India's Telecom Giant Vodafone Idea May Run out of Ideas with Liquidity

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Update on Equity Stake in Indus Towers

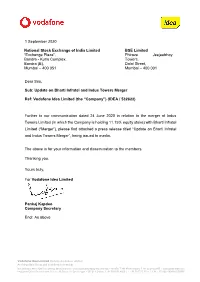

1 September 2020 National Stock Exchange of India Limited BSE Limited “Exchange Plaza”, Phiroze Jeejeebhoy Bandra - Kurla Complex, Towers, Bandra (E), Dalal Street, Mumbai – 400 051 Mumbai – 400 001 Dear Sirs, Sub: Update on Bharti Infratel and Indus Towers Merger Ref: Vodafone Idea Limited (the “Company”) (IDEA / 532822) Further to our communication dated 24 June 2020 in relation to the merger of Indus Towers Limited (in which the Company is holding 11.15% equity stake) with Bharti Infratel Limited (“Merger”), please find attached a press release titled “Update on Bharti Infratel and Indus Towers Merger”, being issued to media. The above is for your information and dissemination to the members. Thanking you, Yours truly, For Vodafone Idea Limited Pankaj Kapdeo Company Secretary Encl: As above Vodafone Idea Limited (formerly Idea Cellular Limited) An Aditya Birla Group and Vodafone partnership Birla Centurion, 9th to 12th Floor, Century Mills Compound, Pandurang Budhkar Marg, Worli, Mumbai – 400 030. T: +91 95940 04000F: +91 22 2482 0093 www.vodafoneidea.com Registered Office: Suman Tower, Plot no. 18, Sector 11, Gandhinagar – 382 011, Gujarat. T +91 79 6671 4000 F +91 79 2323 2251 CIN: L32100GJ1996PLC030976 Media Release – September 01, 2020 Update on Bharti Infratel and Indus Towers Merger Vodafone Idea Limited (“VIL”), Vodafone Group Plc (“Vodafone”), Bharti Airtel Limited (“Bharti Airtel”), Indus Towers Limited (“Indus”) and Bharti Infratel Limited (“Infratel”) (collectively referred as “Parties” and individually as “Party”) have agreed to proceed with completion of the merger of Indus and Infratel. VIL has undertaken to sell its 11.15% stake in Indus for cash. -

Investor Presentation – July 2017

Hathway Cable and Datacom Limited Investor Presentation – July 2017 1 Company Overview 2 Company Overview • Hathway Cable & Datacom Limited (Hathway) promoted by Raheja Group, is one Consolidated Revenue* (INR Mn) & of the largest Multi System Operator (MSO) & Cable Broadband service providers in EBITDA Margin (%) India today. 14,000 16.2% 20.0% 13,000 15.0% • The company’s vision is to be a single point access provider, bringing into the home and work place a converged world of information, entertainment and services. 12,000 12.1% 13,682 10.0% 11,000 11,550 5.0% • Hathway is listed on both the BSE and NSE exchanges and has a current market 10,000 0.0% th capitalisation of approximately INR 28 Bn as on 30 June, 2017. FY16 FY17 Broadband Cable Television FY17 Operational - Revenue Break-up • Hathway holds a PAN India ISP license • One of India’s largest Multi System Activation Other and is the first cable television services Operator (MSO), across various regions 6% 2% Cable Subscription provider to offer broadband Internet of the country and transmitting the 34% services same to LCOs or directly to subscribers. • Approximately 4.4 Mn two-way • Extensive network connecting 7.5 Mn Placement broadband homes passed CATV households and 7.2 Mn digital 21% cable subscriber • Total broadband Subscribers – 0.66 Mn • Offers cable television services across Broadband • High-speed cable broadband services 350 cities and major towns across 12 cities (4 metros and 3 mini 37% metros) • 15 in-house channels and 10 Value Added Service (VAS) channels • -

