Hathway Digital Limited

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Omcs to Cut Margins: Steep Fuel Tax Hikes Swell Centre's Pocket

5/7/2020 OMCs to cut margins: Steep fuel tax hikes swell Centre’s pocket, collection to touch Rs 1.4-lakh-crore/year - The Financial Express MARKET UPDATE TOP GAINER FOREX UPDATE 1Y Return Nifty Redington CRUDE OIL +24.88 9210.00 -60.90 78.20 +5.15 1854 +53 MORE MARKET STATS OMCs to cut margins: Steep fuel tax hikes swell Centre’s pocket, collection to touch Rs 1.4-lakh-crore/year By: Anupam Chatterjee Published: May 7, 2020 5:15:08 AM The steep hikes on auto fuel taxes - Rs 10/litre on petrol and Rs 13/litre on diesel – announced by the Centre late Tuesday won’t inflate the retail prices of these fuels immediately. X X The OMCs have over the last few months been seizing the opportunity afforded by the softening of crude prices to prop up their marketing margins. The steep hikes on auto fuel taxes – Rs 10/litre on petrol and Rs 13/litre on diesel – announced by the Centre late Tuesday won’t inflate the retail prices of these fuels immediately, as the oil marketing companies (OMCs) would for the time being adjust the extra cost against the recent fall in oil prices. The OMCs have over the last few months been seizing the opportunity afforded by the softening of crude prices to prop up their marketing margins. https://www.financialexpress.com/industry/omcs-to-cut-margins-steep-fuel-tax-hikes-swell-centres-pocket-collection-to-touch-rs-1-4-lakh-crore-y… 1/10 5/7/2020 OMCs to cut margins: Steep fuel tax hikes swell Centre’s pocket, collection to touch Rs 1.4-lakh-crore/year - The Financial Express For the Centre, the move could fetch a whopping Rs 1.4 lakh crore additional revenue annually, even with the estimated 12% fall in consumption of the two auto fuels in FY21. -

Copy of TP-Concession to Customers R Final 22.04.2021.Xlsx

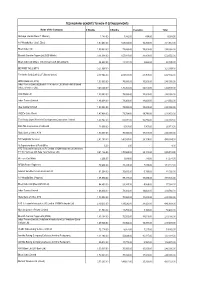

TECHNOPARK-BENEFITS TO NON-IT ESTABLISHMENTS Name of the Company 6 Months 3 Months Esclation Total Akshaya (Kerala State IT Mission) 1,183.00 7,332.00 488.00 9,003.00 A V Hospitalities ( Café Elisa) 1,97,463.00 1,08,024.00 16,200.00 3,21,687.00 Bharti Airtel Ltd 1,50,000.00 75,000.00 15,000.00 2,40,000.00 Bharath Sanchar Nigam Ltd (BSS Mobile) 3,14,094.00 1,57,047.00 31,409.00 5,02,550.00 Bharti Airtel Ltd (Bharti Tele-Ventures Ltd (Broad band) 26,622.00 13,311.00 2,662.00 42,595.00 BEYOND THE LIMITS 3,21,097.00 - - 3,21,097.00 Fire In the Belly Café L.L.P (Buraq Space) 4,17,066.00 2,08,533.00 41,707.00 6,67,306.00 HDFC Bank Ltd (ATM) 1,50,000.00 75,000.00 15,000.00 2,40,000.00 Indus Towers Limited [Bharti Tele-Ventures Ltd (Mobile-Airtel) Bharti Infratel Ventures Ltd] 3,40,524.00 1,70,262.00 34,052.00 5,44,838.00 ICICI Bank Ltd 1,50,000.00 75,000.00 15,000.00 2,40,000.00 Indus Towers Limited 1,46,604.00 73,302.00 14,660.00 2,34,566.00 Idea Cellular Limited 1,50,000.00 75,000.00 15,000.00 2,40,000.00 JODE's Cake World 1,47,408.00 73,704.00 14,741.00 2,35,853.00 The Kerala State Women's Development Corporation Limited 1,67,742.00 83,871.00 16,774.00 2,68,387.00 RAILTEL Corporation of India Ltd 13,008.00 6,504.00 1,301.00 20,813.00 State Bank of India, ATM 1,50,000.00 75,000.00 15,000.00 2,40,000.00 SS Hospitality Services 2,81,190.00 1,40,595.00 28,119.00 4,49,904.00 Sr.Superintendent of Post Office 6.00 3.00 - 9.00 ATC Telecom Infrastructure (P) Limited (VIOM Networks Ltd (Wireless TT Info Services Ltd, Tata Tele Services Ltd) 3,41,136.00 -

