Federal Register/Vol. 85, No. 39/Thursday, February 27, 2020

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Margin Requirements Across Equity-Related Instruments: How Level Is the Playing Field?

Fortune pgs 31-50 1/6/04 8:21 PM Page 31 Margin Requirements Across Equity-Related Instruments: How Level Is the Playing Field? hen interest rates rose sharply in 1994, a number of derivatives- related failures occurred, prominent among them the bankrupt- cy of Orange County, California, which had invested heavily in W 1 structured notes called “inverse floaters.” These events led to vigorous public discussion about the links between derivative securities and finan- cial stability, as well as about the potential role of new regulation. In an effort to clarify the issues, the Federal Reserve Bank of Boston sponsored an educational forum in which the risks and risk management of deriva- tive securities were discussed by a range of interested parties: academics; lawmakers and regulators; experts from nonfinancial corporations, investment and commercial banks, and pension funds; and issuers of securities. The Bank published a summary of the presentations in Minehan and Simons (1995). In the keynote address, Harvard Business School Professor Jay Light noted that there are at least 11 ways that investors can participate in the returns on the Standard and Poor’s 500 composite index (see Box 1). Professor Light pointed out that these alternatives exist because they dif- Peter Fortune fer in a variety of important respects: Some carry higher transaction costs; others might have higher margin requirements; still others might differ in tax treatment or in regulatory restraints. The author is Senior Economist and The purpose of the present study is to assess one dimension of those Advisor to the Director of Research at differences—margin requirements. -

Morning Briefing Global Economic Trading Calendar

A Eurex publication focused on European financial markets, produced by MNl Morning Briefing March 12h 2015 Thursday sees a full day of data, with Council Member KlaasKnot speaks and be up 0.4%also excluding the German and French final inflation in Amsterdam. gasoline station sales. numbers the early feature. EMU data at 1000GMT sees the The US January business At 0700GMT, the German final January industrial output numbers inventories data will cross the wires February harmonised inflation data cross the wires. at 1400GMT. will be published. to be followed by the French numbers at 0745GMT Across the Atlantic, the calendar gets The value of business inventories is and the Spanish data at 0800GMT. underway at 1230GMT, with the expected to fall 0.2% in January after release of the February retail sales, small gains in recent months. ECB Executive Board Member February import/export index and the Benoit Coeure will deliver a speech jobless claims data for the March 7 Late data sees the US February on the future of euro area week. Treasury Statement set for release at investment, quantitative easing, and 1800GMT and Greek debt, in Paris, starting The level of initial jobless claims is at0745GMT. expected to fall by 12,000 to 308,000 the M2 money supply data for the in the March 7 week after rising by Mar 2 week at 2030GMT. Then, at 0915GMT, ECB Governing 7,000 in the previous week. The four- Council Member Jens Weidmann will week moving average rose by The U.S. Treasury is expected to hold a press conference, in 10,250 to 304,750 in the February 28 post a $188.5 billion budget deficit Frankfurt. -

Chicago Mercantile Exchange, Chicago Board of Trade, New York

Sean M. Downey Senior Director and Associate General Counsel Legal Department March 15, 2013 VIA E-MAIL Ms. Melissa Jurgens Office of the Secretariat Commodity Futures Trading Commission Three Lafayette Centre 1155 21st Street, N.W. Washington, DC 20581 RE: Regulation 40.6(a). Chicago Mercantile Exchange Inc./ The Board of Trade of the City of Chicago, Inc./ The New York Mercantile Exchange, Inc./ Commodity Exchange, Inc. Submission # 13-066: Revisions to CME, CBOT and NYMEX/COMEX Position Limit, Position Accountability and Reportable Level Tables Dear Ms. Jurgens: Chicago Mercantile Exchange Inc. (“CME”), The Board of Trade of the City of Chicago, Inc. (“CBOT”), The New York Mercantile Exchange, Inc. (“NYMEX”) and Commodity Exchange, Inc. (“COMEX”), (collectively, the “Exchanges”) are self-certifying revisions to the Position Limit, Position Accountability and Reportable Level Tables (collectively, the “Tables”) in the Interpretations & Special Notices Section of Chapter 5 in the Exchanges’ Rulebooks. The revisions will become effective on April 1, 2013 and are being adopted to ensure that the Tables are in compliance with CFTC Core Principle 7 (“Availability of General Information”), which requires that DCMs make available to the public accurate information concerning the contract market’s rules and regulations, contracts and operations. In connection with CFTC Core Principle 7, the Exchanges launched a Rulebook Harmonization Project with the goal of eliminating old, erroneous and obsolete language, ensuring the accuracy of all listed values (e.g., position limits, aggregation, diminishing balances, etc.) and harmonizing the language and structure of the Tables and product chapters to the best extent possible. The changes to the Tables are primarily stylistic in nature (e.g., format, extra columns, tabs, product groupings, etc.). -

