Livre AIRBUS 2017 RD EV.Indb

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

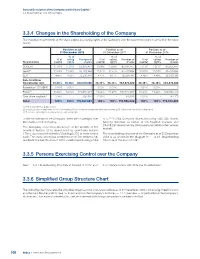

3.3.4 Changes in the Shareholding of the Company

General Description of the Company and its Share Capital / 3.3 Shareholdings and Voting Rights 3.3.4 Changes in the Shareholding of the Company The evolution in ownership of the share capital and voting rights of the Company over the past three years is set forth in the table below: Position as of Position as of Position as of 31 December 2018 31 December 2017 31 December 2016 % of % of % of % of voting Number of % of voting Number of % of voting Number of Shareholders capital rights shares capital rights shares capital rights shares SOGEPA 11.06% 11.06 % 85,835,477 11.08% 11.08% 85,835,477 11.11% 11.11% 85,835,477 GZBV(1) 11.04% 11.04 %85,709,82211.07% 11.07% 85,709,822 11.09% 11.09% 85,709,822 SEPI 4.16% 4.16 %32,330,381 4.17% 4.17% 32,330,381 4.18% 4.18% 32,330,381 Sub-total New Shareholder Agt. 26.26% 26.28% 203,875,680 26.32% 26.33% 203,875,680 26.38% 26.38% 203,875,680 Foundation “SOGEPA” 0.00% 0.00% 0 0.00% 0.00% - 0.00% 0.00% 0 Public(2) 73.66% 73.72% 571,855,277 73.66% 73.67% 570,550,857 73.60% 73.62% 568,853,019 Own share buyback(3) 0.08% - 636,924 0.02% - 129,525 0.02% - 184,170 Total 100% 100% 776,367,881 100% 100% 774,556,062 100% 100% 772,912,869 (1) KfW & other German public entities. -

Livre 1.Indb

European Aeronautic Defence and Space Company EADS N.V. Registration Document 2010 European Aeronautic Defence and Space Company EADS N.V. (the “Company” or “EADS” and together with its subsidiaries, the “Group”) is a Dutch company, which is listed in France, Germany and Spain. The applicable regulations with respect to public information and protection of investors, as well as the commitments made by the Company to securities and market authorities, are described in this registration document (the “Registration Document”). In addition to historical information, this Registration Document includes forward-looking statements. The forward-looking statements are generally identified by the use of forward-looking words, such as “anticipate”, “believe”, “estimate”, “expect”, “intend”, “plan”, “project”, “predict”, “will”, “should”, “may” or other variations of such terms, or by discussion of strategy. These statements relate to EADS’ future prospects, developments and business strategies and are based on analyses or forecasts of future results and estimates of amounts not yet determinable. These forward-looking statements represent the view of EADS only as of the dates they are made, and EADS disclaims any obligation to update forward-looking statements, except as may be otherwise required by law. The forward-looking statements in this Registration Document involve known and unknown risks, uncertainties and other factors that could cause EADS’ actual future results, performance and achievements to differ materially from those forecasted or suggested herein. These include changes in general economic and business conditions, as well as the factors described in “Risk Factors” below. This Registration Document was prepared in accordance with Annex 1 of EC Regulation 809/2004, filed in English with, and approved by, the Autoriteit Financiële Markten (the “AFM”) on 19 April 2011 in its capacity as competent authority under the Wet op het financieel toezicht (as amended) pursuant to Directive 2003/71/EC. -

1.1 Presentation of the Company

Information on the Company’s Activities / 1.1 Presentation of the Company 1.1 Presentation of the Company 1.1.1 Overview Due to the nature of the markets in which the Company operates and the confi dential nature of its businesses, any statements with respect to the Company’s competitive position set out in paragraphs 1.1.1 through 1.1.5 below have been based on the Company’s internal information sources, unless another source has been specifi ed below. With consolidated revenues of € 63.7 billion in 2018, the Company expand the Airbus single-aisle family to cover the 100-150 seat is a global leader in aeronautics, space and related services. segment – and respond to a worldwide market demand for Airbus offers the most comprehensive range of passenger single-aisle jetliners in that segment. airliners. The Company is also a European leader providing tanker, combat, transport and mission aircraft, as well as one of the Despite challenges in the traditional helicopter market, Airbus world’s leading space companies. In helicopters, the Company Helicopters has shown resilient performance, keeping its market provides the most effi cient civil and military rotorcraft solutions leadership in the civil & parapublic segments. worldwide. In 2018, it generated 84.5% of its total revenues in the civil sector (compared to 85% in 2017) and 15.5% in the defence 2. Preserve our leading position in European Defence, Space sector (compared to 15% in 2017). As of 31 December 2018, the and Government markets by focusing on providing military Company’s active headcount was 133,671 employees. -

