Core 1..156 Hansard

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Core 1..186 Hansard (PRISM::Advent3b2 10.50)

CANADA House of Commons Debates VOLUME 141 Ï NUMBER 051 Ï 1st SESSION Ï 39th PARLIAMENT OFFICIAL REPORT (HANSARD) Friday, September 22, 2006 Speaker: The Honourable Peter Milliken CONTENTS (Table of Contents appears at back of this issue.) 3121 HOUSE OF COMMONS Friday, September 22, 2006 The House met at 11 a.m. Foreign Affairs, the actions of the minority Conservative govern- ment are causing the Canadian business community to miss the boat when it comes to trade and investment in China. Prayers The Canadian Chamber of Commerce is calling on the Conservative minority government to bolster Canadian trade and investment in China and encourage Chinese companies to invest in STATEMENTS BY MEMBERS Canada. Business leaders are not alone in their desire for a stronger Ï (1100) economic relationship with China. The Asia-Pacific Foundation [English] released an opinion poll last week where Canadians named China, not the United States, as the most important potential export market CANADIAN FORCES for Canada. Mr. Pierre Lemieux (Glengarry—Prescott—Russell, CPC): Mr. Speaker, I recently met with a special family in my riding. The The Conservatives' actions are being noticed by the Chinese Spence family has a long, proud tradition of military service going government, which recently shut down negotiations to grant Canada back several generations. The father, Rick Spence, is a 27 year approved destination status, effectively killing a multi-million dollar veteran who serves in our Canadian air force. opportunity to allow Chinese tourists to visit Canada. His son, Private Michael Spence, is a member of the 1st Battalion China's ambassador has felt the need to say that we need mutual of the Royal Canadian Regiment. -

Core 1..196 Hansard (PRISM::Advent3b2 10.50)

CANADA House of Commons Debates VOLUME 144 Ï NUMBER 025 Ï 2nd SESSION Ï 40th PARLIAMENT OFFICIAL REPORT (HANSARD) Friday, March 6, 2009 Speaker: The Honourable Peter Milliken CONTENTS (Table of Contents appears at back of this issue.) Also available on the Parliament of Canada Web Site at the following address: http://www.parl.gc.ca 1393 HOUSE OF COMMONS Friday, March 6, 2009 The House met at 10 a.m. Some hon. members: Yes. The Speaker: The House has heard the terms of the motion. Is it the pleasure of the House to adopt the motion? Prayers Some hon. members: Agreed. (Motion agreed to) GOVERNMENT ORDERS Mr. Mark Warawa (Parliamentary Secretary to the Minister of the Environment, CPC) moved that Bill C-17, An Act to Ï (1005) recognize Beechwood Cemetery as the national cemetery of Canada, [English] be read the second time and referred to the Standing Committee on Environment and Sustainable Development. NATIONAL CEMETERY OF CANADA ACT He said: Mr. Speaker, I would like to begin by seeking unanimous Hon. Jay Hill (Leader of the Government in the House of consent to share my time. Commons, CPC): Mr. Speaker, momentarily, I will be proposing a motion by unanimous consent to expedite passage through the The Speaker: Does the hon. member have unanimous consent to House of an important new bill, An Act to recognize Beechwood share his time? Cemetery as the national cemetery of Canada. However, before I Some hon. members: Agreed. propose my motion, which has been agreed to in advance by all parties, I would like to take a quick moment to thank my colleagues Mr. -

