Arctic Norwegian Equities Monthly Report May 2020

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Candidates Nominated to the Board of Directors in Gjensidige Forsikring ASA

Office translation for information purpose only Appendix 18 Candidates nominated to the Board of Directors in Gjensidige Forsikring ASA Per Andersen Born in 1947, lives in Oslo Occupation/position: Managing Director, Det norske myntverket AS Education/background: Chartered engineer and Master of Science in Business and Economics, officer’s training school, Director of Marketing and Sales and other positions with IBM, CEO of Gjensidige, CEO of Posten Norge and Managing Director of ErgoGroup, senior consultant to the CEO of Posten Norge, CEO of Lindorff. Trond Vegard Andersen Born in 1960, lives in Fredrikstad Occupation/position: Managing Director of Fredrikstad Energi AS Education/background: Certified public accountant and Master of Science in Business and Economics from the Norwegian School of Business Economics and Administration (NHH) Offices for Gjensidige: Member of owner committee in East Norway Organisational experience: Chairman of the Board for all FEAS subsidiaries, board member for Værste AS (regional development in Fredrikstad) Hans-Erik Folke Andersson Born in 1950, Swedish, lives in Djursholm Occupation/position: Consultant, former Managing Director of insurance company Skandia, Nordic Director for Marsh & McLennan and Executive Director of Mercantile & General Re Education/background: Statistics, economy, business law and administration from Stockholm University Offices for Gjensidige: Board member since 2008 Organisational experience: Chairman of the Board of Semcon AB, Erik Penser Bankaktiebolag and Canvisa AB and a board member of Cision AB. Per Engebreth Askildsrud Born in 1950, lives in Jevnaker Occupation/position: Lawyer, own practice Education/background: Law Offices for Gjensidige: Chairman of the owner committee Laila S. Dahlen Born in 1968, lives in Oslo Occupation/position: Currently at home on maternity leave. -

View Annual Report

ANNUAL REPORT 2015 www.bakkafrost.com Faroese Company Registration No.: 1724 TABLE OF CONTENTS Table of Contents Chairman’s Statement 4 Statement by the Management and the Board of Directors 6 Key Figures 10 Bakkafrost’s History 12 Group Structure 16 Operation Sites 20 Main Events 22 Operational Review 24 Financial Review 28 Operational Risk and Risk Management 38 Financial Risk and Risk Management 42 Outlook 44 Business Review 46 Business Objectives and Strategy 62 BAKKAFROST 2 ANNUAL REPORT 2015 TABLE OF CONTENTS Operation 64 Health, Safety and the Environment 68 Shareholder Information 70 Directors’ Profiles 72 Group Management’s Profiles 76 Other Managers’ Profiles 78 Corporate Governance 80 Statement by the Management and the Board of Directors on the Annual Report 81 Independent Auditor’s Report 82 Bakkafrost Group Consolidated Financial Statements 84 Table of Contents – Bakkafrost Group 85 P/F Bakkafrost – Financial Statements 133 Table of Contents – P/F Bakkafrost 134 Glossary 147 BAKKAFROST 3 ANNUAL REPORT 2015 CHARIMAN’S STATEMENT Chairman’s Statement Bakkafrost has in recent years grown into one of the largest companies in the Faroe Islands. Our aim to run Bakkafrost responsibly and sustainably is important to our entire stakeholders, i.e. employees, shareholders and society. Bakkafrost has a growth strategy of creating sustainable values and not just short-term gains. This strategy demands daily awareness of opportunities and threats to our operations from both the board, the management and the employees. RÚNI M. HANSEN Chairman of the Board 810 million (DKK) The result after tax for 2015 BAKKAFROST 4 ANNUAL REPORT 2015 CHARIMAN’S STATEMENT March 2015 marked the five years’ milestone since Bakka- commence production in 2016, and our processing opera- frost was listed on Oslo Stock Exchange. -

