Rogers Communications Inc. 2013 Annual Report Media

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

2011 BCE Annual Information Form

Annual Information Form BCE Inc. For the year ended December 31, 2011 March 8, 2012 In this Annual Information Form, Bell Canada is, unless otherwise indicated, referred to as Bell, and comprises our Bell Wireline, Bell Wireless and Bell Media segments. Bell Aliant means, collectively, Bell Aliant Inc. and its subsidiaries. All dollar figures are in Canadian dollars, unless stated otherwise. The information in this Annual Information Form is as of March 8, 2012, unless stated otherwise, and except for information in documents incorporated by reference that have a different date. TABLE OF CONTENTS PARTS OF MANAGEMENT’S DISCUSSION & ANALYSIS AND FINANCIAL STATEMENTS ANNUAL INCORPORATED BY REFERENCE INFORMATION (REFERENCE TO PAGES OF THE BCE INC. FORM 2011 ANNUAL REPORT) Caution Regarding Forward-Looking Statements 2 32-34; 54-69 Corporate Structure 4 Incorporation and Registered Offices 4 Subsidiaries 4 Description of Our Business 5 General Summary 5 23-28; 32-36; 41-47 Strategic Imperatives 6 29-31 Our Competitive Strengths 6 Marketing and Distribution Channels 8 Our Networks 9 32-34; 54-69 Our Employees 12 Corporate Responsibility 13 Competitive Environment 15 54-57 Regulatory Environment 15 58-61 Intangible Properties 15 General Development of Our Business 17 Three-Year History (1) 17 Our Capital Structure 20 BCE Inc. Securities 20 112-114 Bell Canada Debt Securities 21 Ratings for BCE Inc. and Bell Canada Securities 21 Ratings for Bell Canada Debt Securities 22 Ratings for BCE Inc. Preferred Shares 22 Outlook 22 General Explanation 22 Explanation of Rating Categories Received for our Securities 24 Market for our Securities 24 Trading of our Securities 25 Our Dividend Policy 27 Our Directors and Executive Officers 28 Directors 28 Executive Officers 30 Directors’ and Executive Officers’ Share Ownership 30 Legal Proceedings 31 Lawsuits Instituted by BCE Inc. -

ROGERS COMMUNICATIONS INC. ANNUAL INFORMATION FORM (For

ROGERS COMMUNICATIONS INC. ANNUAL INFORMATION FORM (for the fiscal year ended December 31, 2007) March 4, 2008 ROGERS COMMUNICATIONS INC. ANNUAL INFORMATION FORM INDEX The following is an index of the Annual Information Form of Rogers Communications Inc. (“RCI”) referencing the requirements of Form 51-102F2 of the Canadian Securities Administrators. Certain parts of this Annual Information Form are contained in RCI’s Management’s Discussion and Analysis for the fiscal year ended December 31, 2007, and RCI’s 2007 Annual Audited Consolidated Financial Statements, each of which is filed on SEDAR at www.sedar.com and incorporated herein by reference as noted below. Page reference / incorporated by reference from Annual Information 2007 Form MD&A Item 1 — Cover Page p. 1 Item 2 — Index p. 2 Item 3 — Corporate Structure 3.1 — Name and Incorporation p. 3 3.2 — Intercorporate Relationships pgs. 3-5 Item 4 — General Development of the Business 4.1 — Three Year History pgs. 6-10 4.2 — Significant Acquisitions p. 10 Item 5 — Narrative Description of the Business 5.1 — General — Business Overview p. 11 p. 2 — Rogers Wireless pgs. 10-12 — Rogers Cable pgs. 16-19 — Rogers Media pgs. 25-26 — Employees p. 9 — Properties, Trademarks, Environmental and Other Matters pgs. 10-11 5.2 — Risk Factors p. 11 Item 6 — Dividends 6.1 — Dividends p. 12 Item 7 — Description of Capital Structure 7.1 — General Description of Capital Structure p. 12 7.2 — Constraints pgs. 12-13 7.3 — Ratings pgs. 13-14 Item 8 — Market for Securities 8.1 — Trading Price and Volume p. -

