List of Execution Venues Is Not Exhaustive and Subject to Change As Described in the Execution Policy

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Margin Requirements Across Equity-Related Instruments: How Level Is the Playing Field?

Fortune pgs 31-50 1/6/04 8:21 PM Page 31 Margin Requirements Across Equity-Related Instruments: How Level Is the Playing Field? hen interest rates rose sharply in 1994, a number of derivatives- related failures occurred, prominent among them the bankrupt- cy of Orange County, California, which had invested heavily in W 1 structured notes called “inverse floaters.” These events led to vigorous public discussion about the links between derivative securities and finan- cial stability, as well as about the potential role of new regulation. In an effort to clarify the issues, the Federal Reserve Bank of Boston sponsored an educational forum in which the risks and risk management of deriva- tive securities were discussed by a range of interested parties: academics; lawmakers and regulators; experts from nonfinancial corporations, investment and commercial banks, and pension funds; and issuers of securities. The Bank published a summary of the presentations in Minehan and Simons (1995). In the keynote address, Harvard Business School Professor Jay Light noted that there are at least 11 ways that investors can participate in the returns on the Standard and Poor’s 500 composite index (see Box 1). Professor Light pointed out that these alternatives exist because they dif- Peter Fortune fer in a variety of important respects: Some carry higher transaction costs; others might have higher margin requirements; still others might differ in tax treatment or in regulatory restraints. The author is Senior Economist and The purpose of the present study is to assess one dimension of those Advisor to the Director of Research at differences—margin requirements. -

Morning Briefing Global Economic Trading Calendar

A Eurex publication focused on European financial markets, produced by MNl Morning Briefing March 12h 2015 Thursday sees a full day of data, with Council Member KlaasKnot speaks and be up 0.4%also excluding the German and French final inflation in Amsterdam. gasoline station sales. numbers the early feature. EMU data at 1000GMT sees the The US January business At 0700GMT, the German final January industrial output numbers inventories data will cross the wires February harmonised inflation data cross the wires. at 1400GMT. will be published. to be followed by the French numbers at 0745GMT Across the Atlantic, the calendar gets The value of business inventories is and the Spanish data at 0800GMT. underway at 1230GMT, with the expected to fall 0.2% in January after release of the February retail sales, small gains in recent months. ECB Executive Board Member February import/export index and the Benoit Coeure will deliver a speech jobless claims data for the March 7 Late data sees the US February on the future of euro area week. Treasury Statement set for release at investment, quantitative easing, and 1800GMT and Greek debt, in Paris, starting The level of initial jobless claims is at0745GMT. expected to fall by 12,000 to 308,000 the M2 money supply data for the in the March 7 week after rising by Mar 2 week at 2030GMT. Then, at 0915GMT, ECB Governing 7,000 in the previous week. The four- Council Member Jens Weidmann will week moving average rose by The U.S. Treasury is expected to hold a press conference, in 10,250 to 304,750 in the February 28 post a $188.5 billion budget deficit Frankfurt. -

Market Data Services New York Board of Trade (NYBOT)

Prepared Statement of Jack Sabo Vice President – Market Data Services New York Board of Trade (NYBOT) Before the Senate Subcommittee on Federal Financial Management, Government Information, and International Security Field Hearing on “Ensuring Protection of American Intellectual Property Rights for American Industries in China.” November 21, 2005 Chairman Coburn, I appreciate the opportunity to appear before you today to discuss the challenges faced by the U.S. financial community – and, in particular, the New York Board of Trade -- due to piracy of real time market data in China. While the issue of piracy in China is often dominated by high profile industries such as motion pictures, recordings, software and publishing, Chinese piracy also affects the financial industry by robbing exchanges of fees from the sale of market data and by robbing customers from licensed market data vendors, such as Bloomberg, e-Signal, and others. Market data provided by derivative exchanges is vital information used by the global financial industry which includes brokerage houses, banks, fund managers, cotton, coffee, sugar, cattle, corn, orange juice brokers, and many more. They depend on reliable information, whose integrity can be undermined through unauthorized access and piracy of this data. Revenue from market data fees can be as much as 25% of total exchange revenue. As New York’s original futures exchange, the New York Board of Trade (commonly referred to as “NYBOT”) is an historic part of the financial community. It is a traditional futures exchange where traders buy and sell futures on Coffee, Sugar, Cocoa, Cotton, Orange Juice, wood pulp and a variety of financial instruments such as the US Dollar Index. -

