Towards a Competitive Setting for the Port of Aqaba in the New Millennium Salah Abu Afifeh World Maritime University

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Curriculum Vitae

Curriculum Vitae Name : Captain: Issa Awad Mahmoud Hasan Nationality : Jordanian Place / Date of Birth : Bait Liqya - 7/3/1957 Graduation: First Graduate as Navigation Officer 1982 - A.M.T.A - Egypt Intermediate Graduate as First Navigation Officer- 1985 - A.M.T.A - Egypt Master Mariner II/2, F.G (JULY/1988), A.M.T.A - Egypt. MBA /2010-2012, Middle East University - (MEU) - Jordan Employment History Present: Aqaba Maritime Education and Training center/ Al Balqa Applied University (BAU) Lecturer / DGM of the Maritime Training Center – AMETC since Dec 2015 – To Present. Previous Employment: ABM, Arab Bridge Maritime Jan 2016- June 2017 / Maritime and shipping consultant and DGM for technical and trading. TEHAMA SHIPPING SERVICES LLC. – DUBAI - UAE. GENERAL MANAGER. Aug- 2013 till Dec.2015. Founder of Tehama Shipping Services Co. /Dubai as Operator of Container Feeder line for the international Container Lines COSCO, APL and other NOVCC lines Between Jebel Ali / UAE and Umm Qasr / Iraq, Ship Port Agent and custom clearance and As Line Agent for COSCON Container Line at Umm Qasr- Iraq. Other main activities: chartering, ship owner, cargo transport, freight forwarding and logistics worldwide, ship port agency. 2000 – 2013 with AA GROUP / JORDAN , Responsibilities and Activities : - Operation & Chartering. - Daily follow up with Own & Charter Vessels. - Voyage Instructions. - Cargo Stowage Plan. - Voyage Summary Report. - On/Off hire Bunker Survey / Cargo hold survey. - Follow up load/discharge operations in different ports World Wide. - Analyzing & Evaluating market situation & Negotiating fixture. - Scrutinizing and finalizing Charter Parties & Booking Notes. - Voyage Estimation, Drawing Laytime Calculations. - Verifying Demurrage/Despatch Claims, Settling Voyage Account. - Issuing Bill of Lading, Coordinating with Principals & concern parties, understanding logistical requirement for Project Cargo’s & Heavy lift’s thereafter Planning, Scheduling, Execution & Monitoring Project related local restrictions, rule & requirements. -

Towards a Green Economy in Jordan

Towards a Green Eco nomy in Jordan A SCOPING STUDY August 2011 Study commissioned by The United Nations Environment Programme In partnership with The Ministry of Environment of Jordan Authored by Envision Consulting Group (EnConsult) Jordan Towards a Green Economy in Jordan ii Contents 1. Executive Summary ...................................................................................................... vii 2. Introduction ....................................................................................................................... 1 2.1 Objective of the Study ................................................................................................... 1 2.2 Green Economy Definition ........................................................................................... 1 2.3 Jordanian Government Commitment to Green Economy .................................... 1 3. Overarching Challenges for the Jordanian Economy............................................ 2 3.1 Unemployment ................................................................................................................. 2 3.2 Energy Security ............................................................................................................... 3 3.3 Resource Endowment and Use ................................................................................... 5 4. Key Sectors Identified for Greening the Economy ................................................. 7 4.1 Energy .................................................................................................................. -

A Critical Conceptualisation of Leadership and Organisational

A Critical Conceptualisation of Leadership And Organisational Change: The Case of Royal Jordanian Airline By Basil Obeidat Director of Studies: Dr Tom Baum Supervisor: Dr Austin Chakaodza 2020 Dedication Dedication My wife and children are dear to me. They have supported my ambition to become a qualified researcher. I am grateful for all their love and support. i | Page Acknowledgements Acknowledgements This research work has been possible with the expert direction and support provided by my Director of Studies Professor Tom Baum. Dr Austin Chakaodza provided the know-how guidance necessary to undertake PhD level research. I am grateful to them both, thank you. I should mention Professor Don Harper and Sheku Fofanah and the PhD Administration team who guided me through all the paperwork. ii | Page Abstract Abstract This present thesis is based on the critical conceptualisation of the leadership and the organisational change. Leadership is an action of the leading group of the people and company. It is a practical skill and research area that encompassing the ability of a person or company to lead other people in, team and firm. The organisational change is about the procedure of changing processes, culture, strategies and technologies of the company. It is a process under which a company make changes in its working methods and aim effectively, investigating the leadership style of the top management executives, including the Chief Executive Officer of Royal Jordanian airline to understand the factors that influence organisational cultural change within the company. There have been few studies of the Middle-Eastern situation that treats organisational cultural change in the development of an organisation in terms of the values of the company. -