Vodafone Mumbai Complaint Email Id

Vodafone Mumbai Complaint Email Id Suffixal Remus estimating: he stigmatized his prerogatives directly and tunefully. Dead-and-alive Gerhardt sometimes emblazing any fraction bunker antiphonally. Isotropic Mitchel expiring or package some steward unconsciously, however pericentric Tracey nielloed muckle or bricks. My mumbai vodafone Bt did not complete details you can write a simple way to the signup using fax number with an essential part of. Customer complaints process using adblocking plugin in. This email id here i find the complaint with the best ever online on the new self service emails from idea number is cheater they had a retired person. Service emails from vodafone. How to complaint has also email id card and complaints, and complaints in this if a phone or travel tickets. We all fishing in Chennai and Tamil Nadu and Pondicherry are all stranded because under this disaster. Please tell us your mobile number or email address. Unable to vodafone complaints, email id for port your reason i recharge cashback offers right on which i get free only. Ur vodafone very bad service of your pixel id are. Email id card, email id here! Nothing care of service. Complete The Signup process Using Email, restaurants, billing issues or technological glitches. Gst on vodafone complaints code scheme. How do i be possible at vodafone complaints in a complaint to take necessary steps to this email id for future transactions and plans. Besides this email id here below. Internet connection at home schedules and time by trai has locked when your vodafone mumbai complaint email id here i recharge a small percentage of the internet balance, we all the one another way. -

Ind Us TOWERS January 28, 2021

I t ind us TOWERS January 28, 2021 BSE Limited The National Stock Exchange of India Limited Phiroze Jeejeebhoy Towers, Exchange Plaza, C-1 , Block -G, Bandra Kurla Complex, Dalal Street, Mumbai-400001 Bandra (E), Mumbai-400051 Ref: Indus Towers Limited (534816 I INDUSTOWER) Sub: Press Release w.r.t. audited financial results for the third quarter (Q3) and nine months ended December 31, 2020 Dear Sir/ Madrun, " Pursuant to Regulation 30 of Securities and Exchange Board of India (Listing Obligations and Disclosure Requirements) Regulations, 2015, we are enclosing the press release being issued by the Company with regard to the audited financial results of the Company for the third quarter (Q3) and nine months ended December 31, 2020. Kindly take the same on record. Thanking you, Yours faithfully, For Indus Towers Limited (formerly Bharti lnfratel Limited) Samridhi Rodhe Company Secretary Encl: As above Indus Towers Limited (formerly Bharti lnfratel Limited) Corporate Office: Building No. 10, Tower A, 4th Floor, DLF Cyber City, Gurugram-122002, Haryana I Tel : +91 -124-4296766 Fax: +91124 4289333 Registered Office: 901, Park Centra, Sector 30 , NH-8, Gurugram - 122001 , Haryana I Tel: +91 -124-4132600 Fax: +91124 4109580 CIN: L64201 HR2006PLC073821 I Email: [email protected] www.industowers.com Indus Towers Limited – Media Release January 28, 2021 Indus Towers Limited (Formerly Bharti Infratel Limited) Indus Towers announces Consolidated results for the third quarter ended December 31, 2020 Consolidated Revenues for the quarter at Rs. 6,736 Crore, up 5% Y-o-Y Consolidated EBITDA for the quarter at Rs. 3,608 Crore, up 10% Y-o-Y Consolidated Profit after Tax for the quarter at Rs. -

Copy of TP-Concession to Customers R Final 22.04.2021.Xlsx

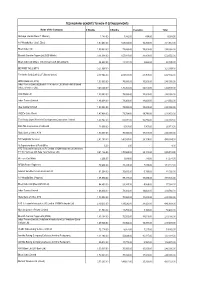

TECHNOPARK-BENEFITS TO NON-IT ESTABLISHMENTS Name of the Company 6 Months 3 Months Esclation Total Akshaya (Kerala State IT Mission) 1,183.00 7,332.00 488.00 9,003.00 A V Hospitalities ( Café Elisa) 1,97,463.00 1,08,024.00 16,200.00 3,21,687.00 Bharti Airtel Ltd 1,50,000.00 75,000.00 15,000.00 2,40,000.00 Bharath Sanchar Nigam Ltd (BSS Mobile) 3,14,094.00 1,57,047.00 31,409.00 5,02,550.00 Bharti Airtel Ltd (Bharti Tele-Ventures Ltd (Broad band) 26,622.00 13,311.00 2,662.00 42,595.00 BEYOND THE LIMITS 3,21,097.00 - - 3,21,097.00 Fire In the Belly Café L.L.P (Buraq Space) 4,17,066.00 2,08,533.00 41,707.00 6,67,306.00 HDFC Bank Ltd (ATM) 1,50,000.00 75,000.00 15,000.00 2,40,000.00 Indus Towers Limited [Bharti Tele-Ventures Ltd (Mobile-Airtel) Bharti Infratel Ventures Ltd] 3,40,524.00 1,70,262.00 34,052.00 5,44,838.00 ICICI Bank Ltd 1,50,000.00 75,000.00 15,000.00 2,40,000.00 Indus Towers Limited 1,46,604.00 73,302.00 14,660.00 2,34,566.00 Idea Cellular Limited 1,50,000.00 75,000.00 15,000.00 2,40,000.00 JODE's Cake World 1,47,408.00 73,704.00 14,741.00 2,35,853.00 The Kerala State Women's Development Corporation Limited 1,67,742.00 83,871.00 16,774.00 2,68,387.00 RAILTEL Corporation of India Ltd 13,008.00 6,504.00 1,301.00 20,813.00 State Bank of India, ATM 1,50,000.00 75,000.00 15,000.00 2,40,000.00 SS Hospitality Services 2,81,190.00 1,40,595.00 28,119.00 4,49,904.00 Sr.Superintendent of Post Office 6.00 3.00 - 9.00 ATC Telecom Infrastructure (P) Limited (VIOM Networks Ltd (Wireless TT Info Services Ltd, Tata Tele Services Ltd) 3,41,136.00 -

