Dear Stockholders

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

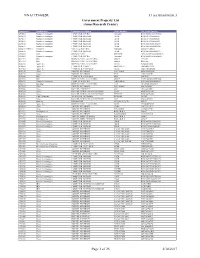

Attachment 3 Page 1 of 25 2/10/2017

NNA17554082R J.1(a) Attachment 3 Government Property List (Ames Research Center) Equipment # Manufacturer Equipment Description Model Number Mfr. Serial Number 2390683 Mazda Technologies COMPUTER, MICRO Tornado6 BTO16021075616500035 1630572 Mazda Technologies COMPUTER, SERVER 1243R BTO812764380800524 1630571 Mazda Technologies COMPUTER, SERVER 1243R BTO812764380800525 1630570 Mazda Technologies COMPUTER, SERVER 1243R BTO812764380800523 2580842 Mazda Technologies COMPUTER, SERVER 1245R BTO1206915856100279 2580841 Mazda Technologies COMPUTER, SERVER 1245R BTO1206915852900278 2580840-VM010 Unknown VIRTUAL MACHINE Unknown 2580840-VM010 2580840 Mazda Technologies COMPUTER, SERVER 1245R BTO1206915852900277 2405303 Seiki DISPLAY UNIT SM40UNP 1SY152700150820D000676 2390684 Mazda Technologies COMPUTER, MICRO Tornado6 BTO16021075616500038 2074375 Dell DISPLAY UNIT, FLAT PANEL 2000FP 1C91004 2074372 Dell DISPLAY UNIT, FLAT PANEL 2000FP IBN105L 3026776 Apple, Inc. DISPLAY UNIT, FLAT PANEL A1316 W82052U56JL 1630634 Apple, Inc. COMPUTER, TABLET MB294LL/A GB024D6NZ3A 1631469 Apple, Inc. COMPUTER, PORTABLE A1286 C02G73HJDRJM 3029439 Cisco SWITCH, ETHERNET WS-C6509E SMG1116N0AB 3029434 Cisco SWITCH, ETHERNET 4948 FOX11040EPE 3028548 Dell COMPUTER, PORTABLE M90 6HJJXB1 3001695 Dell DISPLAY UNIT, FLAT PANEL 2000FP CN09E2494663339F084L 2290190 Mazda Technologies COMPUTER, MICRO TORNADO5 BTO1402986493000010 2104176 Samsung DISPLAY UNIT, FLAT PANEL 181T GH18H4KT602811T 3031474 Cisco SWITCH, ETHERNET WS-C4900M JAE1310544C 3030346 Cisco ROUTER, ETHERNET 2821 -

46 Pt. HP Simplified Bold

TD/HP SMB Express Round Table Innovation at HP Printing & Personal Systems Wim Vandebergen Sales Mgr Belux – SMB Channel – Printing & Personal Systems © Copyright 2013 Hewlett-Packard Development Company, L.P. The information contained herein is subject to change without notice. Before we have a look at the innovations... Did you know ? We have further improved the xls pricelists ? The Product Bulletin tool is back as it was ! The HP xls Computing & Printing Pricelist www.hp.be/pricelists The most used hp sales tool Including Great4Small and HighPerformers line-ups Detailed product techspecs ? (both online & offline) Personal Computing Servers/Storage/Networking NEW : HP Product Bulletin is LIVE again Dowload tool via : www.hp.com/go/qs HP Innovation 5 © Copyright 2012 Hewlett-Packard Development Company, L.P. The information contained herein is subject to change without notice. Leading innovation for more than 75 years 1963 1975 1989 2003 Frequency Standard for Digital data Smart cooling 2012 synthesizer interface bus storage drive Moonshot 1956 1986 2014/15 Oscilloscope 3D graphics 2002 Multi Jet 1972 workstations Rewritable DVD for Fusion 1951 Pocket scientific standard players 2011 High-speed calculator 1986 MagCloud Sprout by frequency counter Commercialized HP 2001 2011 1968 RISC chips 1942 Utility data center 3D Photon Programmable desktop High-reliability voltmeter Engine calculator 1984 1999 2011 Inkjet printer Molecular logic gate StoreOnce 1939 2010 Company founding 1966 ePrint Resistance capacitance audio oscillator Light emitting diode (LED) 1964 1980 2005 Cesium-beam atomic clock Office laser printer 1994 Virus throttle 1980 64-bit architecture 64-channel ultrasound Consumer Computing January 2015 © Copyright 2013 Hewlett-Packard Development Company, L.P. -