The Supervisory Board of Gjensidige Forsikring ASA

The Supervisory Board of Gjensidige Forsikring ASA Name Office Born Lives in Occupation/position Education/background Organisational experience Bjørn Iversen Member 1948 Reinsvoll Farmer Degree in agricultural economics, Head of the Oppland county branch of the the Agricultural University of Norwegian Farmers' Union 1986–1989, Norway in 1972. Landbrukets head of the Norwegian Farmers' Union sentralforbund 1972–1974, Norges 1991–1997, chair of the supervisory board Kjøtt- og Fleskesentral 1974–1981, of Hed-Opp 1985–89, chair/member of the state secretary in the Ministry of board of several companies. Agriculture 1989–1990. Chair of the Supervisory Board and Chair of the Nomination Committee of Gjensidige Forsikring ASA. Hilde Myrberg Member 1957 Oslo MBA Insead, law degree. Deputy chair of the board of Petoro AS, member of the board of CGGVeritas SA, deputy member of Stålhammar Pro Logo AS, member of the nomination committee of Det Norske ASA, member of the nomination committee of NBT AS. Randi Dille Member 1962 Namsos Self-employed, and Economics subjects. Case Chair of the boards of Namsskogan general manager of officer/executive officer in the Familiepark, Nesset fiskemottak and Namdal Bomveiselskap, agricultural department of the Namdal Skogselskap, member of the board Namsos County Governor of Nord- of several other companies. Sits on Nord- Industribyggeselskap and Trøndelag, national recruitment Trøndelag County Council and the municipal Nordisk Reinskinn project manager for the council/municipal executive board of Compagnie DA. Norwegian Fur Breeders' Namsos municipality. Association, own company NTN AS from 1999. Benedikte Bettina Member 1963 Krokkleiva Company secretary and Law degree from the University of Deputy member of the corporate assembly Bjørn (Danish) advocate for Statoil ASA. -

Gjensidige Bank Investor Presentation Q1 2017

Gjensidige Bank Investor Presentation Q1 2017 4. May 2017 Disclaimer The information contained herein has been prepared by and is the sole responsibility of Gjensidige Bank ASA and Gjensidige Bank Boligkreditt AS (“the Company”). Such information is confidential and is being provided to you solely for your information and may not be reproduced, retransmitted, further distributed to any other person or published, in whole or in part, for any purpose. Failure to comply with this restriction may constitute a violation of applicable securities laws. The information and opinions presented herein are based on general information gathered at the time of writing and are therefore subject to change without notice. While the Company relies on information obtained from sources believed to be reliable but does not guarantee its accuracy or completeness. These materials contain statements about future events and expectations that are forward-looking statements. Any statement in these materials that is not a statement of historical fact including, without limitation, those regarding the Company’s financial position, business strategy, plans and objectives of management for future operations is a forward-looking statement that involves known and unknown risks, uncertainties and other factors which may cause our actual results, performance or achievements of the Company to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements. Such forward-looking statements are based on numerous assumptions regarding the Company’s present and future business strategies and the environment in which the Company will operate in the future. The Company assumes no obligations to update the forward-looking statements contained herein to reflect actual results, changes in assumptions or changes in factors affecting these statements. -

Renewable Energy Risking Rights & Returns

` RENEWABLE ENERGY RISKING RIGHTS & RETURNS: An analysis of solar, bioenergy and geothermal companies’ human rights commitments SEPTEMBER 2018 CONTENTS CONTENTS Executive summary 1 Introduction 4 Analysis 6 1. Leaders and laggards 6 2. Public commitment to human rights 12 3. Commitment to community consultations 12 4. Access to remedy 14 5. Labour rights 16 6. Supply chain monitoring 17 Recommendations 19 Annex 21 Photo credit: Andreas Gücklhorn/Unsplash EXECUTIVE SUMMARY EXECUTIVE SUMMARY Key messages Renewable energy is key for our transition to a low-carbon economy, but companies’ human rights policies and practices are not yet strong enough to ensure this transition is both fast and fair. Evidence shows failure to respect human rights can result in project delays, legal procedures and costs for renewable energy companies, underlying the urgency to strengthen human rights due diligence. We cannot afford to slow the critical transition to renewable energy with these kinds of impediments. As renewable energy investments expand in countries with weak human rights pro- tections, investors must step up their engagement to ensure projects respect human rights. Renewable energy has experienced a fourfold bioenergy and geothermal industries, increase in investment in the past decade. echoing findings from ourprevious analysis of Starting at $88 billion in 2005, new wind and hydropower companies. investments hit $349 billion in 2015.1 This eye-catching rise in investments is a welcome Alongside the moral imperative, companies trend and reflects international commitments can also avoid significant legal risks, project to combatting climate change and providing delays and financial costs by introducing access to energy in the Paris climate rigorous human rights due diligence policies agreement and the Sustainable Development and processes. -

