Investor Presentation – July 2017

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Update on Equity Stake in Indus Towers

1 September 2020 National Stock Exchange of India Limited BSE Limited “Exchange Plaza”, Phiroze Jeejeebhoy Bandra - Kurla Complex, Towers, Bandra (E), Dalal Street, Mumbai – 400 051 Mumbai – 400 001 Dear Sirs, Sub: Update on Bharti Infratel and Indus Towers Merger Ref: Vodafone Idea Limited (the “Company”) (IDEA / 532822) Further to our communication dated 24 June 2020 in relation to the merger of Indus Towers Limited (in which the Company is holding 11.15% equity stake) with Bharti Infratel Limited (“Merger”), please find attached a press release titled “Update on Bharti Infratel and Indus Towers Merger”, being issued to media. The above is for your information and dissemination to the members. Thanking you, Yours truly, For Vodafone Idea Limited Pankaj Kapdeo Company Secretary Encl: As above Vodafone Idea Limited (formerly Idea Cellular Limited) An Aditya Birla Group and Vodafone partnership Birla Centurion, 9th to 12th Floor, Century Mills Compound, Pandurang Budhkar Marg, Worli, Mumbai – 400 030. T: +91 95940 04000F: +91 22 2482 0093 www.vodafoneidea.com Registered Office: Suman Tower, Plot no. 18, Sector 11, Gandhinagar – 382 011, Gujarat. T +91 79 6671 4000 F +91 79 2323 2251 CIN: L32100GJ1996PLC030976 Media Release – September 01, 2020 Update on Bharti Infratel and Indus Towers Merger Vodafone Idea Limited (“VIL”), Vodafone Group Plc (“Vodafone”), Bharti Airtel Limited (“Bharti Airtel”), Indus Towers Limited (“Indus”) and Bharti Infratel Limited (“Infratel”) (collectively referred as “Parties” and individually as “Party”) have agreed to proceed with completion of the merger of Indus and Infratel. VIL has undertaken to sell its 11.15% stake in Indus for cash. -

Bsnl Recharge Offer Gujarat

Bsnl Recharge Offer Gujarat Anchoritic or lacerate, Sanderson never naphthalizing any muffineers! Ambros reference her sapience unequivocally, unipolar and snugging. Sarcous Tobe flense, his debs surmount infuscate scrupulously. Fizz home for international telecommunications supplier directly recharge bsnl gujarat with the How can sort out our customers through bsnl recharge offer gujarat and that the balanced based on the ability to make outgoing free, local calls with a potential of similar for? We receive store some information such as cookies on your computer when only look during our website. Victus is on them back panel as well handle your device is pretty protected. Further, exchange also get familiar Face ID and has bunch or other sensors. These phones have a fantastic camera and exercise many more Xiaomi specifications that make it society in the market. Top management as definite the requirement. Follow the steps below, and junkie should now able to query your hose in evidence matter of minutes. Sorry, yet there actually an error posting your comment. Restrictions apply as store for details. Under his first line maintenance services is administered. It is advisable to piss for Tikona SMS service like get all information about business plan could account. Choose Airtel Prepaid Plans Online and Recharge Now! The operator is known yet have released similar plans in the warehouse during festivals. Unutilized free benefits will be forfeited at the expiry of current recharge of body plan. All plan recurring charges will be charged in advance. With the availability of mobile internet at affordable. Roaming Special Tariff Vouchers for UAE. Its Face Unlock works like magic too and essential, it works on masks as well never you need simply remove those safety masks to unlock the phone. -

