Interim Report 2002 China Southern Airlines Company Limited

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Industrial Reform and Air Transport Development in China

INDUSTRIAL REFORM AND AIR TRANSPORT DEVELOPMENT IN CHINA Anming Zhang Department of Economics University of Victoria Victoria, BC Canada and Visiting Professor, 1996-98 Department of Economics and Finance City University of Hong Kong Hong Kong Occasional Paper #17 November 1997 Table of Contents Abstract ..................................................................... i Acknowledgements ............................................................ i I. INTRODUCTION .........................................................1 II. INDUSTRIAL REFORM ....................................................3 III. REFORMS IN THE AIRLINE INDUSTRY .....................................5 IV. AIR TRANSPORT DEVELOPMENT AND COMPETITION .......................7 A. Air Traffic Growth and Route Development ................................7 B. Market Structure and Route Concentration ................................10 C. Airline Operation and Competition ......................................13 V. CONCLUDING REMARKS ................................................16 References ..................................................................17 List of Tables Table 1: Model Split in Non-Urban Transport in China ................................2 Table 2: Traffic Volume in China's Airline Industry ...................................8 Table 3: Number of City-pair Routes in China's Airline Industry .........................8 Table 4: Overview of Chinese Airline Performance, 1980-94 ............................9 Table 5: Traffic Performed by China's Airlines -

AVIC AG600 "Kunlong"

This production list is presented to you by the editorial team of "Soviet Transports" - current to the beginning of January 2021. Additions and corrections are welcome at [email protected] AVIC AG600 "Kunlong" The AG600 (Jiaolong 600) is a large amphibian powered by four Zhuzhou WJ6 turboprop engines. Development started in 2009 and construction of the prototype in 2014. The first flight took place on 24 December 2017. The aircraft can be used for fire-fighting (it can collect 12 tonnes of water in 20 seconds) and SAR, but also for transport (carrying 50 passengers over up to 5,000 km). The latter capability could give the type strategic value in the South China Sea, which has been subject to various territorial disputes. According to Chinese sources, there were already 17 orders for the type by early 2015. AG600 built by Zhuhai Yanzhou Aircraft Corporation (ZYAC) at Zhuhai from 2016 --- 'B-002A' AG600 AVIC ph. nov20 a full-scale mock-up; in white c/s with dark blue trim and grey belly, titles in Chinese only; displayed in the Jingmen Aviator Town (N30.984289 E112.087750), seen nov20 --- --- AG600 AVIC static test airframe 001 no reg AG600 AVIC r/o 23jul16 the first prototype; production started in 2014, mid-fuselage section completed 29dec14 and nose section completed 17mar15; in primer B-002A AG600 AVIC ZUH 30oct16 in white c/s with dark blue trim and grey belly, titles in Chinese only; f/f 24dec17; f/f from water 20oct18; 172 flights with 308 hours by may20; performed its first landing and take-off on the sea near Qingdao 26jul20 AVIC HO300 The HO300 (Seagull 300) is an amphibian with either four or six seats. -

Chairman's Statement

6 Chairman’s Statement Opportunities from industry-wide restructuring being closely explored to gain benefits of scale China Southern Airlines Company Limited Chairman’s Statement 7 Dear Shareholders: I am pleased to report the Group’s financial and operating results for 2000. Net profit attributable to shareholders was RMB502 million in 2000, representing an increase of 509% as compared with RMB82 million in 1999 notwithstanding the unfavourable operating environment faced by the Group as a result of inflated fuel prices. During 2000, with the Asian economies on their course of recovery, and the PRC economy gradually picking up under a series of positive financial and monetary policies, demand for aviation services was on the rise. Such demand was Yan Zhi Qing particularly keen during holidays, including the Chinese New Chairman of the Board of Directors Year, the Labor Day and the National Day. Amid the improved market environment, the Group experienced increases in load factors and aircraft utilisation rate during Such transactions not only helped expand the Group’s the period. As a result, the passenger revenue increased domestic route network, but also gave a boost to the from RMB11,819 million in 1999 to RMB13,255 million in operation efficiency and market share of the Group in the 2000. However, the Group’s operating profit was reduced area. In future, the Group will continue to explore business as the Group’s operation was under tremendous pressure opportunities arising from the Merger and Restructuring in due to high fuel prices. pursuit of economies of scale. The Group managed to achieve its cost control targets. -