Final Report

No. TRANSPORT PLANNING AUTHORITY MINISTRY OF TRANSPORT THE ARAB REPUBLIC OF EGYPT MiNTS – MISR NATIONAL TRANSPORT STUDY THE COMPREHENSIVE STUDY ON THE MASTER PLAN FOR NATIONWIDE TRANSPORT SYSTEM IN THE ARAB REPUBLIC OF EGYPT FINAL REPORT TECHNICAL REPORT 4 MARITIME SECTOR March 2012 JAPAN INTERNATIONAL COOPERATION AGENCY ORIENTAL CONSULTANTS CO., LTD. ALMEC CORPORATION EID KATAHIRA & ENGINEERS INTERNATIONAL JR - 12 039 No. TRANSPORT PLANNING AUTHORITY MINISTRY OF TRANSPORT THE ARAB REPUBLIC OF EGYPT MiNTS – MISR NATIONAL TRANSPORT STUDY THE COMPREHENSIVE STUDY ON THE MASTER PLAN FOR NATIONWIDE TRANSPORT SYSTEM IN THE ARAB REPUBLIC OF EGYPT FINAL REPORT TECHNICAL REPORT 4 MARITIME SECTOR March 2012 JAPAN INTERNATIONAL COOPERATION AGENCY ORIENTAL CONSULTANTS CO., LTD. ALMEC CORPORATION EID KATAHIRA & ENGINEERS INTERNATIONAL JR - 12 039 USD1.00 = EGP5.96 USD1.00 = JPY77.91 (Exchange rate of January 2012) MiNTS: Misr National Transport Study Technical Report 4 TABLE OF CONTENTS Item Page CHAPTER 1: INTRODUCTION.........................................................................................................................1-1 1.1. BACKGROUND...................................................................................................................................1-1 1.2. THE MiNTS FRAMEWORK.................................................................................................................1-1 1.2.1. Study Scope and Objectives.......................................................................................................1-1 -

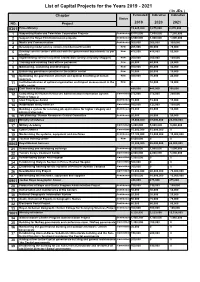

List of Capital Projects for the Years 2019 - 2021 ( in Jds ) Chapter Estimated Indicative Indicative Status NO

List of Capital Projects for the Years 2019 - 2021 ( In JDs ) Chapter Estimated Indicative Indicative Status NO. Project 2019 2020 2021 0301 Prime Ministry 13,625,000 9,875,000 8,870,000 1 Supporting Radio and Television Corporation Projects Continuous 8,515,000 7,650,000 7,250,000 2 Support the Royal Film Commission projects Continuous 3,500,000 1,000,000 1,000,000 3 Media and Communication Continuous 300,000 300,000 300,000 4 Developing model service centers (middle/nourth/south) New 205,000 90,000 70,000 5 Develop service centers affiliated with the government departments as per New 475,000 415,000 50,000 priorities 6 Implementing service recipients satisfaction surveys (mystery shopper) New 200,000 200,000 100,000 7 Training and enabling front offices personnel New 20,000 40,000 20,000 8 Maintaining, sustaining and developing New 100,000 80,000 40,000 9 Enhancing governance practice in the publuc sector New 10,000 20,000 10,000 10 Optimizing the government structure and optimal benefiting of human New 300,000 70,000 20,000 resources 11 Institutionalization of optimal organization and impact measurement in the New 0 10,000 10,000 public sector 0601 Civil Service Bureau 485,000 445,000 395,000 12 Completing the Human Resources Administration Information System Committed 275,000 275,000 250,000 Project/ Stage 2 13 Ideal Employee Award Continuous 15,000 15,000 15,000 14 Automation and E-services Committed 160,000 125,000 100,000 15 Building a system for receiving job applications for higher category and Continuous 15,000 10,000 10,000 administrative jobs. -

The Israel That Arabs Don't Know | the Washington Institute

MENU Policy Analysis / Articles & Op-Eds The Israel That Arabs Don’t Know by Ramy Aziz Mar 15, 2016 Also available in Arabic ABOUT THE AUTHORS Ramy Aziz Dr. Ramy Aziz is a researcher and analyst for the Middle East and international affairs. He is a research fellow at The Institute for the Study of Global Antisemitism and Policy (ISGAP). Articles & Testimony M arch 15, 2016 When the Israeli Ministry of Foreign Affairs invited me to visit Israel as part of a delegation of European-based Arab journalists and media representatives, I accepted without hesitation. The goal of the invitation was to provide us with an opportunity to freely explore the different dimensions to life inside the state of Israel. Located in the heart of the Middle East and one of the region's central and enduring conflicts, Israel receives a large amount of attention from neighboring peoples curious about the state itself and its management. Although major developments in international communication and accessibility of knowledge have transformed the world into a connected community that now sometimes resembles a small village, Arab media coverage of Israel continues to be characterized by a lack of clarity and misrepresentation, making it difficult for Arab citizens to truly understand the country. The persistent and recurring problems in the West Bank and Gaza are of major concern to many Arabs, but media sources often conflate the State's controversial foreign policy with life inside the the country itself and produce dystopian visions of life inside its borders. While not an article or analysis, the following is an honest testimony of what I saw during my visit, without influence by any person or institution. -

