Investments in Other Corporations

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Score Media Inc. Eresearch Stockpotentials

StockPotentials November 26, 2010 . SCORE MEDIA INC. Price (November 26) $1.03 52-Week Range $1.10-$0.35 Shares O/S 81.23 million Market Cap $83.67 million 50-day Average Volume 16,600 200-day Average Volume 25,100 Fiscal Year-End August 31 Symbol TSX: SCR Website www.scoremedia.com Financial Data Source: www.bigcharts.com PROFILE Score Media Inc. (“Score Media” or the “Company”) is a Canadian media company that provides “interactive and authentic sports entertainment”. The Company has established itself as the home for hardcore sports fans. Score Media’s primary asset, the Score Television Network (“theScore”), is a national specialty television service providing sports news, information, highlights, and live- event programming in more than 6.8 million homes across Canada. Score Media is headquartered in Toronto, has approximately 220 employees, and is publicly traded on the Toronto Stock Exchange (TSX). The Company was created in 1997 in response to the growing desire for increased participation in the consumption of sports. CORPORATE STRATEGY Score Media is devoted to: (1) sports reporting with a light-hearted feel; and (2) getting fans more involved with the consumption of sports. On-air personalities are chosen more for their wit and sense eResearch Corporation 56 Temperance Street, Suite 501 of humor, rather than pure sports knowledge. Score Media is also a Toronto, ON M5H 3V5 leader in mobile sports technology, and has holdings in web- Telephone: 416-643-7650 content development companies. Toll Free: 877-856-0765 eResearch Analysts: The Company continues to: (a) develop new ways to improve Mark Edwards, B.Comm. -

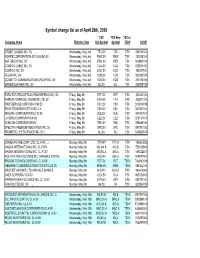

Toronto Stock Exchange and TSX Venture Exchange Symbol Change List

Symbol change list as of April 26th, 2006 TSX TSX New TSX or Company Name Effective Date Old Symbol Symbol TSXV CUSIP TRIZEC CANADA INC. SV Wednesday, May 3rd TZC.SV TZC TSX 896874104 POWER CORPORATION OF CANADA SV Wednesday, May 3rd POW.SV POW TSX 739239101 ADF GROUP INC. SV Wednesday, May 3rd DRX.SV DRX TSX 00089N103 COGECO CABLE INC. SV Wednesday, May 3rd CCA.SV CCA TSX 19238V105 COGECO INC. SV Wednesday, May 3rd CGO.SV CGO TSX 19238T100 VELAN INC. SV Wednesday, May 3rd VLN.SV VLN TSX 922932108 COSSETTE COMMUNICATION GROUP INC. SV Wednesday, May 3rd KOS.SV KOS TSX 221478100 DANIER LEATHER INC. SV Wednesday, May 3rd DL.SV DL TSX 235909108 EXFO ELECTRO-OPTICAL ENGINEERING INC. SV Friday, May 5th EXF.SV EXF TSX 302043104 FAIRFAX FINANCIAL HOLDINGS LTD. SV Friday, May 5th FFH.SV FFH TSX 303901102 FIRSTSERVICE CORPORATION SV Friday, May 5th FSV.SV FSV TSX 33761N109 FOUR SEASONS HOTELS INC. LV Friday, May 5th FSH.SV FSH TSX 35100E104 INSCAPE CORPORATION CL 'B' SV Friday, May 5th INQ.SV INQ TSX 45769T102 LA SENZA CORPORATION SV Friday, May 5th LSZ.SV LSZ TSX 50511P101 TEKNION CORPORATION SV Friday, May 5th TKN.SV TKN TSX 878949106 SPECTRA PREMIUM INDUSTRIES INC. SV Friday, May 5th SPD.SV SPD TSX 847931102 PROMETIC LIFE SCIENCES INC. SV J Friday, May 5th PLI.SV PLI TSX 74342Q104 CANADIAN TIRE CORP. LTD. CL A NV Monday, May 8th CTR.NV CTC.A TSX 136681202 MAGNA INTERNATIONAL INC. CL B MV Monday, May 8th MG.MV.B MG.B TSX 559222500 MAGNA INTERNATIONAL INC. -