February 17, 2020

February 17, 2020 The Manager, Listing Department The General Manager The National Stock Exchange of India Ltd. The Bombay Stock Exchange Limited Exchange Plaza Listing Department Bandra Kurla Complex 15th Floor, P J Towers Bandra (E) Mumbai-400 051 Dalal Street, Mumbai-400 001 NSE Trading Symbol- DEN BSE Scrip Code- 533137 Dear Sirs, Sub.: Media Release titled “Scheme of Amalgamation and Arrangement amongst Network18, TV18, Den & Hathway” Dear Sirs, Attached is the Media Release being issued by the Company titled “Scheme of amalgamation and Arrangement amongst Network18, TV18, Den & Hathway”. You are requested to take the above on record. Thanking You, FCS No. :6887 MEDIA RELEASE Scheme of Amalgamation and Arrangement amongst Network18, TV18, Den & Hathway Consolidates media and distribution businesses of Reliance Creates Media & Distribution platform comparable with global standards of reach, scale and integration News Broadcasting business of TV18 to be housed in Network18 Cable and Broadband businesses of Den and Hathway to be housed in two separate wholly-owned subsidiaries of Network18 February 17, 2020: Reliance Industries (NSE: RELIANCE) announced a consolidation of its media and distribution businesses spread across multiple entities into Network18. Under the Scheme of Arrangement, TV18 Broadcast (NSE: TV18), Hathway Cable & Datacom (NSE: HATHWAY) and Den Networks (NSE: DEN) will merge into Network18 Media & Investments (NSE: NETWORK18). The Appointed Date for the merger shall be February 1, 2020. The Board of Directors of the respective companies approved the Scheme of Amalgamation and Arrangement at their meetings held today. The broadcasting business will be housed in Network18 and the cable and ISP businesses in two separate wholly owned subsidiaries of Network18. -

OTC TCS 2005.Pdf

1 Annual Report 2004-05 Contents Board of Directors ............................................................................................................................................................................................................................... 3 Management Team ............................................................................................................................................................................................................................. 4 Message from the CEO...................................................................................................................................................................................................................... 6 Notice........................................................................................................................................................................................................................................................ 8 Directors' Report ............................................................................................................................................................................................................................... 15 Management Discussion and Analysis ................................................................................................................................................................................... 30 Corporate Governance Report................................................................................................................................................................................................... -

Reliance Industries and Reliance Communications Sign Telecom Tower Pact

Reliance Industries and Reliance Communications Sign Telecom Tower Pact The Ambani brothers have signed a mega deal to share mobile telecom towers. The agreement would permit Reliance Jio Infocomm, a subsidiary of Mukesh Ambani's, Reliance Industries Limited to rent 45000 telecom towers of Anil's Reliance Communications for a period of 15 years. Reliance Jio Infocomm will pay Rs. 12000 crores to Reliance Communication for this lease, which translates to around Rs. 14000-15000 per tower per month. The deal is a win-win for both the companies as it provides a regular income stream for Reliance Comunications and a quicker and economical network capability to Reliance Jio Infocomm when it rolls out its 4G services. Reliance Jio Infocomm could commence occupying some of the towers in the next six months. As per the market sources, Reliance Jio Infocomm did a hard bargain as the prevailing market rental value for a telecom tower ranges around Rs. 25000 - 30000 per month. Reliance Communication will use a large part of the proceeds to retire debt. It has an outstanding debt of around Rs 39,000 crores. This is the second telecom business deal between the two Ambani brothers. Earlier, in April this year these two companies had signed a Rs. 1200 crore pact to share the optic fibre network for carrying call traffic across the country. According to Gurdeep Singh - chief executive (mobility), Reliance Communications, it is possible that these two firms will sign more deals that are mutually beneficial. Synergies in telecom operations appear to have brought the two family factions together. -