Score Media Inc. Eresearch Stockpotentials

StockPotentials November 26, 2010 . SCORE MEDIA INC. Price (November 26) $1.03 52-Week Range $1.10-$0.35 Shares O/S 81.23 million Market Cap $83.67 million 50-day Average Volume 16,600 200-day Average Volume 25,100 Fiscal Year-End August 31 Symbol TSX: SCR Website www.scoremedia.com Financial Data Source: www.bigcharts.com PROFILE Score Media Inc. (“Score Media” or the “Company”) is a Canadian media company that provides “interactive and authentic sports entertainment”. The Company has established itself as the home for hardcore sports fans. Score Media’s primary asset, the Score Television Network (“theScore”), is a national specialty television service providing sports news, information, highlights, and live- event programming in more than 6.8 million homes across Canada. Score Media is headquartered in Toronto, has approximately 220 employees, and is publicly traded on the Toronto Stock Exchange (TSX). The Company was created in 1997 in response to the growing desire for increased participation in the consumption of sports. CORPORATE STRATEGY Score Media is devoted to: (1) sports reporting with a light-hearted feel; and (2) getting fans more involved with the consumption of sports. On-air personalities are chosen more for their wit and sense eResearch Corporation 56 Temperance Street, Suite 501 of humor, rather than pure sports knowledge. Score Media is also a Toronto, ON M5H 3V5 leader in mobile sports technology, and has holdings in web- Telephone: 416-643-7650 content development companies. Toll Free: 877-856-0765 eResearch Analysts: The Company continues to: (a) develop new ways to improve Mark Edwards, B.Comm. -

Wireless Competition in Canada: an Assessment

Volume 6•Issue 27•September 2013 WIRELESS COMPETITION IN CANADA: AN ASSESSMENT Jeffrey Church † Professor, Department of Economics and Director, Digital Economy Program, The School of Public Policy, University of Calgary Andrew Wilkins † Research Associate, Digital Economy Program, The School of Public Policy, University of Calgary SUMMARY If there’s one thing Canadians agree on, it’s that Canada’s wireless industry can and should be more competitive. The federal government is on side with the policy objective of having four carriers in every region and has responded with policies that provide commercial advantages to entrants. But, the rub is that there has not been a study that actually assesses the state of competition in wireless services in Canada, until now. Those in favour of policies that will promote and sustain entry point to Canada’s high average revenue per user and low wireless penetration rate (mobile connections per capita) as evidence that there is insufficient competition. The difficulty is that the facts are not consistent with this simplistic analysis. Measurements of wireless penetration are skewed toward countries that maintain the Calling Party Pays Protocol and favour pay-as-you-go plans, both of which encourage inflated user counts. Canada’s participation per capita on monthly plans and minutes of voice per capita are not outliers. Moreover, in terms of smartphone adoption and smartphone data usage, Canada is a global leader, contributing to high average revenue per user. Consistent with being world leaders in the rollout of high speed wireless networks, Canada lead its peer group in capital expenditures per subscriber in 2012: the competition of importance to Canadians is not just over price, but also over the quality of wireless networks. -

Igniting Growth at a Glance Highlights for 2015

Rogers Communications Inc. 2015 Annual Report Igniting growth At a glance highlights for 2015 Rogers Communications Inc. Wireless Rogers Communications (TSX: RCI; NYSE: RCI) Wireless is Canada’s largest provider of voice and data is a diversified Canadian communications and communications services. We provide these services to media company. We report our results of approximately 9.9 million customers under the Rogers, Fido, chatr and Mobilicity brands. We provide customers operations in the four segments of Wireless, with the best and latest wireless devices, applications and Cable, Business Solutions and Media. leading network speeds. Our far-reaching LTE network covers approximately 93% of all Canadians. Our strategic spectrum investments position us well to provide the network connectivity, speed and reliability our customers Operating revenue Adjusted operating profit have come to enjoy and expect. Wireless also provides (In billions of dollars) (In billions of dollars) seamless wireless roaming across the U.S. and more than 200 other countries and is the Canadian leader in the 2015 13.4 2015 5.0 deployment of machine-to-machine communications and Internet of Things applications. 2014 12.9 2014 5.0 2013 12.7 2013 5.0 Free cash flow Annualized dividend Operating revenue Adjusted operating profit (In billions of dollars) rate at year end ($) (In billions of dollars) (In billions of dollars) 2015 1.7 2015 $1.92 2015 7.7 2015 3.2 2014 1.4 2014 $1.83 2014 7.3 2014 3.2 2013 1.5 2013 $1.74 2013 7.3 2013 3.2 2015 Operating revenue 2015 Operating revenue $13.4 Billion $7.7 Billion Wireless 56% $13.4 Cable 26% $7.7 Network 90% Billion Billion Media 15% Business Solutions 3% Equipment 10% Cable and Business Solutions Media Cable is a leading Canadian cable services provider whose Media is Canada’s premier destination for category-leading service territory covers approximately 4.2 million homes sports entertainment, digital media, television and radio in Ontario, New Brunswick and Newfoundland representing broadcasting and publishing properties. -