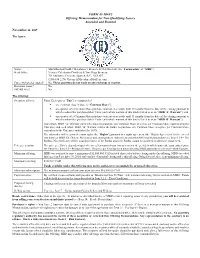

FORM 45-106F2 Offering Memorandum for Non-Qualifying Issuers Amended and Restated

FORM 45-106F2 Offering Memorandum for Non-Qualifying Issuers Amended and Restated November 24, 2017 The Issuer: Name: MacMhaol-onfhaidh (‘Macaloney’) Brewers & Distillers Ltd. (the “Corporation” or “MBD”) Head Office: Victoria Caledonian Distillery & Twa Dogs Brewery, 761 Enterprise Crescent, Saanich, B.C., V8Z 6P7 (250) 634 2276; [email protected] Currently listed or quoted? No. These securities do not trade on any exchange or market. Reporting issuer? No. SEDAR filer? No. The Offering: Securities offered: Units. Each unit (a “Unit”) is composed of: . one common class A share (a “Common Share”); . one quarter of a Common Share purchase warrant exercisable until 19 months from the date of the closing pursuant to which a subscriber purchased their Units (each whole warrant of this kind referred to as an “MBD ‘A’ Warrant”); and . one quarter of a Common Share purchase warrant exercisable until 31 months from the date of the closing pursuant to which a subscriber purchased their Units (each whole warrant of this kind referred to as an “MBD ‘B’ Warrant”). Each whole MBD “A” Warrant entitles the holder to purchase one Common Share at a price per Common Share equivalent to the Unit price and each whole MBD “B” Warrant entitles the holder to purchase one Common Share at a price per Common Share equivalent to the Unit price multiplied by 110%. The subscriber will be granted certain rights (the “Rights”) pursuant to a rights agreement (the “Rights Agreement”) to be entered into between MBD, Dr. Graeme Macaloney and, among others, subscribers under this Offering Memorandum (see Item 5.1.4 – The Rights). -

Rogers Communications Inc. 2013 Annual Report Media

ROGERS COMMUNICATIONS INC. 2013 ANNUAL REPORT WIRELESS CABLE MEDIA ROGERS.COM AT A GLANCE OUR BUSINESS Rogers Communications Inc.. is a diversified Canadian telecommunications and mem dia compana y. Rogers Wireeless is CaC nadaa’ss laargeg st wireless voice and data telecommunications seervicese provider and tht e counntry’s onlyy natioi nal carrier operating on the combined world standard GSMM/HSPS A+A /LLTE techc nooloogy platforms. RRogers Cable is a leading Canadian cable services provider, offeringg high-speeed InI ternnett access, cablel television, and telephony products, and together with Rogers Business Solutions, providdese businness tet lecom, networking, hosting, managed services and IP solutions to small, medium and lal rgr e ennterrprise, government and carrier customers. Rogers Media is Canada’s premier group off categorry-lel ading broadcast, specialty, print and online media assets, with businesses in radio and televisionn broadcasting, televised shopping, sports entertainment, magazine and trade journal publishingg ana d digital media. We are publicly traded on both the TSX and NYSE stock exchanges and are included ini thee S&P& /TSX 60 Index of the largest publicly traded companies in Canada. DELIVERING ON OUR COMMITMENTS IN 2013 FREE CASH FLOW DIVIDEND OPERATING FAST AND RELIABLE GENERATION GROWTH EFFICIENCIES NETWORKS WHAT WE SAID: Deliver another WHAT WE SAID: Increase WHAT WE SAID: Implement WHAT WE SAID: Maintain year of significant consolidated cash returns to shareholders productivity improvement Rogers leadership in network pre-tax free cash flow. consistently over time. initiatives to capture sustainable technology and innovation. operating efficiencies. WHAT WE DID: Generated WHAT WE DID: Increased the WHAT WE DID: Rogers was $2.0 billion of pre-tax free cash annualized dividend per share WHAT WE DID: Reduced operating named both the fastest wireless flow in 2013, supporting the 10% from $1.58 to $1.74 in 2013. -