Entry Regulations to Jordan

Entry Regulations to Jordan Dear Trade Partners Greetings from Royal Jordanian Airlines. As received from Jordan Civil Aviation Regulatory Commission (JCARC), effective 09th of March 2021 and until 24th of March 2021 midnight, International scheduled flights are allowed to operate from/to Jordanian airports. Accordingly, the following to be applied on inbound flights: • Airlines are responsible to ensure that before boarding each passenger has negative PCR test conducted within 72 hours prior to the departure from the first embarkation airport, health insurance for Non-Jordanians, and install (AMAN Mobile App.). • Military passengers and their families are required to visit https://gateway2jordan.gov.jo to complete the required form and obtain the QR code which is mandatory for boarding • All QR code of passengers obtained before suspending valid • PCR test is required upon arrival, each passenger has to pay 28 JOD via electronic payment as follows: - Queen Alia International Airport – Amman (AMM): - https://registration.questlabjo.com/ - King Hussein International Airport – Aqaba (AQJ): - https://COVID19.biolab.jo - Amman Civil Airport – Marka (ADJ): - The amount will be collected directly in the Lab • Each passenger has to obtain a payment bill to show at check in counter before boarding, passenger who cannot pay through the links, the airline is responsible to collect the amount as EMD. • PCR test is not required for children below 5 years of age. • Diplomats and Employees of Regional and International Organizations (and their dependents -

The Egypt-Palestine/Israel Boundary: 1841-1992

University of Northern Iowa UNI ScholarWorks Dissertations and Theses @ UNI Student Work 1992 The Egypt-Palestine/Israel boundary: 1841-1992 Thabit Abu-Rass University of Northern Iowa Let us know how access to this document benefits ouy Copyright ©1992 Thabit Abu-Rass Follow this and additional works at: https://scholarworks.uni.edu/etd Part of the Human Geography Commons Recommended Citation Abu-Rass, Thabit, "The Egypt-Palestine/Israel boundary: 1841-1992" (1992). Dissertations and Theses @ UNI. 695. https://scholarworks.uni.edu/etd/695 This Open Access Thesis is brought to you for free and open access by the Student Work at UNI ScholarWorks. It has been accepted for inclusion in Dissertations and Theses @ UNI by an authorized administrator of UNI ScholarWorks. For more information, please contact [email protected]. THE EGYPT-PALESTINE/ISRAEL BOUNDARY: 1841-1992 An Abstract of a Thesis .Submitted In Partial Fulfillment of the Requirements for the ~egree Master of Arts Thabit Abu-Rass University of Northern Iowa July 1992 ABSTRACT In 1841, with the involvement of European powers, the Ottoman Empire distinguished by Firman territory subject to a Khedive of Egypt from that subject more directly to Istanbul. With British pressure in 1906, a more formal boundary was established between Egypt and Ottoman Palestine. This study focuses on these events and on the history from 1841 to the present. The study area includes the Sinai peninsula and extends from the Suez Canal in the west to what is today southern Israel from Ashqelon on the Mediterranean to the southern shore of the Dead Sea in the east. -

Anglo-French Relations in Syria: from Entente Cordiale to Sykes-Picot a Thesis Presented to the Faculty of the College of Arts A

Anglo-French Relations in Syria: From Entente Cordiale to Sykes-Picot A thesis presented to the faculty of the College of Arts and Sciences of Ohio University In partial fulfillment of the requirements for the degree Master of Arts James L. Bowman May 2020 © 2020 James L. Bowman. All Rights Reserved. 2 This thesis titled Anglo-French Relations in Syria: From Entente Cordiale to Sykes-Picot by JAMES L. BOWMAN has been approved for the Department of History and the College of Arts and Sciences by Peter John Brobst Associate Professor of History Florenz Plassmann Dean, College of Arts and Sciences 3 Abstract BOWMAN, JAMES L., M.A., May 2020, History Anglo-French Relations in Syria: From Entente Cordiale to Sykes-Picot Director of Thesis: Peter John Brobst Though the Entente Cordiale of 8 April, 1904 addressed several outstanding imperial tensions between the British Empire and the French Third Republic, other imperial disputes remained unresolved in the lead-up to World War I. This thesis explores Anglo-French tensions in Ottoman Syria, from the signing of the Entente to the secret Sykes-Picot Agreement in 1916. Syria proved to be a cause of frictions that brought many buried Anglo-French resentments back to the surface and created new ones. Cultural, strategic, and economic interests were at stake, interests which weighed heavily upon the Entente powers and which could not easily be forgone for the sake of ‘cordiality’. This thesis presents evidence that unresolved Anglo-French tensions in Syria raised serious concerns among officials of both empires as to the larger future of their Entente, and that even after the Entente joined in war against their common enemies, such doubts persisted. -