Llhiiillhiiiiiillhillhiiii/////I////Jjj///III Ci

llhIIIllhIIIIIIllhIllhIIII/////I////jjJ///III 12025471 Ci fl/ 2011 Annual ort Dear stockholders et how confident in the First me say am future of Hewlett-Packard We have strong leadership from the consumer markets to the commercialthe industrys broadest portfolio unmatched reach and scale and an exceptionally talented and committed workforce look forward to building on this powerFul foundation to maximize the value of HP in the marketplace the of both the structured information that The in review By harnessing power year resides in databases and the unstructured information like video texts and emails that exists in the real world we are well Throughout fiscal 2011 we experienced number of changes positioned to define the future of information management and challenges Third we met our stated outlook for the fourth quarter As An uncertain macroeconomic environment especially in the are focused on consistent management team we very delivering United States and Europe resulted in weak consumer market financial performance and meeting the public goals we set that persisted throughout the year and commercial market that started strong but softened as the year progressed Fourth we developed go-forward plan for the webOS software platform As you may recall we discontinued our webOS device Additionally we faced number of natural disasters including business in August but we retained the highly regarded operating the tsunami in Japan and flooding in Thailand At HP we decided contribute webOS the system We subsequently to to open loined in the -

HP Simple Template

Eligible models HP EOFY Business Bonus Make the most of tax time with this amazing EOFY Business Bonus offer from HP. Get a $50 pre-paid Visa card for every $750 spent on selected HP products. You could receive up to $1,500 in pre-paid Visa cards when you spend up to $22,500*. This offer is valid only on purchases made between 1 May and 30 June, 2014. Final claims must be received by 14 July, 2014. There are more than 1,000 eligible products across the HP commercial business range! Complete list of eligible products below. ProductGroup HPProductNumber HP Product Description LASERJETS CZ195A HP LaserJet Pro 400 M401n Prntr LASERJETS CF274A HP LaserJet Pro 400 M401d Prntr LASERJETS CF278A HP LaserJet Pro 400 M401dn Prntr LASERJETS CF285A HP LaserJet Pro 400 M401dw Prntr LASERJETS CE528A HP LaserJet P3015dn Printer LASERJETS CE529A HP LaserJet P3015x Printer LASERJETS CF147A HP LaserJet Pro 200 Color M251nw Printer LASERJETS CE956A HP LaserJet Pro 400 Color M451nw Printer LASERJETS CE957A HP LaserJet Pro 400 Color M451dn Printer LASERJETS CF081A HP LaserJet Ent 500 Color M551n Prntr LASERJETS CF082A HP LaserJet Ent 500 Color M551dn Prntr LASERJETS CF083A HP LaserJet Ent 500 Color M551xh Prntr March 2014 Eligible models LASERJETS CE538A HP LaserJet M1536dnf MFP Printer LASERJETS CF286A HP LaserJet Pro 400 M425dn MFP Prntr LASERJETS CF288A HP LaserJet Pro 400 M425dw MFP Prntr LASERJETS A8P79A HP Laserjet Pro 500 MFP M521dn LASERJETS A8P80A HP Laserjet Pro 500 MFP M521dw LASERJETS CF144A HP LaserJet Pro 200 M276n Clr MFP Prntr LASERJETS CF145A -

Scaled Drawings on the HP Touchscreen Personal Computer

For HP Field Personnel Worldwide March 15, 1985 I For HP Use Only MARKETING & INTERNATIONAL SECTOR US Field Operations European Operatione Intercontinental Operrtions Major Accounts Marketing Corporate Marketing MIC Marketinrr Information Center FRD Finance idRemarket~ng Ihvision CSD Comouter Suomrt Div~sion SD 1nst;ument S;bport Division CSO Computer Supplies Operation Vol. 10, No. 10 IPO Instrument Prducts Operation CK Carporate PartsCenter TPk4 Third Party Marketing COMPONENTS, MEASUREMENT & DESIGN SYSTEMS SECTOR Microwave & Communications Gmp(MCG) Editor SPC; Stanford Park Division NMC Network Measurements Division Roman Kichorowsky SAD Signal Analysis Division SPK Spokane Division CTC Colorado Telemm Division Copy Editor QTD Queensferry Telecom Division MTD Microwave Technology Division Tracy Wester QMO Queensferry Microwave Operation Electronic Instruments Group (ElG) NJD New Jersey bvision SCD Santa Clara Division Production Editor BID Boeblingen instrument Division YID YHP Instrument Division Darleen Brettes YCD YHP Computer Operation CD lntemated Circuits Division Design ~yatemsGroup (DSG) Circulation FSD Fort Callins Systems Division FEO Fort Callins Engineering Operation Roster Administrator L SC Logic Systems Division LM? Loge Design Operation COL Colorado Springe Division BCD BaeblincenComouter-". Division Lake Steven. Instr~mrntIhv~\~r,n Computer Newsis published biweekly for Hewlett-Packard Lf hbl~n~rnEng~neertng Operatn)n trSG Technical wftwarr Center field personnel to keep you informed of new HP products Component Gmup MSD Microwave Semiconductor Division and services. OED Optoelectronics Division ED Ootical Communication Division SAO Gutheast Asia Operation Please send address changes and subscription requests Corporate Engineering INFORMATION SYSTEMS & NETWORKS SECTOR to Roster Administrator, 49B2, 19320 Pruneridge Ave., lnformation Systems Gmup (ISG) CSV Computer Systems Division Cupertino, CA 95014. -