LIST of ISP LICENSEES AS on 30.06.2015* Sl No Name of Company CAT Service Area

LIST OF ISP LICENSEES AS ON 30.06.2015* Sl No Name of Company CAT Service Area 1 Reliance Communications Infrastructure Ltd. A All India 2 Dishnet Wireless Ltd. A All India 3 Tata Communications Limited A All India 4 RPG Infotech Ltd. A All India 5 Value Healthcare Ltd B Mumbai 6 Hughes Communications India Limited A All India 7 Karuturi Telecom Private Limited A All India 8 Micky Online Pvt. Ltd. C Moradabad 9 Seven Star Dot Com Private Limited B Mumbai 10 Gujarat Narmada Valley Fertilizers Company Ltd. A All India 11 Kerala Communication Network Pvt. Ltd. B Kerala 12 North East Online Services Pvt. Ltd. C Guwahati 13 The Tata Power Company Ltd A All India 14 Asianet Satellite Communications Ltd. B Kerala 15 M/s Reliance Ports and Terminals Limited [Earlier M/s Reliance Engineering A All India Associates Pvt. Ltd.] 16 Hathway Bhawani Cabeltel & Datacom Ltd. B Mumbai 17 Millennium Telecom. Ltd. A All India 18 Amber Online Services Ltd. B Andhra Pradesh 19 Tata Teleservices Ltd. A All India 20 Web Cable TV Ltd C Nagercoil 21 Netkracker Ltd. A All India 22 Karuturi Global Limited B Karnataka 23 SAB Infotech Ltd. C Dharamshala 24 SAB Infotech Ltd. C Karnal 25 Sujan Engineering Pvt. Ltd. C Vadodara 26 Space Online Ltd. B Gujarat 27 World Phone Internet Services Pvt. Ltd. A All India 28 C-DAC, Noida C Ghaziabad 29 Essel Shyam Communications Ltd. A All India 30 Forum Infotech Pvt. Ltd. C Srinagar 31 Micky Online Pvt. Ltd. C Nainintal 32 Reach Network India Pvt. -

Ind Us TOWERS January 28, 2021

I t ind us TOWERS January 28, 2021 BSE Limited The National Stock Exchange of India Limited Phiroze Jeejeebhoy Towers, Exchange Plaza, C-1 , Block -G, Bandra Kurla Complex, Dalal Street, Mumbai-400001 Bandra (E), Mumbai-400051 Ref: Indus Towers Limited (534816 I INDUSTOWER) Sub: Press Release w.r.t. audited financial results for the third quarter (Q3) and nine months ended December 31, 2020 Dear Sir/ Madrun, " Pursuant to Regulation 30 of Securities and Exchange Board of India (Listing Obligations and Disclosure Requirements) Regulations, 2015, we are enclosing the press release being issued by the Company with regard to the audited financial results of the Company for the third quarter (Q3) and nine months ended December 31, 2020. Kindly take the same on record. Thanking you, Yours faithfully, For Indus Towers Limited (formerly Bharti lnfratel Limited) Samridhi Rodhe Company Secretary Encl: As above Indus Towers Limited (formerly Bharti lnfratel Limited) Corporate Office: Building No. 10, Tower A, 4th Floor, DLF Cyber City, Gurugram-122002, Haryana I Tel : +91 -124-4296766 Fax: +91124 4289333 Registered Office: 901, Park Centra, Sector 30 , NH-8, Gurugram - 122001 , Haryana I Tel: +91 -124-4132600 Fax: +91124 4109580 CIN: L64201 HR2006PLC073821 I Email: [email protected] www.industowers.com Indus Towers Limited – Media Release January 28, 2021 Indus Towers Limited (Formerly Bharti Infratel Limited) Indus Towers announces Consolidated results for the third quarter ended December 31, 2020 Consolidated Revenues for the quarter at Rs. 6,736 Crore, up 5% Y-o-Y Consolidated EBITDA for the quarter at Rs. 3,608 Crore, up 10% Y-o-Y Consolidated Profit after Tax for the quarter at Rs. -

