Contents Background

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Logistics Capacity Assessment

LCA – Liberia Version 1.05 Logistics Capacity Assessment LIBERIA Country Name Liberia Official Name Republic of Liberia Assessment Assessment Dates: From 7th November 2009 To 3rd December 2009 Name of the Assessors Thierry Schweitzer assisted by Mårten Kihlström Title Consultant [email protected] & [email protected] Email contact GLCSC Rome: [email protected] 1//88 LCA – Liberia Version 1.05 1. Table of Contents 1. Table of Contents ...................................................................................................................................... 2 2. Country Profile .......................................................................................................................................... 3 2.1. Introduction & Background ................................................................................................................ 3 2.2. Humanitarian Background ................................................................................................................. 6 2.3. Contact List – NGO‟s ....................................................................................................................... 11 2.4. National Regulatory Departments ................................................................................................... 14 2.5. Customs Information ....................................................................................................................... 15 3. Logistics Infrastructure ........................................................................................................................... -

U.S. Department of Transportation Federal

U.S. DEPARTMENT OF ORDER TRANSPORTATION JO 7340.2E FEDERAL AVIATION Effective Date: ADMINISTRATION July 24, 2014 Air Traffic Organization Policy Subject: Contractions Includes Change 1 dated 11/13/14 https://www.faa.gov/air_traffic/publications/atpubs/CNT/3-3.HTM A 3- Company Country Telephony Ltr AAA AVICON AVIATION CONSULTANTS & AGENTS PAKISTAN AAB ABELAG AVIATION BELGIUM ABG AAC ARMY AIR CORPS UNITED KINGDOM ARMYAIR AAD MANN AIR LTD (T/A AMBASSADOR) UNITED KINGDOM AMBASSADOR AAE EXPRESS AIR, INC. (PHOENIX, AZ) UNITED STATES ARIZONA AAF AIGLE AZUR FRANCE AIGLE AZUR AAG ATLANTIC FLIGHT TRAINING LTD. UNITED KINGDOM ATLANTIC AAH AEKO KULA, INC D/B/A ALOHA AIR CARGO (HONOLULU, UNITED STATES ALOHA HI) AAI AIR AURORA, INC. (SUGAR GROVE, IL) UNITED STATES BOREALIS AAJ ALFA AIRLINES CO., LTD SUDAN ALFA SUDAN AAK ALASKA ISLAND AIR, INC. (ANCHORAGE, AK) UNITED STATES ALASKA ISLAND AAL AMERICAN AIRLINES INC. UNITED STATES AMERICAN AAM AIM AIR REPUBLIC OF MOLDOVA AIM AIR AAN AMSTERDAM AIRLINES B.V. NETHERLANDS AMSTEL AAO ADMINISTRACION AERONAUTICA INTERNACIONAL, S.A. MEXICO AEROINTER DE C.V. AAP ARABASCO AIR SERVICES SAUDI ARABIA ARABASCO AAQ ASIA ATLANTIC AIRLINES CO., LTD THAILAND ASIA ATLANTIC AAR ASIANA AIRLINES REPUBLIC OF KOREA ASIANA AAS ASKARI AVIATION (PVT) LTD PAKISTAN AL-AAS AAT AIR CENTRAL ASIA KYRGYZSTAN AAU AEROPA S.R.L. ITALY AAV ASTRO AIR INTERNATIONAL, INC. PHILIPPINES ASTRO-PHIL AAW AFRICAN AIRLINES CORPORATION LIBYA AFRIQIYAH AAX ADVANCE AVIATION CO., LTD THAILAND ADVANCE AVIATION AAY ALLEGIANT AIR, INC. (FRESNO, CA) UNITED STATES ALLEGIANT AAZ AEOLUS AIR LIMITED GAMBIA AEOLUS ABA AERO-BETA GMBH & CO., STUTTGART GERMANY AEROBETA ABB AFRICAN BUSINESS AND TRANSPORTATIONS DEMOCRATIC REPUBLIC OF AFRICAN BUSINESS THE CONGO ABC ABC WORLD AIRWAYS GUIDE ABD AIR ATLANTA ICELANDIC ICELAND ATLANTA ABE ABAN AIR IRAN (ISLAMIC REPUBLIC ABAN OF) ABF SCANWINGS OY, FINLAND FINLAND SKYWINGS ABG ABAKAN-AVIA RUSSIAN FEDERATION ABAKAN-AVIA ABH HOKURIKU-KOUKUU CO., LTD JAPAN ABI ALBA-AIR AVIACION, S.L. -