Publications Core Magazine, 2012 This

2012 COMMEMORATIVE ISSUE C O RE A Publication of 25 Years of the Fellow Awards the Computer The Origins of Timesharing History Museum An Evening with Walter Isaacson Close up of the Amdahl 470V/6 Computer, 1975. The 470V/6 was the Amdahl Corporation’s fi rst product and ran the same software as IBM System/370 computers but cost less and was smaller and faster. Opposite page: Close-up of IBM 305 RAMAC System Diagram B CORE 2012 / HALL OF FELLOWS DEPARTMENTS MUSEUM UPDATES EXPLORE THE COLLECTION 2 4 6 56 60 58 Contributors An Analog Life An Evening with Oral Histories: Donor Profile Recent Artifact Walter Isaacson The Origins of Donations 3 5 61 Timesharing CEO’s Letter Talking to the Future 7 Museum Donors The President @ CHM C O RE 2012 9 SPECIAL SECTION: TWENTY-FIVE YEARS OF FELLOWS 10 12 14 18 The Fellow Awards Fellows at a Glance Visionary Pioneer 25 Years of Fellows It was 25 years ago that the See an overview of our Fellows— Grace Murray Hopper was a The Computer History Museum Museum began its Fellows where they studied and worked unique individual: a woman in a Fellows often have very inter- program. Since that time, the and what they are known for—in man’s world of computers and esting life trajectories, full of Award has been given to over this two-page chart that shows mathematics and an admiral in dramatic turns and unexpected 60 outstanding individuals in 25 years of Fellows history in an the U.S. Naval Reserve. -

ESTTA800156 02/08/2017 in the UNITED STATES PATENT and TRADEMARK OFFICE BEFORE the TRADEMARK TRIAL and APPEAL BOARD Proceeding 9

Trademark Trial and Appeal Board Electronic Filing System. http://estta.uspto.gov ESTTA Tracking number: ESTTA800156 Filing date: 02/08/2017 IN THE UNITED STATES PATENT AND TRADEMARK OFFICE BEFORE THE TRADEMARK TRIAL AND APPEAL BOARD Proceeding 91220591 Party Plaintiff TCT Mobile International Limited Correspondence SUSAN M NATLAND Address KNOBBE MARTENS OLSON & BEAR LLP 2040 MAIN STREET , 14TH FLOOR IRVINE, CA 92614 UNITED STATES [email protected], [email protected] Submission Motion to Amend Pleading/Amended Pleading Filer's Name Jonathan A. Hyman Filer's e-mail [email protected], [email protected] Signature /jhh/ Date 02/08/2017 Attachments TCLC.004M-Opposer's Motion for Leave to Amend Notice of Opp and Motion to Suspend.pdf(1563803 bytes ) TCLC.004M-AmendNoticeofOpposition.pdf(1599537 bytes ) TCLC.004M-NoticeofOppositionExhibits.pdf(2003482 bytes ) EXHIBIT A 2/11/2015 Moving Definition and More from the Free MerriamWebster Dictionary An Encyclopædia Britannica Company Join Us On Dictionary Thesaurus Medical Scrabble Spanish Central moving Games Word of the Day Video Blog: Words at Play My Faves Test Your Dictionary SAVE POPULARITY Vocabulary! move Save this word to your Favorites. If you're logged into Facebook, you're ready to go. 13 ENTRIES FOUND: moving move moving average moving cluster movingcoil movingiron meter moving pictureSponsored Links Advertise Here moving sidewalkKnow Where You Stand moving staircaseMonitor your credit. Manage your future. Equifax Complete™ Premier. fastmovingwww.equifax.com -

