Urban Utilities in Switzerland: Current Situation and Opportunities for the Private Sector

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Education in Switzerland

Education in Switzerland Objekttyp: Group Zeitschrift: The Swiss observer : the journal of the Federation of Swiss Societies in the UK Band (Jahr): - (1981) Heft 1779 PDF erstellt am: 25.09.2021 Nutzungsbedingungen Die ETH-Bibliothek ist Anbieterin der digitalisierten Zeitschriften. Sie besitzt keine Urheberrechte an den Inhalten der Zeitschriften. Die Rechte liegen in der Regel bei den Herausgebern. Die auf der Plattform e-periodica veröffentlichten Dokumente stehen für nicht-kommerzielle Zwecke in Lehre und Forschung sowie für die private Nutzung frei zur Verfügung. Einzelne Dateien oder Ausdrucke aus diesem Angebot können zusammen mit diesen Nutzungsbedingungen und den korrekten Herkunftsbezeichnungen weitergegeben werden. Das Veröffentlichen von Bildern in Print- und Online-Publikationen ist nur mit vorheriger Genehmigung der Rechteinhaber erlaubt. Die systematische Speicherung von Teilen des elektronischen Angebots auf anderen Servern bedarf ebenfalls des schriftlichen Einverständnisses der Rechteinhaber. Haftungsausschluss Alle Angaben erfolgen ohne Gewähr für Vollständigkeit oder Richtigkeit. Es wird keine Haftung übernommen für Schäden durch die Verwendung von Informationen aus diesem Online-Angebot oder durch das Fehlen von Informationen. Dies gilt auch für Inhalte Dritter, die über dieses Angebot zugänglich sind. Ein Dienst der ETH-Bibliothek ETH Zürich, Rämistrasse 101, 8092 Zürich, Schweiz, www.library.ethz.ch http://www.e-periodica.ch Parents, our free EVERY summer young guests other educational institutions. advisory service from all parts of the world come Both traditional and modern AIGLON choose the helps you to to Switzerland to improve their methods of teaching are applied, SWITZERLAND RIGHT SCHOOL knowledge of foreign languages. including the use of language The British International in the All these visitors have a laboratories. -

Ausgabe August/September 2018 Mitteilungsblatt Der Gemeinde Hüttlingen Herausgeber: Gemeindeverwaltung, Schule, Kirche Und Vereine THUR BLICK Gemeindemitteilungen

Ausgabe August/September 2018 Mitteilungsblatt der Gemeinde Hüttlingen Herausgeber: Gemeindeverwaltung, Schule, Kirche und Vereine THUR BLICK Gemeindemitteilungen Mitteilungen des Einwohneramtes Erneuerungswahlen Gemeinderat: Kandidatin oder Kandidat gesucht! Jubilare An der Berchtoldsgemeindeversammlung 2019 wer- 12. August Wüthrich, Ernst, Hüttlingen 86 den die Gesamterneuerungswahlen für den Gemein- 15. August Tanner, Bärbel, Eschikofen 80 derat stattfinden. 22. August Känzig, Elsy, Mettendorf 75 Bis auf Manfred Manser, Ressort Tiefbau und Um- 27. September Gessler, Hans Ulrich, Mettendorf 85 welt, stellen sich alle Bisherigen zur Wiederwahl. 03. September Langone, Raffaele, Eschikofen 80 Gesucht wird nun eine Kandidatin oder ein Kandidat 16. September Wegmüller, Rosa, Hüttlingen 75 für die Wahl in den Gemeinderat. Wir gratulieren den Jubilarinnen und Jubilaren ganz Sind Sie das neue Mitglied im Gemeinderat? herzlich. Wir wünschen Glück und Zufriedenheit, Gesucht wird ein neues Mitglied in den Gemeinderat vor allem aber gute Gesundheit. (Wahl an der Berchtoldsgemeinde 2019). Die wichtigste Voraussetzung ist das Interesse am Todesfälle Wohl unserer Gemeinde. Im Gegenzug bietet Ihnen 23. Mai Wirz, Martin, Hüttlingen das Amt eine interessante und verbindende Aufgabe, 9. Juni Wirz, Dora, Hüttlingen unterstützt von einem kollegialen Team. Wir sind gerne bereit, Sie in einem persönlichen Ge- Wir entbieten den Angehörigen unsere herzliche An- spräch über die zu erwartenden Aufgaben zu infor- teilnahme. mieren und von Ihnen zu erfahren, wo Ihre Interes- sen oder Stärken liegen. Publikation von Zivilstandmitteilungen Melden Sie sich auch, wenn Sie nicht selber kandi- Falls Sie nicht wünschen, dass Sie betreffende Mit- dieren wollen, aber eine ideale Person für ein solches teilungen im Thurblick erscheinen, teilen Sie uns das Amt zu kennen glauben. -