Globaler Airline-Newsletter Von Berlinspotter.De

Globaler Airline-Newsletter von Berlinspotter.de Sehr geehrte Leser, Hiermit erhalten Sie als PDF die europäischen und globalen Airline-News aus dem Bearbeitungszeitraum 2. bis 15. April – unterteilt in die Update-Blöcke der Premium- Version (ein Wechsel ist jederzeit möglich). Ich danke Ihnen für die Unterstützung des einzigen deutschsprachigen Luftfahrt- Newsletter. Mit freundlichen Grüßen Oliver Pritzkow Webmaster Berlinspotter.de --- 5.4. --- EUROPA Aegean Airlines stellte eine 737-300 (SX-BGW, msn 29264) außer Dienst. Sie ging an Deutsche Structured Finance zurück. Im Gegenzug übernahm man einen werksneuen Airbus A320-200 (SX-DVM, msn 3439). Air Baltic erhielt eine ex-Air Berlin 737-300 (YL-BBJ, msn 30333) per Leasing von Boullioun Aviation Services. Air Berlin bekommt einen neuen Großaktionär. Access Industries wird den Anteil der Vatas-Tochter Haarlem One in Höhe von 18,56 % übernehmen. Vatas war erst im Januar 2008 bei Air Berlin eingestiegen und hatte ihren Anteil rasch erhöht. Allerdings liegt das Aktienpaket derzeit bei der NordLB. Diese hatte vom Pfandrecht Gebrauch gemacht und sich als Sicherheit für geplatzte Aktiengeschäfte mit Vatas dieses Paket geholt. Access Industries gehört dem russischstämmigen US-Milliardär Leonard Blawatnik. Weitere Beteiligungen sind der british-russische Ölförderer TNK- BP sowie der russische Aluminiumkonzern Rusal. Die Air Berlin-Aktie legte zunächst um fast 10 5 % zu, nachdem sie erst wenige Tage zuvor aufgrund einer gesenkten Gewinnprognose einbrach. Als die Pfändung des Aktienpakets bekannt wurde, sank sie auf 5 %. Air France nahm am 1. April die erste Route unter dem neuen USA-Europa- OpenSky-Abkommen auf. Vom Flughafen London Heathrow hob man in Kooperation mit Partner Delta Air Lines zum ersten Direktflug nach Los Angeles ab. -

Only Fools Who Send Hyenas to Roast Meat for Them: in Search of the Doctrinal Foundations of the Not-So-Ordinary Crime of Patrimonicide Ndiva Kofele-Kale

Florida A & M University Law Review Volume 9 Article 3 Number 1 Celebrating Our Legacy Fall 2013 Only Fools Who Send Hyenas to Roast Meat for Them: In Search of the Doctrinal Foundations of the Not-So-Ordinary Crime of Patrimonicide Ndiva Kofele-Kale Follow this and additional works at: http://commons.law.famu.edu/famulawreview Part of the Criminal Law Commons, Human Rights Law Commons, and the International Law Commons Recommended Citation Ndiva Kofele-Kale, Only Fools Who Send Hyenas to Roast Meat for Them: In Search of the Doctrinal Foundations of the Not-So-Ordinary Crime of Patrimonicide, 9 Fla. A&M U. L. Rev. (2013). Available at: http://commons.law.famu.edu/famulawreview/vol9/iss1/3 This Article is brought to you for free and open access by Scholarly Commons @ FAMU Law. It has been accepted for inclusion in Florida A & M University Law Review by an authorized editor of Scholarly Commons @ FAMU Law. For more information, please contact [email protected]. ONLY FOOLS WHO SEND HYENAS TO ROAST MEAT FOR THEM: IN SEARCH OF THE DOCTRINAL FOUNDATIONS OF THE NOT-SO- ORDINARY CRIME OF PATRIMONICIDE Ndiva Kofele-Kale* ABSTRACT Crimes against humanity are generally considered crimes of such unimaginable horror that they shock the conscience of mankind. The Article challenges the international community to take a mental leap by recognizing that the contemporary version of official corruption is so fundamentally different from its historical antecedents that it de- serves to (a) be called a different name: indigenous spoliation or patrimonicide; and (b), to be treated as an extraordinary crime that rises up to the level of a crime against humanity. -