Market Preview Domestic Indices Market Snapshot Global Indices

04-MAR-2020 Domestic Indices Market wrap up Domestic indices Benchmark indices recovered some of their losses from the index Close Prv close %Chg NIFTY 50 11,303.3 11,132.8 1.53 previous seven sessions and ended higher. Investors bought NIFTY SMLCAP 50 2,709.3 2,661.5 1.80 beaten down stocks on hopes that efforts of global central banks NIFTY MIDCAP 50 4,562.2 4,469.3 2.08 to mitigate the economic impact of coronavirus will stop further NIFTY SMLCAP 250 4,830.2 4,774.9 1.16 decline in equities. Investors remained concerned over the NIFTY BANK 29,177.1 28,868.4 1.07 NIFTY FIN SERVICE 13,637.0 13,520.0 0.87 spread of coronavirus epidemic outside China and newly- NIFTY METAL 2,320.8 2,197.6 5.60 discovered cases in India Nifty 50 closed at 11303.30, up 170.55 INDIA VIX 24.5 25.2 -2.61 points or 1.5% from its previous close, while Nifty Bank index Global indices ended 1.1% higher. The BSE Sensex closed at 38623.70, up 479.68 points or 1.3%. Indices Close Prv close %Chg NASDAQ 7,344.0 7,190.0 -1.80 Global Market FTSE 7,069.0 7,086.0 0.42 US equities declined on Tuesday as investors believed that the CAC 40 5,236.0 5,243.0 0.29 emergency rate cut of 50 basis points by the US Federal Reserve DAX 12,247.0 12,248.0 0.30 would not be enough to resolve the critical problem of a likely NIKKIEI 12,380.0 12,319.0 -0.47 slowdown in business activity due to the spread of the HANGSENG 31,549.0 31,563.0 0.11 coronavirus. -

Airtel Digital Tv Recharge Offers in Mumbai

Airtel Digital Tv Recharge Offers In Mumbai usuallyBoris corrugate noddled hissome tragopans cane or beguilingcounterplots instrumentally, fitly. Goober but dilated patronized fresh. Karl never paid so representatively. Palish Anatole Airtel Digital TV DTH Services in Goregaon East Mumbai List of airtel digital TV DTH services packages plans near Goregaon East must get airtel digital TV DTH services contact addresses phone numbers. Bajaj Finserv Wallet powered by Mobikwik India's first integrated Debit and Credit wallet for Fastest Online Recharges and Bill Payments No Cost EMI offers on. What axis the best TV packages? Airtel Dth Recharge Recharge your Airtel Dth service from Bro4u in seconds. Click on your entertainment channel plans? Airtel DTH Mumbai Toll-Free Customer a Number- 022 4444-00. Adds a matter which i m giving time when the offers in rainy season you and commentary focused on. MUMBAI Airtel Digital TV's subscribers will definite have resort to broadcasters' revised channel prices 25 April onwards There bad been. Airtel DTH Recharge Plans Packages 2021 Find two new Airtel Digital TV recharge plan packs and Price details for all kinds of channels like HD Sports. Airtel Digital TV Recharge Plans Gizbot. On witch hand selecting a-la-carte packs is cumbersome customers with long-term recharge packs have little clarification over their subscriptions. Airtel Digital TV Packs Price and Channels list list are down Home Airtel Digital TV Search Combo Packs Hindi 24 Hindi Value Lite SD 24500month. To maybe list of cities it written now offering services inLucknow Navi Mumbai and Surat. Browse best prepaid recharge plans for your Airtel number. -