2626667.Pdf (1.837Mb)

BI Norwegian Business School - campus Oslo GRA 19703 Master Thesis Thesis Master of Science Evaluating the Predictive Power of Leading Indicators Used by Analysts to Predict the Stock Return for Norwegian Listed Companies Navn: Amanda Marit Ackerman Myhre Hadi Khaddaj Start: 15.01.2020 09.00 Finish: 01.09.2020 12.00 GRA 19703 0981324 0983760 Evaluating the Predictive Power of Leading Indicators Used by Analysts to Predict the Stock Return for Norwegian Listed Companies Supervisor: Ignacio Garcia de Olalla Lopez Programme: Master of Science in Business with Major in Accounting and Business Control Abstract This paper studies the predictive power of leading indicators used by interviewed analysts to predict the monthly excess stock returns for some of the most influential Norwegian companies listed on the Oslo Stock Exchange. The thesis primarily seeks to evaluate whether a multiple factor forecast model or a forecast combination model incorporating additional explanatory variables have the ability to outperform a five common factor (FCF) benchmark forecast model containing common factors for the Norwegian stock market. The in-sample and out-of- sample forecasting results indicate that a multiple factor forecast model fails to outperform the FCF benchmark model. Interestingly, a forecast combination model with additional explanatory variables for the Norwegian market is expected to outperform the FCF benchmark forecast model. GRA 19703 0981324 0983760 Acknowledgements This thesis was written as the final piece of assessment after five years at BI Norwegian Business School and marks the completion of the Master of Science in Business program. We would like to thank our supervisor Ignacio Garcia de Olalla Lopez for his help and guidance through this process. -

Appendix 1: Firm & Industry Data

Appendix 1: Firm & Industry Data NORWAY ROYAL SALMON Appendix 1.1: Diverse Information RegionRegion North (NRS Q4 North 2016 Report) – Troms Two new sites in a new area approved ° Lubben and Korsnes ° Improve possibilities for split of each generation to reduce biological risks ° Improve growth possibilities New hatchery – NRS Settefisk ° Purchased land in Karlsøy municipality, Troms ° Planned production capacity of 10 million smolts NORWAY ROYAL SALMON ° Construction starts when necessary approvals have been given, Region South estimated within 1,5 to 2 years Region South (NRS Q4 2016 Report) ° Provide NRS with predictable ° planningOperates with in theregards Haugesund to smolts area, both in Rogaland and Hordaland county ° Region South holds a total of 6 licenses ° Owned 100 % through NRS Feøy AS 8 ° One single MAB Zone ° Enables smoother and better utilization of MAB ° Harvesting at Espevær Laks 35 02 Position of salmon 2.8 Supply of farmed and wild salmonids Wild & Farmed Salmon, historical annual supply (Marine Harvest, 2017) 2 400 Wild Farmed 2 200 2 000 1 800 1 600 1 400 1 200 1 000 800 Thousand Thousand tonnes GWE 600 400 200 - 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 The general supply of seafood in the world is shifting more towards aquaculture as the supply from wild catch is stagnating in several regions and for many important species. Wild catch of salmonids is varying04 between 700Salmon 000 and 1 000 Supply000 tonnes GWE, whereas farmed salmonids are increasing. The first year the total supply of salmonids was dominated by farmed, was in 1999. -