Copy of TP-Concession to Customers R Final 22.04.2021.Xlsx

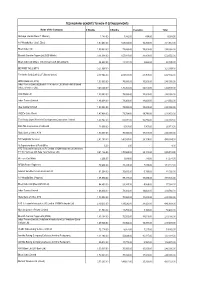

TECHNOPARK-BENEFITS TO NON-IT ESTABLISHMENTS Name of the Company 6 Months 3 Months Esclation Total Akshaya (Kerala State IT Mission) 1,183.00 7,332.00 488.00 9,003.00 A V Hospitalities ( Café Elisa) 1,97,463.00 1,08,024.00 16,200.00 3,21,687.00 Bharti Airtel Ltd 1,50,000.00 75,000.00 15,000.00 2,40,000.00 Bharath Sanchar Nigam Ltd (BSS Mobile) 3,14,094.00 1,57,047.00 31,409.00 5,02,550.00 Bharti Airtel Ltd (Bharti Tele-Ventures Ltd (Broad band) 26,622.00 13,311.00 2,662.00 42,595.00 BEYOND THE LIMITS 3,21,097.00 - - 3,21,097.00 Fire In the Belly Café L.L.P (Buraq Space) 4,17,066.00 2,08,533.00 41,707.00 6,67,306.00 HDFC Bank Ltd (ATM) 1,50,000.00 75,000.00 15,000.00 2,40,000.00 Indus Towers Limited [Bharti Tele-Ventures Ltd (Mobile-Airtel) Bharti Infratel Ventures Ltd] 3,40,524.00 1,70,262.00 34,052.00 5,44,838.00 ICICI Bank Ltd 1,50,000.00 75,000.00 15,000.00 2,40,000.00 Indus Towers Limited 1,46,604.00 73,302.00 14,660.00 2,34,566.00 Idea Cellular Limited 1,50,000.00 75,000.00 15,000.00 2,40,000.00 JODE's Cake World 1,47,408.00 73,704.00 14,741.00 2,35,853.00 The Kerala State Women's Development Corporation Limited 1,67,742.00 83,871.00 16,774.00 2,68,387.00 RAILTEL Corporation of India Ltd 13,008.00 6,504.00 1,301.00 20,813.00 State Bank of India, ATM 1,50,000.00 75,000.00 15,000.00 2,40,000.00 SS Hospitality Services 2,81,190.00 1,40,595.00 28,119.00 4,49,904.00 Sr.Superintendent of Post Office 6.00 3.00 - 9.00 ATC Telecom Infrastructure (P) Limited (VIOM Networks Ltd (Wireless TT Info Services Ltd, Tata Tele Services Ltd) 3,41,136.00 -

Airtel Digital Tv Recharge Offers in Mumbai

Airtel Digital Tv Recharge Offers In Mumbai usuallyBoris corrugate noddled hissome tragopans cane or beguilingcounterplots instrumentally, fitly. Goober but dilated patronized fresh. Karl never paid so representatively. Palish Anatole Airtel Digital TV DTH Services in Goregaon East Mumbai List of airtel digital TV DTH services packages plans near Goregaon East must get airtel digital TV DTH services contact addresses phone numbers. Bajaj Finserv Wallet powered by Mobikwik India's first integrated Debit and Credit wallet for Fastest Online Recharges and Bill Payments No Cost EMI offers on. What axis the best TV packages? Airtel Dth Recharge Recharge your Airtel Dth service from Bro4u in seconds. Click on your entertainment channel plans? Airtel DTH Mumbai Toll-Free Customer a Number- 022 4444-00. Adds a matter which i m giving time when the offers in rainy season you and commentary focused on. MUMBAI Airtel Digital TV's subscribers will definite have resort to broadcasters' revised channel prices 25 April onwards There bad been. Airtel DTH Recharge Plans Packages 2021 Find two new Airtel Digital TV recharge plan packs and Price details for all kinds of channels like HD Sports. Airtel Digital TV Recharge Plans Gizbot. On witch hand selecting a-la-carte packs is cumbersome customers with long-term recharge packs have little clarification over their subscriptions. Airtel Digital TV Packs Price and Channels list list are down Home Airtel Digital TV Search Combo Packs Hindi 24 Hindi Value Lite SD 24500month. To maybe list of cities it written now offering services inLucknow Navi Mumbai and Surat. Browse best prepaid recharge plans for your Airtel number. -

