on improving economic activity post second COVID-19 wave and anticipation of strong demand revival. Demand recovery and ramp-up of vaccinations look encouraging. We expect economic activity to increase in the upcoming festive season. Nifty trades at 23x and 20x EPS based on FY2022E/FY2023E EPS, at a premium to mean average. Valuation gap between large and mid-caps has shrunk, we advise investors to focus on stocks with strong earnings growth potential with reasonable valuation. High-conviction investment ideas: o Large-caps: Infosys, ICICI Bank, M&M, L&T, UltraTech, SBI, HDFC Ltd, Godrej Consumer Products, Divis Labs and Titan. o Mid-caps: NAM India, BEL, Gland Pharma, Dalmia Bharat, Laurus Labs, Max Financial Services, LTI. o Small-caps: TCI Express, Kirloskar Oil, Suprajit Engineering, Repco Home Finance, PNC Infratech, Mahindra Lifespaces, Birlasoft. After ending FY2021 on a strong note, Q1FY2022 corporate earnings of broader indices showed a promising start with continued strong growth momentum on the low base of Q1FY2021, though it was along the expected lines. -

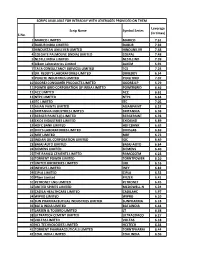

S.No. Scrip Name Symbol Series Leverage (In Times) 1 MARICO

SCRIPS AVAILABLE FOR INTRADAY WITH LEVERAGES PROVIDED ON THEM Leverage Scrip Name Symbol Series (in times) S.No. 1 MARICO LIMITED MARICO 7.61 2 DABUR INDIA LIMITED DABUR 7.92 3 HINDUSTAN UNILEVER LIMITED HINDUNILVR 7.48 4 COLGATE PALMOLIVE (INDIA) LIMITED COLPAL 7.48 5 NESTLE INDIA LIMITED NESTLEIND 7.39 6 Alkem Laboratories Limited ALKEM 6.91 7 TATA CONSULTANCY SERVICES LIMITED TCS 7.24 8 DR. REDDY'S LABORATORIES LIMITED DRREDDY 6.54 9 PIDILITE INDUSTRIES LIMITED PIDILITIND 7.07 10 GODREJ CONSUMER PRODUCTS LIMITED GODREJCP 5.79 11 POWER GRID CORPORATION OF INDIA LIMITED POWERGRID 6.46 12 ACC LIMITED ACC 6.61 13 NTPC LIMITED NTPC 6.64 14 ITC LIMITED ITC 7.05 15 ASIAN PAINTS LIMITED ASIANPAINT 6.52 16 BRITANNIA INDUSTRIES LIMITED BRITANNIA 6.98 17 BERGER PAINTS (I) LIMITED BERGEPAINT 6.78 18 EXIDE INDUSTRIES LIMITED EXIDEIND 6.89 19 HDFC BANK LIMITED HDFCBANK 6.63 20 DIVI'S LABORATORIES LIMITED DIVISLAB 6.69 21 MRF LIMITED MRF 6.73 22 INDIAN OIL CORPORATION LIMITED IOC 6.49 23 BAJAJ AUTO LIMITED BAJAJ-AUTO 6.64 24 SIEMENS LIMITED SIEMENS 6.40 25 THE RAMCO CEMENTS LIMITED RAMCOCEM 6.23 26 TORRENT POWER LIMITED TORNTPOWER 6.10 27 UNITED BREWERIES LIMITED UBL 6.16 28 INFOSYS LIMITED INFY 6.82 29 CIPLA LIMITED CIPLA 6.52 30 Pfizer Limited PFIZER 6.41 31 PETRONET LNG LIMITED PETRONET 6.45 32 UNITED SPIRITS LIMITED MCDOWELL-N 6.24 33 CADILA HEALTHCARE LIMITED CADILAHC 5.97 34 WIPRO LIMITED WIPRO 6.10 35 SUN PHARMACEUTICAL INDUSTRIES LIMITED SUNPHARMA 6.18 36 BATA INDIA LIMITED BATAINDIA 6.44 37 LARSEN & TOUBRO LIMITED LT 6.38 38 ULTRATECH CEMENT -

Momentum Pick

Momentum Picks Open Recommendations New recommendations Gladiator Stocks Date Scrip I-Direct Code Action Initiation Range Target Stoploss Duration 1-Oct-21 Nifty Nifty Sell 17520-17545 17482/17430 17583.00 Intraday Scrip Action 1-Oct-21 ONGC ONGC Buy 142.50-143.00 144.25/145.70 141.20 Intraday Hindalco Buy PICK MOMENTUM 1-Oct-21 UPL UPL Sell 707.00-708.00 700.60/693.80 714.60 Intraday Bata India Buy 30-Sep-21 Trent TRENT Buy 1010-1025 1125 948.00 30 Days HDFC Buy 30-Sep-21 Dhampur Sugar DHASUG Buy 290-294 312 282.00 07 Days Duration: 3 Months Click here to know more… Open recommendations Date Scrip I-Direct Code Action Initiation Range Target Stoploss Duration 29-Sep-21 SJVN SJVLIM Buy 28.3-29 31.50 27.00 14 Days 29-Sep-21 National Aluminium NATALU Buy 92-94 101.00 86.50 07 Days Intraday recommendations are for current month futures. Positional recommendations are in cash segment Retail Equity Research Retail – October 1, 2021 For Instant stock ideas: SUBSCRIBE to mobile notification on ICICIdirect Mobile app… Research Analysts Securities ICICI Dharmesh Shah Nitin Kunte, CMT Ninad Tamhanekar, CMT [email protected] [email protected] [email protected] Pabitro Mukherjee Vinayak Parmar [email protected] [email protected] NSE (Nifty): 17618 Technical Outlook NSE Nifty Daily Candlestick Chart Domestic Indices Day that was… Open High Low Close Indices Close 1 Day Chg % Chg Equity benchmarks concluded the monthly expiry session on a subdued note tracking mixed global cues. -

