Richmond Regional Comprehensive Economic Development Strategy

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Nomination Form

••.w=i.==.c ·-~-·--·--'·--~-··--~···-·----~- NPS Fonn 10-900 0MB No. 1024-0018 (Rav, 10-90) \/ Lf - ~ / 1t./ 9"' United States Department of the Interior National Parle Service Nf?.K P- '/ ~ /lf NATIONAL REGISTER OF HISTORIC PLACES REGISTRATION FORM This form is for use in nominating or requesting determinations for individual properties and districls. See instructions in How ID Complel81he National Register of Historic Places Registration Fonn (National Register Bulletin 1SA}. Complete each Item by marking "x" In the appropriate boX or by entering the iul"Olmatlon requested. If.,, 111m does not apply 1D the property being documented, enter "NIA" for •not app;ii:ahle • For func:tlonS. an:hil8Clllr8I clasllllcalkw,, matarials, and areas of signlllc:ance, enter only categcA las and sub allllgooea fnlmlhe inslnlctions. Place addltlonal entries and narrative Items on continuation sheets (NPS Form 1D-900a). U• a typaw,1181, word processor, or computer, to complete all Items. 1. Name ofPropaty historic name ___CBUR.CH HILL NORm HISTORIC DISTRicr/ VDHR m.E No. 127-820_ other names /site number _CHURCH HILL 2. Location- =====.... ==-=... ======= ..... -==m=-===========--==--=======-====== ================ street & number __MllnllaD, Clay, Leip aad M Streem not for publication_ from 10atll to north; 21 St through 30th Streem from West to East aor town_ Richmond vicinity - state Virglllla_ code_VA_ county _(ln~ependentclty) code 7§0 zip code 23223 · ::.... ,=========== ..... ===•===========~=== ~~----~-------===-~-~~---------====== 3. State/Federal Agency Certification 5-=== =-------=---- --===============----====================-----= As the d>lnated authority under the National Historic Preservation Ad. of 1986, as amended, I hereby certify that this nomi i8tlon _ request for determination of eligibility meets the documentation standards for registering prope,1ies In the National Register of Historic Places and meets the procedural and professional requirements set forth in 36 CFR Part 60. -

Virginia ' Shistoricrichmondregi On

VIRGINIA'S HISTORIC RICHMOND REGION GROUPplanner TOUR 1_cover_17gtm.indd 1 10/3/16 9:59 AM Virginia’s Beer Authority and more... CapitalAleHouse.com RichMag_TourGuide_2016.indd 1 10/20/16 9:05 AM VIRGINIA'S HISTORIC RICHMOND REGION GROUP TOURplanner p The Virginia Museum of Fine Arts’ permanent collection consists of more than 35,000 works of art. © Richmond Region 2017 Group Tour Planner. This pub- How to use this planner: lication may not be reproduced Table of Contents in whole or part in any form or This guide offers both inspira- by any means without written tion and information to help permission from the publisher. you plan your Group Tour to Publisher is not responsible for Welcome . 2 errors or omissions. The list- the Richmond region. After ings and advertisements in this Getting Here . 3 learning the basics in our publication do not imply any opening sections, gather ideas endorsement by the publisher or Richmond Region Tourism. Tour Planning . 3 from our listings of events, Printed in Richmond, Va., by sample itineraries, attractions Cadmus Communications, a and more. And before you Cenveo company. Published Out-of-the-Ordinary . 4 for Richmond Region Tourism visit, let us know! by Target Communications Inc. Calendar of Events . 8 Icons you may see ... Art Director - Sarah Lockwood Editor Sample Itineraries. 12 - Nicole Cohen G = Group Pricing Available Cover Photo - Jesse Peters Special Thanks = Student Friendly, Student Programs - Segway of Attractions & Entertainment . 20 Richmond ; = Handicapped Accessible To request information about Attractions Map . 38 I = Interactive Programs advertising, or for any ques- tions or comments, please M = Motorcoach Parking contact Richard Malkman, Shopping . -