Investor Presentation Creating a Diversified Media and Distribution Powerhouse Synopsis of Transaction

TV Investor Presentation Creating a Diversified Media and Distribution Powerhouse Synopsis of transaction Merging of RIL’s media & distribution businesses into Network18 Listed entities TV18, Den and Hathway to be merged into Network18 Network18 shares to be issued to shareholders of all of the above in swap-ratio as determined by valuers Ring-fencing of businesses by placing in wholly owned subsidiaries (WOS) Cable Distribution, Internet Service Provider (ISP) and Digital businesses and investments to be placed under separate WOS’s of Network18 – Cable Co, ISP Co & Digital Co Resultant: Diversified business, with better visibility and control Network18 standalone = News Broadcasting business of TV18 Cable Co = Combined Cable business of Den and Hathway + stake in GTPL ISP Co = Combined ISP business of Den and Hathway Digital Co = Digital News business (New18.com, FirstPost, MoneyControl) Unique combination of content & distribution across linear and digital Net debt free company. Mid-cap stock with ~2000 Cr market-cap Flagship Media & Distribution entity of Reliance group 2 Simplification of the listed media & distribution businesses of the group Current Structure Reliance Industries Ltd Sole (“RIL”) Sole Beneficiary Beneficiary Digital Media Independent Distribution Media Trust Trust Erstwhile Erstwhile RIL RIL RIL Public Public Den Public Hathway Companies Companies Promoters Companies Promoters 78.7% 13.4% 7.9% 72.0% 5.9% 22.1% 75.0% 25.0% NW18 (Listed) DEN Hathway 39.6% (Listed) (Listed) 51.2% TV18 IMT + RIL (Listed) Cos: -

Tata Consultancy Services Ltd. TV18 Broadcast Ltd

Tata Consultancy Services TV18 BroadcastLtd. Ltd. RESULT UPDATE 12th October, 2017 RESULT UPDATE 19th April2017 India Equity Institutional Research II Result Update – Q2FY18 II 12th October, 2017 Page 2 TV 18 Broadcast Ltd. Niche Channels Started Bearing Fruit !! CMP Target Potential Upside Market Cap (INR Mn) Recommendation Sector INR 40 INR 57 42.5% 69,174 BUY Media Result highlights •TV18 reported its Q2 FY18 results, where revenues fell below our estimates but margins have improved on yoy basis •Revenue stood at INR 2,272 Mn, up 4% qoq and down 5% yoy •EBITDA (under Ind AS consolidated) stood at INR (1) Mn in Q2 FY18, an improvement over INR (109 Mn) in Q2 FY17 •PAT was recorded at INR 75 Mn in Q2 FY18, versus INR 51 Mn in Q2 FY17, primarily due to improvement in performance of JVs and gaining operating efficiency MARKET DATA KEY FINANCIALS Shares outs (Mn) 1714 Particulars (INR Mn) FY17 FY18E FY19E EquityCap (INR Mn) 3429 Net Sales 9794 10083 10,890 Mkt Cap (INR Mn) 69174 EBITDA 313 445 2,178 52 Wk H/L (INR) 50/33 PAT 191 1520 3,267 EPS 0.11 0.89 1.91 Volume Avg (3m K) 6444.5 OPM 3.2% 4.4% 20.0% Face Value (INR) 2 NPM 2.0% 15.1% 30.0% Bloomberg Code TV18 IN Source: Company, KRChoksey Research SHARE PRICE PERFORMANCE Highlights of Q2 FY18 (i) Revenues in Q2 FY18 were largely subdued, as the market is reviving from GST implications, and traders are still cautious to increase their spending for advertisements. -