Verzeichnis Der Erfolgreichen Maturandinnen Und Maturanden 2020

Kantonsschule Frauenfeld 30.06.2020 Gymnasiale Maturaprüfungen 2020 Verzeichnis der erfolgreichen Maturandinnen und Maturanden 2020 Klasse Name Vorname Adresse PLZ Ort 4ma Ballabio Leila Oberäuliweg 8 8560 Märstetten Bauer Nils Sonnental 3 8555 Müllheim Dorf Bongartz Clara Klingenbergstrasse 3 8508 Homburg Bosshart Carmen Mühlegraben 4 9542 Münchwilen Gemperli Silvan Dammbühlweg 12 9545 Wängi Gjura Shkurte Talackerstrasse 4 9506 Lommis Harder Anika Hauptstrasse 17 8524 Buch b. Frauenfeld Hascher Léa Oberdorfstrasse 14 8553 Eschikofen Hodel Andrina Südrainstrasse 3 8508 Homburg Hollenstein Layla Rosenbergstrasse 20 8357 Guntershausen Huber Cédric Gachnangerstrasse 5 8500 Gerlikon Mauerhofer Loris Brunnackerstrasse 28 9507 Stettfurt Mauerhofer Raphael Brunnackerstrasse 28 9507 Stettfurt Maurer Leandro Hertenstrasse 24 8500 Frauenfeld Meier Linda Mezikonerstrasse 36 9542 Münchwilen Naegeli Ladina Poststrasse 12 8552 Felben-Wellhausen Rauber Jan Tannhalde 9 9545 Wängi Schleich Sandro Stählibuckstrasse 22 8500 Frauenfeld Stühlinger Florian Sonnenhaldenstrasse 5 8508 Homburg Stutz Alexandra Kirchstrasse 17 8556 Wigoltingen Wicker Talia Betburweg 7 8536 Hüttwilen Wintsch Nicole Keiblenstrasse 2 8356 Ettenhausen TG Wüthrich Roman Saumstrasse 2 9506 Lommis Anzahl 23 Klasse Name Vorname Adresse PLZ Ort 4mb Aliti Blertan Friedauweg 8 8355 Aadorf Biedermann Marvin Speicherstrasse 14c 8500 Frauenfeld Bolli Mario Erlenstrasse 9 8500 Frauenfeld Bundi Fabian Zwinglistrasse 14 8400 Winterthur Durmishi Kreshnik Bändlistrasse 2 8556 Wigoltingen Egloff Anja -

Powering a Modern Switzerland Annual Report 2020 Powering a Modern Switzerland

Powering a modern Switzerland Annual Report 2020 Powering a modern Switzerland Customer-centric, trustworthy, committed Foreword 2 Key events 4 7,054 million 178 million Board of Directors and 6 francs in operating income, francs in Group profit, Executive Management down 1.6 percent year-on-year. down 77 million francs year-on-year. Business results 8 Strategy 14 Markets 24 Logistics Services 26 1,706 million 191 million Communication Services 32 With a fall of 5.6 percent, the Thanks to booming online PostalNetwork 36 volume of addressed letters retail, PostLogistics delivered Mobility Services 40 declined again in 2020. 23 percent more parcels in Switzerland. 1 Swiss Post Solutions 44 PostFinance 46 Employees 50 Public service, society and 56 the environment 124 billion 127 million Five-year overview 63 francs, up by 3.3 percent, PostBus transported of key figures represents the level of average around 24 percent fewer PostFinance customer assets. passengers in 2020 due to the coronavirus pandemic. P 81 points 30% Customer satisfaction is the CO2 efficiency remained at a high level, improvement over 2010 as in the previous year. achieved by Swiss Post by This Annual Report is supplemented by a the end of 2020. separate Financial Report (management report, corporate governance and annual financial statements), comprehensive Business Report key figures and a Global Reporting Initiative Index. Reference documents can be found on page 62. These documents are available in electronic format in the online version of the Business Report 1 For the new definition of parcel volumes, see the Financial Report, page 33. at annualreport.swisspost.ch. -

Objektblatt: V 1

Richtplan Bereich Themengruppe Verkehr Strassenverkehr Objektblatt: V 1 Gegenstand Grundsätze Ausgangslage / Situation – Im Rahmen der Leitbilddiskussionen im Jahr 2002 wurden verkehrsberuhi- gende Massnahmen an den Ortseingängen und den stark frequentierten Kreuzungen sowie der Schutz der Fussgänger und Radfahrer angespro- chen. Ziele – Basierend auf den Ergebnissen der Leitbilddiskussion soll eine Verbesse- rung der Verkehrsführung überprüft werden. Parallel dazu ist eine Verbes- serung der Verkehrssicherheit (insbesondere für Radfahrer und Fussgän- ger) anzustreben. – Für das AMP-Areal ist entsprechend der zukünftigen Nutzung eine geeigne- te Anbindung an das übergeordnete Verkehrsnetz zu untersuchen. Richtplaninhalt – Festlegungen diesbezüglich umfassen die Überprüfung der Signalisation und der Strassenraumgestaltung im Allgemeinen sowie die Verfassung ei- Vororientierung Zwischenergebnis nes Massnahmenkatalogs mit einer entsprechenden Priorisierung. Festsetzung Abhängigkeiten Vergleiche Objektblatt Nr. Dokumentation V1 Strassenverkehr Koordination / Ablauf Beteiligte Stellen intern: Beteiligte Stellen extern: Bauen | Liegenschaften Gemeinderat Andere: ........................... Kanton St. Gallen: ARE TBA Andere:.................. Nachbargemeinden: Bettwiesen Braunau Münchwilen Wil Wuppenau Zuzwil Andere: ............................................. Federführung: Bauen | Liegenschaften Finanzierung Gemeinde: Voranschlag Fr. Investitionsrechnung Fr. Finanzplan Fr. Weitere beteiligte Stellen (Kostenteiler ist festzulegen) Kanton Nachbargemeinden: -

Les Agites Un Projet De Vie À Corseaux

LES AGITES UN PROJET DE VIE À CORSEAUX « SI LE SOLEIL ENTRE DANS LA MAISON, IL EST UN PEU DANS VOTRE COEUR. » Le Corbusier Visuel non contractuel www.lesagites-corseaux.ch EN QUELQUES CHIFFRES LES AGITES 16 APPARTEMENTS 450 MÈTRES DE 1.5 KM DU CENTRE 60 MINUTES DE DE DIVERSES L’ÉCOLE ET DES DE VEVEY BERNE, GENÈVE SUPERFICIES TRANSPORTS ET VERBIER PUBLICS À moins de 20 minutes Immeuble avec un à pied et 8 minutes Accessible en transports parking souterrain Situé au coeur en bus publics et proche de de Corseaux l’autoroute 3 SOMMAIRE CORSEAUX & ENVIRONS 4-5 LE PROJET 6-9 LES LOGEMENTS 10-11 LA PHILOSOPHIE 12-13 LES PROMOTEURS 14 Visuel non contractuel non Visuel LES AGITES CORSEAUX CORSEAUX & ENVIRONS Charmante commune située sur les rives du Lac Léman, Corseaux est un village qui bénéficie d’une situation privilégiée sur la Riviera, réputée pour son microclimat particulièrement doux. Situé entre Lausanne et Montreux, à deux pas de Vevey, le village bénéficie Parcelle des Agites d’un environnement proche pour pratiquer ses loisirs préférés : excursions, sports, activités culturelles, et contemplation. Toute l’année, la région est ponctuée de manifestations interna- tionales comme le Festival de Jazz en juillet, les représentations de théâtre et concerts classiques en hiver ainsi que le Marché de Noël, Tous en Coeur, le Festival du Rire et le fameux Chaplin’s World. Vue sur Corseaux École de Corseaux 4 5 École BERNEBERNE Commerces VEVEY Train / Funiculaire Bus LAUSANNE CORSEAUX MONTREUX GENÈVE VERBIER Corseaux possède un environnement urbain complet avec des services de proximité (école, transports publics et restaurants). -

Directive Sur La Collecte Et Le Traitement Des Déchets 2021

Directive sur la collecte A conserver ! et le traitement des déchets 2021 Mesdames, Messieurs, La présente directive détaille le fonctionnement de Ramassage ECOPOINT Déchèterie Matières Porte-à-porte ddddddddddd intercommunale récupération écologique des déchets urbains auprès des ménages et entreprises des Communes du Cercle de valorisables En Praz Corsier, ceci dans le but d’obtenir une valorisation Libon respectueuse de l’environnement. Chacun peut ainsi contribuer à ménager les ressources en effectuant un tri Commerces spécialisés Corseaux Corsier Jongny Chardonne Corseaux Corsier Jongny Chardonne de qualité. Aluminium et emballages en alu • • • • • • Les lieux, termes et dates importants pour l’élimination des déchets sont énoncés dans ce document. Canettes en alu • • • • • • Les principes généraux de l’élimination des déchets en Capsules de café en alu Suisse sont aussi disponibles sur Internet et à • • • • • l’administration communale. Ferraille • • Un grand merci de votre collaboration. Huiles usagées • • • • • • Piles et accumulateurs au plomb <5kg & Batteries au plomb >5kg • Electronique de bureau et de • loisirs • Adresses importantes : Petits appareils électriques, gros Chardonne Rue du Village 19 021 921 49 24 appareils électroménagers, jouets, • articles de sport • www.chardonne.ch Corseaux Rue du Village 4 021 925 40 11 Verres Triés ou Mélangés • M T M M • • www.corseaux.ch Corsier-sur-Vevey Rue du Château 4 021 925 92 90 Végétaux de jardins privés • • • • • www.corsier-sur-vevey.ch Déchets alimentaires propres (crus Jongny -

Schlussbericht – Einzugsgebiet Limmat Und Reppisch, AWEL 2005

AWEL Amt für Abfall, Wasser, Energie und Luft Einzugsgebiet Limmat und Reppisch Schlussbericht 1 2 Baudirektion des Kantons Zürich, AWEL Amt für Abfall, Wasser, Energie und Luft Massnahmenplan Wasser im Einzugsgebiet Limmat und Reppisch Auftraggeber Baudirektion Kanton Zürich Vertreter des Auftraggebers: Amt für Abfall, Wasser, Energie und Ernst Basler + Partner AG Luft AWEL Zollikerstrasse 65 Walcheplatz 2 8702 Zollikon 8090 Zürich Telefon 044 395 11 11 Telefon 043 259 32 02 Email [email protected] Email [email protected] www.ebp.ch www.awel.ch Projektteam Mitarbeiter Fachgebiete Sennhauser, Werner & Rauch AG Peter Rauch Projektleitung Schöneggstrasse 30 Martin Gutmann Siedlungsentwässerung 8953 Dietikon Sabine Bäni Abwasserreinigung Telefon 044 745 16 16 Wasserqualität Email [email protected] Massnahmenbewertung www.swr.ch ASP Landschaftsarchitekten AG Hans-Ulrich Weber Landschaftsplanung Zürich Peter Stutz Gewässerrevitalisierung Erika Dalle Vedove Landwirtschaft Erholung Planbearbeitung Redaktion Schlussbericht Dr. Heinrich Jäckli AG Dr. Walter Labhart Grundwasser Zürich Wasserqualität Schälchli, Abegg + Hunzinger, Dr. Ueli Schälchli Hochwasserschutz Zürich Gewässerrevitalisierung creato – Netzwerk für kreative Dr. Christian Zimmermann Gewässerökologie Umweltplanung Gewässerrevitalisierung Ennetbaden 30. April 2005 3 Baudirektion des Kantons Zürich, AWEL Amt für Abfall, Wasser, Energie und Luft Massnahmenplan Wasser im Einzugsgebiet Limmat und Reppisch Inhaltsverzeichnis 1 Ausgangslage ....................................................................................................................................... -

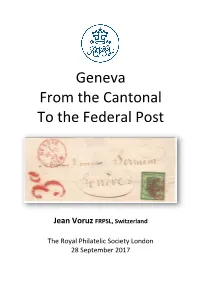

Geneva from the Cantonal to the Federal Post

Geneva From the Cantonal To the Federal Post Jean Voruz FRPSL, Switzerland The Royal Philatelic Society London 28 September 2017 Front cover illustration On 1 st October 1849, the cantonal posts are reorganized and the federal post is created. The Geneva cantonal stamps are still valid, but the rate for local letters is increased from 5 to 7 cents. As the "Large Eagle" with a face value of 5c is sold at the promotional price of 4c, additional 3c is required, materialized here by the old newspapers stamp. One of the two covers being known dated on the First Day of the establishment of the Federal Service. 2 Contents Frames 1 - 2 Cantonal Post Local Mail Frame 2 Cantonal Post Distant Mail Frame 3 Cantonal Post Sardinian & French Mail Frame 4 Transition Period Nearest Cent Frames 4 - 6 Transition Period Other Phases Frame 7 Federal Post Local Mail Frame 8 Federal Post Distant Mail Frames 9 - 10 Federal Post Sardinian & French Mail Background Although I started collecting stamps in 1967 like most of my classmates, I really entered the structured philately in 2005. That year I decided to display a few sheets of Genevan covers at the local philatelic society I joined one year before. Supported by my new friends - especially Henri Grand FRPSL who was one of the very best specialists of Geneva - I went further and got my first FIP Large Gold medal at London 2010 for the postal history collection "Geneva Postal Services". Since then the collection received the FIP Grand Prix International at Philakorea 2014 and the FEPA Grand Prix Finlandia 2017. -

Compte-Rendu De La Seance Du Conseil Intercommunal Du 9 Decembre 2020

Conseil communal COMPTE-RENDU DE LA SEANCE DU CONSEIL INTERCOMMUNAL DU 9 DECEMBRE 2020 2 postes étant à repourvoir au Codir Mme Elvira Rölli, municipale à Arzier-Le Muids a fait acte de candidature. La question a été posée de savoir s’il était opportun de le faire seulement 6 mois avant la fin de la législature. Le Codir n’y voyant pas d’inconvénient, Mme Rölli a été élue . Elle sera ainsi la 2ème femme du Codir sur 9 membres. Budget 2021 La situation financière de la Région de Nyon est assez tendue. Le budget présentait un déficit de chf 59'500.- - . Deux amendements proposés par la Cofin et approuvés par le Codir ont ramené ce déficit à chf. 7'500.- - . Il n’a pas suscité de discussions particulières et a été approuvé à une large majorité. Demande de crédit pour une convention quadriennale en soutien des activités de l’Usine à Gaz, période 2021-2024 Il s’agissait du renouvellement d’une convention existante. Les montants alloués chaque année sont progressifs afin de tenir compte à la fois de la diminution des spectacles en raison du Covid-19 et du fait que les travaux ne sont pas terminés. Un amendement demandant d’augmenter la part de la région (entre chf 70'000.- - et chf 100'000.- -) de chf 20'000.- - a été déposé mais refusé. La convention a par contre été acceptée à une large majorité. Postulat de Michel Girardet pour la mise en place d’une véritable politique de soutien au sport au niveau régional La réponse du Codir était une véritable coquille vide sans aucune proposition concrète. -