General Comments Summary Ii

GENERAL COMMENTS SUMMARY II General Comments This section presents the 27 comments received from the public regarding various aspects of the Draft 2026 Comprehensive Plan since the original General Comments Manual was published in November 2008. These comments have been received through a variety of means including, but not limited to, direct mail, e-mail, and submissions to the County’s website for the Draft 2026 Comprehensive Plan. While later sections of this document present more specific comments regarding the Draft 2026 Future Land Use Plan Map and Draft 2026 Major Thoroughfare Plan Map, the comments in this section are more general and have been organized by magisterial district. In some cases, comments contained specific questions, which warranted an immediate response. Those responses made by staff are shown along with the respective comments. We would like to take this opportunity to express our appreciation to all those who took the time to forward us their comments regarding the various parts of the Draft 2026 Comprehensive Plan. 240 2026 Comprehensive Plan General Comments – Part II – Fairfield Submittal Type: Mail Comment Response Mr. Emerson: Dear Mr. and Mrs. Davidson: We are writing to you about a parcel of property that we currently own, I am responding to your October 9, 2008 letter regarding the which is located at 2104 Cool Lane, Richmond, Virginia 23223. The recommended designation of the Tax Parcel 800-726-1663 in the Draft Tax Parcel I.D. number for this property is 800-726-1663, and it is 2026 Comprehensive Plan. The property is generally located in the zoned R-4, one family residence district. -

1207 School Street Fully Entitled Land Site

1207 SCHOOL STREET RICHMOND, VIRGINIA LAND AREA 4.95 Acres INVESTMENT OFFERING APPROVED UNITS Divaris Real Estate is pleased to present the opportunity to acquire a development site strategically positioned in a rapidly growing area of FULLY ENTITLED LAND SITE 200 Richmond, Virginia. 1207 School Street is conveniently located with- PROPOSED 200-UNIT APARTMENT DEVELOPMENT in walking distance of Virginia Commonwealth University and Virginia ZONING Union University, and is minutes from downtown Richmond. The site B-7 Mixed Use has excellent access from Interstate 64 and Interstate 95. HARRISON HALL 1207 School Street is Fully Zoned and Entitled for up to 200 apartment (804) 814-5299 CELL units. The development is well suited for Market Rate Apartments, [email protected] Student Housing, Work Force Housing or LIHTC Housing. PETER VICK (804) 814-9977 [email protected] Divaris Real Estate Inc. 200 S 10th Street #1010 Richmond, VA 23219 www.divaris.com | (804) 643-4700 1207 SCHOOL STREET 1207 SCHOOL STREET | RICHMOND, VIRGINIA | DIVARIS REAL ESTATE INC. TABLE OF CONTENTS BROAD STREET CORRIDOR AERIALS EXECUTIVE SUMMARY MARKET OVERVIEW MARKET COMPARABLES NEIGHBORING CAMPUSES SITE PLANS 1207 SCHOOL STREET | RICHMOND, VIRGINIA | DIVARIS REAL ESTATE INC. BROAD STREET CORRIDOR AERIAL | 1207 SCHOOL STREET 1207 SCHOOL STREET | RICHMOND, VIRGINIA | DIVARIS REAL ESTATE INC. BROAD STREET CORRIDOR AERIAL | 1207 SCHOOL STREET 1207 SCHOOL STREET | RICHMOND, VIRGINIA | DIVARIS REAL ESTATE INC. EXECUTIVE SUMMARY | 1207 SCHOOL STREET • 1207 School Street is strategically located within walking distance of Virginia Commonwealth University and Virginia Union University. Its frontage on Interstate 95/64 make it a signature site in the City of Richmond. -

VENUE DIRECTORY Maximum Available Outside Caterers Wheelchair ABC License Capacity Venue Space Welcome Access Required