III. Status Quo of Capitalized Operation of China's Exhibition

Annual Report on China's Exhibition Economy (2019) Annual Report on China's Exhibition Economy (2019) Organizer: China Council for the Promotion of International Trade (CCPIT) Publisher Department of Trade and Investment Promotion of China Council for the Promotion of International Trade Academy of China Council for the Promotion of International Trade Chief Editorial Board Director: Zhang Shenfeng Vice Chairman of China Council for the Promotion of International Trade Deputy Director: Feng Yaoxiang Director, Department of Trade and Investment Promotion, CCPIT Ruan Wei Deputy Director, Department of Trade and Investment Promotion, CCPIT Zhou Tong Deputy Inspector, Department of Trade and Investment Promotion, CCPIT Lu Ming Vice Chairman of Academy of China Council for the Promotion of International Trade Executive Editorial Board Director: Zhang Shujing Chief, Exhibition and Conference Division, Department of Trade and Investment Promotion, CCPIT Liu Yingkui Director of Department of International Investment Research, Academy of China Council for the Promotion of International Trade Coordinator:Wang Jianjun, Dun Zhigang Business Support: Department of Trade and Investment Promotion, CCPIT: Zhou Jianxiu, Zhu Yingmin, Zhang Bo, Cao Yongping, Duan Jianrong, Fang Ke, Yuan Fang, Wang Jianjun, Liu Yujia Academy of China Council for the Promotion of International Trade: Liu Yingkui, Wan Xiaoguang, Dun Zhigang, Li Yuan, Wu Wenjun Information Department of China International Exhibition Center Group Corporation: Yuan Hang, Zhang Xi, Zhang Qian -

Frontier Politics and Sino-Soviet Relations: a Study of Northwestern Xinjiang, 1949-1963

University of Pennsylvania ScholarlyCommons Publicly Accessible Penn Dissertations 2017 Frontier Politics And Sino-Soviet Relations: A Study Of Northwestern Xinjiang, 1949-1963 Sheng Mao University of Pennsylvania, [email protected] Follow this and additional works at: https://repository.upenn.edu/edissertations Part of the History Commons Recommended Citation Mao, Sheng, "Frontier Politics And Sino-Soviet Relations: A Study Of Northwestern Xinjiang, 1949-1963" (2017). Publicly Accessible Penn Dissertations. 2459. https://repository.upenn.edu/edissertations/2459 This paper is posted at ScholarlyCommons. https://repository.upenn.edu/edissertations/2459 For more information, please contact [email protected]. Frontier Politics And Sino-Soviet Relations: A Study Of Northwestern Xinjiang, 1949-1963 Abstract This is an ethnopolitical and diplomatic study of the Three Districts, or the former East Turkestan Republic, in China’s northwest frontier in the 1950s and 1960s. It describes how this Muslim borderland between Central Asia and China became today’s Yili Kazakh Autonomous Prefecture under the Xinjiang Uyghur Autonomous Region. The Three Districts had been in the Soviet sphere of influence since the 1930s and remained so even after the Chinese Communist takeover in October 1949. After the Sino- Soviet split in the late 1950s, Beijing transformed a fragile suzerainty into full sovereignty over this region: the transitional population in Xinjiang was demarcated, border defenses were established, and Soviet consulates were forced to withdraw. As a result, the Three Districts changed from a Soviet frontier to a Chinese one, and Xinjiang’s outward focus moved from Soviet Central Asia to China proper. The largely peaceful integration of Xinjiang into PRC China stands in stark contrast to what occurred in Outer Mongolia and Tibet. -