Canada Gazette, Part I

EXTRA Vol. 140, No. 3 ÉDITION SPÉCIALE Vol. 140, no 3 Canada Gazette Gazette du Canada Part I Partie I OTTAWA, FRIDAY, FEBRUARY 3, 2006 OTTAWA, LE VENDREDI 3 FÉVRIER 2006 CHIEF ELECTORAL OFFICER DIRECTEUR GÉNÉRAL DES ÉLECTIONS CANADA ELECTIONS ACT LOI ÉLECTORALE DU CANADA Return of Members elected at the 39th general election Rapport de députés(es) élus(es) à la 39e élection générale Notice is hereby given, pursuant to section 317 of the Canada Avis est par les présentes donné, conformément à l’article 317 Elections Act, that returns, in the following order, have been de la Loi électorale du Canada, que les rapports, dans l’ordre received of the election of Members to serve in the House of ci-dessous, ont été reçus relativement à l’élection de députés(es) à Commons of Canada for the following electoral districts: la Chambre des communes du Canada pour les circonscriptions ci-après mentionnées : Electoral Districts Members Circonscriptions Députés(es) South Surrey—White Rock— Russ Hiebert Surrey-Sud—White Rock— Russ Hiebert Cloverdale Cloverdale Kitchener—Conestoga Harold Glenn Albrecht Kitchener—Conestoga Harold Glenn Albrecht Wild Rose Myron Thompson Wild Rose Myron Thompson West Vancouver—Sunshine Blair Wilson West Vancouver—Sunshine Blair Wilson Coast—Sea to Sky Country Coast—Sea to Sky Country Nepean—Carleton Pierre Poilievre Nepean—Carleton Pierre Poilievre Whitby—Oshawa Jim Flaherty Whitby—Oshawa Jim Flaherty Saint-Hyacinthe—Bagot Yvan Loubier Saint-Hyacinthe—Bagot Yvan Loubier Sudbury Diane Marleau Sudbury Diane Marleau Toronto—Danforth -

Trudeau Attacks Calls to Close Borders: “There Is a Lot of Knee-Jerk Reaction That Isn’T Keeping People Safe”

The road to Canada's COVID-19 outbreak, Pt. 3: timeline of federal government failure at border to slow the virus Author of the article: David Staples • Edmonton Journal Publishing date: April 3, 2020 • 29 minute read Prime Minister Justin Trudeau speaks from behind a podium bearing the hyperlink to a federal government website about the coronavirus disease during a press conference about COVID-19 in front of his residence at Rideau Cottage in Ottawa, on Sunday, March 22, 2020. JUSTIN TANG / THE CANADIAN PRESS Pt. 3, March: Trudeau attacks calls to close borders: “There is a lot of knee-jerk reaction that isn’t keeping people safe” COVID-19 exploded upon the world in March 2020, shutting down much of the economy in Europe and North America by mid-month, just as it had already done in Asia in January and February. But early in the month, the Liberal government in Ottawa clung to the notion that it must not close its borders to travellers, or quarantine them when they arrived, even as that was by then standard practice in Asia, and even as infection brought in by travellers were spreading in Canadian towns and cities. Yet by the end of the month, the Liberal policy did a complete about-face, shutting down our borders. In Parts 1 and 2, we looked at the multi-partisan in effort to dig in and question Canada‟s border policies on COVID-19. In Part. 3 of our series, the timeline is extended into March, detailing the key quotes and debates leading to the federal policy change. -

ÉCOLE DE POLITIQUE APPLIQUÉE Faculté

ÉCOLE DE POLITIQUE APPLIQUÉE Faculté des lettres et sciences humaines Université de Sherbrooke Le rôle du Renouveau Sherbrookois lors des élections municipales de 2009 à Sherbrooke Par Vincent Boutin Professeurs membres du jury : Mme Isabelle Lacroix, directrice Mme Eugénie Dostie-Goulet, lectrice M. Jean-Herman Guay, lecteur 18 septembre 2012 Library and Archives Bibliothèque et Canada Archives Canada Published Héritage Direction du Branch Patrimoine de l'édition 395 Wellington Street 395, rue Wellington Ottawa ON K1A0N4 Ottawa ON K1A 0N4 Canada Canada Your file Votre référence ISBN: 978-0-494-90961-4 Our file Notre référence ISBN: 978-0-494-90961-4 NOTICE: AVIS: The author has granted a non- L'auteur a accordé une licence non exclusive exclusive license allowing Library and permettant à la Bibliothèque et Archives Archives Canada to reproduce, Canada de reproduire, publier, archiver, publish, archive, preserve, conserve, sauvegarder, conserver, transmettre au public communicate to the public by par télécommunication ou par l'Internet, prêter, télécommunication or on the Internet, distribuer et vendre des thèses partout dans le loan, distrbute and sell theses monde, à des fins commerciales ou autres, sur worldwide, for commercial or non- support microforme, papier, électronique et/ou commercial purposes, in microform, autres formats. paper, electronic and/or any other formats. The author retains copyright L'auteur conserve la propriété du droit d'auteur ownership and moral rights in this et des droits moraux qui protégé cette thèse. Ni thesis. Neither the thesis nor la thèse ni des extraits substantiels de celle-ci substantial extracts from it may be ne doivent être imprimés ou autrement printed or otherwise reproduced reproduits sans son autorisation. -