A Project Study Report On

A Project Study Report On ―Advertisement Effectiveness‖ Submitted in partial fulfillment for the Award of degree of Master of Business Administration Submitted By: - Submitted To:- Mukesh Kumar Yadav Mrs. Suhasini Varma MBAPart 2nd year HOD MBA 2011-2013 Rajasthan Institute of Engineering & Technology, Bhakrota Jaipur Preface Acknowledgement I express my sincere thanks to my project guide Dr. Suhasini Varma, HOD MBA., for guiding me right from the inception till the successful completion of the project. I sincerely acknowledge her for extending their valuable guidance, support for literature, critical reviews of project and the report and above all the moral support she had provided to me with all stages of this project. I would also like to thank the supporting staff Mrs. Monika Shekhawat Department, for their help and cooperation throughout our project. Mukesh Kumar Yadav Executive Summary Contents 1. Introduction to the Industry 2. Introduction to the Organization 3. Research Methodology 3.1 Title of the Study 3.2 Duration of the Project 3.3 Objective of Study 3.4 Type of Research 3.5 Sample Size and method of selecting sample 3.6 Scope of Study 3.7 Limitation of Study 4. Facts and Findings 5. Analysis and Interpretation 6. SWOT 7. Conclusion 8. Recommendation and Suggestions 9. Appendix 10. Bibliography Introduction to the Industry Indian advertising industry is talking business today and has evolved from being a small-scale business to a full-fledged industry. It has emerged as one of the major industries and tertiary sectors and has broadened its horizons be it the creative aspect, the capital employed or the number of personnel involved. -

Business Strategies in Telecom Sector: a Case of Reliance Jio Infocomm Ltd

RESEARCH PAPER Management Volume : 4 | Issue : 6 | June 2014 | ISSN - 2249-555X Business strategies in Telecom sector: A case of Reliance Jio Infocomm Ltd. KEYWORDS Telecom sector, Decision dynamics, strategic initiatives, Reentry Dr. Vaishali Rahate Prof. Parvin Shaikh Datta Meghe Institute of Management Studies Datta Meghe Institute of Management Studies Nagpur Nagpur India has immense opportunities for telecom operators and is one of the best markets for telecom business. ABSTRACT However it is equally fraught with challenges like Intense competition ,Infrastructure requirement & Rigorous Regulatory framework (License fees, Spectrum allocation & auction etc.) The case traces the series of events which led to the formation of RJio Infocomm and also elaborates about the various strategic initiatives by Mr.Mukesh Ambani,CMD RIL to ensure a successful reentry in the sector. This case presents a brief overview of the decision making dynamics of the CMD, for making a comeback in Telecom sector and also gives an opportunity for further discussion on the future strategies of RIL. Background: India has immense opportunities for telecom operators and Telecom Industry scenario in India is one of the best markets for telecom business. The history of the Indian Telecom sector goes way back to 1851, when the first operational landlines were laid by The Introduction: British Government in Calcutta. With independence, all for- Challenges in Telecom Industry scenario in India eign telecommunication companies were nationalized to The telecom sector in India remains one of the key business form Post, Telephone and Telegraph, a monopoly run by the grounds for telecom giants like Vodafone Group PLC (VOD), Government of India. -