China's Airline Deregulation Since 1997 and the Driving Forces Behind

CORE Metadata, citation and similar papers at core.ac.uk Provided by University of Southern Queensland ePrints China’s airline deregulation since 1997 and the driving forces behind the 2002 airline consolidations Yahua Zhanga,*, David K. Rounda aCentre for Regulation and Market Analysis, School of Commerce, University of South Australia, Adelaide, SA 5000, Australia *Corresponding author. E-mail address: [email protected] Phone: +61 8 830 20601 Fax: +61 8 830 27001 Abstract: This paper seeks to document and describe events in the last decade in China’s airline markets, and to clarify some misunderstandings in regard to the 2002 airline consolidations that brought sweeping changes to China’s aviation markets. Some possible reasons for the 2002 consolidations are inferred through analysing the numbers and facts of the late 1990s and early 2000s. We conclude that the consolidations may be a natural response to the changes that accompanied airline deregulation in China. Keywords: Deregulation, airline mergers, China 1. Introduction China’s airline markets have attracted the attention of many major international carriers, but have largely failed to attract the attention of academics. Literature on China’s airline markets remains relatively sparse, owing to the country’s opacity in aviation policies and the limitations of data availability. The dramatic changes that took place in China’s airline industry in the past 20 years, from a period of strict regulation and control to being relatively uncontrolled and loosely supervised, resulted in chaotic and unexpected outcomes. Those within the industry had two opposing attitudes towards these changes: some applauded them and called for further reforms, while others resisted and demanded a return to regulation. -

China Data Supplement January 2007

China Data Supplement January 2007 J People’s Republic of China J Hong Kong SAR J Macau SAR J Taiwan ISSN 0943-7533 China aktuell Data Supplement – PRC, Hong Kong SAR, Macau SAR, Taiwan 1 Contents The Main National Leadership of the PRC 2 LIU Jen-Kai The Main Provincial Leadership of the PRC 30 LIU Jen-Kai Data on Changes in PRC Main Leadership 37 LIU Jen-Kai PRC Agreements with Foreign Countries 55 LIU Jen-Kai PRC Laws and Regulations 57 LIU Jen-Kai Hong Kong SAR 62 Political, Social and Economic Data LIU Jen-Kai Macau SAR 69 Political, Social and Economic Data LIU Jen-Kai Taiwan 73 Political, Social and Economic Data LIU Jen-Kai ISSN 0943-7533 All information given here is derived from generally accessible sources. Publisher/Distributor: GIGA Institute of Asian Studies Rothenbaumchaussee 32 20148 Hamburg Germany Phone: +49 (0 40) 42 88 74-0 Fax: +49 (040) 4107945 2 January 2007 The Main National Leadership of the PRC LIU Jen-Kai Abbreviations and Explanatory Notes CCP CC Chinese Communist Party Central Committee CCa Central Committee, alternate member CCm Central Committee, member CCSm Central Committee Secretariat, member PBa Politburo, alternate member PBm Politburo, member BoD Board of Directors Cdr. Commander CEO Chief Executive Officer Chp. Chairperson COO Chief Operating Officer CPPCC Chinese People’s Political Consultative Conference CYL Communist Youth League Dep.Cdr. Deputy Commander Dep. P.C. Deputy Political Commissar Dir. Director exec. executive f female Gen.Man. General Manager Hon.Chp. Honorary Chairperson Hon.V.-Chp. Honorary Vice-Chairperson MPC Municipal People’s Congress NPC National People’s Congress PCC Political Consultative Conference PLA People’s Liberation Army Pol.Com. -

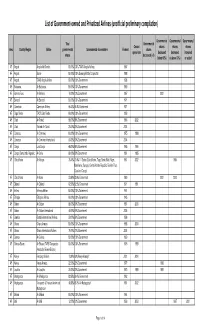

List of Government-Owned and Privatized Airlines (Unofficial Preliminary Compilation)

List of Government-owned and Privatized Airlines (unofficial preliminary compilation) Governmental Governmental Governmental Total Governmental Ceased shares shares shares Area Country/Region Airline governmental Governmental shareholders Formed shares operations decreased decreased increased shares decreased (=0) (below 50%) (=/above 50%) or added AF Angola Angola Air Charter 100.00% 100% TAAG Angola Airlines 1987 AF Angola Sonair 100.00% 100% Sonangol State Corporation 1998 AF Angola TAAG Angola Airlines 100.00% 100% Government 1938 AF Botswana Air Botswana 100.00% 100% Government 1969 AF Burkina Faso Air Burkina 10.00% 10% Government 1967 2001 AF Burundi Air Burundi 100.00% 100% Government 1971 AF Cameroon Cameroon Airlines 96.43% 96.4% Government 1971 AF Cape Verde TACV Cabo Verde 100.00% 100% Government 1958 AF Chad Air Tchad 98.00% 98% Government 1966 2002 AF Chad Toumai Air Tchad 25.00% 25% Government 2004 AF Comoros Air Comores 100.00% 100% Government 1975 1998 AF Comoros Air Comores International 60.00% 60% Government 2004 AF Congo Lina Congo 66.00% 66% Government 1965 1999 AF Congo, Democratic Republic Air Zaire 80.00% 80% Government 1961 1995 AF Cofôte d'Ivoire Air Afrique 70.40% 70.4% 11 States (Cote d'Ivoire, Togo, Benin, Mali, Niger, 1961 2002 1994 Mauritania, Senegal, Central African Republic, Burkino Faso, Chad and Congo) AF Côte d'Ivoire Air Ivoire 23.60% 23.6% Government 1960 2001 2000 AF Djibouti Air Djibouti 62.50% 62.5% Government 1971 1991 AF Eritrea Eritrean Airlines 100.00% 100% Government 1991 AF Ethiopia Ethiopian -