Rogers Communications Reports Fourth Quarter

ROGERS COMMUNICATIONS REPORTS FOURTH QUARTER 2015 RESULTS • Rogers 3.0 plan delivers solid financial and operating metrics for the fourth quarter • Continued revenue growth of 3% driven by growth of 4% in Wireless, our largest segment representing approximately 60% of total revenue and adjusted operating profit • Wireless adjusted operating profit growth of 4%; Wireless postpaid net additions of 31,000, an improvement of 89,000 year on year, on an 11 basis point improvement in churn • Postpaid ARPA up 4% with strong growth in Share Everything customers, up 63% • Internet net additions of 16,000, an improvement of 20,000 year on year; Internet revenue up 10% • Strong operating fundamentals delivered operating cash flow and free cash flow of $950 million and $274 million, respectively • Customer complaints as reported by the Commissioner for Complaints for Telecommunications Services (CCTS) declined faster than key competitors’, down 26% in 2015 and down 50% over the past two years • Met 2015 guidance and announced our 2016 outlook, with continued growth in operating revenue and adjusted operating profit as well as a declining capital expenditure profile expected to drive higher free cash flow TORONTO (January 27, 2016) - Rogers Communications Inc., a leading diversified Canadian communications and media company, today announced its unaudited financial and operating results for the fourth quarter ended December 31, 2015. Consolidated Financial Highlights Three months ended December 31 Twelve months ended December 31 (In millions of Canadian -

Rogers Wireless Inc

333 Bloor Street East Toronto, Ontario M4W 1G9 Tel. (416) 935-7211 Fax (416) 935-7719 [email protected] Dawn Hunt Vice-President Government & Intercarrier Relations March 14, 2003 Jan Skora Director General Radiocommunications and Broadcasting Regulatory Branch EMAILED TO: [email protected] Industry Canada 300 Slater Street Ottawa, Ontario K1A 0C8 Dear Mr. Skora, Re: Comments - Canada Gazette Notices: DGRB-004-02 and DGRB-001-03 Consultation on a New Fee and Licensing Regime for Cellular and Incumbent Personal Communications Services (PCS) Licensees Pursuant to the Canada Gazette, Part I, dated December 21, 2002, and February 21, 2003 respectively, RWI is pleased to file the attached comments regarding the above noted proceeding. The comments are submitted in Adobe Acrobat (PDF) version 5.0 software produced on a computer using a Windows 2000 Professional operating system. If there are any questions regarding these comments, please do not hesitate to contact the undersigned. Sincerely, Original Signed by: Joel Thorp On Behalf of: Dawn Hunt, DH:jt Attach. Department of Industry CONSULTATION ON A NEW FEE AND LICENSING REGIME FOR CELLULAR AND INCUMBENT PERSONAL COMMUNICATIONS SERVICES (PCS) LICENSEES DGRB-004-02 COMMENTS OF ROGERS WIRELESS INC. March 14, 2003 COMMENTS OF ROGERS WIRELESS INC. DGRB-004-02 Table of Contents 1EXECUTIVE SUMMARY ................................................................................................3 DETAILED COMMENTS...................................................................................................4 -

Long-Time Cable Shows Come to End of the Line

Coming in 2 weeks... the best Suds and Sauce in Aurora ALL YOU CAN EAT The Totten Beverley Varcoe 905-727-3154 Wealth Advisory DINNER BUFFET Highly Qualified to Handle Your Group Real Estate Needs with Over 20 $11.95 years of Award Winning service! DavidB. Totten Only Senior Vice President, Wealth Advisor Nightly from 5 pm - 9 pm 17310 Yonge Street, Suite 11 *Per Person, plus taxes. Newmarket, Ontario 905.830.4468 Howard Johnson Hotel Aurora www.davidtotten.ca 15520 Yonge Street Your Community Realty, Aurora If you are already a client of BMO Nesbitt Burns, please contact your Investment Advisor for more information. Reservations - 905-727-1312 BROKER, CRES, SRES Please visit us at www.beverleyvarcoe.com www.hojoaurora.com Market Value Appraiser Aurora’s Independent Community Newspaper Vol. 8 No. 42 905-727-3300 auroran.com FREE Week of August 26, 2008 Briefly Permanent markers Probably one of the nicest evening attractions in Aurora is about to get better. For the last several years, Aurora Legion members have placed candles on headstones of people buried in the Aurora Cemetery, who served in the armed forces. It’s a spectacular sight and this year, it will happen Saturday, Sept. 20, followed by a graveside service the next day. However, in addition to the candlelight ceremony, the Legion’s Ladies Auxiliary, headed up by Jean Anderson, will place permanent three-inch markers on the foundation or the side of all affected memorial stones. Some 350 markers have been ordered and are expected to be in place for this year’s ceremony. -