Airbus Annual Report 2017

ANNUAL REPORT 2017 AIRBUS - Connecting ANNUAL REPORT ANNUAL the skies 2017 Contents /04 /26 Opening Measuring new horizons our results — Interview with the Digital — Interview with Transformation Of cer the Chief Financial Of cer — Launching Skywise – Data in the sky — K e y g u r e s /10 /32 Sharing Delivering our vision our priorities — Letter from the Chairman of the Board — Commercial Aircraft — Board of Directors — Helicopters — Interview with the Chief Executive Of cer — Defence and Space — Executive Committee — Highlights 2017 — Interview with the General Counsel — Share information and the Chief Ethics and Compliance Of cer — Responsibility and Sustainability Registration Document Financial Statements Contents Annual Report 2017 - AIRBUS 001 /04 /26 Airbus is forever innovating, Opening Measuring forever progressing, new horizons our results forever challenging the present — Interview with the Digital — Interview with to be ready for the future. Transformation Of cer the Chief Financial Of cer — Launching Skywise – Data in the sky — K e y g u r e s Airbus aspires to be a digital aerospace champion, connecting software, hardware and customer perspectives for maximum insights and opportunities for growth. Connecting /10 /32 Sharing Delivering the skies our vision our priorities — Letter from the Chairman of the Board — Commercial Aircraft — Board of Directors — Helicopters — Interview with the Chief Executive Of cer — Defence and Space — Executive Committee — Highlights 2017 — Interview with the General Counsel — Share information and the Chief Ethics and Compliance Of cer — Responsibility and Sustainability Registration Document Financial Statements 002 Executive summary Executive summary 002 Executive summary Annual Report 2017 - AIRBUS 003 2017 was a defining year for Airbus, with digitalisation taking an increasingly important role in the Company’s development. -

Aviation Forum Attendees 18/19

Aviation Forum Attendees 18/19 Company Job Function . PMO and MBA Student 14bis Supply Tracking CEO and Co-founder 3D CONTECH GmbH & Co.KG Geschäftsführer 3D ICOM GmbH & Co. KG Vertriebsbeauftragter 3D ICOM GmbH & Co. KG Head of Engineering 3D Systems EVP, General Manager, Metals & Healthcare 3D Systems GmbH Direct Sales Manager Aerospace EMEA 3D Systems GmbH Sales Manager 3D Systems GmbH Direct Sales Manager 3D Systems GmbH Manager Metals Customer Innovation Center Leuven 3D Systems GmbH Direct Sales Manager 3D Printers 3D Systems GmbH Direct Sales Manager 3D.aero GmbH CAO 3D.aero GmbH Marketing Manager AAA GmbH President Aalberts Material Technology GmbH ACA Aerospace Consultancy Associates GmbH Geschäftsführer ACA Aerospace Consultancy Associates GmbH Partner ACA Aerospace Consultancy Associates GmbH Assistenz der Geschäftsführung ACA GmbH Senior Consultant ACA GmbH Partner ACA GmbH Partner ACA GmbH Partner ACA GmbH Partner Accenture Manging Director Accenture GmbH Senior Manager Accenture GmbH Senior Functional Strategy Executive Accenture GmbH A & D Lead Austria, Switzerland, Germany and Russia Accenture GmbH Consulting Manager Accenture Strategy Managing Director ACI Laser GmbH Technischer Vertrieb ACI Laser GmbH Technischer Vertrieb ACstyria Mobilitätscluster GmbH Project Manager Aerospace ACstyria Mobilitätscluster GmbH Head of Aerospace Actrans GmbH Partner Actrans GmbH Senior Consultant Actrans GmbH Partner Actrans GmbH Senior Consultant, Aerospace & Cyber Security Adamet Niemet CEO Adamet Niemet Procurement Specialist Adamet-Niemet -