PRISM::Advent3b2 8.25

HOUSE OF COMMONS OF CANADA CHAMBRE DES COMMUNES DU CANADA 39th PARLIAMENT, 1st SESSION 39e LÉGISLATURE, 1re SESSION Journals Journaux No. 1 No 1 Monday, April 3, 2006 Le lundi 3 avril 2006 11:00 a.m. 11 heures Today being the first day of the meeting of the First Session of Le Parlement se réunit aujourd'hui pour la première fois de la the 39th Parliament for the dispatch of business, Ms. Audrey première session de la 39e législature, pour l'expédition des O'Brien, Clerk of the House of Commons, Mr. Marc Bosc, Deputy affaires. Mme Audrey O'Brien, greffière de la Chambre des Clerk of the House of Commons, Mr. R. R. Walsh, Law Clerk and communes, M. Marc Bosc, sous-greffier de la Chambre des Parliamentary Counsel of the House of Commons, and Ms. Marie- communes, M. R. R. Walsh, légiste et conseiller parlementaire de Andrée Lajoie, Clerk Assistant of the House of Commons, la Chambre des communes, et Mme Marie-Andrée Lajoie, greffier Commissioners appointed per dedimus potestatem for the adjoint de la Chambre des communes, commissaires nommés en purpose of administering the oath to Members of the House of vertu d'une ordonnance, dedimus potestatem, pour faire prêter Commons, attending according to their duty, Ms. Audrey O'Brien serment aux députés de la Chambre des communes, sont présents laid upon the Table a list of the Members returned to serve in this dans l'exercice de leurs fonctions. Mme Audrey O'Brien dépose sur Parliament received by her as Clerk of the House of Commons le Bureau la liste des députés qui ont été proclamés élus au from and certified under the hand of Mr. -

Télécharger Le Fichier (PDF )

Jacques Gagnon 71 BILAN POLITIQUE DES CANTONS-DE-L’EST 2006–2012 Jacques Gagnon, chercheur autonome Sherbrooke Résumé Faisant suite à des bilans similaires publiés dans la revue et ailleurs1, cet article fait le bilan des modifications de la carte électorale, des résultats des élections fédérales de 2008 et 2011 et provinciales de 2007, 2008 et 2012, du personnel politique et de quelques enjeux touchant la région des Cantons-de-l’Est, de 2006 à 2012. Abstract Following the publication of similar assessments in this journal and other publications1, this article draws up the modifications to the electoral map, the results of the 2008 and 2011 federal elections, and the 2007, 2008 and 2012 provincial elections, the political personalities and some issues pertaining to the Eastern Townships from 2006 to 2012. Toponymie et démographie Deux municipalités régionales de comté (MRC) ont changé de nom en 2006 et 2008, soit la MRC d’Asbestos rebaptisée Les Sources et la MRC de L’Amiante renommée Les Appalaches. Faut-il se surprendre de l’abandon de toute référence toponymique au minerai qui fit autrefois la fortune de ces sous-régions? De plus, la municipalité de Bromont est détachée en 2009 de la MRC de la Haute-Yamaska pour se greffer à la MRC de Brome-Missisquoi à la suite d’un référendum local portant sur cette question. On constate par ailleurs que la démographie régionale évolue peu, contrairement à celle de la métropole et des capitales provinciale et fédérale. Le tableau qui suit en donne la preuve : 72 REVUE D’ÉTUDES DES CANTONS-DE-L’EST -