Prior Compliance List of Aircraft Operators Specifying the Administering Member State for Each Aircraft Operator – June 2014

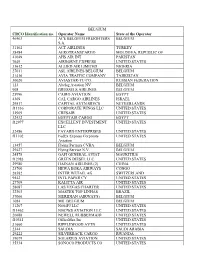

Prior compliance list of aircraft operators specifying the administering Member State for each aircraft operator – June 2014 Inclusion in the prior compliance list allows aircraft operators to know which Member State will most likely be attributed to them as their administering Member State so they can get in contact with the competent authority of that Member State to discuss the requirements and the next steps. Due to a number of reasons, and especially because a number of aircraft operators use services of management companies, some of those operators have not been identified in the latest update of the EEA- wide list of aircraft operators adopted on 5 February 2014. The present version of the prior compliance list includes those aircraft operators, which have submitted their fleet lists between December 2013 and January 2014. BELGIUM CRCO Identification no. Operator Name State of the Operator 31102 ACT AIRLINES TURKEY 7649 AIRBORNE EXPRESS UNITED STATES 33612 ALLIED AIR LIMITED NIGERIA 29424 ASTRAL AVIATION LTD KENYA 31416 AVIA TRAFFIC COMPANY TAJIKISTAN 30020 AVIASTAR-TU CO. RUSSIAN FEDERATION 40259 BRAVO CARGO UNITED ARAB EMIRATES 908 BRUSSELS AIRLINES BELGIUM 25996 CAIRO AVIATION EGYPT 4369 CAL CARGO AIRLINES ISRAEL 29517 CAPITAL AVTN SRVCS NETHERLANDS 39758 CHALLENGER AERO PHILIPPINES f11336 CORPORATE WINGS LLC UNITED STATES 32909 CRESAIR INC UNITED STATES 32432 EGYPTAIR CARGO EGYPT f12977 EXCELLENT INVESTMENT UNITED STATES LLC 32486 FAYARD ENTERPRISES UNITED STATES f11102 FedEx Express Corporate UNITED STATES Aviation 13457 Flying -

Logistics Capacity Assessment

INTER-AGENCY-LCA - Sierra Leone Logistics Capacity Assessment Sierra Leone Country Name Sierra Leone Official Name Republic of Sierra Leone Assessment Assessment Dates: From 1st December 2009 To 1st January 2010 Name of the Assessor Yann Ilboudo Title Cluster Logistics Officer Email Contact [email protected] 1/98 INTER-AGENCY-LCA - Sierra Leone Table of Contents 1. Country Profile ................................................................................................................................................................... 3 1.1. Introduction / Background ....................................................................................................................................... 3 1.2. Humanitarian Background ....................................................................................................................................... 5 1.3. National Regulatory Departments .......................................................................................................................... 8 1.4. Customs Information ............................................................................................................................................... 9 2. Logistics Infrastructure .................................................................................................................................................... 18 2.1. Port Assessment ................................................................................................................................................... -