Participation in Clean Sky 2

Participation in Clean Sky 2 Version [R8] February 2020 In the light of the applicable rules set in the Work Plan 2020-2021 (ref. Chapter “3.3. Call management rules” of the Work Plan 2020-21”), the present document wishes to support applicants interested in the Clean Sky 2 Call for Proposals with their eligibility and admissibility check. The list of Members of Clean Sky 2 is published in accordance with articles 4.3 and 4.5 of Regulation No 558/2014 of 06 May 2014 establishing the Clean Sky 2 Joint Undertaking. Please note the admissibility conditions and eligibility rules applicable to the Calls launched by CS2 JU and as laid down in the General Annexes of the CSJU Work Plan. 1. Leaders and Participating Affiliates # Organization Name Participation Status LPA REG FRC AIR ENG SYS SAT ECO2 TE2 1 Leonardo MW Limited (ex AgustaWestland Limited ) Leader X X 2 Airbus Defence and Space GmbH Leader X X 3 Airbus Defence and Space SAU Leader X X X X 3A Compañía Española de Sistemas Aeronáuticos (CESA) Participating Affiliate X 4 Airbus Operations GmbH Leader X X X 4A Premium Aerotec GmbH Participating Affiliate X 5 AIRBUS OPERATIONS SAS Leader X X X X 5B STELIA AEROSPACE Participating Affiliate X 6 Airbus Helicopters SAS Leader X 6A Airbus Helicopters Deutschland GmbH Leader X X 6B Airbus Helicopters Polska Sp z o.o. Participating Affiliate X 7 Airbus Helicopters España Leader X 8 Airbus Operations Limited Leader X X X 9 Airbus Operations SL Leader X X X 10 Airbus SAS Leader X X X X 11 Dassault Aviation SA Leader X X X 12 Deutsches Zentrum Fuer Luft - Und Raumfahrt Ev - Leader X X X X X DLR 13 Evektor, spol. -

Airbus Group

Defense & Aerospace Companies, Volume II - International Airbus Group Outlook · In March 2015, Airbus Group initiated a second divestment of its shares in Dassault Aviation · Airbus Group is riding the boom in the commercial aircraft market that has fueled a record backlog of EUR857 billion · Airbus D&S is being restructured via mergers and divestments; some 5,000 jobs will be eliminated, primarily in Europe · The company has consolidated its focus in India in hopes of winning upcoming contracts Headquarters Airbus Group SE In mid-2013, following a failed merger attempt with 4, rue du Groupe d'Or BAE Systems, EADS's ownership structure was BP 90112 drastically altered as shareholders changed a Franco- 31703 – Blagnac Cedex, France German ownership pact in favor of greater management Telephone: + 33 0 5 81 31 75 00 freedom. Under the plan, France and Germany now Website: http://www.airbus-group.com hold core stakes of 12 percent each, Spain holds 4 percent, and the rest is floated freely to investors. In 2014, the European Aeronautic Defence and Space Prior to the changes, the triumvirate of nations held over Company (EADS) rebranded itself as Airbus Group, 50 percent of the firm. As part of the changes, France after its largest operation. agreed to give up veto powers over the company's Originally, EADS was formed through Europe's post- industrial policy. Cold War consolidation efforts. At the time of its At the start of 2015, Airbus Group employed about formation in 2000, EADS comprised the activities of the 138,622 people around the world. founding partners Aerospatiale Matra SA of France, Construcciones Aeronáuticas SA (CASA) of Spain, and Note: For details on Airbus Group's major subsidiaries, DaimlerChrysler Aerospace AG (DASA) of Germany. -