Mao Indictment

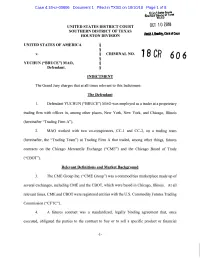

Case 4:18-cr-00606 Document 1 Filed in TXSD on 10/10/18 Page 1 of 8 UNITED STATES DISTRICT COURT OCT 1 0 2018 SOUTHERN DISTRICT OF TEXAS HOUSTON DIVISION UNITED STATES OF AMERICA § § v. § CRIMINAL NO. § 18 CR 60 6 YUCHUN ("BRUCE") MAO, § Defendant. § INDICTMENT The Grand Jury charges that at all times relevant to this Indictment: The Defendant 1. Defendant YUCHUN ("BRUCE") MAO was employed as a trader at a proprietary trading firm with offices in, among other places, New York, New York, and Chicago, Illinois (hereinafter "Trading Firm A"). 2. MAO worked with two co-conspirators, CC-1 and CC-2, on a trading team (hereinafter, the "Trading Team") at Trading Firm A that traded, among other things, futures contracts on the Chicago Mercantile Exchange ("CME") and the Chicago Board of Trade ("CBOT"). Relevant Definitions and Market Background 3. The CME Group Inc. ("CME Group") was a commodities marketplace made up of several exchanges, including CME and the CBOT, which were based in Chicago, Illinois. At all relevant times, CME and CBOT were registered entities with the U.S. Commodity Futures Trading Commission ("CFTC"). 4. A futures contract was a standardized, legally binding agreement that, once executed, obligated the parties to the contract to buy or to sell a specific product or financial -1- Case 4:18-cr-00606 Document 1 Filed in TXSD on 10/10/18 Page 2 of 8 instrument in the future. That is, the buyer and seller of a futures contract agreed on a price today for a product or financial instrument to be delivered (by the seller), in exchange for money (to be provided by the buyer), on a future date. -

Briefing.Com

PORTFOLIO STRATEGY | PUBLISHED BY RAYMOND JAMES & ASSOCIATES Michael Gibbs, Director of Equity Portfolio & Technical Strategy | (901) DECEMBER 9, 2020 | 9:02 AM EST 579-4346 | [email protected] Joey Madere, CFA | (901) 529-5331 | [email protected] Richard Sewell, CFA | (901) 524-4194 | [email protected] Mitch Clayton, CMT, Senior Technical Analyst | (901) 579-4812 | [email protected] Morning Brew - December 9, 2020 U.S. FUTURES (BRIEFING.COM) The S&P 500 futures trade five points, or 0.1%, above fair value following yesterday's record closes in the benchmark index, Nasdaq Composite, and Russell 2000. Stimulus developments have been of interest this morning. Briefly, Treasury Secretary Mnuchin offered a new $916 billion stimulus bill that includes $600 direct payments to Americans but no enhanced unemployment benefits. The bill is slightly larger than the $908 billion bipartisan bill that excludes direct payments but includes unemployment relief. Democratic Congressional leadership called it progress, according to Bloomberg, but reiterated the need for unemployment relief and said talking points should still be focused on the bipartisan plan. They also shot down Senate Majority Leader McConnell's suggestion of leaving out funding for state and local governments. When the market opens for trading, attention will divert back to equities for the DoorDash (DASH) IPO, which priced shares at $102.00 for a $38.7 billion valuation on a fully-diluted basis. On the data front, investors will receive the JOLTS - Job Openings report for October and Wholesale Inventories for October (Briefing.com consensus 0.9%) at 10:00 a.m. -