Moneygram | Canada Post

Pay for utilities, phone services, cable bills and more at your local post office with MoneyGram! Please consult the list below for all available billers. Payez vos factures de services publics, de services téléphoniques, de câblodistribution et autres factures à votre bureau de poste local avec MoneyGram! Consultez la liste ci-dessous pour tous les émetteurs de factures participants. A B C D E F G H I J K L M N O P Q R S T U V W X Y Z BILLER NAME/ PROVINCE AVAILABLE SERVICE/ NOM DE L’ÉMETTEUR DE FACTURE SERVICE DISPONIBLE 310-LOAN BC NEXT DAY/JOUR SUIVANT 407 ETR ON NEXT DAY/JOUR SUIVANT A.R.C. ACCOUNTS RECOVERY CORPORATION BC NEXT DAY/JOUR SUIVANT AAA DEBT MANAGERS BC NEXT DAY/JOUR SUIVANT ABERDEEN UTILITY SK NEXT DAY/JOUR SUIVANT ABERNETHY UTILITY SK NEXT DAY/JOUR SUIVANT ACCORD BUSINESS CREDIT ON NEXT DAY/JOUR SUIVANT ACTION COLLECTIONS & RECEIVABLES MANAGEMENT ON NEXT DAY/JOUR SUIVANT AFFINITY CREDIT SOLUTIONS AB NEXT DAY/JOUR SUIVANT AJAX, TOWN OF - TAXES ON NEXT DAY/JOUR SUIVANT ALBERTA BLUE CROSS AB NEXT DAY/JOUR SUIVANT ALBERTA MAINTENANCE ENFORCEMENT PROGRAM AB NEXT DAY/JOUR SUIVANT ALBERTA MOTOR ASSOCIATION - INSURANCE COMPANY AB NEXT DAY/JOUR SUIVANT ALGOMA POWER ON NEXT DAY/JOUR SUIVANT ALIANT ACTIMEDIA NL NEXT DAY/JOUR SUIVANT ALIANT MOBILITY - NS/NB NS NEXT DAY/JOUR SUIVANT ALIANT MOBILITY / NL NS NEXT DAY/JOUR SUIVANT ALIANT MOBILITY/PEI PE NEXT DAY/JOUR SUIVANT ALLIANCEONE ON NEXT DAY/JOUR SUIVANT ALLSTATE INSURANCE ON NEXT DAY/JOUR SUIVANT ALLY CREDIT CANADA ON NEXT DAY/JOUR SUIVANT ALLY CREDIT CANADA LIMITED (AUTO) -

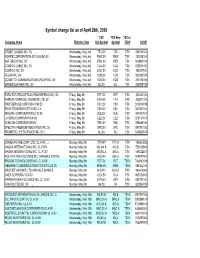

Toronto Stock Exchange and TSX Venture Exchange Symbol Change List

Symbol change list as of April 26th, 2006 TSX TSX New TSX or Company Name Effective Date Old Symbol Symbol TSXV CUSIP TRIZEC CANADA INC. SV Wednesday, May 3rd TZC.SV TZC TSX 896874104 POWER CORPORATION OF CANADA SV Wednesday, May 3rd POW.SV POW TSX 739239101 ADF GROUP INC. SV Wednesday, May 3rd DRX.SV DRX TSX 00089N103 COGECO CABLE INC. SV Wednesday, May 3rd CCA.SV CCA TSX 19238V105 COGECO INC. SV Wednesday, May 3rd CGO.SV CGO TSX 19238T100 VELAN INC. SV Wednesday, May 3rd VLN.SV VLN TSX 922932108 COSSETTE COMMUNICATION GROUP INC. SV Wednesday, May 3rd KOS.SV KOS TSX 221478100 DANIER LEATHER INC. SV Wednesday, May 3rd DL.SV DL TSX 235909108 EXFO ELECTRO-OPTICAL ENGINEERING INC. SV Friday, May 5th EXF.SV EXF TSX 302043104 FAIRFAX FINANCIAL HOLDINGS LTD. SV Friday, May 5th FFH.SV FFH TSX 303901102 FIRSTSERVICE CORPORATION SV Friday, May 5th FSV.SV FSV TSX 33761N109 FOUR SEASONS HOTELS INC. LV Friday, May 5th FSH.SV FSH TSX 35100E104 INSCAPE CORPORATION CL 'B' SV Friday, May 5th INQ.SV INQ TSX 45769T102 LA SENZA CORPORATION SV Friday, May 5th LSZ.SV LSZ TSX 50511P101 TEKNION CORPORATION SV Friday, May 5th TKN.SV TKN TSX 878949106 SPECTRA PREMIUM INDUSTRIES INC. SV Friday, May 5th SPD.SV SPD TSX 847931102 PROMETIC LIFE SCIENCES INC. SV J Friday, May 5th PLI.SV PLI TSX 74342Q104 CANADIAN TIRE CORP. LTD. CL A NV Monday, May 8th CTR.NV CTC.A TSX 136681202 MAGNA INTERNATIONAL INC. CL B MV Monday, May 8th MG.MV.B MG.B TSX 559222500 MAGNA INTERNATIONAL INC. -

An Historical Analysis of Foreign Ownership Restrictions in the Canadian

An Historical Analysis of Foreign Ownership Restrictions in the Canadian Telecommunications Sector Marsha Ann Tate ([email protected]) College of Communications The Pennsylvania State University Communications 581 Fall 2001 Semester Paper Dr. Taylor Foreign Ownership Restrictions in the Canadian Telecom Sector: M. A. Tate 2 Introduction In addition to a several thousand mile long border, Canada also shares a variety of cultural, economic, historical, sociological, and technological similarities with the United States. These numerous commonalties have helped foster close ties between the two countries. As the U.S. State Department's March 2000 Background Note: Canada attests: The bilateral relationship between the United States and Canada is perhaps the closest and most extensive in the world. It is reflected in the staggering volume of trade -- over $1.4 billion a day--and people--over 200 million a year--crossing the U.S.-Canadian border. Canada and the United States also share one of the world's largest bilateral direct investment relationships. Stock of U.S. direct investment in Canada was estimated at $116.7 billion, or about 72% of total foreign direct investment in Canada at the end of 1999. Conversely, Canada is the third-largest foreign investor in the United States with direct investments totaling approximately $90.4 billion at the end of 1999 (Background Note: Canada; U.S. Department of State, March 2000). Canada's multiple similarities to the United States coupled with large disparities in population and market size (Canada's market is approximately ten times smaller than its U.S. counterpart), have historically raised Canadian fears of cultural, economic, and political domination at the hands of its southern neighbor. -

2005 London Majors Program

MORTGAGES we make mortgages ••• make sense www.omac-mortgages.com Thank you London for making us your #I mortgage team! Helping Londoners for over 12 years achieve home ownership, and save on their mortgages The banks make their profits from charging you higher rates. We make our living, at no cost to you (OAC), by getting you the lowest rate! Is your bank really giving you the lowest rate they can offer? Not sure? Call us. WESTMOUNT SHOPPING 99 HORTON ST. W. CENTRE (just west of Wharncliffe) 471-4218 432-0622 Dave Provident! Jill Houston Karrl Sims Pat Brown AS SEEN ON: Rogers Cable 13 • The London Knights • No Price Like Home AS HEARD ON: AM 980 • AM 1290 • AM 1410 • AM 900 • AM 800 • AM 1070 • FM 96 • FM 103.9 H E AD O F FI C E : 3 46 WONDERLAND RD . S . LONDON, ON • 432 - 0026 Jletter J[rom t!Je ,J)resibent/@bJner What a phenomenal 2004 season the Majors had. We went from a team that no one was worried about during the regular season to league championship finalists and a real giant killer in the playoffs; knocking off Kitchener in 7 games, Toronto in 5 games before finally succumbing to Guelph in the finals. It was a great feeling from being the owner of the team, but also from being a fan of the game. I can't even begin to describe the electricity in the air during our home games in the playoffs. For that Scott Dart - brief period in time all the talk was about the incredible run that the Majors were on and speculating on far we were going to go.