Resolution Declaring Property Surplus

Resolution # 2019-032 RESOLUTION DECLARING MISCELLANEOUS PERSONAL PROPERTY SURPLUS WHEREAS the below-described property is no longer necessary, useful or suitable for municipal purposes NOW, THEREFORE, BE IT RESOLVED that the following property be declared surplus and disposed of according to state statutes, including release to insurance company due to total loss: 2019 Annual City Auction AIRPORT – Items on Airport Resolution 2019-03 & 2019-05 HP ELITE DESK 800 System# S1855 2UA41626H9 HP ELITE DESK 800 System# S1856 2UA41626H8 22" HP Computer Monitor 22" Samsung Computer Monitor 15" Gateway Computer Monitor Smart UPS-1500 SUA1500RM2U AS0737232070 Smart UPS-1500 SUA1500RM2U AS0349310734 Smart UPS-1500 SUA1500RM2U Minuteman UPS 3-Ring Binders-Assorted Sizes Assorted Office Desks 2003 Chevrolet Tahoe 1GNEK13V03J246310 Condition: Needs a Transmission Mileage: Unknown-Cluster won't light up Brother Inkjet Printer LC75/LC71 Series MFC-J430W Assorted Interior Doors Slotted Display Wall Boards Assorted Wall Tiles Assorted Floor Tiles Assorted Rolls of Wall Paper Pallet of Stone Lounge Chairs - Used 47" Monitors (Qty 20)-Not working Small Display Cabinets Outdoor Display Lights (Qty 4) AIR QUALITY (708) 1 2002 Dodge Durango VIN #1B8HS38N52F172728 CIVIC CENTER (913) 1993 Ford Ranger – CTY1400 Vin number 1FTCR14U5PTA45398 (does not run) Walk behind mower (does not run) 55 Theater Lights 16 Work Lights Pallet fork with Stinger 1- JITAI Xtreme Scooter (does not run) 19 – Electric Hand Dryers 3 – Display Cabinets 5’ wide x 56” tall 1 – Six Burner -

Buying for Workplace Equality 2016 a Few Ways You Can Help Fight Dear for Equality Every Day: Friends,Take Action for Equality

5 A Guide To Companies, Products And Services That Support Lesbian, Gay, Bisexual And Transgender Workplace Inclusion BUYING FOR WORKPLACE EQUALITY 2016 A FEW WAYS YOU CAN HELP FIGHT DEAR FOR EQUALITY EVERY DAY: FRIENDS,TAKE ACTION FOR EQUALITY Share this information with your friends, family and co-workers. Help them become supporters of workplace equality by factoring the information from this guide into 1 purchasing decisions. Advocate for equality in the work- place. If your company isn’t on this list or you think it can do better, go to www.hrc.org/cei to find out how to 2 engage your employer. Get active about equality. Sign up for newsletters and Action Alerts at 3 www.hrc.org/workplace. 1 The maxim that the customer is always right has never been truer in today’s hyper- connected global market. Consumers can publicly praise or criticize businesses they patronize with the click of a button and influence friends’ and strangers’ purchasing behaviors. Businesses cannot afford to ignore the increasingly savvy and engaged consumer. As consumers, you know that you have a choice. And with this Buying for Workplace Equality guide, providing the most accurate review of a business’s workplace policies toward lesbian, gay, bisexual and transgender employees, we hope that you feel empowered to make those purchasing decisions that are most important to you. This year’s guide includes results from the 2016 Corporate Equality Index, which features 407 businesses that scored a perfect 100 percent. All scores are based on the same set of criteria, rating 40 LGBT-related policies, benefits and corporate practices among the largest US businesses. -