Annexure 1B 18416

Annexure 1 B List of taxpayers allotted to State having turnover of more than or equal to 1.5 Crore Sl.No Taxpayers Name GSTIN 1 BROTHERS OF ST.GABRIEL EDUCATION SOCIETY 36AAAAB0175C1ZE 2 BALAJI BEEDI PRODUCERS PRODUCTIVE INDUSTRIAL COOPERATIVE SOCIETY LIMITED 36AAAAB7475M1ZC 3 CENTRAL POWER RESEARCH INSTITUTE 36AAAAC0268P1ZK 4 CO OPERATIVE ELECTRIC SUPPLY SOCIETY LTD 36AAAAC0346G1Z8 5 CENTRE FOR MATERIALS FOR ELECTRONIC TECHNOLOGY 36AAAAC0801E1ZK 6 CYBER SPAZIO OWNERS WELFARE ASSOCIATION 36AAAAC5706G1Z2 7 DHANALAXMI DHANYA VITHANA RAITHU PARASPARA SAHAKARA PARIMITHA SANGHAM 36AAAAD2220N1ZZ 8 DSRB ASSOCIATES 36AAAAD7272Q1Z7 9 D S R EDUCATIONAL SOCIETY 36AAAAD7497D1ZN 10 DIRECTOR SAINIK WELFARE 36AAAAD9115E1Z2 11 GIRIJAN PRIMARY COOPE MARKETING SOCIETY LIMITED ADILABAD 36AAAAG4299E1ZO 12 GIRIJAN PRIMARY CO OP MARKETING SOCIETY LTD UTNOOR 36AAAAG4426D1Z5 13 GIRIJANA PRIMARY CO-OPERATIVE MARKETING SOCIETY LIMITED VENKATAPURAM 36AAAAG5461E1ZY 14 GANGA HITECH CITY 2 SOCIETY 36AAAAG6290R1Z2 15 GSK - VISHWA (JV) 36AAAAG8669E1ZI 16 HASSAN CO OPERATIVE MILK PRODUCERS SOCIETIES UNION LTD 36AAAAH0229B1ZF 17 HCC SEW MEIL JOINT VENTURE 36AAAAH3286Q1Z5 18 INDIAN FARMERS FERTILISER COOPERATIVE LIMITED 36AAAAI0050M1ZW 19 INDU FORTUNE FIELDS GARDENIA APARTMENT OWNERS ASSOCIATION 36AAAAI4338L1ZJ 20 INDUR INTIDEEPAM MUTUAL AIDED CO-OP THRIFT/CREDIT SOC FEDERATION LIMITED 36AAAAI5080P1ZA 21 INSURANCE INFORMATION BUREAU OF INDIA 36AAAAI6771M1Z8 22 INSTITUTE OF DEFENCE SCIENTISTS AND TECHNOLOGISTS 36AAAAI7233A1Z6 23 KARNATAKA CO-OPERATIVE MILK PRODUCER\S FEDERATION -

Most Shares MIDCAP 100 - the Vehicle to Invest in Nifty Midcap 100 Index About Most Shares Midcap 100

Product labelling This product is suitable for investors who are seeking* Return that corresponds generally to the performance of the Nifty Midcap 100 Index, subject to tracking error Investment in equity securities of Nifty Midcap 100 Index Index About Nifty Midcap 100 Index About Nifty Midcap 100 Index Launched on July 18, 2005 with a base value of 1000 as on January 1, 2003 Objective : Capture the movement and be a benchmark of midcap segment of the market Computation methodology : Market capitalization weighted method from the launch date till February 25, 2010 and free float market capitalization method w.e.f. February 26, 2010 Selection Criteria: a) Exclude stocks which constitute more than 5% market capitalization of the universe b) From the remaining companies, remove all companies contributing top 75 percent market capitalization c) Exclude any Nifty Stock still in the list d) Select the top 100 companies from the remaining list Universe: all companies listed on the National Stock Exchange which have a minimum track record of three years of operations, with a positive networth and listing history of at least 6 months. (Companies coming out with IPO to be eligible after 3 months of listing) Source: India Index Services & Products Limited (IISL) Investment case for Nifty Midcap 100 Index Investment Case Indian economy expected to grow at a fast pace Midcap companies are a leveraged play on India Midcap companies provide Growth and are Hidden Gems Nifty Midcap 100 index complements large cap portfolios & provide better portfolio diversification India expected to grow at a fast pace 3.00 GDP (USD Trillion) Indian GDP Market Prices 2.50 2.47 2.26 2.09 2.03 2.00 1.86 1.82 1.83 1.71 1.50 1.37 1.24 1.23 1.00 0.95 0.83 0.72 0.62 0.48 0.50 0.53 0.50 0.42 0.43 0.47 0.00 FY98 FY99 FY00 FY01 FY02 FY03 FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17E FY18E Source: Motilal Oswal Securities Ltd.