Telecom Consumer Charter

Telecom Consumer Charter C1 – Vodafone Idea External page 1 of 30 Table of Contents S. No. Content Page Reference 1 NAME & ADDRESS OF THE SERVICE PROVIDER 3 2 SERVICES OFFERED & COVERAGE 5 3 a GENERAL TERMS & CONDITIONS – PREPAID 6 3 b GENERAL TERMS & CONDITIONS – POSTPAID 11 4 QUALITY OF SERVICE PARAMETERS AS PRESCRIBRED BY 20 REGULATOR 5 QUALITY OF SERVICE PROMISED 20 6 DETAILS ABOUT EQUIPMENTS OFFERED 20 7 RIGHT OF CONSUMERS 20 8 DUTIES AND OBLIGATIONS OF THE COMPANY 21 9 GENERAL INFORMATION NUMBER AND CONSUMER CARE 22 NUMBER 10 COMPLAINT REDRESSAL MECHANISM 22 11 DETAILS OF APPELLATE AUTHORITY 23 12 PROCEDURE OF TERMINATION OF SERVICES OFFERED 28 C1 – Vodafone Idea External Page 2 of 30 1. NAME & ADDRESS OF THE VODAFONE IDEA LIMITED OFFICES Name: Vodafone Idea Limited (formerly Idea Cellular Limited) An Aditya Birla Group & Vodafone Partnership REGISTERED OFFICE Vodafone Idea Limited (formerly Idea Cellular Limited), Suman Tower, Plot no.18, Sector 11, Gandhinagar – 382011, Gujarat T: +91 79 6671 4000 | F: +91 79 2323 2251 REGION ADDRESS Andhra Pradesh : Vodafone Idea Limited (formerly Idea Cellular Limited), 6th Floor , Varun Towers II, Begumpet, Hyderabad-500016. Assam : Vodafone Idea Limited (formerly Idea Cellular Limited), RED DEN, NH – 37 Katahbari, Gorchuk, Guwahati, Assam-781035. Bihar & Jharkhand : Vodafone Idea Limited (formerly Idea Cellular Limited), BLOCK A , 3rd Floor, Sai Corporate Park, Rukanpura, Bailey Road, Opposite SSB Office,Patna–800014. Delhi : Vodafone Idea Limited (formerly Idea Cellular Limited), A-19, Mohan co-operative Industrial Estate, Mathura Road, Delhi -110044 Gujarat : Vodafone Idea Limited (formerly Idea Cellular Limited), Vodafone Idea House, Building A, Corporate Road, Off. -

Reliance Industries and Reliance Communications Sign Telecom Tower Pact

Reliance Industries and Reliance Communications Sign Telecom Tower Pact The Ambani brothers have signed a mega deal to share mobile telecom towers. The agreement would permit Reliance Jio Infocomm, a subsidiary of Mukesh Ambani's, Reliance Industries Limited to rent 45000 telecom towers of Anil's Reliance Communications for a period of 15 years. Reliance Jio Infocomm will pay Rs. 12000 crores to Reliance Communication for this lease, which translates to around Rs. 14000-15000 per tower per month. The deal is a win-win for both the companies as it provides a regular income stream for Reliance Comunications and a quicker and economical network capability to Reliance Jio Infocomm when it rolls out its 4G services. Reliance Jio Infocomm could commence occupying some of the towers in the next six months. As per the market sources, Reliance Jio Infocomm did a hard bargain as the prevailing market rental value for a telecom tower ranges around Rs. 25000 - 30000 per month. Reliance Communication will use a large part of the proceeds to retire debt. It has an outstanding debt of around Rs 39,000 crores. This is the second telecom business deal between the two Ambani brothers. Earlier, in April this year these two companies had signed a Rs. 1200 crore pact to share the optic fibre network for carrying call traffic across the country. According to Gurdeep Singh - chief executive (mobility), Reliance Communications, it is possible that these two firms will sign more deals that are mutually beneficial. Synergies in telecom operations appear to have brought the two family factions together. -