To Process Or Not to Process: the Production Transformation Option

TO PROCESS OR NOT TO PROCESS: THE PRODUCTION TRANSFORMATION OPTION by George Dotsis* and Nikolaos T. Milonas** February 2015 * Department of Economics, National and Kapodistrian University of Athens, 1 Sofokleous street, Athens 105 59 Greece, Tel. +30210 368 3973, e-mail: [email protected] ** Department of Economics, National and Kapodistrian University of Athens, 1 Sofokleous street, Athens 105 59 Greece, Tel. +30210 368 9442, e-mail: [email protected] The authors would like to thank the participants of the Finance Workshop at the University of Massachusetts-Amherst for useful comments on an earlier draft. The author alone has the responsibility for any remaining errors. TO PROCESS OR NOT TO PROCESS: THE PRODUCTION TRANSFORMATION OPTION Abstract This paper examines the implications of the production transformation asymmetry on prices of the commodity relative to the prices of its derivative products. When the production transformation process of a harvested good is irreversible, the price linkage between the harvested good and its derivatives breaks. This happens in the case where the supply of the good declines significantly and when independent demand for the good exists. Because the price of the good can rise above the combined value of its derivatives, it is associated with a valuable option not to process. The equilibrium processing margins are derived within a three period model. We show that the option not to process is valuable and can only be exercised by those who carry the commodity. Furthermore, it is shown that a partial hedging strategy is sufficient to reduce all price risk and it is superior to a strategy of no hedging. -

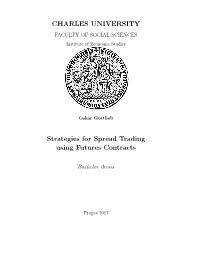

CHARLES UNIVERSITY Strategies for Spread Trading Using Futures

CHARLES UNIVERSITY FACULTY OF SOCIAL SCIENCES Institute of Economic Studies Oskar Gottlieb Strategies for Spread Trading using Futures Contracts Bachelor thesis Prague 2017 Author: Oskar Gottlieb Supervisor: doc. PhDr. Ladislav Kriˇstoufek Ph.D. Academic Year: 2016/2017 [Year of defense: 2017] Bibliografick´yz´aznam GOTTLIEB, Oskar. Strategies for Spread Trading Using Futures Contracts Praha 2017. 80 s. Bakal´aˇrsk´apr´ace (Bc.) Univerzita Karlova, Fakulta soci´aln´ıch vˇed, Institut ekonomick´ych studi´ı. Vedouc´ıdiplomov´epr´ace doc. PhDr. Ladislav Kriˇstoufek Ph.D. Anotace (abstrakt) Tato pr´ace se zamˇeˇruje na spready na futuritn´ıch trz´ıch, konkr´etnˇestuduje obchodn´ıstrategie zaloˇzen´ena dvou pˇr´ıstupech - kointegrace otestovan´ana inter-komoditn´ıch spreadech a sez´onnost kterou pozorujeme na kalend´aˇrn´ıch (intra-komoditn´ıch) spreadech. Na p´arech kontrakt˚u, kter´ejsou kointegrovan´e budeme testovat strategie zaloˇzen´ena n´avratu k pr˚umˇeru. Tˇri strategie budou vyuˇz´ıvat filtr tzv. ‘f´erov´ehodnoty’, jedna bude pracovat s hodnotou relativn´ı. Podobn´ym zp˚usobem budeme na kalend´aˇrn´ıch spreadech testovat strategie typu “buy and hold”. Vˇsechny strategie testujeme na in-sample a out-of-sample datech. Sez´onn´ıstrategie nevygenerovaly dostateˇcnˇeziskov´e strategie, nˇekter´einter-komoditn´ıspready se naopak uk´azaly jako profitab- iln´ıv obou testovac´ıch period´ach. V´yjimku u inter-komoditn´ıch spread˚u tvoˇrily zejm´ena vˇseobecnˇezn´am´espready, kter´ev out-of-sample testech neobst´aly. Kl´ıˇcov´aslova Futuritn´ıkontrakty, kointegrace, sez´onnost, strategie zaloˇzen´ena reverzi k pr˚umˇeru, futuritn´ıspready Bibliographic note GOTTLIEB, Oskar. Strategies for Spread Trading Using Futures Contracts Prague 2017. -

CME Group and Nasdaq Extend Exclusive Nasdaq-100 Futures License Through 2029

October 1, 2018 CME Group and Nasdaq Extend Exclusive Nasdaq-100 Futures License Through 2029 Nasdaq futures and options on futures trade an average of 437,000-plus contracts each day, an increase of 52 percent year-to-date CHICAGO, Oct. 1, 2018 /PRNewswire/ -- CME Group and Nasdaq today announced a ten-year extension of CME Group's exclusive license to offer futures and options on futures based on the Nasdaq-100 and other Nasdaq indexes, through 2029. As the world's leading and most diverse derivatives marketplace, CME Group operates the largest equity index futures complex in the world. Nasdaq is a leading global provider of trading, clearing, exchange technology, listing, information and public company services. "We are extremely pleased to extend our exclusive licensing agreement with Nasdaq, said CME Group Chairman and Chief Executive Officer Terry Duffy. "Building on more than 20 years of partnership, this agreement will ensure market participants worldwide will continue to have seamless access to our suite of Nasdaq products, allowing them to manage risk or gain exposure to the 100 largest non-financial companies. Customers also benefit from capital efficiencies by trading alongside our industry-leading equity index products." "The Nasdaq-100 has been a top performing large cap growth index over the last ten years and has been providing investors with access to the world's most innovative companies, including Amazon, Apple, Facebook, Alphabet, Intel, Microsoft, and Starbucks among many others," said Adena Friedman, President and CEO of Nasdaq. "We have been partners with CME Group for more than 20 years and extending our relationship enables market participants access to our global benchmark products in order to manage their equity market risk." In 1982, CME Group pioneered futures trading on equity indices. -

Copyrighted Material

Index A convertible, 106 MBS Index, 82 Adjustable-rate mortgages (ARMs), 97 stock-index, 137 Municipal Bond Index, 82 Agency securities. See Bonds Arnott, Robert, 84 BATS Global Markets, 52–53 Alaska, 91 Asian Development Bank, 87 Basis points, 20–21, 23–24, 32, 39, 44, 46–47, 48, 107, Alerian MLP Index, 117–118 Ask 109–110, 147, 149, 151, 153–154 Allied Capital, 113 premium, 141–142 benchmark Alternative assets. See Commodities, Real estate price, 5, 14, 27, 54–55, 66, 71, 94, 109, 116, 120, base metals prices, 131 Alternative Display Facility, 54, 55 132, 134, 142, 154, 162 CDS rate, 156 Alternative funds rate, 21, 149 commodities, 129 angel investing, 165–166, 170 Auctions, debt, 3, 18–20, 24–26, 30, 90 fund performance, 79, 128, 160–161, 164, funds of funds, 167 Australia, 113 168, 177 global macro, 166–167 Auto loans, 93 futures, 129 hedge funds, 63, 106, 113, 127, 165–169, 177 index, bonds, 81–83 long-biased, 167 B index, commodities, 174–175 long-short, 167 Backwardation, 135–136, 137 index, hard assets, 85 managed futures, 167 Bank for International Settlements (BIS), index, MLPs, 117 market neutral, 167 12, 150 index, stocks, 83, 125, 137 private equity, 63, 165–166, 169, 170 Bank of America, 100, 103 index, real estate, short-biased, 167 Merrill Lynch, 82, 175 index, REITs, 120–121 venture capital, 165–166, 170 Bank reserves, 36 interest rate, 8, 24, 32, 36, 97, 110, 147 Amazon.com, 164, 166 Bankers’ acceptances (BAs), 36 maturities, 49, American Depositary Bankruptcy. See also Eastman Kodak, Lehman mortgage-backed bonds, 95 Receipts (ADRs), 56 Brothers, Risk gold price, 65, 85 Shares (ADSs), 56 corporate, 21, 40, 54, 99–100, 103, 108, oil price, 70, 72, 131 Angel investing. -

Putting on the Crush: Day Trading the Soybean Complex Spread Dominic Rechner Geoffrey Poitras