CSA Notice 44-302 - Replacement of National Instrument 44-101 Short Form Prospectus Distributions

Notices / News Releases 1.1.2 CSA Notice 44-302 - Replacement of National Instrument 44-101 Short Form Prospectus Distributions CSA NOTICE 44-302 - REPLACEMENT OF NATIONAL INSTRUMENT 44-101 SHORT FORM PROSPECTUS DISTRIBUTIONS December 16, 2005 Introduction On October 21, 2005, the Canadian Securities Administrators (CSA), published a notice relating to the replacement of National Instrument 44-101 Short Form Prospectus Distributions (Former NI 44-101) which came into effect in December 2000 with National Instrument 44- 101 Short Form Prospectus Distributions (New NI 44-101). New NI 44-101 will come into force on December 30, 2005. Substance and Purpose New NI 44-101 modifies the qualification, disclosure and other requirements of the short form prospectus system so that this prospectus system can build on and be more consistent with recent developments and initiatives of the CSA. Transition Section 2.8(1) of New NI 44-101 requires issuers to file a one-time notice of intention to be qualified to file a short form prospectus (a qualification notice) at least 10 business days prior to filing its first preliminary short form prospectus under New NI 44-101. Section 2.8(4) grandfathers issuers which have a current AIF as defined in Former NI 44-101 as at December 29, 2005 by deeming such issuers to have filed a qualification notice on December 14, 2005 (which is 10 business days prior to implementation of New NI 44- 101). Therefore, grandfathered issuers which otherwise satisfy the New NI 44-101 qualification criteria may file a preliminary short form prospectus under New NI 44-101 on or after December 30, 2005. -

OSC Bulletin

The Ontario Securities Commission OSC Bulletin February 9, 2007 Volume 30, Issue 6 (2007), 30 OSCB The Ontario Securities Commission Administers the Securities Act of Ontario (R.S.O. 1990, c. S.5) and the Commodity Futures Act of Ontario (R.S.O. 1990, c. C.20) The Ontario Securities Commission Published under the authority of the Commission by: Cadillac Fairview Tower Carswell Suite 1903, Box 55 One Corporate Plaza 20 Queen Street West 2075 Kennedy Road Toronto, Ontario Toronto, Ontario M5H 3S8 M1T 3V4 416-593-8314 or Toll Free 1-877-785-1555 416-609-3800 or 1-800-387-5164 Contact Centre - Inquiries, Complaints: Fax: 416-593-8122 Capital Markets Branch: Fax: 416-593-3651 - Registration: Fax: 416-593-8283 Corporate Finance Branch: - Team 1: Fax: 416-593-8244 - Team 2: Fax: 416-593-3683 - Team 3: Fax: 416-593-8252 - Insider Reporting Fax: 416-593-3666 - Take-Over Bids: Fax: 416-593-8177 Enforcement Branch: Fax: 416-593-8321 Executive Offices: Fax: 416-593-8241 General Counsel’s Office: Fax: 416-593-3681 Office of the Secretary: Fax: 416-593-2318 The OSC Bulletin is published weekly by Carswell, under the authority of the Ontario Securities Commission. Subscriptions are available from Carswell at the price of $549 per year. Subscription prices include first class postage to Canadian addresses. Outside Canada, these airmail postage charges apply on a current subscription: U.S. $175 Outside North America $400 Single issues of the printed Bulletin are available at $20 per copy as long as supplies are available. Carswell also offers every issue of the Bulletin, from 1994 onwards, fully searchable on SecuritiesSource™, Canada’s pre-eminent web-based securities resource. -