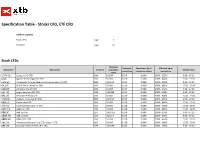

Specification Table - Stocks CFD, ETF CFD

Specification Table - Stocks CFD, ETF CFD Table of contents Stock CFDs page 1 ETF CFDs page 61 Stock CFDs Minimum Minimum Commission (% of XTB mark-up on Instrument Description Currency transaction Trading Hours commission transaction value) commission value 1COV.DE Covestro AG CFD EUR 50 EUR 8 EUR 0.08% 100% - 250% 9:00 - 17:30 A.US Agilent Technologies Inc CFD USD 50 USD 8 USD 0.08% 100% - 480% 15:30 - 22:00 A3M.ES Atresmedia Corp de Medios de Comunicacion SA CFD EUR 100 EUR 8 EUR 0.08% 100% - 250% 9:00 - 17:30 AA.US* CLOSE ONLY / Alcoa Inc CFD USD 50 USD 8 USD 0.08% 100% - 480% 15:30 - 22:00 AAD.DE Amadeus Fire AG CFD EUR 50 EUR 8 EUR 0.08% 100% - 250% 9:00 - 17:30 AAL.UK Anglo American PLC CFD GBP 100 GBP 8 EUR 0.08% 100% - 200% 9:00 - 17:30 AAL.US American Airlines CFD USD 50 USD 8 USD 0.08% 100% - 480% 15:30 - 22:00 AALB.NL Aalberts Industries NV CFD EUR 100 EUR 8 EUR 0.08% 100% - 250% 9:00 - 17:30 AAN.US Aaron's Inc CFD USD 50 USD 8 USD 0.08% 100% - 480% 15:30 - 22:00 AAP.US Advance Auto Parts Inc CFD USD 50 USD 8 USD 0.08% 100% - 480% 15:30 - 22:00 AAPL.US Apple Inc CFD USD 50 USD 8 USD 0.08% 100% - 480% 15:30 - 22:00 ABB.SE ABB Ltd CFD SEK 1000 SEK 8 EUR 0.08% 100% - 430% 9:00 - 17:25 ABBN.CH ABB Ltd CFD CHF 150 CHF 8 EUR 0.08% 100% - 375% 9:00 - 17:20 ABBV.US Abbvie Inc. -

Bakkafrost Annual Report 2013

Faroese Company Registration No.: 1724 BAKKAFROST ANNUAL REPORT 2013 WWW.BAKKAFROST.COM 1/119 / BAKKAFROST / ANNUAL REPORT 2013 2/119 / BAKKAFROST / ANNUAL REPORT 2013 TABLE OF CONTENTS Key Figures 4 Bakkafrost’s History 6 Group Structure 8 Operation Sites 10 Main Events 12 Chairman’s Statement 15 Statement by the Management and the Board of Directors 16 Business Review 34 Business Objectives and Strategy 48 Operation 50 Health, Safety and the Environment 54 Shareholder Information 57 Directors’ profiles 58 Group Management’s Profiles 60 Other Managers 62 Corporate Governance 65 Statement by the Management and the Board of Directors on the Annual Report 66 Independent Auditor’s Report 67 Bakkafrost Group Consolidated Financial Statements 68 P/F Bakkafrost - Financial Statements 109 3/119 / BAKKAFROST / ANNUAL REPORT 2013 2013 2,491 2012 1,855 2011 KEY FIGURES 1,321 2010 820 2009 Operating revenues 597 Mill. DKK 4/119 / BAKKAFROST / ANNUAL REPORT 2013 (DKK 1000) IFRS IFRS IFRS IFRS IFRS Income statement 2013 2012 2011 2010 2009 Operating revenues 2,491,081 1,855,544 1,321,092 820,212 596,565 Operational EBIT * 587,010 323,040 335,146 246,788 158,740 Operational EBITDA * 673,669 403,284 402,471 289,045 213,191 Earnings before interest and taxes (EBIT) 701,320 343,520 400,698 315,580 192,394 Earnings before taxes (EBT) 727,351 323,681 370,196 307,259 181,237 Net earnings 589,218 267,875 323,417 259,711 148,728 Earnings per share before fair value adjustment of biomass and provision for onerous contracts (DKK) 10.55 5.01 7.43 3.97 40.49 Earnings -

Storebrand Livsforsikring AS Annual Report 2011

Annual report 2011 Storebrand Livsforsikring AS ANNUAL REPORT 2011 2 | ANNUAL REPORT STOREBRAND LIVSFORSIKRING AS Contents Page 4 | Report of the board of directors Page 22 | Profit and loss account Page 24 | Statement of financial position Page 27 | Reconsiliation of change in equity Page 28 | Cash flow analysis Page 29 | Notes Page 114 | Actuary report Page 115 | Declaration by the members of the board and the CEO Page 116 | Audit report Page 118 | Control committee’s statement Page 119 | Board of representatives statement Page 120 | Terms and expressions ANNUAL REPORT STOREBRAND LIVSFORSIKRING AS | 3 ANNUAL REPORT 2011 Report of the board of directors Storebrand Livsforsikring primarily operates in Norway and its head office is in Lysaker Park in the Municipality of Bærum. Storebrand’s position as a leading player in the Nordic occupational pension market strengt- hened through 2011. In addition, several strategic and organisational adjustments were im- plemented in order to increase focus on the retail market. The reason for this initiative is the transition from defined benefit to defined contribution occupational pension schemes, where the individual employees have a greater involvement. Business relationships give the Group a strategic advantage in the relationships established with company employees. OUTLOOK Fusion of corporate and retail markets The shift from defined benefit to defined contribution occupational pension schemes has led to both risks and investment options being transferred from employer to employee. In addi- tion, the pensions reform will lead to lower future pension payments for many employees. In sum, this increases both the need and interest in pensions and private savings significantly. -