VENUE DIRECTORY Maximum Available Outside Caterers Wheelchair ABC License Capacity Venue Space Welcome Access Required ALTRIA THEATER 6 North Laurel Street - Richmond, VA 23220 850 INDOOR NO YES NO 804-592-3339 - Ad inside front cover AMBER GROVE 16216 Genito Road - Moseley, VA 23120 200 BOTH NO NO YES 804-608-1946 - Ad page 56 THE AMERICAN CIVIL WAR MUSEUM 500 Tredegar Street - Richmond, VA 23219 400 OUTDOOR YES YES YES 804-649-1861 ext. 148 - Ad page 45 APPLE BLOSSOM PLANTATION 6311 S. Courthouse Rd. - Providence Forge, VA 23140 500 BOTH YES YES YES 804-307-3239 - Ad page 92 ART WORKS 320 Hull Street - Richmond, VA 23224 250 INDOOR YES YES YES 804-291-1400 - Ad page 64 ASHTON CREEK VINEYARD & EVENTS 14501 Jefferson Davis Highway - Chester, VA 23831 300 BOTH YES YES NO 804-896-1586 - Ad page 62 THE BARNS OF KANAK 5503 Ruffin Road - Prince George, VA 23875 360 BOTH YES YES YES 804-586-1882 - Ad page 58 THE BERKELEY HOTEL 1200 East Cary Street - Richmond, VA 23219 100 INDOOR NO NO NO 804-225-5141 - Ad page 73 THE BOATHOUSE AT CITY POINT 701 West Randolph Road - Hopewell, VA 23860 150 OUTDOOR YES NO NO 804-616-4222 - Ad page 33 THE BOATHOUSE AT ROCKETTS LANDING 4708 East Old Main Street - Richmond, VA 23231 250 BOTH NO YES NO 804-622-2628 - Ad page 33 THE BOATHOUSE AT SUNDAY PARK 4602 Millridge Parkway - Midlothian, VA 23112 300 BOTH NO YES NO 804-744-2545 - Ad page 33 THE BOLLING HAXALL HOUSE 211 East Franklin Street - Richmond, VA 23219 300 BOTH YES YES YES 804-643-2847 ext. -

Richmond New Construction & Proposed Multifamily Projects 3Q18

Richmond New Construction & Proposed Multifamily Projects 3Q18 ID PROPERTY UNITS 1 Artisan Hill 204 2 Abberly at Centerpointe 271 3 Elan Williamsburg 198 4 South Bank Phase II 55 5 Penstock Quarter 327 54 6 Nexus 268 7 Alta Citizen 222 8 MARQ, The 364 76 23 9 Premier at Town Center 131 72 69 71 52 45 10 Roebuck, The 57 68 73 53 42 35 11 East 51 at Rocketts Landing 156 70 74 39 38 46 12 Rockefeller Phase II, The 60 41 43 13 Colony Village Phase II 166 75 36 14 Shockoe Center 160 5 40 44 Total Lease-Up 2,639 37 15 Belt Atlantic, The 216 22 27 16 1001 East Bryd 237 51 20 47 17 1125 Commerce Road 100 28 26 18 2501 East Main Street 216 16 14 19 700 E 4th Street Development 100 59 65 25 18 21 20 Belvidere, The 129 64 50 49 30 32 4 34 29 21 Current, The 214 33 1 Total Under Construction 1,212 61 19 22 Marshall Lofts 167 2 31 11 23 Canopy at Ginter Park 301 15 17 24 Moore's Lake 200 48 55 25 Winterfield at Midlothian, The 238 58 26 Vida East 178 60 62 27 Herod Seed 163 63 13 28 Locks at 3Twenty-One, The 187 66 24 29 Main & Pear Street 144 116 30 Manchester Development 100 57 56 31 New Manchester 104 113 111 32 Paper Board Company Building 100 115 33 PortRVA Phase II 188 34 Walkers Creek 200 3 35 1500 Roseneath 50 112 36 3013 Cutshaw 100 77 380 East Washington 100 114 117 37 Belvidere, The 129 78 Pecan Acres Estates 50 110 38 Cooperage Phase II, The 55 79 Petersburg Hotel Redevelopment 60 80 South Line at Perry Place 176 81 79 39 Dalian Development 100 77 40 Grace and Stuart 105 81 VSU Chesterfield Avenue 62 78 80 41 Quality Inn & Suites 210 82 -