Broadcasting Public Notice CRTC 2008-100

Broadcasting Public Notice CRTC 2008-100 Ottawa, 30 October 2008 Regulatory policy Regulatory frameworks for broadcasting distribution undertakings and discretionary programming services Table of contents Paragraph Summary Introduction 1 Background 5 The Canadian broadcasting system 11 Need for a new regulatory framework 27 Calibrating the role of broadcasting distribution undertakings and the 30 programming sector Key elements of the Call for comments 34 Regulatory framework for broadcasting distribution undertakings 35 Basic service – Terrestrial broadcasting distribution undertakings 36 Basic service – Direct-to-home undertakings 46 Access rules for Canadian programming services 60 Access rules for high definition pay and specialty services 74 Access rules for minority-language services 80 Access rules for unrelated Category B, exempt and pay audio services 87 Preponderance of Canadian programming services 95 Packaging requirements 103 Third-language services distributed by broadcasting distribution 129 undertakings New forms of advertising available to broadcasting distribution 139 undertakings Advertising in local availabilities of non-Canadian services 144 Issues relating to dispute resolution 154 Signal sourcing and transport 169 Licence classes and exemptions for broadcasting distribution 187 undertakings Other issues relating to broadcasting distribution undertakings 202 Regulatory framework for pay and specialty programming undertakings 235 Authorization of non-Canadian services 239 Genre exclusivity – Canadian services 250 -

Toronto Maple Leafs 2009-10 Schedule

TORONTO MARLIES 2009-10 2009-10 FEEL THE SPIRIT 2008-09 TORONTO MARLIES MEDIA GUIDE TORONTO MAPLE LEAFS Toronto Maple Leafs 2009-10 Schedule SUN MON TUE WED THU FRI SAT MTL WSH OCT 127:00 CBC 3 7:00 CBC OTT PIT 456789107:00 TSN 7:00 CBC NYR COL NYR 11 127:00 RSN 137:30 LTV 14 15 16 17 7:00 CBC VAN 18 19 20 21 22 23 24 7:00 CBC ANA DAL BUF MTL 25 2610:00 LTV27 28 8:00 TSN29 30 7:30 RSN 31 7:00 CBC NOV TBL CAR DET 123457:30 RSN 6 7:00 LTV 7 7:00 CBC MIN CHI CGY 8 9 107:00 RSN 11 12 13 8:30 RSN 14 7:00 CBC OTT CAR WSH 0]SfTS^]½cVXeTX]7TaT½bc^cWTPcW[TcTbfW^Z]^fXcP]SP 15 16 177:30 RSN18 19 7:00 TSN 20 21 7:00 CBC NYI TBL FLA 22 237:00 RSN 24 257:00 TSN26 27 7:30 LTV 28 BUF 8]cWXbR^d]cahcWTaT½bPf^aSU^aVTccX]VcWX]VbS^]T8c\TP] 29 307:00 RSN MTL CBJ BOS DEC 17:30 TSN2 3 7:00 LTV4 5 7:00 CBC <^[b^]2P]PSXP]Xb_a^dSc^QTcWT^UÄRXP[QTTabd__[XTa^UcWT ATL NYI BOS WSH 67897:00 RSN 7:00 TSN 107:00 LTV 11 12 7:00 CBC OTT PHX BUF BOS 13 147:00 RSN 15 16 7:30 TSN 17 18 7:30 TSN 19 7:00 CBC BUF NYI MTL 20 217:00 RSN 22 237:00 LTV 24 25 26 7:00 CBC PIT EDM 277:00 LTV28 29 30 9:30 RSN 31 CGY JAN 1 2 7:00 CBC FLA PHI BUF PIT 3457:00 RSN 67:00 TSN7 8 7:30 RSN 9 7:00 CBC CAR PHI WSH 10 11 127:00 RSN 13 14 7:00 TSN 15 7:00 TSN 16 NSH ATL TBL FLA 17 188:00 RSN 19 7:00 LTV20 21 7:00 TSN22 23 7:00 CBC LAK NJD VAN 24 25 267:00 RSN 27 28 29 7:00 TSN 30 7:00 CBC 31 NJD NJD OTT FEB 12347:00 RSN 5 7:00 RSN 6 7:00 CBC SJS STL 7 87:00 RSN 9101112 8:00 LTV 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 [[2P]PSXP]bfW^bW^fXc CAR BOS OTT MAR 1237:00 RSN 47:00 TSN5 6 7:00 CBC ! -