1 Hewlett-Packard Now #2 Supplier 1 of Manufacturing Software Woddwide

For HP Field Personnel Worldwide November 15, 1984 1 Hewlett-Packard Now #2 Supplier 1 of Manufacturing Software Woddwide T"' For HP Use Only MARKETING & INTERNATIONAL SECTOR US Field Operations European Operations Intercontinental Operations Major Accounts Marketing Corporate Marketing MlC Marketing Information Center Vol. 10. No. 2 FRD Systems FinanceIRemarketing Division CSD Computer Support Division ISD Instrument Support Division Editor CSO Computer Supplies Operation Jim Colosi IPO Instrument Products Operation CPC Corporate Parts Center MEASUREMENT. DESIGN &MANUFACTURING SYSTEMS SECTOR Editorial Assistant Microwave & Communications Group Darleen Brettes MCG Microwave & Communications Group SPD Stanford Park Division NMD Network Measurements Division SAD Signal Analysis Division Circulation SPK Spokane Division Roster Administrator (408-864-5621) CTD Colorado Telecammunications Division QTD Queensferry Telecommunications Division Electronic Instruments Group EIG Electronic Instruments Group NJD New Jersey Division Computer Newsis published biweekly for Hewlett-Packard SDC? San Diegn Division field personnel to keep you informed of new HP products SCD Santa Clara Division Bl[l Boeblingen Instrument Division and services. YIC YHP Instrument Division ICD Integrated Circuits Division Design Systems Group Please send address changes and subscription requests DSG Design Systems Group to Roster Administrator, 49B2, Phone 408-864-5621, FSD Fort Collins Systems Division LSD Logic Systems Division or TELNET 1-864-5621. COL Colorado Springs -

HEWLETT-PACKARD COMPANY (Exact Name of Registrant As Specified in Its Charter) Delaware 94-1081436 (State Or Other Jurisdiction of (I.R.S

Meg Whitman President and CEO Dear Stockholders, Fiscal 2012 was the first year in a multi-year journey to turn HP around. We diagnosed the problems facing the company, laid the foundation to fix them, and put in place a plan to restore HP to growth. We know where we need to go, and we are starting to make progress. The Year in Review In the first year of our turnaround effort, we provided a frank assessment of the challenges facing HP, laid out clear strategies at all levels of the corporation, and mapped out our journey to restore HP’s financial performance. Most importantly, we did what we said we would do in fiscal 2012 – we began taking action to bring costs in line with the revenue trajectory of the business and met our full-year non-GAAP earnings per share outlook. We have just completed year one of our journey, and we are already seeing tangible proof that the steps we have taken are working. This includes generating $10.6 billion in cash flow from operations for fiscal $10.6B 2012. HP used that cash to make significant progress in rebuilding our balance sheet – reducing our in cash flow from net debt by $5.6 billion during the year – and returned $2.6 billion to stockholders in the form of share operations for repurchases and dividends. fiscal 2012 Our efforts in fiscal 2012 also included beginning to tackle the structural and execution issues we identified, and building the foundation we need to improve our performance in the face of dynamic market trends and macroeconomic challenges. -

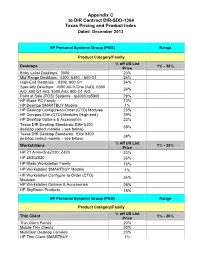

Appendix C to DIR Contract DIR-SDD-1364 Texas Pricing and Product Index Dated: December 2013

Appendix C to DIR Contract DIR-SDD-1364 Texas Pricing and Product Index Dated: December 2013 HP Personal Systems Group (PSG) Range Product Category/Family % off US List Desktops 1% - 38% Price Entry-Level Desktops: 3500 23% Mid-Range Desktops: 4300, 6300, , 600 G1, 26% High-End Desktops : 8300, 800 G1 34% Specialty Desktops: 4300 All-in-One (AiO), 6300 26% AiO, 600 G1 AiO, 8300 AiO, 800 G1 AiO Point of Sale (POS) Systems - rp3000,rp5800 29% HP Blade PC Family 10% HP Desktop SMARTBUY Models 1% HP Desktop Configure-to-Order (CTO) Modules 23% HP Compaq Elite (CTO) Modules (High-end) 29% HP Desktop Options & Accessories 23% Texas DIR Desktop Standards: Elite 6300 38% desktop (select models – see below) Texas DIR Desktop Standards: Elite 8300 38% desktop (select models – see below) % off US List Workstations 1% - 35% Price HP Z1 All-in-OneZ220, Z420 33% HP Z620Z820 35% HP Blade Workstation Family 18% HP Workstation SMARTBUY Models 1% HP Workstation Configure-to-Order (CTO) 34% Modules HP Workstation Options & Accessories 28% HP SkyRoom Products 15% HP Personal Systems Group (PSG) Range Product Category/Family % off US List Thin Client 1% - 20% Price Thin Client Family 20% Mobile Thin Clients 20% MultiSeat Desktop Families 20% HP Thin Client SMARTBUY 1% Appendix C to DIR Contract DIR-SDD-1364 Texas Pricing and Product Index Dated: December 2013 HP Thin Client Configure-to-Order (CTO) 20% Modules HP Thin Client Options & Accessories 20% % off US List Notebook and Tablet PC 1% - 34% Price HP Mini Notebook, HP 19% HP Chromebook 8% HP Slate and