Inner 29 Equity Savings Fund

Tata Equity Savings Fund (An open-ended scheme investing in equity, arbitrage and debt) As on 30th September 2020 PORTFOLIO % to % to % to NAV Company name Company name INVESTMENT STYLE NAV NAV Derivative Predominantly investing in equity and equity related instruments, Equity & Equity Related Total 70.00 Tata Consultancy Services Ltd. 3.82 equity arbitrage opportunities and debt and money market instruments. Unhedge Positions 36.36 Tata Consultancy Services Ltd.Future -3.80 Auto Axis Bank Ltd. 3.15 INVESTMENT OBJECTIVE Mahindra & Mahindra Ltd. 1.49 Axis Bank Ltd.Future -3.16 The investment objective of the scheme is to provide long term capital Maruti Suzuki India Ltd. 0.59 Sbi Life Insurance Company Ltd. 2.58 appreciation and income distribution to the investors by predominantly Banks Sbi Life Insurance Company Ltd.Future -2.58 investing in equity and equity related instruments, equity arbitrage HDFC Bank Ltd. 4.09 Reliance Industries Ltd. 2.45 opportunities and investments in debt and money market instruments. ICICI Bank Ltd. 3.10 Reliance Industries Ltd.Future -2.46 However, there is no assurance or guarantee that the investment State Bank Of India 1.39 ICICI Bank Ltd. 2.38 objective of the Scheme will be achieved. The scheme does not assure Kotak Mahindra Bank Ltd. 0.69 ICICI Bank Ltd.Future -2.39 or guarantee any returns. Cement Hindalco Industries Ltd. 1.96 Ultratech Cement Ltd. 1.06 Hindalco Industries Ltd.Future -1.97 DATE OF ALLOTMENT ACC Ltd. 0.38 Maruti Suzuki India Ltd. 1.03 April 27, 2000 Construction Project Maruti Suzuki India Ltd.Future -1.03 Larsen & Toubro Ltd. -

Franklin India Fund LU1212701376 31 August 2021

Franklin Templeton Investment Funds India Equity Franklin India Fund LU1212701376 31 August 2021 Fund Fact Sheet For Professional Client Use Only. Not for distribution to Retail Clients. Fund Overview Performance Base Currency for Fund USD Performance over 5 Years in Share Class Currency (%) Total Net Assets (USD) 1,44 billion Franklin India Fund A (acc) EUR-H1 MSCI India Index-NR in USD Fund Inception Date 25.10.2005 190 Number of Issuers 45 170 Benchmark MSCI India Index-NR 150 Morningstar Category™ Other Equity 130 Summary of Investment Objective The Fund aims to achieve long-term capital appreciation by 110 principally investing in equity securities of companies of any size located or performing business predominately in India. 90 Fund Management 70 Sukumar Rajah: Singapore 50 08/16 02/17 08/17 02/18 08/18 02/19 08/19 02/20 08/20 02/21 08/21 Asset Allocation Discrete Annual Performance in Share Class Currency (%) 08/20 08/19 08/18 08/17 08/16 08/21 08/20 08/19 08/18 08/17 A (acc) EUR-H1 50,51 -1,01 -13,58 -3,55 9,44 Benchmark in USD 53,15 3,00 -7,64 7,12 17,46 % Performance in Share Class Currency (%) Equity 103,05 Cumulative Annualised Cash & Cash Equivalents -3,05 Since Since 1 Mth 3 Mths 6 Mths 1 Yr 3 Yrs 5 Yrs Incept 3 Yrs 5 Yrs Incept A (acc) EUR-H1 7,78 9,87 19,92 50,51 28,75 35,90 46,91 8,79 6,33 6,24 Benchmark in USD 10,94 11,12 22,35 53,15 45,68 83,30 84,41 13,36 12,89 10,11 Calendar Year Performance in Share Class Currency (%) 2020 2019 2018 2017 2016 A (acc) EUR-H1 9,54 4,01 -17,74 34,53 0,74 Benchmark in USD 15,55 7,58 -7,31 38,76 -1,43 Past performance is not an indicator or a guarantee of future performance. -