2014 Annual Report Rogers Communications Inc. Wireless Cable Media

one ROGERS COMMUNICATIONS INC. 2014 ANNUAL REPORT WIRELESS CABLE MEDIA ROGERS COMMUNICATIONS INC. Rogers Communications (TSX: RCI; NYSE: RCI) is a diversified Canadian telecommunications and media company. As discussed on the following pages, Rogers Communications is engaged in the telecom and media businesses through its primary reporting segments Wireless, Cable, Business Solutions and Media. ROGERS COMMUNICATIONS WIRELESS CABLE BUSINESS SOLUTIONS MEDIA WIRELESS SEGMENT The Wireless segment provides wireless voice and data communications services across Canada to approximately 9.5 million customers under the Rogers, Fido and chatr brands. Wireless is Canada’s largest wireless provider and the only national carrier operating on the combined global standard GSM/HSPA+/LTE technology platforms. Wireless is also Canada’s leader in innovative wireless services, and provides customers with the best and latest wireless devices and applications and the fastest network speeds. Wireless provides seamless wireless roaming across the U.S. and more than 200 other countries, and is the Canadian leader in the deployment of mobile commerce and machine-to-machine communications. CABLE AND BUSINESS SOLUTIONS SEGMENTS Cable is a leading Canadian cable services provider, whose service territory covers approximately 4.0 million homes in Ontario, New Brunswick and Newfoundland representing approximately 30% of the total Canadian cable market. Our advanced digital hybrid fibre-coax network provides market leading high-speed broadband Internet access speeds, the most innovative selection of digital television and online viewing and telephony services to millions of residential and small business customers. Together with the Business Solutions segment, it also provides scalable carrier-grade business telecom, networking, hosting and managed data services, and IP connectivity and solutions to medium and large enterprise, government and carrier customers. -

OSC Bulletin

The Ontario Securities Commission OSC Bulletin August 20, 2020 Volume 43, Issue 34 (2020), 43 OSCB The Ontario Securities Commission administers the Securities Act of Ontario (R.S.O. 1990, c. S.5) and the Commodity Futures Act of Ontario (R.S.O. 1990, c. C.20) The Ontario Securities Commission Published under the authority of the Commission by: Cadillac Fairview Tower Thomson Reuters 22nd Floor, Box 55 One Corporate Plaza 20 Queen Street West 2075 Kennedy Road Toronto, Ontario Toronto, Ontario M5H 3S8 M1T 3V4 416-593-8314 or Toll Free 1-877-785-1555 416-609-3800 or 1-800-387-5164 Contact Centre – Inquiries, Complaints: Fax: 416-593-8122 TTY: 1-866-827-1295 Office of the Secretary: Fax: 416-593-2318 42711450 The OSC Bulletin is published weekly by Thomson Reuters Canada, under the authority of the Ontario Securities Commission. Thomson Reuters Canada offers every issue of the Bulletin, from 1994 onwards, fully searchable on SecuritiesSource™, Canada’s pre-eminent web-based securities resource. SecuritiesSource™ also features comprehensive securities legislation, expert analysis, precedents and a weekly Newsletter. For more information on SecuritiesSource™, as well as ordering information, please go to: http://www.westlawecarswell.com/SecuritiesSource/News/default.htm or call Thomson Reuters Canada Customer Support at 1-416-609-3800 (Toronto & International) or 1-800-387-5164 (Toll Free Canada & U.S.). Claims from bona fide subscribers for missing issues will be honoured by Thomson Reuters Canada up to one month from publication date. Space is available in the Ontario Securities Commission Bulletin for advertisements. The publisher will accept advertising aimed at the securities industry or financial community in Canada. -