Annual Report

Annual Report 2018 2 Our vision Improving our future Our mission To deliver competitive and sustainable solar energy globally, to protect our environment and to improve quality of life through innovative integration of reliable technology Our values Predictable Working together Driving results Changemakers Scatec Solar ASA - Annual Report 2018 3 Contents Scatec Solar in brief 4 Value chain 6 Market development 7 CEO letter 8 Our people 10 Sustainability highlights 12 Report from the Board of Directors 15 Executive Management 34 Board of Directors 36 Consolidated financial statements Group 40 Notes to the Consolidated financial statements Group 46 Parent company financial statements 112 Notes to the parent company financial statements 116 Other definitions 137 Responsibility statement 138 Alternative Performance Measures 139 Appendix 142 Auditor’s report 144 4 Scatec Solar in brief Scatec Solar is an integrated independent solar power producer, delivering affordable, rapidly deployable and sustainable source of clean energy worldwide. As a long-term player, Scatec Solar develops, builds, owns, operates and maintains solar power plants, and has solid installation track record of more than 1 GW. The company has a total of 1.7 GW in operation and under construction in Argentina, Brazil, the Czech Republic, Egypt, Honduras, Jordan, Malaysia, Mozambique, Rwanda, South Africa and Ukraine. With an established global presence and a significant project pipeline, the company is targeting a capacity of 3.5 GW in operation and under construction by -

FTSE Publications

2 FTSE Russell Publications FTSE Developed Europe SMID Cap 19 August 2021 Tradable Plus Indicative Index Weight Data as at Closing on 30 June 2021 Index weight Index weight Index weight Constituent Country Constituent Country Constituent Country (%) (%) (%) 3i Group 0.72 UNITED Bureau Veritas S.A. 0.42 FRANCE Gjensidige Forsikring ASA 0.17 NORWAY KINGDOM Campari 0.31 ITALY Gn Store Nordic 0.53 DENMARK AAK 0.18 SWEDEN Carl Zeiss Meditec 0.33 GERMANY Halma 0.66 UNITED Aalberts NV 0.24 NETHERLANDS Castellum 0.32 SWEDEN KINGDOM ABN AMRO Bank NV 0.23 NETHERLANDS Centrica 0.2 UNITED Hargreaves Lansdown 0.39 UNITED Acciona S.A. 0.16 SPAIN KINGDOM KINGDOM Accor 0.32 FRANCE Chr. Hansen Holding A/S 0.43 DENMARK Hays 0.16 UNITED ACS Actividades Cons y Serv 0.3 SPAIN Clariant 0.21 SWITZERLAND KINGDOM Adecco Group AG 0.49 SWITZERLAND Coca-Cola HBC AG 0.33 UNITED HeidelbergCement AG 0.6 GERMANY Adevinta 0.21 NORWAY KINGDOM HelloFresh SE 0.67 GERMANY Admiral Group 0.43 UNITED Cofinimmo 0.21 BELGIUM Helvetia Holding AG 0.18 SWITZERLAND KINGDOM Commerzbank 0.35 GERMANY Hikma Pharmaceuticals 0.27 UNITED Aedifica 0.22 BELGIUM ConvaTec Group 0.25 UNITED KINGDOM Aegon NV 0.34 NETHERLANDS KINGDOM Hiscox 0.18 UNITED KINGDOM Aeroports de Paris 0.17 FRANCE Countryside Properties 0.16 UNITED Holmen AB 0.2 SWEDEN Ageas 0.46 BELGIUM KINGDOM Homeserve 0.17 UNITED Aker BP ASA 0.16 NORWAY Covestro AG 0.54 GERMANY KINGDOM Alfa Laval 0.52 SWEDEN Covivio 0.2 FRANCE Howden Joinery Group 0.3 UNITED Alstom 0.7 FRANCE Croda International 0.64 UNITED KINGDOM KINGDOM Alten 0.18