De Doute Sur Le Lancement Des Élections Aujourd'hui

f C f \ * * : ; ■.. ■: ■ 80e ANNEE — No 145 4 CAHIERS. 36 PAGES SHERBROOKE, 9 AOUT 1989 (WEEK END 1.00$) 0.50e — Domicile 2 85$ par semaine Revers de 4-2: la pire séquence de la saison pour les Expos DI Avant que 1la Cour suprême ait consenti à casser 1l'injonction Chantal Daigle se lait avorter par Marie TISON plus haut tribunal du pays de L’avocat de Chantal Daigle, Me pas théorique, même si l’avor OTTAWA (PC) - Chantal casser l’injonction qui l’empê Daniel Bédard, a été incapable de tement avait été pratiqué. Il a ex Daigle a obtenu un avor chait de mettre un terme à sa dire où et quand l’avortement a pliqué que Mme Daigle pouvait grossesse, par un jugement una été pratiqué. être accusée d’outrage au tribu tement sans attendre la permis nal, qu’une action en dommages sion de la Cour suprême du Ca nime rendu séance tenante, en et intérêts pouvait être intentée nada. Ce qui n’a pas empêché le toute fin d’après-midi hier. contre elle et que toutes les fem mes du Québec étaient toujours assujetties au jugement de la Cour d’appel du Québec. «Je crois qu’il faut continuer le la nouvelle taxe débat avant que la situation ne devienne chaotique», a-t-il décla ré. L’avocat de l’ex-ami Jean-Guy Wilson profitera surtout Tremblay, Me Henri Kelada, a déclaré au contraire que la cause devait être abandonnée. au reste du Canada «C’est un litige privé, a-t-il af firmé. -

Twitter En Tant Que Sphère Publique Numérique : Les Élections Générales

Twitter en tant que sphère publique numérique : les élections générales au Québec en 2014 Katherine Sullivan Thèse présentée à la Faculté des études supérieures et postdoctorales de l’Université d'Ottawa dans le cadre du programme de maîtrise en communication pour l'obtention du grade Maîtrise ès Arts (M.A) Sous la supervision de Pierre C. Bélanger, Ph. D © Katherine Sullivan, Ottawa, Canada, 2015 ii Sommaire L’accessibilité, la popularité et la fonctionnalité des médias sociaux s’immiscent peu à peu dans les formes de communication politique. Lors des élections générales au Québec en 2014, le service de microblogage Twitter a servi d’espace aux débats et au partage d’information tant pour les citoyens que les politiciens. En validant le concept de la sphère publique d’Habermas dans un contexte numérique, cette thèse vise à cerner les potentialités cyberdémocratiques de Twitter. Nous nous intéressons aux manières avec lesquelles 26 candidats québécois ont fait usage de Twitter pendant la période officielle de la campagne, soit entre le 5 mars et le 7 avril 2014. Près de 13 000 messages numériques publiés par 26 candidats québécois ont été analysés afin d’en dégager les modalités d’usage. Ceux-ci ont été quantifiés de façon à déterminer si leur utilisation s’inscrit dans une optique de marketing politique ou de sphère publique numérique. À la lumière de nos résultats, force est de constater que Twitter a été majoritairement utilisé dans une optique de marketing politique par une majorité des candidats associés aux Parti Québécois, Parti Libéral du Québec et la Coalition Avenir Québec. -

The Hill Times' Insider's Guide To

ELECTIONThe Hill Times’ Insider’s 2019 Guide to Justin Tr ud ea u C h a r l Rod i lo r e b i a g A P u n g e u s z K eth Ma a ab y t z ie i ry l a a T M m E e C Y l Str M f v k a h r h o e r o a r l n s y d s - M e f F s t r t i a e a n h ing c h F ç S R o y n t r i e a a e s l e c m B e e a l a r m n s d g T e oo ice y S G da a d B e h l J B n er a e a g m lp i C e l n u a l N s B a R l v O a i d d r ’ e R e p e B g a s a i n n Ger Karin L al a n ly i d ja Jo s G i e B zie Po a i a SEPTEMBER 16, 2019 u o t S n n t R u e e a r t l t l i a t d K j é s r i t a t A M l H ex a n d Harris r B o len ros ck n e l B a E s o B la e A r B l a r e g h i a u u t B a n o h s n u u c i d l C R r e l o w e r M w i c e S c Ast h r C e e a r ta v a i a r o s l Z Bern y e ier A A m A n xi l a a B i M n n e i n f s e e n Bro e R r y y a J a d n H m h e t e t r u o e w r J s a t r d l Sch ie o w n B a D i l l M o r n e a u CONTENTS 11 03 Races to Watch Liberal War Room Top 25 juiciest races to Campaigning ‘from the front’ watch in this election will test Liberal strategists By Aidan Chamandy By Abbas Rana & Neil Moss 04 12 Conservative Political advertising War Room Liberal election ad ‘head and Tried and tested team shoulders’ above Conservative, behind Conservative Party’s NDP offerings, says bid to return to government U.S. -

