Currency, Bullion and Accounts. Monetary Modes in the Roman World

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

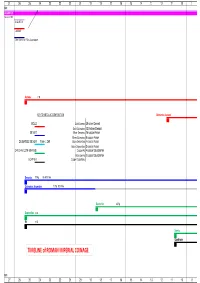

TIMELINE of ROMAN IMPERIAL COINAGE

27 26 25 24 23 22 21 20 19 18 17 16 15 14 13 12 11 10 9 B.C. AUGUSTUS 16 Jan 27 BC AUGUSTUS CAESAR Other title: e.g. Filius Augustorum Aureus 7.8g KEY TO METALLIC COMPOSITION Quinarius Aureus GOLD Gold Aureus 25 silver Denarii Gold Quinarius 12.5 silver Denarii SILVER Silver Denarius 16 copper Asses Silver Quinarius 8 copper Asses DE-BASED SILVER from c. 260 Brass Sestertius 4 copper Asses Brass Dupondius 2 copper Asses ORICHALCUM (BRASS) Copper As 4 copper Quadrantes Brass Semis 2 copper Quadrantes COPPER Copper Quadrans Denarius 3.79g 96-98% fine Quinarius Argenteus 1.73g 92% fine Sestertius 25.5g Dupondius 12.5g As 10.5g Semis Quadrans TIMELINE of ROMAN IMPERIAL COINAGE B.C. 27 26 25 24 23 22 21 20 19 18 17 16 15 14 13 12 11 10 9 8 7 6 5 4 3 2 1 1 2 3 4 5 6 7 8 9 10 11 A.D.A.D. denominational relationships relationships based on Aureus Aureus 7.8g 1 Quinarius Aureus 3.89g 2 Denarius 3.79g 25 50 Sestertius 25.4g 100 Dupondius 12.4g 200 As 10.5g 400 Semis 4.59g 800 Quadrans 3.61g 1600 8 7 6 5 4 3 2 1 1 2 3 4 5 6 7 8 91011 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 19 Aug TIBERIUS TIBERIUS Aureus 7.75g Aureus Quinarius Aureus 3.87g Quinarius Aureus Denarius 3.76g 96-98% fine Denarius Sestertius 27g Sestertius Dupondius 14.5g Dupondius As 10.9g As Semis Quadrans 3.61g Quadrans 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46 47 48 49 TIBERIUS CALIGULA CLAUDIUS Aureus 7.75g 7.63g Quinarius Aureus 3.87g 3.85g Denarius 3.76g 96-98% fine 3.75g 98% fine Sestertius 27g 28.7g -

The Roman Empire – Roman Coins Lesson 1

Year 4: The Roman Empire – Roman Coins Lesson 1 Duration 2 hours. Date: Planned by Katrina Gray for Two Temple Place, 2014 Main teaching Activities - Differentiation Plenary LO: To investigate who the Romans were and why they came Activities: Mixed Ability Groups. AFL: Who were the Romans? to Britain Cross curricular links: Geography, Numeracy, History Activity 1: AFL: Why did the Romans want to come to Britain? CT to introduce the topic of the Romans and elicit children’s prior Sort timeline flashcards into chronological order CT to refer back to the idea that one of the main reasons for knowledge: invasion was connected to wealth and money. Explain that Q Who were the Romans? After completion, discuss the events as a whole class to ensure over the next few lessons we shall be focusing on Roman Q What do you know about them already? that the children understand the vocabulary and events described money / coins. Q Where do they originate from? * Option to use CT to show children a map, children to locate Rome and Britain. http://www.schoolsliaison.org.uk/kids/preload.htm or RESOURCES Explain that the Romans invaded Britain. http://resources.woodlands-junior.kent.sch.uk/homework/romans.html Q What does the word ‘invade’ mean? for further information about the key dates and events involved in Websites: the Roman invasion. http://www.schoolsliaison.org.uk/kids/preload.htm To understand why they invaded Britain we must examine what http://www.sparklebox.co.uk/topic/past/roman-empire.html was happening in Britain before the invasion. -

Ancient Roman Measures Page 1 of 6

Ancient Roman Measures Page 1 of 6 Ancient Rome Table of Measures of Length/Distance Name of Unit (Greek) Digitus Meters 01-Digitus (Daktylos) 1 0.0185 02-Uncia - Polex 1.33 0.0246 03-Duorum Digitorum (Condylos) 2 0.037 04-Palmus (Pala(i)ste) 4 0.074 05-Pes Dimidius (Dihas) 8 0.148 06-Palma Porrecta (Orthodoron) 11 0.2035 07-Palmus Major (Spithame) 12 0.222 08-Pes (Pous) 16 0.296 09-Pugnus (Pygme) 18 0.333 10-Palmipes (Pygon) 20 0.370 11-Cubitus - Ulna (pechus) 24 0.444 12-Gradus – Pes Sestertius (bema aploun) 40 0.74 13-Passus (bema diploun) 80 1.48 14-Ulna Extenda (Orguia) 96 1.776 15-Acnua -Dekempeda - Pertica (Akaina) 160 2.96 16-Actus 1920 35.52 17-Actus Stadium 10000 185 18-Stadium (Stadion Attic) 10000 185 19-Milliarium - Mille passuum 80000 1480 20-Leuka - Leuga 120000 2220 http://www.anistor.gr/history/diophant.html Ancient Roman Measures Page 2 of 6 Table of Measures of Area Name of Unit Pes Quadratus Meters2 01-Pes Quadratus 1 0.0876 02-Dimidium scrupulum 50 4.38 03-Scripulum - scrupulum 100 8.76 04-Actus minimus 480 42.048 05-Uncia 2400 210.24 06-Clima 3600 315.36 07-Sextans 4800 420.48 08-Actus quadratus 14400 1261.44 09-Arvum - Arura 22500 1971 10-Jugerum 28800 2522.88 11-Heredium 57600 5045.76 12-Centuria 5760000 504576 13-Saltus 23040000 2018304 http://www.anistor.gr/history/diophant.html Ancient Roman Measures Page 3 of 6 Table of Measures of Liquids Name of Unit Ligula Liters 01-Ligula 1 0.0114 02-Uncia (metric) 2 0.0228 03-Cyathus 4 0.0456 04-Acetabulum 6 0.0684 05-Sextans 8 0.0912 06-Quartarius – Quadrans 12 0.1368 -