Group ROW by State of Administration

Prior compliance list of aircraft operators specifying the administering Member State for each aircraft operator – June 2013 Inclusion in the prior compliance list allows aircraft operators to know which Member State will most likely be their administering Member State in a close future so they can get in contact with the competent authority of that Member State to discuss the requirements and the next steps. Due to a number of reasons, and especially because a number of aircraft operators use services of management companies, some of those operators have not been identified in the latest update of the EEA- wide list of aircraft operators adopted on 29 January 2013. The present version of the prior compliance list includes those aircraft operators, which have submitted their fleet lists between 9 December 2012 and January 2013. It also preliminary informs aircraft operators which may be affected by the accession of Croatia to the EU i.e Croatia may become their administering Member State. BELGIUM CRCO Identification no. Operator Name State of the Operator 123 Abelag Aviation BELGIUM 31102 ACT AIRLINES TURKEY 7649 AIRBORNE EXPRESS UNITED STATES 33612 ALLIED AIR LIMITED NIGERIA 30020 AVIASTAR-TU CO. RUSSIAN FEDERATION 31416 AVIA TRAFFIC COMPANY RUSSIAN FEDERATION 908 BRUSSELS AIRLINES BELGIUM 25996 CAIRO AVIATION EGYPT 4369 CAL CARGO AIRLINES ISRAEL 29517 CAPITAL AVTN SRVCS NETHERLANDS f11336 CORPORATE WINGS LLC UNITED STATES 32909 CRESAIR INC UNITED STATES 32432 EGYPTAIR CARGO EGYPT f12977 EXCELLENT INVESTMENT UNITED STATES LLC f11102 -

General Introduction and Ex-President Jammeh's

The Commission of Inquiry COMMISSION OF INQUIRY INTO THE FINANCIAL ACTIVITES OF PUBLIC BODIES, ENTERPRISES AND OFFICES AS REGARDS THEIR DEALINGS WITH FORMER PRESIDENT YAHYA A.J.J. JAMMEH AND CONNECTED MATTERS REPORT VOLUMES 1 & 2 GENERAL INTRODUCTION & EX-PRESIDENT JAMMEH’S FINANCIAL DEALINGS & CORRUPTION (BANK ACCOUNTS) 10th AUGUST 2017 - 29th MARCH 2019 The Commission of Inquiry CONTENTS Page ACKNOWLEDGEMENT 3 - 4 VOLUME 1 General Introduction 5 – 40 VOLUME 2 Introduction 41 Chapter 1 Central Bank Accounts 41 - 132 Chapter 2 Accounts with Guaranty Trust Bank Limited 133 - 156 Chapter 3 Accounts with Trust Bank Limited 157 - 193 Chapter 4 Accounts with Other Banks 194 Chapter 5 Gambia Embassy in Washington – Procurement Accounts 195 - 196 Chapter 6 APRC Accounts 197 – 200 APPENDIX 1 201 - 203 Chapter 7 Recommendations 204 - 212 2 The Commission of Inquiry ACKNOWLEDGEMENTS A few of us are ever given the opportunity or occasion to serve our country in some unique way during our lifetime. This Commission of Inquiry has been unique in many ways. Of these, we believe the most important is its potential to help shape the future direction of our country by avoiding some of the exposed pitfalls and follies of the past 22 years. We recognize the honour of having been given the opportunity to serve, and in this regard, would like to express our gratitude to the President of the Republic of The Gambia, His Excellency, Adama Barrow, for the great honor we have been accorded in our appointment to this national assignment. Many Commissions of Inquiry preceded this Commission. However, no other Gambian Commission is yet to be confronted by a task of such magnitude and complexity, as is apparent from this Report. -

A Case Study of the Tourism Industry in Cameroon

SUSTAINABLE TOURISM DEVELOPMENT MANAGEMENT IN CENTRAL AFRICA: A CASE STUDY OF THE TOURISM INDUSTRY IN CAMEROON. ALBERT NSOM KIMBU A thesis submitted in partial fulfilment of the requirements of Nottingham Trent University for the degree of Doctor of Philosophy Nottingham Business School Nottingham Trent University May 2010 © Albert N. Kimbu Copyright Statement This work is the intellectual property of the author. You may copy up to 5% of this work for private study, or personal, non-commercial research. Any re-use of the information contained within this document should be fully referenced, quoting the author, title, university, degree level and pagination. Queries or requests for any other use, or if a more substantial copy is required, should be directed in the owner(s) of the Intellectual Property Rights. II Abstract The tourism industry in sub-Saharan Africa has been experiencing one of the fastest growth rates in the last decade at more than 10% in 2006, +7% in 2007 and +5% in 2008 and 2009 respectively and this positive trend is predicted to continue in future in spite of the present global recession. However, there are significant variations in tourism growth between the various countries and different sub-regions. Until now, there has been no detailed examination by researchers to find out the reasons for these variations in general and the stagnation and even decline in tourism growth observed in countries of the Central African sub-region in particular, which have recognised natural and socio-cultural potentials of developing a thriving sustainable tourism industry. Using Cameroon as a case study, this research examines the reasons of this stagnation in the Central African sub-region, and explores the possibility of tailoring, adapting and/or applying the key concepts of sustainable tourism in developing and managing the tourism industry in the Central African sub-region which is still at an early stage of development through the conception of a strategic framework for sustainable tourism development management in Cameroon. -