Impact of Reliance JIO on the Indian Telecom Industry

www.ijemr.net ISSN (ONLINE): 2250-0758, ISSN (PRINT): 2394-6962 Volume-7, Issue-3, May-June 2017 International Journal of Engineering and Management Research Page Number: 259-263 Impact of Reliance JIO on the Indian Telecom Industry Noorul Haq Administrative Officer, Kalindi College, University of Delhi, INDIA ABSTRACT MHz band across seven circles. This way JIO has Telecom industry is under severe competition strengthened its passive infrastructure which is the key where number of players are using different marketing and the reason that it can compete with well-established strategies to lure and retain the customers. In the age of telecom players and offer high-speed of data and voice digital technology, this war is producing benefits to the calls. customers. The present study tends to produce the impact Now it has become a challenging time for the of launching of JIO in the Indian Market on the customers and other market players. To study this, references and incumbents. The company had launched its marketable data sources have been analyzed, and the overall impact on services from September 05, 2016, with very attractive the market condition, customer base and profitability of the offers which included free voice calls for lifetime and companies have been taken into consideration in a broader roaming services for its customers along with lowest manner. Besides this, the temporary impact of the JIO in ever data charges at about one-tenth of the prevailing the present conditions as well as the future prospects has rates, reversing a few well set trends of the Indian also been analyzed to understand the impact purposefully. -

India's Telecom Giant Vodafone Idea May Run out of Ideas with Liquidity

NUS Credit Research Initiative nuscri.org India’s telecom giant Vodafone Idea may run out of ideas with liquidity issues looming by Vivane Raj ● NUS-CRI 1-year PD illustrates a significant difference in credit health of Airtel and Vodafone Idea, two of the largest telecom providers in India ● A looming cash crunch and a substantial debt burden weigh heavily on Vodafone Idea, while Airtel fares relatively better with lower debt and growing market share ● NUS-CRI Forward PD indicates that both carriers’ short-term credit risks will increase Once the largest player in the Indian telecommunications sector, Vodafone Idea has suffered significantly as rivals Bharti Airtel (Airtel) and Reliance Jio1 have overtaken the top spots in the market. As a result of a price war with the introduction of Reliance Jio’s near-zero contract rates in 2016, Airtel and Vodafone Idea were forced to sustain prolonged losses in order to match these low rates. Currently, Vodafone Idea is facing cash burn from a burden of unpaid government licensing fees. This is supported by the meteoric jump in the NUS-CRI 1-year Probability of Default (PD) (1-year PD) in 2019 and 2020 for the company. While there was a drop in the PD from its highest levels in Feb 2020 as seen from Figure 1, the NUS-CRI Forward 1-year Probability of Default (Forward PD2) indicates a deterioration in credit outlook for Vodafone Idea (see Figure 3). This is contrasted by Airtel, which managed to weather the storm relatively better. In sum, this brief analyses the credit quality of Vodafone Idea compared to Airtel and explore the factors which have caused this divergence in credit health. -

TV18 Broadcast Limited Annual Accounts - FY : 2016-17 2 TV18 Broadcast Limited

TV18 Broadcast Limited Annual Accounts - FY : 2016-17 2 TV18 Broadcast Limited Independent Auditor’s Report To The Members of TV18 Broadcast Limited Report on the Standalone Ind AS Financial Statements We have audited the accompanying standalone Ind AS financial statements of TV18 Broadcast Limited (“the Company”), which comprise the Balance Sheet as at March 31, 2017, and the Statement of Profit and Loss (including Other Comprehensive Income), the Cash Flow Statement and the Statement of Changes in Equity for the year then ended, and a summary of the significant accounting policies and other explanatory information. Management’s Responsibility for the Standalone Ind AS Financial Statements The Company’s Board of Directors is responsible for the matters stated in Section 134(5) of the Companies Act, 2013 (“the Act”) with respect to the preparation of these standalone Ind AS financial statements that give a true and fair view of the financial position, financial performance including other comprehensive income, cash flows and changes in equity of the Company in accordance with the accounting principles generally accepted in India, including the Indian Accounting Standards (Ind AS) prescribed under section 133 of the Act. This responsibility also includes maintenance of adequate accounting records in accordance with the provisions of the Act for safeguarding the assets of the Company and for preventing and detecting frauds and other irregularities; selection and application of appropriate accounting policies; making judgments and estimates that are reasonable and prudent; and design, implementation and maintenance of adequate internal financial controls, that were operating effectively for ensuring the accuracy and completeness of the accounting records, relevant to the preparation and presentation of the standalone Ind AS financial statements that give a true and fair view and are free from material misstatement, whether due to fraud or error.