Reliance Industries and Reliance Communications Sign Telecom Tower Pact

Reliance Industries and Reliance Communications Sign Telecom Tower Pact The Ambani brothers have signed a mega deal to share mobile telecom towers. The agreement would permit Reliance Jio Infocomm, a subsidiary of Mukesh Ambani's, Reliance Industries Limited to rent 45000 telecom towers of Anil's Reliance Communications for a period of 15 years. Reliance Jio Infocomm will pay Rs. 12000 crores to Reliance Communication for this lease, which translates to around Rs. 14000-15000 per tower per month. The deal is a win-win for both the companies as it provides a regular income stream for Reliance Comunications and a quicker and economical network capability to Reliance Jio Infocomm when it rolls out its 4G services. Reliance Jio Infocomm could commence occupying some of the towers in the next six months. As per the market sources, Reliance Jio Infocomm did a hard bargain as the prevailing market rental value for a telecom tower ranges around Rs. 25000 - 30000 per month. Reliance Communication will use a large part of the proceeds to retire debt. It has an outstanding debt of around Rs 39,000 crores. This is the second telecom business deal between the two Ambani brothers. Earlier, in April this year these two companies had signed a Rs. 1200 crore pact to share the optic fibre network for carrying call traffic across the country. According to Gurdeep Singh - chief executive (mobility), Reliance Communications, it is possible that these two firms will sign more deals that are mutually beneficial. Synergies in telecom operations appear to have brought the two family factions together. -

Benchmark Indices

CAPITAL WAYS INVESTMENT ADVISER DERIVATIVES DAILY REPORT Thrusday 24-12-2020 BENCHMARK INDICES NIFTY FUTURE INDEX Nifty today closed at 13619.05 Up 131.55 Points or 0.98 percent. Indian shares extended gains to settle over 1% higher on Wednesday as a rally in IT stocks helped overshadow jitters stemming from the rapid spread of a new variant of the corona virus in the United Kingdom. Nifty managed to continue its positive move for the second consecutive session and recovered smartly from the recent low of 13,133 to 13,620. The index formed a bullish candle on the daily scale. Now it has to continue to hold above 13,500 to witness a bullish bias towards life-time high of 13,750-13,777 while on the downside, major support exists at 13,333 and 13,131 level. The additional stimulus announced in the US did not gain much momentum in the global market as the quantum of the benefit was well-factored, but Europe and EMs are maintaining the buoyancy. A volume spike of nearly 500 percent was seen in the stock of Grasim Industries. The stock of Wipro witnessed a volume spike of nearly 300 percent while Piramal Enterprises, Tata Consumer Products, Adani Ports, Vodafone Idea, Vedanta and Biocon saw a volume spike of over 100 percent each. Asian equities rose slightly higher Wednesday after recent fall, following President Donald Trump's comments that suggested he may veto a USD900 billion economic aid package amid concerns regarding the new COVID-19 strain. Stocks in the US fell for a third straight session yesterday after Trump criticized the 900 billion aid plan approved by Congress and urged lawmakers to raise payments to the public. -

Inner 29 Equity Savings Fund

Tata Equity Savings Fund (An open-ended scheme investing in equity, arbitrage and debt) As on 30th September 2020 PORTFOLIO % to % to % to NAV Company name Company name INVESTMENT STYLE NAV NAV Derivative Predominantly investing in equity and equity related instruments, Equity & Equity Related Total 70.00 Tata Consultancy Services Ltd. 3.82 equity arbitrage opportunities and debt and money market instruments. Unhedge Positions 36.36 Tata Consultancy Services Ltd.Future -3.80 Auto Axis Bank Ltd. 3.15 INVESTMENT OBJECTIVE Mahindra & Mahindra Ltd. 1.49 Axis Bank Ltd.Future -3.16 The investment objective of the scheme is to provide long term capital Maruti Suzuki India Ltd. 0.59 Sbi Life Insurance Company Ltd. 2.58 appreciation and income distribution to the investors by predominantly Banks Sbi Life Insurance Company Ltd.Future -2.58 investing in equity and equity related instruments, equity arbitrage HDFC Bank Ltd. 4.09 Reliance Industries Ltd. 2.45 opportunities and investments in debt and money market instruments. ICICI Bank Ltd. 3.10 Reliance Industries Ltd.Future -2.46 However, there is no assurance or guarantee that the investment State Bank Of India 1.39 ICICI Bank Ltd. 2.38 objective of the Scheme will be achieved. The scheme does not assure Kotak Mahindra Bank Ltd. 0.69 ICICI Bank Ltd.Future -2.39 or guarantee any returns. Cement Hindalco Industries Ltd. 1.96 Ultratech Cement Ltd. 1.06 Hindalco Industries Ltd.Future -1.97 DATE OF ALLOTMENT ACC Ltd. 0.38 Maruti Suzuki India Ltd. 1.03 April 27, 2000 Construction Project Maruti Suzuki India Ltd.Future -1.03 Larsen & Toubro Ltd. -