2013 Official Country Guide by the GAMBIA TOURISM BOARD the GAMBIA the SMILING COAST of AFRICA 1 Contents

2013 Official Country Guide BY THE GAMBIA TOURISM BOARD THE GAMBIA THE SMILING COAST OF AFRICA 1 Contents Welcome to the Smiling Coast of Africa 4 Discover nature in The Gambia 24 Our Message To You 5 Fishing 29 Country info 6 Earth friendly places 30 The history of the land 8 The adventurous you 32 A quick view 10 Insights into Cruises to The Gambia 34 What to see ... or what to do ... 12/13 Access to cash 35 The laid-back you 14 Getting here 36 The sporty you 15 Tourism info 38 The Gambia Beach Boogie 16 The artful you 17 The cultural you 17 The fashionable you 18 The cool in you 19 Eating Out 20 The business you 21 Roots 22 For your natural side 23 2 THE GAMBIA THE SMILING COAST OF AFRICA Welcome to the Smiling Coast of Africa Our Message To You Thank you for picking up a copy of our 2013 Official Country Guide edition. It gives me great pleasure as Minister of Tourism and Culture to introduce This annual publication is intended to keep you abreast of developments this brand new edition of our Visitors Guide, a flagship publication of The in the Tourism Industry of The Gambia; a formidable world class destination Gambia Tourism Board. This new updated and greatly expanded edition renowned for its hospitable and friendly people; attributes that has earned provides a comprehensive showcase of the range of attractions in terms of the destination the globally recognized slogan…”The Smiling Coast of cultural patrimony, eco-tourism, exotic fauna and flora, trendy and exquisite Africa.” resort facilities available throughout our beautiful country. -

Eine Fähre Für Senegal

230 231 sen013_012 tb Praktische Reisetipps A–Z Anreise | 232 Diplomatische Vertretungen | 242 Ein- und Ausreisebestimmungen | 243 Geld und Finanzen | 253 Gesundheit | 256 Notfall | 260 Reisezeit | 263 Sicherheit und Kriminalität | 264 Unterkunft | 266 Verkehrsmittel | 268 j Bunt & billig: Minibus in Senegal 232 Anreise Anreise Linienflüge nach Senegal Derzeit existieren keine Direktflüge von Deutschland nach Senegal. Wer nach Dakar will, muss also mindestens einen Zwischenstopp einkalkulieren. Täglich eine Verbindung bietet Air France via Paris-CDG. Französische Chartergesell- schaften starten in der Regel von Paris- Orly. Ebenfalls täglich fliegt Royal Air Maroc mit Zubringerflügen von Deutsch - land via Casablanca. Weitere Airlines mit Destination Dakar sind u.a. Brussels Airlines (via Brüssel), TAP (Air Portugal, mit Stopp in Lissabon) und Iberia (Zwi- schenlandung in Madrid bzw. Las Pal- mas). Die 2011 gestartete halbstaatliche Fluglinie Senegal Airlines bedient keine europäischen Flughäfen, sondern kon- sen_052 tb zentriert sich ganz auf den westafrikani- schen Markt. Geldwechsler und Taxifahrer konfron- tiert. Auf der sicheren Seite sind Pau- Flughafen in Senegal schaltouristen und Reisende, die im Auf- trag ihres Hotels abgeholt werden. Für Wer im Internet nach dem „schlimms - alle anderen gilt: Ruhe bewahren! Las- ten Flughafen der Welt“ googelt, be- sen Sie sich nicht auf dubiose Angebote kommt nicht selten zur Antwort: Aéro- ein. Legen Sie sich vorsorglich auf eine port Léopold Sédar Senghor in Dakar. Unterkunft Ihrer Wahl fest. Vereinbaren Grund: Die technische Ausstattung ist Sie mit dem Taxifahrer den Fahrpreis hoffnungslos veraltet, die Kapazität un- und ignorieren Sie sämtliche Vermittler. zureichend, es gibt praktisch keine Sitz- Nachts – praktisch alle Flüge aus Europa plätze und das Personal ist wegen dem landen nach 22 Uhr – sollten Sie für täglichen Chaos meist demotiviert und Fahrten in die City nicht mehr als 5000 unfreundlich. -