Aviation Forum in Hamburg

www.ipm-scm.com III/2015 AVIATION Content In focus: AVIATION FORUM Hamburg 2015 Recent advances in operations research towards Supply Chain Integration Challenges in Commercial efficient airline management Aerospace Konstantin Biel, Technische Universität Darmstadt, Key issues: Challenges and Opportunities for Cabin‘s Jörg M. Ries, City University London Future, Industry 4.0 potentials in configured mass production Collaborative quality management in aerospace Conference information, profiles of speakers and experts, Laurent Martin-Rohmer, SupplyOn AG list of partners, sponsors and exhibitors Competitiveness of French and German Risk Sharing Partnership (RSP) in Aerospace: aerospace suppliers The RSP 2.0 Model Michael Santo, Jochen Schmid, Prof. Dr. Stephan M. Wagner, Stephan Baur, ETH Zürich h&z Unternehmensberatung AG AVIATION FORUM 2015 When the coolant becomes a Liquid Tool. From aviator to aviator: Let us show you how we Ballooning is another passion can lift-off together of the Blaser staff Titanium machining Other Coolant brands Blaser Coolant 0.2 mm) 0.1 (Tool wear (Tool Vb 35 45 80 Cutting Time (min), fz 0.15mm fz: feed rate per tooth Metalworking fluids to optimize productivity, economic efficiency and machining quality. Blaser Swisslube AG 3415 Hasle-Rüegsau Tel. 034 460 01 01 [email protected] www.blaser.com When the coolant becomes a Liquid Tool. Editorial TM AVIATION From aviator to aviator: Let us show you how we Ballooning is another passion can lift-off together of the Blaser staff This SUPPLY CHAIN MANAGEMENT™ issue is published in connection with the 5th AVIATION FORUM Hamburg 2015. The international conference and exhibition has developed into a key platform for Airbus, where we connect with our global suppliers and partners to present and discuss future perspec- tives and directions for the global aerospace industry. -

Financial Statements 2018 Financial Statements

Financial Statements 2018 Financial Statements 02 Airbus / Financial Statements 2018 1 Airbus SE IFRS Consolidated Financial Statements 2 Notes to the IFRS Consolidated Financial Statements 3 Airbus SE IFRS Company Financial Statements 4 Notes to the IFRS Company Financial Statements 5 Other Supplementary Information Including the Independent Auditor’s Report Airbus / Financial Statements 2018 03 Chapter 1 04 Airbus / Financial Statements 2018 1 Airbus SE IFRS Consolidated Financial Statements Airbus SE – IFRS Consolidated Income Statement for the years ended 31 December 2018 and 2017 06 Airbus SE – IFRS Consolidated Statement of Comprehensive Income for the years ended 31 December 2018 and 2017 07 Airbus SE – IFRS Consolidated Statement of Financial Position for the years ended 31 December 2018 and 2017 08 Airbus SE – IFRS Consolidated Statement of Cash Flows for the years ended 31 December 2018 and 2017 10 Airbus SE – IFRS Consolidated Statement of Changes in Equity for the years ended 31 December 2018 and 2017 11 Airbus / Financial Statements 2018 05 Airbus SE – IFRS Consolidated Financial Statements / Airbus SE – IFRS Consolidated Income Statement for the years ended 31 December 2018 and 2017 (I n € million) Note 2018 201 7 Revenue (1) 10 63,707 59,022 Cost of sales (1) (54,920) (52,149) Gross margin (1) 10 8,787 6,873 Selling expenses (861) (872) Administrative expenses (1,574) (1,567) Research and development expenses 11 (3,217) (2,807) Other income 13 1,656 981 Other expenses 13 (182) (336) Share of profit from investments accounted -

Gemeinsame Umwelterklärung 2013 Augsburg · Nordenham · Varel · Bremen

Gemeinsame Umwelterklärung 2013 Augsburg · Nordenham · Varel · Bremen 1 Premium AEROTEC · Gemeinsame Umwelterklärung 2013 Auf einen Blick Technologien für die Zukunft der Luftfahrt Premium AEROTEC ist in der Luft in seinem Element. Das Unternehmen zählt zu den weltweit führenden in der Entwicklung und Herstellung von Strukturen und Fertigungssystemen für den zivilen und militärischen Flugzeugbau. An seinen Standorten Augsburg, Bremen, Nordenham, Varel und Braşov (Rumänien) fertigt Europas führender Luftfahrtzulieferer modernste Flugzeugstrukturen aus Aluminium, Titan und Kohlenstofffaserverbundstoffen für die gesamte Airbus-Familie. Darüber hinaus leistet Premium AEROTEC einen wesentlichen Beitrag zur Entwicklung und Herstellung der A350 XWB. Zudem liefert das Unternehmen Bauteile für die Boeing 787 „Dreamliner”, den Eurofighter sowie die A400M. Auf dem soliden Fundament aus jahrzehntelanger Erfahrung im Flugzeugbau wurde Premium AEROTEC im Jahr 2009 als Zusammenschluss des EADS-Werks in Augsburg und der Airbus-Standorte Nordenham und Varel als eigenständiges Unternehmen gegründet. Mit seiner inno- vativen Schubkraft sichert sich das Unternehmen eine Position an der Weltspitze dieses hochtechnologischen Industriesegments. Um Zukunft effizient mitgestalten zu können, braucht es einzigartige Ideen, die höchsten technischen Fortschritt mit einer optimalen ökologischen und wirtschaftlichen Effizienz in Einklang bringen. Daher arbeitet Premium AEROTEC bei der Neu- und Weiterentwicklung leichter und maximal belastbarer Flugzeugstrukturen beispielsweise eng mit Universitäten, dem Deutschen Zentrum für Luft- und Raum- fahrt (DLR) und der Fraunhofer-Gesellschaft zusammen. Am Standort Augsburg wurde unter anderem die patentierte VAP®-Technologie (Vacuum Assisted Process) entwickelt. Dieses Verfahren ermöglicht es, große CFK-Bauteile, wie zum Beispiel die Druckschotts mit rund 4,5 Meter Durchmesser, für die A350 XWB oder die Boeing 787 in einem Arbeitsgang zu fertigen. -