Coins and Medals Including Renaissance and Later Medals from the Collection of Dr Charles Avery and Byzantine Coins from the Estate of Carroll F

Coins and Medals including Renaissance and Later Medals from the Collection of Dr Charles Avery and Byzantine Coins from the Estate of Carroll F. Wales (Part I) To be sold by auction at: Sotheby’s, in the Upper Grosvenor Gallery The Aeolian Hall, Bloomfield Place New Bond Street London W1 Days of Sale: Wednesday 11 and Thursday 12 June 2008 10.00 am and 2.00 pm Public viewing: 45 Maddox Street, London W1S 2PE Friday 6 June 10.00 am to 4.30 pm Monday 9 June 10.00 am to 4.30 pm Tuesday 10 June 10.00 am to 4.30 pm Or by previous appointment. Catalogue no. 31 Price £10 Enquiries: James Morton, Tom Eden, Paul Wood, Jeremy Cheek or Stephen Lloyd Cover illustrations: Lot 465 (front); Lot 1075 (back); Lot 515 (inside front and back covers, all at two-thirds actual size) in association with 45 Maddox Street, London W1S 2PE Tel.: +44 (0)20 7493 5344 Fax: +44 (0)20 7495 6325 Email: [email protected] Website: www.mortonandeden.com This auction is conducted by Morton & Eden Ltd. in accordance with our Conditions of Business printed at the back of this catalogue. All questions and comments relating to the operation of this sale or to its content should be addressed to Morton & Eden Ltd. and not to Sotheby’s. Important Information for Buyers All lots are offered subject to Morton & Eden Ltd.’s Conditions of Business and to reserves. Estimates are published as a guide only and are subject to review. The actual hammer price of a lot may well be higher or lower than the range of figures given and there are no fixed “starting prices”. -

Small Change and Big Changes: Minting and Money After the Fall of Rome

This is a repository copy of Small Change and Big Changes: minting and money after the Fall of Rome. White Rose Research Online URL for this paper: http://eprints.whiterose.ac.uk/90089/ Version: Draft Version Other: Jarrett, JA (Completed: 2015) Small Change and Big Changes: minting and money after the Fall of Rome. UNSPECIFIED. (Unpublished) Reuse Unless indicated otherwise, fulltext items are protected by copyright with all rights reserved. The copyright exception in section 29 of the Copyright, Designs and Patents Act 1988 allows the making of a single copy solely for the purpose of non-commercial research or private study within the limits of fair dealing. The publisher or other rights-holder may allow further reproduction and re-use of this version - refer to the White Rose Research Online record for this item. Where records identify the publisher as the copyright holder, users can verify any specific terms of use on the publisher’s website. Takedown If you consider content in White Rose Research Online to be in breach of UK law, please notify us by emailing [email protected] including the URL of the record and the reason for the withdrawal request. [email protected] https://eprints.whiterose.ac.uk/ Small Change and Big Changes: It’s a real pleasure to be back at the Barber again so soon, and I want to start by thanking Nicola, Robert and Jen for letting me get away with scheduling myself like this as a guest lecturer for my own exhibition. I’m conscious that in speaking here today I’m treading in the footsteps of some very notable numismatists, but right now the historic name that rings most loudly in my consciousness is that of the former Curator of the coin collection here and then Lecturer in Numismatics in the University, Michael Hendy. -

Experimental Investigation of Silvering in Late Roman Coinage

Mat. Res. Soc. Symp. Proc. Vol. 712 © 2002 Materials Research Society Experimental investigation of silvering in late Roman coinage C. Vlachou, J.G. McDonnell, R.C. Janaway Department of Archaeological Sciences, University of Bradford, BD7 1DP, UK. ABSTRACT Roman Coinage suffered from severe debasement during the 3rd century AD. By 250 AD., the production of complex copper alloy (Cu-Sn-Pb-Ag) coins with a silvered surface, became common practice. The same method continued to be applied during the 4th century AD for the production of a new denomination introduced by Diocletian in 293/4 AD. Previous analyses of these coins did not solve key technological issues and in particular, the silvering process. The British Museum kindly allowed further research at Bradford to examine coins from Cope’s Archive in more detail, utilizing XRF, SEM-EDS metallography, LA-ICP-MS and EPMA. Metallographic and SEM examination of 128 coins, revealed that the silver layer was very difficult to trace because its thickness was a few microns and in some cases it was present under the corrosion layer. Results derived from the LA-ICP-MS and EPMA analyses have demonstrated, for the first time, the presence of Hg in the surface layers of these coins. A review of ancient sources and historic literature indicated possible methods which might have been used for the production of the plating. A programme of plating experiments was undertaken to examine a number of variables in the process, such as amalgam preparation, and heating cycles. