Quarterly Report, Q1 2020

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

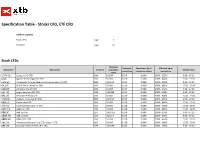

Specification Table - Stocks CFD, ETF CFD

Specification Table - Stocks CFD, ETF CFD Table of contents Stock CFDs page 1 ETF CFDs page 61 Stock CFDs Minimum Minimum Commission (% of XTB mark-up on Instrument Description Currency transaction Trading Hours commission transaction value) commission value 1COV.DE Covestro AG CFD EUR 50 EUR 8 EUR 0.08% 100% - 250% 9:00 - 17:30 A.US Agilent Technologies Inc CFD USD 50 USD 8 USD 0.08% 100% - 480% 15:30 - 22:00 A3M.ES Atresmedia Corp de Medios de Comunicacion SA CFD EUR 100 EUR 8 EUR 0.08% 100% - 250% 9:00 - 17:30 AA.US* CLOSE ONLY / Alcoa Inc CFD USD 50 USD 8 USD 0.08% 100% - 480% 15:30 - 22:00 AAD.DE Amadeus Fire AG CFD EUR 50 EUR 8 EUR 0.08% 100% - 250% 9:00 - 17:30 AAL.UK Anglo American PLC CFD GBP 100 GBP 8 EUR 0.08% 100% - 200% 9:00 - 17:30 AAL.US American Airlines CFD USD 50 USD 8 USD 0.08% 100% - 480% 15:30 - 22:00 AALB.NL Aalberts Industries NV CFD EUR 100 EUR 8 EUR 0.08% 100% - 250% 9:00 - 17:30 AAN.US Aaron's Inc CFD USD 50 USD 8 USD 0.08% 100% - 480% 15:30 - 22:00 AAP.US Advance Auto Parts Inc CFD USD 50 USD 8 USD 0.08% 100% - 480% 15:30 - 22:00 AAPL.US Apple Inc CFD USD 50 USD 8 USD 0.08% 100% - 480% 15:30 - 22:00 ABB.SE ABB Ltd CFD SEK 1000 SEK 8 EUR 0.08% 100% - 430% 9:00 - 17:25 ABBN.CH ABB Ltd CFD CHF 150 CHF 8 EUR 0.08% 100% - 375% 9:00 - 17:20 ABBV.US Abbvie Inc. -

FTSE Publications

2 FTSE Russell Publications FTSE Developed Europe SMID Cap 19 August 2021 Tradable Plus Indicative Index Weight Data as at Closing on 30 June 2021 Index weight Index weight Index weight Constituent Country Constituent Country Constituent Country (%) (%) (%) 3i Group 0.72 UNITED Bureau Veritas S.A. 0.42 FRANCE Gjensidige Forsikring ASA 0.17 NORWAY KINGDOM Campari 0.31 ITALY Gn Store Nordic 0.53 DENMARK AAK 0.18 SWEDEN Carl Zeiss Meditec 0.33 GERMANY Halma 0.66 UNITED Aalberts NV 0.24 NETHERLANDS Castellum 0.32 SWEDEN KINGDOM ABN AMRO Bank NV 0.23 NETHERLANDS Centrica 0.2 UNITED Hargreaves Lansdown 0.39 UNITED Acciona S.A. 0.16 SPAIN KINGDOM KINGDOM Accor 0.32 FRANCE Chr. Hansen Holding A/S 0.43 DENMARK Hays 0.16 UNITED ACS Actividades Cons y Serv 0.3 SPAIN Clariant 0.21 SWITZERLAND KINGDOM Adecco Group AG 0.49 SWITZERLAND Coca-Cola HBC AG 0.33 UNITED HeidelbergCement AG 0.6 GERMANY Adevinta 0.21 NORWAY KINGDOM HelloFresh SE 0.67 GERMANY Admiral Group 0.43 UNITED Cofinimmo 0.21 BELGIUM Helvetia Holding AG 0.18 SWITZERLAND KINGDOM Commerzbank 0.35 GERMANY Hikma Pharmaceuticals 0.27 UNITED Aedifica 0.22 BELGIUM ConvaTec Group 0.25 UNITED KINGDOM Aegon NV 0.34 NETHERLANDS KINGDOM Hiscox 0.18 UNITED KINGDOM Aeroports de Paris 0.17 FRANCE Countryside Properties 0.16 UNITED Holmen AB 0.2 SWEDEN Ageas 0.46 BELGIUM KINGDOM Homeserve 0.17 UNITED Aker BP ASA 0.16 NORWAY Covestro AG 0.54 GERMANY KINGDOM Alfa Laval 0.52 SWEDEN Covivio 0.2 FRANCE Howden Joinery Group 0.3 UNITED Alstom 0.7 FRANCE Croda International 0.64 UNITED KINGDOM KINGDOM Alten 0.18 -

Arctic Norwegian Equities Monthly Report July 2020

Arctic Norwegian Equities Monthly Report July 2020 FUND COMMENTS Arctic Norwegian Equities gave 3.4% return in July (I-class) versus 4% for the OSEFX benchmark index. Year to date the fund has returned -14.3% compared to -10.1% for the OSEFX. Since inception the fund has returned 120.7% versus 100.2% for the benchmark index. In July many of the largest companies on the Oslo Stock Exchange an- nounced results for the 2nd quarter. Several companies delivered above market expectations. Of note is DNB which rose near 10 percent on the day of reporting, driven by lower loan losses and higher other income. A number of companies also announced positive profit warmings, including B2 Holding, XXL, Atea and Europris. In July positive attribution for the Fund versus the benchmark index came from overweights in Atea and Crayon, and underweight in Mowi. Atea announced positive results for the 2nd quarter. Revenues were up by 12 percent from Q2 last year, and the company’s operating profit and bottom line were 50 percent higher than market expec- tations. Atea has further strengthened its competitive position in the Nordics, with a marked share in excess of 20 percent. Crayon also rose in July, partly due to strong software sales for Atea. Crayon is a large global partner of Microsoft. Microsoft announced 2nd quarter results which exceeded market expectations on the top- and bottom line. Shares in salmon farming declined in July, partly due to weak salmon price development. Demand for air transport to China has been reduced after discovery of coronavirus on a salmon cutting board in Beijing. -

Renewable Hydrogen, Made Cost Competitive

SPECIAL FEATURE – HYDROGEN ENERGY Renewable hydrogen, made cost competitive An interview with Jon André Løkke, CEO of Nel ASA, by Joanna Sampson magine a time before petroleum and electricity – horse- drawn carriages dominated the highways and byways and candles provided artificial lighting. The world was I transformed by fossil solutions in just a few centuries. But we are currently being faced with the side effects of utilising fossil energy – climate change and pollution. The obvious solution to these problems is exchanging fossil fuels with new renewable energies like solar, wind, and wave power. According to one company in Norway, it’s time for another global transformation. This time, it will be transformed by hydrogen, the simplest and most abundant element in the universe. In 1940, Nel undertook the world’s largest water Nel ASA has a vision of empowering generations with clean electrolysis installation at Rjukan, Norway, with a total 3 energy forever. To achieve this, CEO Jon André Løkke hydrogen production capacity exceeding 30,000Nm /hour believes hydrogen, along with renewable energy, must from hydropower. play a main role in the biggest energy transition since the Just over a decade later, in 1953, Nel started up a second discovery of oil. large-scale hydro-powered electrolyser plant for supplying Three quarters of the sun is made from hydrogen, providing hydrogen to ammonia production in Glomfjord, Norway. us with all the clean energy we need for at least another And in 1959 the company completely redesigned the five billion years. Realising that we have unlimited access electrolyser unit, forming the basis for today’s atmospheric to the sun raises an interesting question though: how do we electrolyser. -

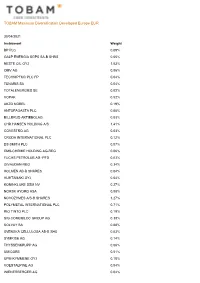

TOBAM Maximum Diversification Developed Europe EUR

TOBAM Maximum Diversification Developed Europe EUR 30/04/2021 Instrument Weight BP PLC 0.09% GALP ENERGIA SGPS SA-B SHRS 0.05% NESTE OIL OYJ 1.03% OMV AG 0.06% TECHNIPFMC PLC FP 0.04% TENARIS SA 0.04% TOTALENERGIES SE 0.02% VOPAK 0.52% AKZO NOBEL 0.19% ANTOFAGASTA PLC 0.05% BILLERUD AKTIEBOLAG 0.03% CHR HANSEN HOLDING A/S 1.41% COVESTRO AG 0.03% CRODA INTERNATIONAL PLC 0.12% DS SMITH PLC 0.07% EMS-CHEMIE HOLDING AG-REG 0.06% FUCHS PETROLUB AG -PFD 0.03% GIVAUDAN-REG 0.34% HOLMEN AB-B SHARES 0.04% HUHTAMAKI OYJ 0.04% KONINKLIJKE DSM NV 0.27% NORSK HYDRO ASA 0.08% NOVOZYMES A/S-B SHARES 1.27% POLYMETAL INTERNATIONAL PLC 0.71% RIO TINTO PLC 0.19% SIG COMBIBLOC GROUP AG 0.38% SOLVAY SA 0.08% SVENSKA CELLULOSA AB-B SHS 0.03% SYMRISE AG 0.14% THYSSENKRUPP AG 0.06% UMICORE 0.51% UPM-KYMMENE OYJ 0.18% VOESTALPINE AG 0.04% WIENERBERGER AG 0.04% TOBAM Maximum Diversification Developed Europe EUR 30/04/2021 Instrument Weight YARA INTERNATIONAL ASA 0.08% A P MOLLER - MAERSK A/S - A 0.06% A P MOLLER - MAERSK A/S - B 0.08% ACS ACTIVIDADES CONS Y SERV 0.07% ADDTECH AB-B SHARES 0.03% ADP 0.04% AENA SA 0.11% ALSTOM 0.17% ANDRITZ AG 0.03% ATLANTIA SPA 0.08% BELIMO HOLDING AG-REG 0.04% BUCHER INDUSTRIES AG-REG 0.04% BUNZL PLC 0.10% DEUTSCHE LUFTHANSA-REG 0.05% DIPLOMA PLC 0.04% DSV PANALPINA A/S 0.45% EASYJET PLC 0.20% ELIS SA 0.03% EPIROC AB-A 0.10% EPIROC AB-B 0.06% FERROVIAL SA 0.05% FLUGHAFEN ZURICH AG-REG 0.03% GEA GROUP AG 0.06% GEBERIT AG-REG 0.21% HAYS PLC 0.03% HOMESERVE PLC 0.04% HOWDEN JOINERY GROUP PLC 0.06% IMCD GROUP NV 0.07% IMI PLC 0.05% -

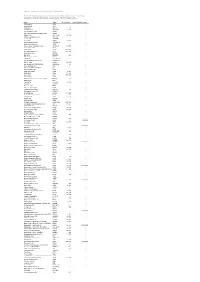

International Smallcap Separate Account As of July 31, 2017

International SmallCap Separate Account As of July 31, 2017 SCHEDULE OF INVESTMENTS MARKET % OF SECURITY SHARES VALUE ASSETS AUSTRALIA INVESTA OFFICE FUND 2,473,742 $ 8,969,266 0.47% DOWNER EDI LTD 1,537,965 $ 7,812,219 0.41% ALUMINA LTD 4,980,762 $ 7,549,549 0.39% BLUESCOPE STEEL LTD 677,708 $ 7,124,620 0.37% SEVEN GROUP HOLDINGS LTD 681,258 $ 6,506,423 0.34% NORTHERN STAR RESOURCES LTD 995,867 $ 3,520,779 0.18% DOWNER EDI LTD 119,088 $ 604,917 0.03% TABCORP HOLDINGS LTD 162,980 $ 543,462 0.03% CENTAMIN EGYPT LTD 240,680 $ 527,481 0.03% ORORA LTD 234,345 $ 516,380 0.03% ANSELL LTD 28,800 $ 504,978 0.03% ILUKA RESOURCES LTD 67,000 $ 482,693 0.03% NIB HOLDINGS LTD 99,941 $ 458,176 0.02% JB HI-FI LTD 21,914 $ 454,940 0.02% SPARK INFRASTRUCTURE GROUP 214,049 $ 427,642 0.02% SIMS METAL MANAGEMENT LTD 33,123 $ 410,590 0.02% DULUXGROUP LTD 77,229 $ 406,376 0.02% PRIMARY HEALTH CARE LTD 148,843 $ 402,474 0.02% METCASH LTD 191,136 $ 399,917 0.02% IOOF HOLDINGS LTD 48,732 $ 390,666 0.02% OZ MINERALS LTD 57,242 $ 381,763 0.02% WORLEYPARSON LTD 39,819 $ 375,028 0.02% LINK ADMINISTRATION HOLDINGS 60,870 $ 374,480 0.02% CARSALES.COM AU LTD 37,481 $ 369,611 0.02% ADELAIDE BRIGHTON LTD 80,460 $ 361,322 0.02% IRESS LIMITED 33,454 $ 344,683 0.02% QUBE HOLDINGS LTD 152,619 $ 323,777 0.02% GRAINCORP LTD 45,577 $ 317,565 0.02% Not FDIC or NCUA Insured PQ 1041 May Lose Value, Not a Deposit, No Bank or Credit Union Guarantee 07-17 Not Insured by any Federal Government Agency Informational data only. -

NEL Hydrogen AS (Unaudited)

NEL ASA – update February 2016 Jon André Løkke, CEO 1 NEL ASA • Established by Norsk Hydro in 1927 • First dedicated hydrogen company on the OSE* (NEL.OSE) • Extensive competence in designing hydrogen energy systems and refuelling stations, through Norsk Hydro, Statoil and H2 Logic: – >500 large scale electrolysers sold in >50 countries – 28 hydrogen refuelling stations delivered to 7 countries • Pure play company with long track record: – Most energy efficient electrolysers, robust and proven technology – Refuelling stations with highest uptime and lowest cost of ownership – Long list of new technology developments that will secure a leading position * OSE – Oslo Stock Exchange 2 NEL ASA Q4 2015 – IN SHORT Highlights of the quarter H2 Logic AS (unaudited) • Entered into a letter of intent with Uno-X Gruppen AS (Uno-X), for the rollout of minimum 20 hydrogen refuelling stations covering all the major cities in Norway within 2020 • H2 Logic AS, was awarded a contract for one H2Station fueling station for H2 MOBILITY Deutschland GmbH & Co.KG with an option for multiple repeat-orders. The station will be one among the first in a planned staged expansion onwards 2023 of up to 400 stations in Germany and a total investment of around 400 million euro • Raised NOK 111 million in gross proceeds through a private placement of 30 million new shares at a price of NOK 3.70 per share • The cash balance at the end of the fourth quarter was NOK 313 million NEL Group NEL Hydrogen AS (unaudited) 3 PROUD HISTORY & EXTENSIVE HYDROGEN KNOWHOW SINCE 1927 Glomfjord, -

Kvinnedagen 2021 – Grafpakke

Kvinnedagen, kvinner og aksjer Et skråblikk fra Stiftelsen AksjeNorge Data per 31. 12.2020 Kristin Skaug, daglig leder i Kvinner og menn fordelt på antall Verdifordeling (kjønn) Kvinner Kvinner 20 % 29 % Menn 71 % Menn 80 % Data per 31/12/2020 fra Euronext VPS. Grafikk: AksjeNorge Antall menn og kvinner øker Antall privatpersoner fordelt på kjønn 600 000 500 000 400 000 300 000 200 000 100 000 - 2013 2014 2015 2016 2017 2018 2019 2020 Total Kvinner Menn Data per 31/12/2020 fra Euronext VPS. Grafikk: AksjeNorge Antall investorer og deres fordeling på ulike markedsplasser 300 000 250 000 200 000 150 000 100 000 50 000 - Kvinner Menn Kvinner Menn Kvinner Menn Kun investert på Både Oslo Børs og Kun investert på OSLO BØRS Euronext Growth Euronext Growth Data per 31/12/2020 fra Euronext VPS. Grafikk: AksjeNorge Data per 31/12/2020 fra Euronext VPS. Grafikk: AksjeNorge Data per 31/12/2020 fra Euronext VPS. Grafikk: AksjeNorge Både kvinner og menn Data per 31/12/2020 fra Euronext VPS. Grafikk: AksjeNorge Selskap SUM Antall Sum verdi Snittverdi EQUINOR ASA 33453 3 521 471 686 105 266 DNB ASA 17582 2 595 596 472 147 628 NORSK HYDRO ASA 14618 678 897 035 46 443 ORKLA ASA A- AKSJER 13800 2 015 831 673 146 075 TELENOR ASA 12789 871 269 279 68 126 NORWEGIAN AIR 11934 51 648 620 4 328 YARA INTERNATIO 11577 696 674 556 60 177 STOREBRAND ASA ORD. 9141 402 403 610 44 022 GJENSIDIGE FORS 8386 1 081 592 213 128 976 MOWI ASA 5646 459 845 488 81 446 Aker Solution 5288 153 048 234 28 943 REC SILICON ASA 5244 135 159 097 25 774 NEL ASA 5052 350 341 312 69 347 AKER OFFSHORE W 4800 111 445 602 23 218 AKER CARBON CAP 4762 132 969 987 27 923 Når du tar med alle markedsplassene med, ser du at Aker offshore wind og Aker carbon capture kommer med fra Euronext Growth Data per 31/12/2020 fra Euronext VPS. -

Belåningssatser Pr 12.08.2021

Belåningssatser pr 24.09.2021 Endring av belåningssatser vil skje løpende OBX Ticker Company ISIN Margin rate ADE ADEVINTA ASA NO0010844038 66% AKER AKER ASA-A SHARES NO0010234552 74% AKRBP AKER BP ASA NO0010345853 41% AKSO AKER SOLUTIONS ASA NO0010716582 66% BAKKA BAKKAFROST P/F FO0000000179 84% DNB DNB BANK ASA NO0010161896 60% ENTRA ENTRA ASA NO0010716418 77% EQNR EQUINOR ASA NO0010096985 85% GJF GJENSIDIGE FORSIKRING ASA NO0010582521 82% LSG LEROY SEAFOOD GROUP ASA NO0003096208 85% MOWI MOWI ASA NO0003054108 85% NEL NEL ASA NO0010081235 75% NHY NORSK HYDRO ASA NO0005052605 85% NOD NORDIC SEMICONDUCTOR ASA NO0003055501 84% ORK ORKLA ASA NO0003733800 85% RECSI REC SILICON ASA NO0010112675 65% SALM SALMAR ASA NO0010310956 85% SCATC SCATEC ASA NO0010715139 61% SCHA SCHIBSTED ASA-CL A NO0003028904 84% STB STOREBRAND ASA NO0003053605 79% SUBC SUBSEA 7 SA LU0075646355 74% TEL TELENOR ASA NO0010063308 85% TGS TGS ASA NO0003078800 83% TOM TOMRA SYSTEMS ASA NO0005668905 85% YAR YARA INTERNATIONAL ASA NO0010208051 85% Ticker Company ISIN Margin rate ABG ABG SUNDAL COLLIER HOLDING NO0003021909 62% ACC AKER CARBON CAPTURE ASA NO0010890304 64% ACR AXACTOR SE NO0010840515 60% AFG AF GRUPPEN ASA NO0003078107 75% AGAS AVANCE GAS HOLDING LTD BMG067231032 41% AKAST AKASTOR ASA NO0010215684 41% AKBM AKER BIOMARINE ASA NO0010886625 75% AKH AKER HORIZONS ASA NO0010921232 62% ARCH ARCHER BMG0451H1170 75% ARCUS ARCUS ASA NO0010776875 75% #Confidential ARR ARRIBATEC GROUP ASA NO0003108102 65% ASA ATLANTIC SAPPHIRE ASA NO0010768500 74% ATEA ATEA ASA NO0004822503 -

Active Ownership Report: 2020 Danske Bank Asset Management January 2021 Active Ownership Report

Active Ownership Report: 2020 Danske Bank Asset Management January 2021 Active Ownership Report When customers entrust us with their assets and savings, it is our duty to serve their interests by providing investment solutions with the goal to deliver competitive and long-term performance. Our firm commitment to Responsible Investment is an integral part of this duty. It is about making better-informed investment decisions – addressing issues of risk, problems, and dilemmas, and influencing portfolio companies through active ownership to contribute to a positive outcome. Active ownership – through direct dialogue, collaborative engagement and voting at the annual general meetings – is an important part of our ability to create long-term value to the companies we invest in and to our customers. We believe it is more responsible to address material sustainability matters as investors rather than refraining from investing when issues of concern arise, leaving the problem to someone else to solve. Our portfolio managers are the change agents who can impact companies to manage risks and opportunities. The aim of our Active Ownership Report covering three parts ‘Engagements’, ‘Collaborative Engagements’ and ‘Voting’ is to provide our customers and stakeholders with regular updates on our progress and results. The three parts of the report Part 1: Engagements Part 2: Voting Part 3: Collaborative Engagements 2 Where to get additional information Sustainable Investment Policy Our Sustainable Investment Journey click here click here Active Ownership Instruction Active Ownership Stories click here click here Voting Guidelines Proxy Voting Dashboard click here click here 3 Active Ownership Report, Part 1 Engagements This presentation is intended to be used as marketing material as defined by the European Directive 2014/65/EU dated 15 May 2014 (MiFID II) in Austria, Belgium, Denmark, Finland, France, Germany, Luxembourg, the Netherlands, Norway, Sweden, Switzerland and the United Kingdom. -

Positions in Financial Instruments As of July 10Th 2017

Disclosure - positions in financial instruments as of July 10th 2017 Please find below a list of positions in financial instruments held by employees of Arctic Securities AS with regard to Arctic Securities' research coverage universe. The list is updated monthly. Name Ticker No of shares Nominal NOK in bonds AF Gruppen AFG - - Akastor ASA AKA - - Aker ASA AKER 2 - Aker BP ASA AKERBP 1 500 - Aker Solutions ASA AKSO - - American Shipping Company ASA AMSC - - Archer Ltd. ARCHER 33 400 - Ardmore Shipping Corp. ASC US - - Asetek A/S ASETEK - - Atea ASA ATEA 2 803 - Atlantic Sapphire AS ATLANTIC - - Atwood Oceanics, Inc. ATW - - Avance Gas Holdings Limited AVANCE 24 045 - Awilco LNG ASA ALNG - - Axactor AB AXA 877 846 - B2Holding AS (B2H) B2H 242 500 - BerGenBio ASA BGBIO - - BW LPG BWLPG 223 - BW Offshore Limited BWO - - Cherry AB CHER.B-SE - - Corem Property Group AB CORE SS - - Cxense ASA Cxense 20 332 - Danske Bank A/S (DANSKE) DANSKE 27 - DHT Holdings, Inc. DHT - - Diamond Offshore Drilling DO - - Diana Shipping Inc DSX - - DNB ASA (DNB) DNB 8 907 - DNO ASA DNO 17 500 - DOF ASA DOF 500 000 - Dorian LPG LPG - - Electromagnetic Geoservices ASA EMGS 15 - ENSCO plc ESV - - Entra ASA ENTRA 3 878 - Euronav EURN - - Europris ASA EPR - - Faroe Petroleum plc FPM - - Fastighets AB Balder BALDB 85 - Fingerprint Cards AB FING-B - - Flex LNG Ltd FLNG 19 000 - Fred. Olsen Energy ASA FOE 100 - Frontline Ltd. FRO 5 550 - Gaslog Ltd. GLOG - - Genmab A/S GEN - - Gentian Diagnostics GENT-ME 214 195 - Gjensidige Forsikring ASA (GJF) GJF 12 537 - Golar LNG Ltd GLNG - - Golden Ocean Group Ltd. -

1 Årsrapport 2018

Første halvår 12018 Andre halvår 2 2018 Årsrapport 2018 Verdipapirfond forvaltet av Storebrand Asset Management AS Innhold Årsberetning 2018 3 Regnskap og noter Delphi Fondene 6 Storebrand Global Obligasjon 150 Storebrand Fondene aksjefond 15 Storebrand Global Solutions 154 Storebrand Fondene rentefond 40 Storebrand Global Value 157 Storebrand Høyrente 160 Porteføljer Storebrand Indeks – Alle Markeder 163 Delphi Europe 55 Storebrand Indeks – Norge 196 Delphi Global Valutasikret 57 Storebrand Indeks – Nye Markeder 199 Delphi Global 58 Storebrand Kombinasjon 214 Delphi Kombinasjon 60 Storebrand Likviditet 215 Delphi Nordic 63 Storebrand Norge Fossilfri 219 Delphi Norge 65 Storebrand Norge I 221 FO Norsk Kreditt 67 Storebrand Norge 223 FO Norsk Likviditet 70 Storebrand Norsk Kreditt IG 20 225 SEB NOK Liquidity Fund 72 Storebrand Norsk Kreditt IG 229 Storebrand Aksje Innland 73 Storebrand Optima Norge 236 Storebrand AksjeSpar 75 Storebrand Rente+ 238 Storebrand Global ESG Plus 76 Storebrand Stat 241 Storebrand Global ESG 90 Storebrand Vekst 242 Storebrand Global Indeks Valutasikret 104 Storebrand Verdi 244 Storebrand Global Indeks 105 Storebrand Global Kreditt IG 134 Børser og markedsplasser 245 Storebrand Global Multifactor 139 Revisors beretning 249 Storebrand Global Multifaktor Valutasikret 149 Avkastning og risiko 251 Årsberetning 2018 for verdipapirfond forvaltet av Storebrand Asset Management AS Om virksomheten Storebrand Asset Management AS (SAM) er et forvalt- Avkastning og risiko ningsselskap med konsesjon etter verdipapirfondloven og Børsnedgangen reflekteres i fondenes verdiutvikling, og i lov om alternative investeringsfond til bl.a. forvaltning av 2018 ga 25 av 37 fond negativ avkastning. verdipapirfond og alternative investeringsfond samt aktiv forvaltning etter verdipapirhandelloven. Selskapet ble Blant 14 aktive aksjefond ga to fond verdioppgang, mens etablert i 1981 og er et heleid datterselskap av Storebrand fem fond ga positiv differanseavkastning sammenlignet ASA.