RICHMOND Accelerating Success

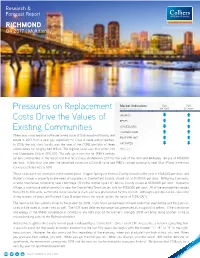

Research & Forecast Report RICHMOND Accelerating success. Q4 2017 | Multifamily Market Indicators RVA RVA Pressures on Replacement Relative to prior period Q4 2017 Q1 2018* Costs Drive the Values of VACANCY RENTS Existing Communities CONCESSIONS TRANSACTIONS There was a marked rise in the perceived value of Richmond multifamily real PRICE PER UNIT estate in 2017 from a year ago, especially for Class B value-add properties. In 2016, the big story locally was the sale of the CORE portfolio of three CAP RATES communities for roughly $81 Million. The highest value was that of the 210 *Projected unit Champions Club at $110,000. The sale set a new bar for 1980’s vintage garden communities in the region but that record was shattered in 2017 by the sale of the 340-unit Wellesley Terrace at $151,000 per door. In less than one year, the perceived values for a Class B value add 1980’s vintage community near Short Pump in Henrico County escalated nearly 50%. Those sales were not anomalies in the market place. Copper Springs in Henrico County closed out the year at $148,000 per door, and Hunter’s Chase, a property in dire need of upgrades, in Chesterfield County, closed out at $131,000 per door. Millspring Commons, a rental townhouse community near Hermitage HS in the northern part of Henrico County closed at $130,000 per door. Huguenot Village, a townhouse rental community near the Chesterfield Town Center, sold for $135,000 per door. All of these properties ranged from 210 to 300 units, so the total dollar volume of each sale was phenomenal for this market. -

Cultural Resource and Current Condition Assessment

REPORT > FULTON GAS WORKS SITE CULTURAL RESOURCE ASSESSMENT AND CURRENT CONDITIONS REPORT DATE > JANUARY 2017 LOCATION > Richmond, Virginia PREPARED FOR > Timmons Group PREPARED BY > Dutton + Associates, LLC Dutton + Associates CULTURAL RESOURCE SURVEY, PLANNING, AND MANAGEMENT FULTON GAS WORKS SITE CULTURAL RESOURCE ASSESSMENT AND CURRENT CONDITIONS REPORT RICHMOND, VIRGINIA PREPARED FOR: TIMMONS GROUP PREPARED BY: DUTTON + ASSOCIATES, LLC 1115 CROWDER DRIVE MIDLOTHIAN, VIRGINIA 23113 PRINCIPAL INVESTIGATOR: DAVID H. DUTTON, M.A. DARA A. FRIEDBERG, M.S. JANUARY 2017 ABSTRACT ABSTRACT The results of the study revealed that the project area was in the vicinity of the earliest settled area of Rocketts Landing. Historic maps and documents indicate that early development would have been consigned primarily to the western portion of the project area. Gillies Creek flowsd south and east of the project area, and at times possibly within it. The tributary Bloody Run, now filled, bisected the project area. Development had occurred in the western portion of the land by the early nineteenth century in form of dwellings and a tobacco factory. Following the incredible success of the City Gas Works on Cary Street between 15th and 16th streets, the City purchased land in Rocketts Landing for the construction of a new plant. The plant began operations in 1856. The Civil War, multiple floods, and changes in manufactured gas technology necessitated multiple repairs and rebuildings of the Gas Works. Changes between the 1920s and 1950s created the more modern layout of the site. What had become known as Fulton Gas Works continued operations until 1972 from which time it has remained vacant. -