Mao Indictment

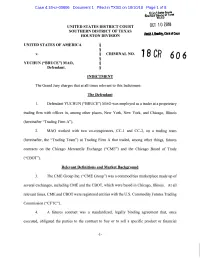

Case 4:18-cr-00606 Document 1 Filed in TXSD on 10/10/18 Page 1 of 8 UNITED STATES DISTRICT COURT OCT 1 0 2018 SOUTHERN DISTRICT OF TEXAS HOUSTON DIVISION UNITED STATES OF AMERICA § § v. § CRIMINAL NO. § 18 CR 60 6 YUCHUN ("BRUCE") MAO, § Defendant. § INDICTMENT The Grand Jury charges that at all times relevant to this Indictment: The Defendant 1. Defendant YUCHUN ("BRUCE") MAO was employed as a trader at a proprietary trading firm with offices in, among other places, New York, New York, and Chicago, Illinois (hereinafter "Trading Firm A"). 2. MAO worked with two co-conspirators, CC-1 and CC-2, on a trading team (hereinafter, the "Trading Team") at Trading Firm A that traded, among other things, futures contracts on the Chicago Mercantile Exchange ("CME") and the Chicago Board of Trade ("CBOT"). Relevant Definitions and Market Background 3. The CME Group Inc. ("CME Group") was a commodities marketplace made up of several exchanges, including CME and the CBOT, which were based in Chicago, Illinois. At all relevant times, CME and CBOT were registered entities with the U.S. Commodity Futures Trading Commission ("CFTC"). 4. A futures contract was a standardized, legally binding agreement that, once executed, obligated the parties to the contract to buy or to sell a specific product or financial -1- Case 4:18-cr-00606 Document 1 Filed in TXSD on 10/10/18 Page 2 of 8 instrument in the future. That is, the buyer and seller of a futures contract agreed on a price today for a product or financial instrument to be delivered (by the seller), in exchange for money (to be provided by the buyer), on a future date. -

Briefing.Com

PORTFOLIO STRATEGY | PUBLISHED BY RAYMOND JAMES & ASSOCIATES Michael Gibbs, Director of Equity Portfolio & Technical Strategy | (901) DECEMBER 9, 2020 | 9:02 AM EST 579-4346 | [email protected] Joey Madere, CFA | (901) 529-5331 | [email protected] Richard Sewell, CFA | (901) 524-4194 | [email protected] Mitch Clayton, CMT, Senior Technical Analyst | (901) 579-4812 | [email protected] Morning Brew - December 9, 2020 U.S. FUTURES (BRIEFING.COM) The S&P 500 futures trade five points, or 0.1%, above fair value following yesterday's record closes in the benchmark index, Nasdaq Composite, and Russell 2000. Stimulus developments have been of interest this morning. Briefly, Treasury Secretary Mnuchin offered a new $916 billion stimulus bill that includes $600 direct payments to Americans but no enhanced unemployment benefits. The bill is slightly larger than the $908 billion bipartisan bill that excludes direct payments but includes unemployment relief. Democratic Congressional leadership called it progress, according to Bloomberg, but reiterated the need for unemployment relief and said talking points should still be focused on the bipartisan plan. They also shot down Senate Majority Leader McConnell's suggestion of leaving out funding for state and local governments. When the market opens for trading, attention will divert back to equities for the DoorDash (DASH) IPO, which priced shares at $102.00 for a $38.7 billion valuation on a fully-diluted basis. On the data front, investors will receive the JOLTS - Job Openings report for October and Wholesale Inventories for October (Briefing.com consensus 0.9%) at 10:00 a.m. -