A New Challenge for Spatial Planning: Light Pollution in Switzerland

A New Challenge for Spatial Planning: Light Pollution in Switzerland Dr. Liliana Schönberger Contents Abstract .............................................................................................................................. 3 1 Introduction ............................................................................................................. 4 1.1 Light pollution ............................................................................................................. 4 1.1.1 The origins of artificial light ................................................................................ 4 1.1.2 Can light be “pollution”? ...................................................................................... 4 1.1.3 Impacts of light pollution on nature and human health .................................... 6 1.1.4 The efforts to minimize light pollution ............................................................... 7 1.2 Hypotheses .................................................................................................................. 8 2 Methods ................................................................................................................... 9 2.1 Literature review ......................................................................................................... 9 2.2 Spatial analyses ........................................................................................................ 10 3 Results ....................................................................................................................11 -

Kanton Thurgau Im Fokus 2018 3 Inhaltsverzeichnis Der Kanton Thurgau Und Seine Gemeinden

Staatskanzlei Dienststelle für Statistik Kanton Thurgau im Fokus 2018 Statistisches Jahrbuch Inhaltsverzeichnis Der Kanton Thurgau und seine Gemeinden 6 Der Kanton Thurgau und seine Gemeinden 8 Thurgauer Geschichte in Kürze Bevölkerung und Gesellschaft 10 Bevölkerung 15 Religion und Konfession 16 Soziale Sicherheit 19 Gesundheit 22 Bildung 25 Kultur 26 Gemeindeübersicht Wirtschaft und Arbeit Herausgeber Dienststelle für Statistik des Kantons Thurgau, 30 Volkswirtschaft Zürcherstrasse 177, 8510 Frauenfeld, Telefon 058 345 53 60, 32 Branchenstruktur statistik.tg.ch 32 Aussenhandel Zeichenerklärung x Entfällt aus Datenschutzgründen … Zahl unbekannt, weil (noch) nicht erhoben oder (noch) 34 Arbeitsmarkt nicht berechnet 35 Einkommen und Löhne * Entfällt, weil trivial oder Begriff nicht anwendbar 36 Tourismus / Landwirtschaft Bildnachweis Umschlag: Fotolia; Seiten 5, 63: Donald Kaden; Seiten 9, 41: Pixabay; 37 Banken und Versicherungen Seite 29: Shutterstock; Seite 51: Staatskanzlei Thurgau 38 Gemeindeübersicht Bezugsquelle Büromaterial-, Lehrmittel- und Drucksachenzentrale des Kantons Thurgau, bldz.tg.ch, Telefon 058 345 53 70, Artikel-Nr.: 01.042 Bauen und Wohnen Gestaltung Joss & Partner Werbeagentur AG, Weinfelden 42 Bautätigkeit Druckerei Medienwerkstatt AG, Sulgen 44 Bestand und Struktur der Wohngebäude Erscheint jährlich. 46 Mieten und Wohneigentum Ausgabe 2018 47 Leerwohnungsbestand / Siedlungsflächen Mit finanzieller Unterstützung durch die Thurgauer Kantonalbank. 48 Gemeindeübersicht Kanton Thurgau im Fokus 2018 3 Inhaltsverzeichnis