Competitiveness of the EU Aerospace Industry with Focus On: Aeronautics Industry

FWC Sector Competitiveness Studies - Competitiveness of the EU Aerospace Industry with focus on: Aeronautics Industry Within the Framework Contract of Sectoral Competitiveness Studies – ENTR/06/054 Final Report Client: European Commission, Directorate-General Enterprise & Industry Munich, 15 December 2009 Disclaimer: The views and propositions expressed herein are those of the experts and do not necessar- ily represent any official view of the European Commission or any other organisations mentioned in the Report ECORYS Nederland BV P.O. Box 4175 3006 AD Rotterdam Watermanweg 44 3067 GG Rotterdam The Netherlands T +31 (0)10 453 88 00 F +31 (0)10 453 07 68 E [email protected] W www.ecorys.com Registration no. 24316726 ECORYS Macro & Sector Policies T +31 (0)10 453 87 53 F +31 (0)10 452 36 60 Table of contents 1 Introduction 19 1.1 Previous Work 19 1.2 Particularities of the Industry 20 1.3 Historical Evolution of the Industry 23 1.3.1 Horizontal Evolution of the Industry 23 1.3.2 Vertical Evolution 25 1.4 Business Cycles in the Aerospace Industry 26 2 The Quantitative Analysis of the European Aerospace Industry 31 2.1 The Sectoral Analysis of the European Aerospace Industry 32 2.1.1 The Development and Performance of the Aerospace Industry 33 2.1.2 The Structure of the Industry 36 2.1.3 Performance Comparison to the Total European Economy 37 2.1.4 The Regional Distribution of the European Aerospace Industry 39 2.1.5 The Intra-European Trade Relations of the European Aerospace Industry 46 2.1.6 The Extra-European Trade of the Aerospace -

Livre AIRBUS 2016 RD EV.Indb

Registration Document 2016 WorldReginfo - 8235fdfd-56c1-4f5c-b144-3d65d27a9621 Registration Document Airbus Group SE (the “Company”) is a European p ublic words, such as “anticipate”, “believe”, “estimate”, “expect”, company (Societas Europaea), with its seat in Amsterdam, The “intend”, “plan”, “project”, “predict”, “will”, “should”, “may” or Netherlands, which is listed in France, Germany and Spain. The other variations of such terms, or by discussion of strategy. applicable regulations with respect to public information and These statements relate to the Company’s future prospects, protection of investors, as well as the commitments made by developments and business strategies and are based the Company to securities and market authorities, are described on analyses or forecasts of future results and estimates in this Registration Document (the “Registration Document”). of amounts not yet determinable. These forward-looking In 2017, the Company continues to further integrate by merging statements represent the view of the Company only as of its Group structure with the commercial aircraft activities of the dates they are made, and the Company disclaims any Airbus, with associated restructuring measures. The merger obligation to update forward-looking statements, except is contemplated to take place mid-2017. In this new set-up, as may be otherwise required by law. The forward-looking the Company will retain Airbus Defence and Space and Airbus statements in this Registration Document involve known and Helicopters as Divisions. See “— Information on Airbus Activities unknown risks, uncertainties and other factors that could — 1.1.1 Overview”. cause the Company’s actual future results, performance and In 2016, there are no changes to the segment reporting.