Market Information – Glossary of Terms Centrifuge. a Perforated

Market Information – Glossary of Terms Centrifuge. A perforated appliance which spins inside a casing to separate sugar crystals from molasses. Sugar that has come through a centrifuge is centrifugal sugar. Chicago Board of Trade (CBOT). Established in 1848, it is the oldest financial futures and options exchange in the world and situated in Chicago, Illinois. In 2007, the Chicago Board of Trade merged with the Chicago Mercantile Exchange to form the CME Group. Some its commodity futures prices (such as wheat, soya beans and maize) form the principal world price benchmarks. Contract expiry. The date at which trading a particular futures contract ends and becomes either physically or cash settled. For the New York No. 11 raw sugar contract this is the last trading day of the month prior to the delivery month. For the London No. 5 white sugar contract it is sixteen calendar days before the first day of the delivery month. Free on Board (FOB). A term requiring the seller to deliver goods on board a vessel designated by the buyer. The seller fulfils their obligation to deliver when the goods have passed over the ship's rail. Generally, a seller has an obligation to deliver goods, and assume the costs of delivery to a named place for transfer to a carrier, such as a ship. EU sugar regime. In 2006 a major reform achieved simplification and greater market orientation of the EU's sugar policy. The total EU production quota of 13.5 million tonnes of sugar is divided between nineteen Member States, of which the UK’s share is 1.056mt. -

CME Group and Nasdaq Extend Exclusive Nasdaq-100 Futures License Through 2029

October 1, 2018 CME Group and Nasdaq Extend Exclusive Nasdaq-100 Futures License Through 2029 Nasdaq futures and options on futures trade an average of 437,000-plus contracts each day, an increase of 52 percent year-to-date CHICAGO, Oct. 1, 2018 /PRNewswire/ -- CME Group and Nasdaq today announced a ten-year extension of CME Group's exclusive license to offer futures and options on futures based on the Nasdaq-100 and other Nasdaq indexes, through 2029. As the world's leading and most diverse derivatives marketplace, CME Group operates the largest equity index futures complex in the world. Nasdaq is a leading global provider of trading, clearing, exchange technology, listing, information and public company services. "We are extremely pleased to extend our exclusive licensing agreement with Nasdaq, said CME Group Chairman and Chief Executive Officer Terry Duffy. "Building on more than 20 years of partnership, this agreement will ensure market participants worldwide will continue to have seamless access to our suite of Nasdaq products, allowing them to manage risk or gain exposure to the 100 largest non-financial companies. Customers also benefit from capital efficiencies by trading alongside our industry-leading equity index products." "The Nasdaq-100 has been a top performing large cap growth index over the last ten years and has been providing investors with access to the world's most innovative companies, including Amazon, Apple, Facebook, Alphabet, Intel, Microsoft, and Starbucks among many others," said Adena Friedman, President and CEO of Nasdaq. "We have been partners with CME Group for more than 20 years and extending our relationship enables market participants access to our global benchmark products in order to manage their equity market risk." In 1982, CME Group pioneered futures trading on equity indices. -

After a Five-Year Rally, the Commodities Market Has Turned Ugly. As Prices

Blo o m b e r g M a r ke t s COMMODITIES 120 November 2006 CRUNCH By Edward Robinson ‚At 7:55 a.m., five minutes before the opening bell, An- thony Compagnino and Michael Ragazzo huddle in their office on the New York Board of Trade floor—a booth with a dozen telephones and no chairs—to plot their next move in the cocoa pit. “I should have picked a less stressful job, like bomb defusing,” says Ragazzo, a com- modities broker at East Coast Options Services. After five years, the rally in commodity prices has hit a wall. For two days, Ragazzo and Compagnino, his boss, have been selling cocoa futures as prices have plummet- ed 15 percent. Hedge funds that have been riding the richest commodities boom in a generation have dumped cocoa en masse, upending the market. Now, on July 19, the guys at East Cost Options agree that the worst is over. Compagnino, 46, wearing a blue and gold trader’s jacket, hustles to the top rung of the cocoa pit, the tiered ring where trading takes place. Ragazzo, 48, in a matching coat, takes up a position nearby, a phone to each ear. The bell sounds—and all hell breaks loose. One floor broker barks a bid to buy cocoa for September delivery for $1,517 a metric ton. Another hollers an offer to sell at $1,507. The traders down in the pit can’t settle on a price. Compagnino starts selling. “Thirty Seps at 18! Thirty Seps at 18!” Compagnino thunders, offering to sell 30 September contracts on cocoa for $1,518 per ton. -