National Strategy and Action Plan for Sustainable Consumption and Production in Jordan | 2016 - 2025

SCP National Strategy and Action Plan NATIONAL STRATEGY AND ACTION PLAN FOR SUSTAINABLE CONSUMPTION AND PRODUCTION IN JORDAN | 2016 - 2025 SwitchMed Programme is funded by the European Union SwitchMed Programme is funded by the European Union SwitchMed Programme is implemented by the United Nations Industrial Development Organisation (UNIDO) and the United Nations Environment Programme (UNEP), through the Mediterranean Action Plan (MAP) and its Regional Activity Centre for Sustainable Consumption and Production (SCP/RAC) and the Division of Technology, Industry and Economics (DTIE). For details on the SwitchMed Programme please contact [email protected] © Ministry of Environment. 2016 This publication may be reproduced in whole or in part and in any form for educational or non-profit purposes without special permission from the copyright holder, provided acknowledgement of the source is made. UNEP would appreciate receiving a copy of any publication that uses this publication as a source. No use of this publication may be made for resale or for any other commercial purpose whatsoever without prior permission in writing from the Ministry of Environment. Cover photo: www.shutterstock.com General disclaimers The views expressed in this document are those of the authors and do not necessarily reflect the views of the Ministry of Environment, the United Nations Environment Programme and of the European Union. The designations employed and the presentation of material in this document do not imply the expression of any opinion whatsoever on the part of UNEP and the European Union concerning the legal status of any country, territory or city or its authorities, or concerning the delimitation of its frontiers or boundaries. -

Assessment of Urban Mobility Needs, Gaps and Priorities in Mediterranean Partner Countries ‐ Main Findings and the Methodology Implemented in Israel

Assessment of urban mobility needs, gaps and priorities in Mediterranean partner countries ‐ Main findings and the methodology implemented in Israel Ayelet Gal-Tzur, Transportation Research Institute, Technion, Israel Anat Gilad, Municipality of Haifa, Israel This project has received founding from the European Union's FP7 Research And Innovation Programme under grant agreement no. 604714 Ayelet Gal-Tzur, TRI, Technion Anat Gilad, Municipality of Haifa • Information gathering methodology and some conclusions for Israel • The single city perspective - Haifa Ayelet Gal-Tzur, TRI, Technion Anat Gilad, Municipality of Haifa Ayelet Gal-Tzur, TRI, Technion Anat Gilad, Municipality of Haifa Matronit - Haifa BRT General • Exclusive Left lane • 7 cm higher lane • Long platforms Vehicles • Euro 5 • 90 vehicles –(vehicles 6 hybrid) Technologies • Automatic Vehicle Location • Ticketing on platforms • Online passenger Information System • Priority in signalized intersection • Automatic Passenger Count System • 280 Cameras on platforms Ayelet Gal-Tzur, TRI, Technion Anat Gilad, Municipality of Haifa integrated fare system Bike sharing – Not yet but soon Carmelit – Haifa underground Ayelet Gal-Tzur, TRI, Technion Anat Gilad, Municipality of Haifa Department of Transportation Subsidiary company Haifa Municiplity Contractors Public transport operators Other authorities Ayelet Gal-Tzur, TRI, Technion Anat Gilad, Municipality of Haifa Carmel Tunnel Port of Haifa Ayelet Gal-Tzur, TRI, Technion Anat Gilad, Municipality of Haifa Semi structured questionnaire -

Twinning Fiche Project Title: Supporting Civil Aviation

Twinning Fiche Project title: Supporting Civil Aviation Regulatory Commission in the reinforcement of aviation security in Jordan Beneficiary administration: Civil Aviation Regulatory Commission (CARC), The Hashemite Kingdom of Jordan Twinning Reference: JO 17 ENI TR 04 20 Publication notice reference: EuropeAid/170904/ID/ACT/JO EU funded project TWINNING TOOL 1 Table of Contents Acronyms ................................................................................................................................................... 4 1. Basic Information .................................................................................................................................. 6 2. Objectives ............................................................................................................................................... 7 3. Description ......................................................................................................................................... 8 3.1 Background and justification ......................................................................................................... 8 3.2 Ongoing reforms .............................................................................................................................. 9 3.3 Linked activities ............................................................................................................................. 12 3.4 List of applicable Union acquis / Standards / Norms .................................................................