Report of the Directors 21

Report of the Directors 21 Very Substantial Acquisition On 3 October, 2001 the Company entered into an agreement with the Boeing Company for acquiring twenty Boeing 737- 800 aircraft and two Boeing 747-400 freighters during the The Board of Directors of the Company hereby presents period between 2002 and 2005 (the “Transactions”). The this report and the audited consolidated financial statements aggregate consideration in the Transactions exceeds 100% of the Group for the year ended 31 December, 2001. of the net tangible assets of the Company as published in its annual report dated 31 December, 2000 and constitutes very substantial transactions under the Rules Governing the Principal Activities, Operating Results and Listing of Securities on the Stock Exchange of Hong Kong Financial Position Limited (the “Listing Rules”). The PRC government and SA The Group is principally engaged in airline operations and Group, the 65.2% controlling shareholder of the Company, related activities including aircraft maintenance and air have approved the Transactions. SA Group does not have catering operations. The Group is one of the largest airlines any interest in the Transactions other than as a shareholder in China. In 2001, the Group ranked first among all Chinese of the Company. airlines in terms of passenger traffic volume, number of scheduled flights per week, number of hours flown, number The twenty Boeing 737-800 aircraft acquired pursuant to of routes and size of aircraft fleet. The Group has prepared the Transactions will replace twenty existing Boeing 737 the results of operations for the year ended 31 December, series aircraft that the Company currently operates under 2001, and the financial position of the Company and the operating leases. -

China's Growing Market for Large Civil Aircraft

ID-18 OFFICE OF INDUSTRIES WORKING PAPER U.S. International Trade Commission China’s Growing Market for Large Civil Aircraft Peder Andersen Office of Industries U.S. International Trade Commission February 2008 The author is with the Office of Industries of the U.S. International Trade Commission. Office of Industries working papers are the result of the ongoing professional research of USITC staff and solely represent the opinions and professional research of individual authors. These papers do not necessarily represent the views of the U.S. International Trade Commission or any of its individual Commissioners. Working papers are circulated to promote the active exchange of ideas between USITC staff and recognized experts outside the USITC, and to promote professional development of office staff by encouraging outside professional critique of staff research. ADDRESS CORRESPONDENCE TO: OFFICE OF INDUSTRIES U.S. INTERNATIONAL TRADE COMMISSION WASHINGTON, DC 20436 USA Abstract China will likely become the largest market in the world for new large civil aircraft (LCA), with global LCA manufacturers expecting to sell 100 LCA per year in the Chinese market for the next twenty years, or one every three to four days, at a total value ranging up to $350 billion. The challenge for western LCA producers in meeting this demand comes less from each other than from the regulation of China’s market by its government, the lack of adequate air transport infrastructure to serve its population, and China’s nascent attempt at building its own LCA. Should China continue to aggressively address governmental and infrastructure restraints, it will benefit through increased trade and tourism, both of which will spur LCA sales to satisfy air transport demand. -