Putting on the Crush: Day Trading the Soybean Complex Spread Dominic Rechner Geoffrey Poitras INTRODUCTION n recent years, spread trading strategies for financial commodities have received I considerable attention [Rentzler (1986); Poitras (1987); Yano (1989)] while, with some exceptions, spreads in agricultural commodities have been relatively ignored. Limited or no information is available, for example, on the performance of various profit margin trading rules arising from^roduction relationships between tradeable agricultural input and outgut-prices, e.g., soybean meal, corn and live hogs [Kenyon and Clay (1987)]. Of ttfea^icultural spreading strategies, the so-called "soy crush" or soybean complex spread is possibly the most well known.' Trading rules arising from this spread exploit the gross processing margin (GPM) inherent in the processing of raw soybeans into crude oil and meal. The primary objective of this study is to show that it is possible to use the GPM, derived from the known relative proportions of meal, oil, and beans, to specify profitable rules for day trading the soy crush spread.^ This article first reviews relevant results of previous studies on the soybean complex and its components followed by specifics on the GPM-based, intraday trading rule under consideration. Assumptions on contract selection, transactions costs, and margin costs are discussed. Simulation results for the trade on daily data over the period February 1, 1978 to July 30, 1991 are presented. The results indicate that, for sufficiently large filter sizes, the trading rule under consideration is profitable during the sample periods examined. It is argued that the results of this study refiect the potential profitability of fioor trading in the soybean pits. -

Financial and Commodity-Specific Expectations in Soybean Futures Markets

Financial and Commodity-specific expectations in soybean futures markets A.N.Q. Cao; S.-C. Grosche Institute for Food and Resource Economics, Rheinische Friedrich-Wilhelms- Universität Bonn, , Germany Corresponding author email: [email protected] Abstract: We conceptualize the futures price of an agricultural commodity as an aggregate expectation for the spot price of a commodity. The market agents have divergent opinions about the price development and the price drivers, which initiates trading. In informationally efficient markets, the price will thus reflect expectations about its influencing variables. Using historical decompositions from an SVARX model, we analyze the contribution of financial and commodity- specific expectation shocks to changes in a trading- volume weighted price index for corn and soybean futures on the Chicago Board of Trade (CBOT) over the time period 2005- 2016. Financial expectations are instrumented with the DJ REIT Index, commodity demand expectations with the CNY/USD exchange rate and supply expectations with changes in the vapor pressure deficit. Results show that the price index was affected by cumulative shocks in the REIT index during the time of the food price crisis, but these shocks are only of small magnitude. Weather fluctuations have a minimal impact on the week-to-week fluctuation of the commodity price index. Acknowledegment: JEL Codes: C32, C52 #1831 Financial and commodity-specific expectations in soybean futures markets1 Abstract. We conceptualize the futures price of an agricultural commodity as an aggregate expectation for the spot price of a commodity. The market agents have divergent opinions about the price development and the price drivers, which initiates trading. -

Agriculture: a Glossary of Terms, Programs, and Laws, 2005 Edition

Agriculture: A Glossary of Terms, Programs, and Laws, 2005 Edition Updated June 16, 2005 Congressional Research Service https://crsreports.congress.gov 97-905 Agriculture: A Glossary of Terms, Programs, and Laws, 2005 Edition Summary The complexities of federal farm and food programs have generated a unique vocabulary. Common understanding of these terms (new and old) is important to those involved in policymaking in this area. For this reason, the House Agriculture Committee requested that CRS prepare a glossary of agriculture and related terms (e.g., food programs, conservation, forestry, environmental protection, etc.). Besides defining terms and phrases with specialized meanings for agriculture, the glossary also identifies acronyms, abbreviations, agencies, programs, and laws related to agriculture that are of particular interest to the staff and Members of Congress. CRS is releasing it for general congressional use with the permission of the Committee. The approximately 2,500 entries in this glossary were selected in large part on the basis of Committee instructions and the informed judgment of numerous CRS experts. Time and resource constraints influenced how much and what was included. Many of the glossary explanations have been drawn from other published sources, including previous CRS glossaries, those published by the U.S. Department of Agriculture and other federal agencies, and glossaries contained in the publications of various organizations, universities, and authors. In collecting these definitions, the compilers discovered that many terms have diverse specialized meanings in different professional settings. In this glossary, the definitions or explanations have been written to reflect their relevance to agriculture and recent changes in farm and food policies.