Richmond Riverfront Plan Amendment 1: Downriver Update 2017 26 November 2012 2017 Richmond Riverfront Plan

RICHMOND RIVERFRONT PLAN AMENDMENT 1: DOWNRIVER UPDATE 2017 26 NOVEMBER 2012 2017 RICHMOND RIVERFRONT PLAN SECTION 1 / Introduction 5 SECTION 2 / Riverfront Plan 9 SECTION 3 / Riverfront Priorities 101 SECTION 4 / Governance+ Implementation 107 SECTION 5 / Funding+ Maintenance 113 SECTION 6 / Conclusion 125 SECTION 7 / Appendix 1: Analysis 129 SECTION 8 / Appendix 2: Adopting Ordinance 175 SECTION 9 / Amendment 1: Downriver Update 2017 177 SECTION 10 / Appendix 3: Adopting Ordinance 207 CONTENTS Front Cover Image: CPJ Photography PAGE 3 RICHMOND RIVERFRONT PLAN SEE SECTION 9 AMENDMENT 1: DOWNRIVER UPDATE 2017 26 NOVEMBER 2012 DOWNRIVER HISTORY View of Rocketts from Libby Hill as it appeared c. 1800 (published 1896) I VALENTINE RICHMOND HISTORY CENTER The view down the James River from Libby Hill has an uncanny similarity to the upriver view from Richmond Hill at Richmond- GILLIES CREEK Gillies Creek runs through one of the largest creek valleys in the Richmond area. Its confluence with the Upon-Thames, England. Richmond’s founder, William Byrd of Westover, recognized the similarity when establishing and naming James is midway along the lower waterfront. Richmond in 1733. The scene that enraptured Byrd and countless others since is a beautiful arc of the tidewater James. The north shore of this arc is an area historically known as Rocketts, a thriving shipping area in the nineteenth century with wharves ROCKETTS/FULTON Rocketts is the name of a ferry that operated across the river near the mouth of Gillies Creek. The extending for more than half a mile along the river. In the late nineteenth and twentieth centuries, the increasing size and depth wharves that developed along the river in this area became known as Rocketts as well, with the wharves farthest downriver of merchant vessels reduced the number of ships docking at Rocketts, due to the comparatively shallow waters of the port. -

Final Notes Hi

Number 49 Virginia Department of Historic Resources 2005 Number 49 Virginia Department of Historic Resources 2005 Notes from the Director 3 Virginia Landmarks Register Adds 81 New Listings 5 The Lost World of Rocketts Landing 37 By Matt Gottlieb Curator’s Corner: Artifacts from DHR’s Collections: 41 Colonial Pipes of Virginia By Keith Egloff The Sharon Indian School, 1919–1965 43 By Lisa Kroll Forty Years of Preservation: Virginia’s Easement Program 49 By Calder Loth New Preservation Easements Received on 14 Properties 55 65 New Historical Markers for Virginia’s Roadways 59 Update on the Historic Rehabilitation Tax Credit Program 62 Virginia Department of Historic Resources 2801 Kensington Avenue Richmond, Virginia 23221 www.dhr.virginia.gov Kathleen S. Kilpatrick, Director Notes on Virginia is published annually by the Virginia Department of Historic Resources. Editor: Randall B. Jones; Photographic Assistant and Technical Consultant: Zak Billmeier; Designer: Judy Rumble, Virginia Office of Graphic Communications, Department of General Services. All photographs are from the department’s archives, unless otherwise indicated. DHR Department of Historic Resources Central Office: Our Mission 2801 Kensington Avenue Richmond, VA 23221 (804) 367-2323 The Department of Historic Resources’ (804) 367-2391 (fax) Capital Region Office: mission is to foster, encourage, and 2801 Kensington Avenue Richmond, VA 23221 (804) 367-2323, ext. 107 support the stewardship and use of (804) 367-2391 (fax) Virginia’s significant architectural, Roanoke Region Office: 1030 Penmar Avenue SE Roanoke, VA 24013 archaeological, and cultural resources. (540) 857-7585 (540) 857-7588 (fax) Tidewater Region Office: 14415 Old Courthouse Way Newport News, VA 23608 (757) 886-2807 (757) 886-2808 (fax) Winchester Region Office: Virginia Historic Resources Board State Review Board 107 N. -