Rogers Communications Inc. Investor Relations 2012 Annual Report

Creating World-Leading Internet Experiences ROGERS COMMUNICATIONS INC. 2012 ANNUAL REPORT WIRELESS CABLE MEDIA A A W W E E SE SE CO LI CO LI WA WA FE AT A GLANCE FE ST ST N N AMIN AMIN NETWORK SHARE NL NETWORK SHARE NL C C NN NN I I ST SURF ST SURF TC TC ONN ONN EC EC YL DOWNLOAD YL DOWNLOAD RELIABLE CURE RELIABLE CURE OUR BUSINESS C C T T OA OA E E INSP INSP H H AC AC ACCESS AM ACCESS AM UP UP RogersSTRE CommunicationsAMIN Inc. is a diversifiedG Canadian communicationsCO and media company engaged STREAMING CO M M in the telecom and media businesses. Rogers Wireless is Canada’s largest wirelessLI voice and data LI LO communications services provider and the country’s only national carrier operating on the combined LO RE RE G G RF RF FE FE D D SS SS + NN NN INSPIRworld standard GSM/HSPA /LTE technologyE platforms. RogersKING Cable is a leading Canadian cable services INSPIRE KING AD provider, offering cable television, high-speed Internet access, and telephony products, and together with AD ST ST TA TA SU SU AC RELI AC RELI XT XT Rogers Business Solutions, provides business telecom, data networking andST IP solutions to small, ST FREEDO FREEDO SU SU EC EC medium and large enterprise, government and carrier customers. RogersCE Media is Canada’s premier CE TH TH SE SE RELIABLEST RELIABLEST group of category-leading broadcast, specialty, print and online media assets, with businesses in radio CE SECURE CE SECURE UPLOAD YL UPLOAD YL AB AB CONNand televisionEC Tbroadcasting, televised shopping, sports entertainment,EA magazine and trade journal CONNECT EA T T RF RF ACRE CEINSPIR SS ACRE CEINSPIR SS publishing and digital media. -

ANNUAL REPORT 2020–2021 Tokens

EVERY VOICE IS A SPARK. ANNUAL REPORT 2020–2021 Tokens OUR WORLD IS CHANGING. LET’S MAKE IT BETTER. LET’S HELP OUR INDUSTRY COME ROARING BACK. WE’RE BRINGING UP NEW VOICES. WE’RE LISTENING TO THOSE THAT NEED TO Wildhood BE HEARD. WE’RE SEEING THAT CANADIAN CONTENT REPRESENTS WE’RE HERE EACH AND TO MAKE OUR EVERY ONE INDUSTRY OF US. BOLD, INCLUSIVE, About Sex INNOVATIVE. Au pays des Mitchifs WE SUPPORT STORYTELLERS AND CREATORS WITH A UNIQUE STORY TO TELL. WE’RE HERE TO SPARK COURAGEOUS STORIES TO HELP GIVE THEM MORE Red Earth Uncovered THAN A STAGE. Blood Quantum WE SUPPORT STORYTELLERS WHO ARE TALENTED AND DETERMINED. THEIR WORK REACHES AUDIENCES AROUND THE WORLD AND SPARKS PASSION FOR CANADA’S No Visible Trauma STORIES. 17 TABLE OF REPORT ANNUAL 2020–2021 CONTENTS 3 OUR RESPONSE TO THE COVID-19 PANDEMIC Introduction 106 4 FUNDING RESULTS Experimental 118 Export-Related Programs 166 TV 130 International Treaty 170 Coproductions Indigenous Content 148 Support Program Funding 174 1 ABOUT CMF Summary Official Language 154 Financial Contributors 20 Board Members 56 Minority Community Sector Development 178 Mandate and Vision 22 2021 Appointees 60 Support Support to the CMF Board Funding Model 24 Regional Support 160 Program Administration 182 of Directors CMF by the Numbers 26 Management Team 62 Message from the Chair 28 Industry Consultations 66 Message from 30 the President and CEO Strategic Actions 68 5 FINANCIAL OVERVIEW and Research Meet Seven 34 Management Discussion 190 Financial Statements 196 Accomplished Creators Industry Partnerships