Group ROW by State of Administration

BELGIUM CRCO Identification no. Operator Name State of the Operator 46463 ACE BELGIUM FREIGHTERS BELGIUM S.A. 31102 ACT AIRLINES TURKEY 38484 AEROTRANSCARGO MOLDOVA, REPUBLIC OF 41049 AHS AIR INT PAKISTAN 7649 AIRBORNE EXPRESS UNITED STATES 33612 ALLIED AIR LIMITED NIGERIA 27011 ASL AIRLINES BELGIUM BELGIUM 31416 AVIA TRAFFIC COMPANY TAJIKISTAN 30020 AVIASTAR-TU CO. RUSSIAN FEDERATION 123 Abelag Aviation NV BELGIUM 908 BRUSSELS AIRLINES BELGIUM 25996 CAIRO AVIATION EGYPT 4369 CAL CARGO AIRLINES ISRAEL 29517 CAPITAL AVTN SRVCS NETHERLANDS f11336 CORPORATE WINGS LLC UNITED STATES 32909 CRESAIR UNITED STATES 32432 EGYPTAIR CARGO EGYPT f12977 EXCELLENT INVESTMENT UNITED STATES LLC 32486 FAYARD ENTERPRISES UNITED STATES f11102 FedEx Express Corporate UNITED STATES Aviation 13457 Flying Partners CVBA BELGIUM 29427 Flying Service N.V. BELGIUM 24578 GAFI GENERAL AVIAT MAURITIUS f12983 GREEN DIESEL LLC UNITED STATES 29980 HAINAN AIRLINES (2) CHINA 23700 HEWA BORA AIRWAYS CONGO 28582 INTER WETAIL AG SWITZERLAND 9542 INTL PAPER CY UNITED STATES 27709 KALITTA AIR UNITED STATES 28087 LAS VEGAS CHARTER UNITED STATES 32303 MASTER TOP LINHAS BRAZIL 37066 MERIDIAN (AIRWAYS) BELGIUM 1084 MIL BELGIUM BELGIUM 31207 N604FJ LLC UNITED STATES f11462 N907WS AVIATION LLC UNITED STATES 26688 NEWELL RUBBERMAID UNITED STATES f10341 OfficeMax Inc UNITED STATES 31660 RIPPLEWOOD AVTN UNITED STATES 2344 SAUDIA SAUDI ARABIA 29222 SILVERBACK CARGO RWANDA 39079 SOLARIUS AVIATION UNITED STATES 35334 SONOCO PRODUCTS CO UNITED STATES BELGIUM 26784 SOUTHERN AIR UNITED STATES 38995 STANLEY BLACK&DECKER UNITED STATES 27769 Sea Air BELGIUM 34920 TRIDENT AVIATION SVC UNITED STATES 30011 TUI AIRLINES - JAF BELGIUM 27911 ULTIMATE ACFT SERVIC UNITED STATES 13603 VF CORP UNITED STATES 36269 VF INTERNATIONAL SWITZERLAND 37064 VIPER CLASSICS LTD UNITED KINGDOM f11467 WILSON & ASSOCIATES OF UNITED STATES DELAWARE LLC 37549 YILTAS GROUP TURKEY BULGARIA CRCO Identification no.