From 9/11 to 8/29: Post-Disaster Recovery and Rebuilding in New York and New Orleans

From 9/11 to 8/29: Post-Disaster Recovery and Rebuilding in New York and New Orleans Kevin Fox Gotham Miriam Greenberg Social Forces, Volume 87, Number 2, December 2008, pp. 1039-1062 (Article) Published by The University of North Carolina Press DOI: 10.1353/sof.0.0131 For additional information about this article http://muse.jhu.edu/journals/sof/summary/v087/87.2.gotham.html Access Provided by Tulane University at 04/20/11 3:40PM GMT From 9/11 to 8/29: Post-Disaster Recovery and Rebuilding in New York and New Orleans Kevin Fox Gotham, Tulane University Miriam Greenberg, University of California, Santa Cruz This article examines the process of post-disaster recovery and rebuilding in New York City since 9/11 and in New Orleans since the Hurricane Katrina disaster (8/29). As destabilizing events, 9/11 and 8/29 forced a rethinking of the major categories, concepts and theories that long dominated disaster research. We analyze the form, trajectory and problems of reconstruction in the two cities with special emphasis on the implementation of the Community Development Block Grant program, the Liberty Zone and the Gulf Opportunity Zone, and tax-exempt private activity bonds to finance and promote reinvestment. Drawing on a variety of data sources, we show that New York and New Orleans have become important laboratories for entrepreneurial city and state governments seeking to use post-disaster rebuilding as an opportunity to push through far-reaching neoliberal policy reforms. The emphasis on using market-centered approaches for urban recovery and rebuilding in New York and New Orleans should be seen not as coherent or sustainable responses to urban disaster but rather as deeply contradictory restructuring strategies that are intensifying the problems they seek to remedy. -

Federal Register/Vol. 85, No. 39/Thursday, February 27, 2020

11596 Federal Register / Vol. 85, No. 39 / Thursday, February 27, 2020 / Proposed Rules COMMODITY FUTURES TRADING All comments must be submitted in F. § 150.8—Severability COMMISSION English, or if not, be accompanied by an G. § 150.9—Process for Recognizing Non- English translation. Comments will be Enumerated Bona Fide Hedging 17 CFR Parts 1, 15, 17, 19, 40, 140, 150, posted as received to https:// Transactions or Positions With Respect and 151 to Federal Speculative Position Limits comments.cftc.gov. You should submit H. Part 19 and Related Provisions— RIN 3038–AD99 only information that you wish to make Reporting of Cash-Market Positions available publicly. If you wish the I. Removal of Part 151 Position Limits for Derivatives Commission to consider information III. Legal Matters that you believe is exempt from A. Introduction AGENCY: Commodity Futures Trading disclosure under the Freedom of B. Key Statutory Provisions Commission. Information Act (‘‘FOIA’’), a petition for C. Ambiguity of Section 4a With Respect ACTION: Proposed rule. to Necessity Finding confidential treatment of the exempt D. Resolution of Ambiguity SUMMARY: The Commodity Futures information may be submitted according E. Evaluation of Considerations Relied Trading Commission (‘‘Commission’’ or to the procedures established in § 145.9 Upon by the Commission in Previous 1 ‘‘CFTC’’) is proposing amendments to of the Commission’s regulations. Interpretation of Paragraph 4a(a)(2) regulations concerning speculative The Commission reserves the right, F. Necessity Finding but shall have no obligation, to review, G. Request for Comment position limits to conform to the Wall IV. Related Matters Street Transparency and Accountability pre-screen, filter, redact, refuse, or remove any or all submissions from A. -