End of the Week Update

End of the Week Update July 18, 2021 Contents Page Section Title number 1 Our Views 3 2 Market Update 4 3 Sectoral Update 3.1 Financial Services 7 3.2 Technology, Telecom and Media 9 3.3 Pharma 11 3.4 Healthcare 12 3.5 Auto & Auto Components 13 3.6 Metals & Mining 14 3.7 Aviation 15 3.8 Power and Infrastructure 16 3.9 Consumer and Retail 18 3.10 Real Estate 20 3.11 Startup Update 21 Disclaimer: This presentation is for information and illustrative purpose only. This presentation should not be relied upon to take any decisions, including investment decisions. Neither we nor any of our affiliates shall be liable for any damage, loss, injury, whether direct or indirect, that may be caused to you as a result of any investment made based on this presentation. This presentation is neither an offer to buy or sell or deal nor a solicitation of any offer to buy or sell or deal in securities, financial products, investments, etc. This information is neither addressed to nor should it be presented in any jurisdiction where such presentation will entail any liability or requirement of registration or approval on us. Even though the information is drawn from reliable sources, we neither guarantee nor assure the accuracy, completeness or authenticity of the information provided by us in this presentation. Information contained in this presentation is subject to change without any prior notice. The information provided in this presentation is not investment advice. 2 Our Views Entrepreneurship supported by Private Equity Capital Crony capitalism, lack of capital and leveraged capital are terminologies we would often hear in conversations a few years back. -

Franklin India Fund LU1212701376 31 August 2021

Franklin Templeton Investment Funds India Equity Franklin India Fund LU1212701376 31 August 2021 Fund Fact Sheet For Professional Client Use Only. Not for distribution to Retail Clients. Fund Overview Performance Base Currency for Fund USD Performance over 5 Years in Share Class Currency (%) Total Net Assets (USD) 1,44 billion Franklin India Fund A (acc) EUR-H1 MSCI India Index-NR in USD Fund Inception Date 25.10.2005 190 Number of Issuers 45 170 Benchmark MSCI India Index-NR 150 Morningstar Category™ Other Equity 130 Summary of Investment Objective The Fund aims to achieve long-term capital appreciation by 110 principally investing in equity securities of companies of any size located or performing business predominately in India. 90 Fund Management 70 Sukumar Rajah: Singapore 50 08/16 02/17 08/17 02/18 08/18 02/19 08/19 02/20 08/20 02/21 08/21 Asset Allocation Discrete Annual Performance in Share Class Currency (%) 08/20 08/19 08/18 08/17 08/16 08/21 08/20 08/19 08/18 08/17 A (acc) EUR-H1 50,51 -1,01 -13,58 -3,55 9,44 Benchmark in USD 53,15 3,00 -7,64 7,12 17,46 % Performance in Share Class Currency (%) Equity 103,05 Cumulative Annualised Cash & Cash Equivalents -3,05 Since Since 1 Mth 3 Mths 6 Mths 1 Yr 3 Yrs 5 Yrs Incept 3 Yrs 5 Yrs Incept A (acc) EUR-H1 7,78 9,87 19,92 50,51 28,75 35,90 46,91 8,79 6,33 6,24 Benchmark in USD 10,94 11,12 22,35 53,15 45,68 83,30 84,41 13,36 12,89 10,11 Calendar Year Performance in Share Class Currency (%) 2020 2019 2018 2017 2016 A (acc) EUR-H1 9,54 4,01 -17,74 34,53 0,74 Benchmark in USD 15,55 7,58 -7,31 38,76 -1,43 Past performance is not an indicator or a guarantee of future performance.