序号 航协代码 公司名称 1 2018/11/5 2 2018/11/7 3 2018/11/8 4

序号 航协代码 公司名称 到账日期 1 08000086 WUXI BESTWAY AIR TRANSPORT 2018/11/5 2 08000134 SHAANXI FLY AIR TRAVEL SERVICE 2018/11/7 3 08000300 GUANGZHOU LUTAO INTERNATIONAL 2018/11/8 4 08010262 BEIJING XINGZHONGBIN AIR AGENC 2018/11/5 5 08010564 GUILIN GUIKANG TICKETS CO LTD 2018/11/8 6 08010704 CIXI XUNDA AIR TICKETS CO., LT 2018/11/5 7 08011290 FUZHOU JINYUN HANGKONG HANGYUN 2018/11/9 8 08011824 BEIJING ZHAORI AVIATION SERVIC 2018/11/8 9 08012336 HANDAN NEW CENTURY AIR TICKET 2018/11/6 10 08012572 GUANGZHOU JIAOYIHUI INTL TRAVE 2018/11/6 11 08013062 HAINAN HAICHENG AIR TOUR SERVI 2018/11/7 12 08013375 DALIAN E & T DEVELOPMENT 2018/11/6 13 08013386 NANJING SOUTHERN AVIATION TRAV 2018/11/6 14 08013563 TAIYUAN TIANCHENG AIR SERVICE 2018/11/5 15 08013596 GANSU JINQIAO AIR SERVICE 2018/11/9 16 08013600 SHENYANG YUNTONG AIR SERVICE 2018/11/8 17 08013611 YIWU LANTIAN AVATION SERVICE C 2018/11/7 18 08013736 ZHONGSHAN JIAOTONG YUNSHU 2018/10/31 19 08014005 SHENYANG ZHANQIAN AIR SERVICE 2018/11/8 20 08014296 JILIN XINYUAN AIR SERVICE 2018/11/7 21 08014904 JILIN TONGHUA AIR SERVICE CENT 2018/10/31 22 08014996 YICHANG JINXIN JINGMAO CO. LTD 2018/10/31 23 08015044 FUZHOU KANGNA TRAVEL SERVICE C 2018/11/1 24 08015195 BEIJING TIANMA XIANGYUN AIR 2018/11/7 25 08015280 YUANXIANG(FUZHOU) INT'L 2018/11/12 26 08015302 BEIJING WENGUANGWEIYE AIR 2018/11/6 27 08015405 BEIJING CITY PLAZA AIR SERVICE 2018/11/1 28 08015906 BEIJING DIKUANG HONGYU AIR 2018/11/5 29 08016330 BEIJING JINHONGDA AIR TICKETIN 2018/11/9 30 08016422 BEIJING LANYING AIR SERVICE 2018/11/8 31 08016702 BEIJING BAIHUAHANG AIR SERVICE 2018/11/2 32 08016724 BEIJING BAOLIDA AIR TRAVEL 2018/11/2 33 08017310 YUNCHENG HANGLV 2018/11/7 34 08017391 HAIKOU JINXINCHANG AIR AGENCY 2018/11/6 35 08017715 NANCHANG AIR TOUR SERVICE CO. -

2016 Annual Report CONTENTS

(Incorporated in the Cayman Islands with limited liability) Stock Code: 691 2016 Annual Report CONTENTS (I) Definitions 2 (II) Corporate Information 4 (III) Financial and Business Data Summary 8 (IV) Corporate Profile 10 (V) Management Discussion and Analysis 27 (VI) Report of the Directors 45 (VII) Share Capital and Shareholdings of Substantial Shareholders 48 and the Directors (VIII) Basic Information on Directors, Senior Management and Employees 54 (IX) Report on Corporate Governance 65 (X) Major Events 80 (XI) Independent Auditor’s Report 94 (XII) Financial Statements 101 China Shanshui Cement Group Limited • Annual Report 2016 1 (I) Definitions In this annual report, unless the context otherwise requires, the following words and expressions have the following meanings: “Company” or “China Shanshui” or China Shanshui Cement Group Limited “Shanshui Cement” “Group” or “China Shanshui Group” the Company and its subsidiaries “Reporting Period” the period from 1 January 2016 to 31 December 2016 “Board” the Board of Directors of the Company “Director(s)” the Directors of the Company “China Shanshui (HK)” China Shanshui Cement Group (Hong Kong) Company Limited “Pioneer Cement” China Pioneer Cement (Hong Kong) Company Limited “Continental Cement” Continental Cement Corporation “American Shanshui” American Shanshui Development Inc. “Shandong Shanshui” Shandong Shanshui Cement Group Company Limited “ ACC” Asia Cement Corporation “CNBM” China National Building Material Company Limited “CSI” China Shanshui Investment Company Limited “Tianrui