Architectural Reconnaissance Survey, AMCE and AMFY Segments

ARCHITECTURAL RECONNAISSANCE Rͳ12 SURVEY, AMCE AND AMFY SEGMENTS ΈSEGMENTS 17 AND 19Ή D.C. TO RICHMOND SOUTHEAST HIGH SPEED RAIL October 2016 Architectural Reconnaissance Survey for the Washington, D.C. to Richmond, Virginia High Speed Rail Project AM Jct to Centralia ‐ S Line (AMCE) and AM Jct to Fulton Yard (AMFY) Segments, Chesterfield County and City of Richmond Architectural Reconnaissance Survey for the Washington, D.C. to Richmond, Virginia High Speed Rail Project AM Jct to Centralia - S Line (AMCE) and AM Jct to Fulton Yard (AMFY) Segments, City of Richmond and Chesterfield County by Emily K. Anderson and Heather D. Staton Prepared for Virginia Department of Rail and Public Transportation 600 E. Main Street, Suite 2102 Richmond, Virginia 23219 Prepared by DC2RVA Project Team 801 E. Main Street, Suite 1000 Richmond, Virginia 23219 October 2016 November 15, 2016 Kerri S. Barile, Principal Investigator Date ABSTRACT Dovetail Cultural Resource Group (Dovetail), on behalf of the Virginia Department of Rail and Public Transportation (DRPT), conducted a reconnaissance-level architectural survey of the AM Jct to Centralia - S Line (AMCE) and AM Jct to Fulton Yard (AMFY) segments of the Washington, D.C. to Richmond Southeast High Speed Rail (DC2RVA) project. The proposed Project is being completed under the auspices of the Federal Railroad Administration (FRA) in conjunction with DRPT. Because of FRA’s involvement, the undertaking is required to comply with the National Environmental Policy Act (NEPA) and Section 106 of the National Historic Preservation Act of 1966, as amended. The project is being completed as Virginia Department of Historic Resources (DHR) File Review #2014-0666. -

Environmental Assessment

ENVIRONMENTAL ASSESSMENT APPENDIX B: Agency Correspondence MEETING NOTES Broad Street Bus Rapid Transit (BRT) Study DHR #2010-0219 March 5, 2010 Meeting Attendees: Marc Holma, Virginia Dept of Historic Resources Andrea Kampinen, Virginia Dept of Historic Resources Amy Inman, Virginia Dept of Rail & Public Transportation Anne Darnall, Parsons Kerri Barile, Dovetail Cultural Resource Group A meeting was held on Friday, March 5, 2010 in the Virginia Department of Historic Resources (DHR) conference room in Richmond, Virginia (see attached agenda). The purpose of the meeting, attended by the recipients of this memo, was to present a synopsis of the BRT project, discuss the initial agency coordination steps, receive verbal concurrence on Area of Potential Effect (APE), and set a course of action for future work. Project Summary/Introduction The project involves the creation of a BRT line along 7 miles of Borad Street. Currently the inclusion of a guideway (dedicated bus lanes) for some or all of the 7-mile section between Willow Lawn and Rocketts Landing is being considered as are up to 16 new BRT stations. As the Alternatives Analysis proceeds more information will be developed to determine if a dedicated guideway should be included within the roadway for the buses, where this guideway should be located. Station locations will also be selected and several types of station prototypes will developed based on the size of stations needed and their locations within the corridor (e.g., central business district, neighborhood areas, etc.). As discussed, the Federal Transit Agency (FTA) is the lead federal agency for this project; however, they have appointed the Virginia Department of Rail and Public Transportation (DRPT) and the GRTC Transit System (GRTC) as their local representatives on this work.