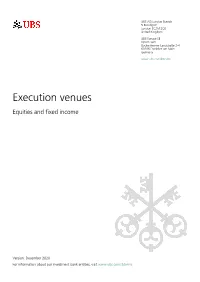

Execution Venues Equities and Fixed Income

UBS AG London Branch 5 Broadgate London EC2M 2QS United Kingdom UBS Europe SE OpernTurm Bockenheimer Landstraße 2-4 60306 Frankfurt am Main Germany www.ubs.com/ibterms Execution venues Equities and fixed income Version: December 2020 For information about our investment bank entities, visit www.ubs.com/ibterms Execution venues This is a non-exhaustive list of the main execution venues that we use outside UBS and our own systematic internalisers. We will review and update it from time to time in accordance with our UK and EEA MiFID Order Handling & Execution Policy. We may use other execution venues where appropriate. Equities Cash Equities Direct access Aquis Exchange Europe Aquis Exchange PlcAthens Stock Exchange BATS Europe, a CBOE Company Borsa Italiana CBOE NL CBOE UK Citadel Securities (Europe) Limited SI Deutsche Börse Group - Xetra Euronext Amsterdam Stock Exchange Euronext Brussels Stock Exchange Euronext Lisbon Stock Exchange Euronext Paris Stock Exchange Instinet Blockmatch Euronext DublinITG Posit London Stock Exchange Madrid Stock Exchange Nasdaq Copenhagen Nasdaq Helsinki Nasdaq Stockholm Oslo Bors Sigma X Europe Sigma X MTFTower Research Capital Europe Limited SI Turquoise Europe TurquoiseUBS Investment Bank UBS MTF Vienna Stock Exchange Virtu Financial Ireland Limited Warsaw Stock Exchange Via intermediate broker Budapest Stock Exchange Cairo & Alexandria Stock Exchange Deutsche Börse - Frankfurt Stock Exchange Istanbul Stock Exchange Johannesburg Stock Exchange Moscow Exchange Prague Stock Exchange SIX Swiss Exchange Tel Aviv Stock Exchange Structured Products Direct access Börse Frankfurt (Zertifikate Premium) Börse Stuttgart (EUWAX) Xetra SIX Swiss Exchange SeDeX Milan Euronext Amsterdam London Stock Exchange Madrid Stock Exchange NASDAQ OMX Stockholm JSE Johannesburg Stock Exchange OTC matching CATS-OS Fixed Income Cash bonds Via Bond Port Bloomberg EuroTLX Euronext ICE (KCG) BondPoint Market Axess MOT MTS BondsPro 1 © UBS 2020. -

Download Cotton Market Information

Cotton No.2 Intercontinental Exchange® (ICE®) became the center of global trading in “soft” commodities with its acquisition of the New York Board of Trade (NYBOT) in 2007. Now known as ICE Futures U.S.®, the exchange offers futures and options on futures on soft commodities including coffee, cocoa, frozen concentrated orange juice, sugar and cotton. Cotton futures have traded in New York since 1870, first on the New York Cotton Exchange, then on the New York Board of Trade and now on ICE Futures U.S. Options on cotton futures were introduced in 1984. Futures and options on futures are used by both the domestic and global cotton industries to price and hedge transactions. Because cotton is at the center of the global textiles industry, it is a preferred contract among commodity trading advisors and hedge funds. ICE Futures U.S. is the exclusive global market for Cotton No. 2 futures and options. A BRIEF HISTORY OF COTTON IN COMMERCE the economy in the American south, the perpetuation of slavery and Cotton is grown widely around the world and has been used for ultimately the American Civil War. at least 7,000 years. While the oldest archaeological fragments have been found in Mexico, the Indus valley in modern Pakistan Cotton was so critical to British and French industries at the time was the first commercial cotton-growing center. Alexander the that both countries contemplated intervening on behalf of the Great brought cotton back from the Indus Valley into the Hellenistic Confederacy during the Civil War, their opposition to slavery world.