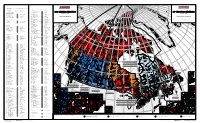

Map of Canada, Official Results of the 38Th General Election – PDF Format

2 5 3 2 a CANDIDATES ELECTED / CANDIDATS ÉLUS Se 6 ln ln A nco co C Li in R L E ELECTORAL DISTRICT PARTY ELECTED CANDIDATE ELECTED de ELECTORAL DISTRICT PARTY ELECTED CANDIDATE ELECTED C er O T S M CIRCONSCRIPTION PARTI ÉLU CANDIDAT ÉLU C I bia C D um CIRCONSCRIPTION PARTI ÉLU CANDIDAT ÉLU É ol C A O N C t C A H Aler 35050 Mississauga South / Mississauga-Sud Paul John Mark Szabo N E !( e A N L T 35051 Mississauga--Streetsville Wajid Khan A S E 38th GENERAL ELECTION R B 38 ÉLECTION GÉNÉRALE C I NEWFOUNDLAND AND LABRADOR 35052 Nepean--Carleton Pierre Poilievre T A I S Q Phillip TERRE-NEUVE-ET-LABRADOR 35053 Newmarket--Aurora Belinda Stronach U H I s In June 28, 2004 E T L 28 juin, 2004 É 35054 Niagara Falls Hon. / L'hon. Rob Nicholson E - 10001 Avalon Hon. / L'hon. R. John Efford B E 35055 Niagara West--Glanbrook Dean Allison A N 10002 Bonavista--Exploits Scott Simms I Z Niagara-Ouest--Glanbrook E I L R N D 10003 Humber--St. Barbe--Baie Verte Hon. / L'hon. Gerry Byrne a 35056 Nickel Belt Raymond Bonin E A n L N 10004 Labrador Lawrence David O'Brien s 35057 Nipissing--Timiskaming Anthony Rota e N E l n e S A o d E 10005 Random--Burin--St. George's Bill Matthews E n u F D P n d ely E n Gre 35058 Northumberland--Quinte West Paul Macklin e t a s L S i U a R h A E XEL e RÉSULTATS OFFICIELS 10006 St. -

Court File No.: CV-18-00605134-00CP ONTARIO

Court File No.: CV-18-00605134-00CP ONTARIO SUPERIOR COURT OF JUSTICE BETWEEN: MICKY GRANGER Plaintiff - and - HER MAJESTY THE QUEEN IN RIGHT OF THE PROVINCE OF ONTARIO Defendant Proceeding under the Class Proceedings Act, 1992 MOTION RECORD OF THE PLAINTIFF (CERTIFICATION) (Returnable November 27 & 28, 2019) VOLUME II of II March 18, 2019 GOLDBLATT PARTNERS LLP 20 Dundas Street West, Suite 1039 Toronto ON M5G 2C2 Jody Brown LS# 58844D Tel: 416-979-4251 / Fax: 416-591-7333 Email: [email protected] Geetha Philipupillai LS# 74741S Tel.: 416-979-4252 / Fax: 416-591-7333 Email: [email protected] Lawyers for the Plaintiff - 2 TO: HER MAJESTY THE QUEEN IN RIGHT - OF THE PROVINCE OF ONTARIO Crown Law Office – Civil Law 720 Bay Street, 8th Floor Toronto, ON, M5G 2K1 Amy Leamen LS#: 49351R Tel: 416.326.4153 / Fax: 416.326.4181 Lawyers for the Defendant TABLE OF CONTENTS TAB DESCRIPTION PG # 1. Notice of Motion (Returnable November 27 and 28, 2019) 1 A. Appendix “A” – List of Common Issues 6 2. Affidavit of Micky Granger (Unsworn) 8 3. Affidavit of Tanya Atherfold-Desilva sworn March 18, 2019 12 A. Exhibit “A”: Office of the Independent Police Review Director – 20 Systemic Review Report dated July 2016 B. Exhibit “B”: Office of the Independent Police Review Director - 126 Executive Summary and Recommendations dated July 2016 C. Exhibit “C”: Office of the Independent Police Review Director – Terms of 142 Reference as of March 2019 D. Exhibit “D”: Affidavit of David D.J. Truax sworn August 30, 2016 146 E. Exhibit “E”: Centre of Forensic Investigators & Submitters Technical 155 Information Sheets effective April 2, 2015 F.