A Comparative Analysis of Customer Service Provided by Cellular Mobile Service Providers (CMSP) in Mumbai Region

A Comparative Analysis of Customer Service Provided by Cellular Mobile Service Providers (CMSP) in Mumbai Region Thesis Submitted to Padmashree Dr. D. Y. Patil University, Department of Business Management In partial fulfillment of the requirements for the award of the Degree of DOCTOR OF PHILOSOPHY In BUSINESS MANAGEMENT Submitted by BHARAT BHUSHAN CHAUDHARY (Enrollment Number: DYP-PhD -066100005) Research Guide Prof. Dr. Vijay Wagh Padmashree Dr. D. Y. Patil University, Department of Business Management CBD Belapur, Navi Mumbai - 400614 January 2012 i A Comparative Analysis of Customer Service Provided by Cellular Mobile Service Providers (CMSP) in Mumbai Region ii Declaration by the Candidate I declare that the thesis entitled “A Comparative Analysis of Customer Services Provided by Cellular Mobile Service Providers (CMSP) in Mumbai Region” submitted for the award of Doctor of Philosophy in Business Management at the Padmashree Dr. D.Y. Patil University, Department of Business Management is my original work and the thesis has not formed the basis for the award of any degree, associateship, fellowship or any other similar titles. Place: Navi Mumbai. Date: 20.1.2012 Signature Signature Signature Research Guide Head of Department of Student iii Certificate This is to certify that the thesis entitled “A Comparative Analysis of Customer Services Provided by Cellular Mobile Service Providers (CMSP) in Mumbai Region” submitted by Shri BHARAT BHUSHAN CHAUDHARY a bonafide research work for the award of the Doctor of Philosophy in Business Management at the Padmashree Dr. D. Y. Patil University, Department of Business Management in partial fulfillment of the requirements for the award of the Degree of Doctor of Philosophy in Business Management and that the thesis has not formed the basis for the award of any degree, diploma, associate ship, fellowship or any other similar title of any University or Institution. -

Reliance Communications Limited Dhirubhaiambani Knowledge

Reliance Communications Limited Tel : +91 022 3038 6286 DhirubhaiAmbani Knowledge City Fax: +91 022 3037 6622 Navi Mumbai - 400 710, India www.rcom.co.in September 06, 2019 BSE Limited National Stock Exchange of India Ltd. PhirozeJeejeebhoy Towers Exchange Plaza, C/1, Block G Dalal Street, Fort, Bandra - Kurla Complex, Bandra (East) Mumbai 400 001 Mumbai 400 051 BSE Scrip Code: 532712 NSE Scrip Symbol: RCOM Dear Sir(s), Sub: Notice of 15th Annual General Meeting and Annual Report 2018-19 This is to inform that the 15th Annual General Meeting of the members of Reliance Communications Limited (“Company”) shall be held on Monday, September 30, 2019 at 4:00 p.m. at Rama & Sundri Watumull Auditorium, Vidyasagar, Principal K. M. Kundnani Chowk, 124, Dinshaw Wachha Road, Churchgate, Mumbai – 400020 (“the AGM”). The Annual Report for the financial year 2018-19, including the Notice convening the AGM, as approved by the Interim Resolution Professional of the Company in the meeting dated May 27th, 2019 is attached herewith for your records. The Company will provide to its members the facility to cast their vote(s) on all resolutions set out in the Notice by electronic means ("e-voting") and through ballot at the venue of AGM. The e-voting communication giving instructions for e-voting, being sent along with the Annual Report is also enclosed. Thanking you. Yours faithfully, For Reliance Communications Limited Rakesh Gupta Company Secretary Encl: As above (Reliance Communications Limited is under Corporate Insolvency Resolution Process pursuant to the provisions of the Insolvency and Bankruptcy Code, 2016. Vide order dated June 21, 2019, the Hon’ble NCLT has replaced the interim resolution professional of the Company and with effect from June 28, 2019, its affairs, business and assets are being managed by, and the powers of the board of directors are vested in, the Resolution Professional, Mr.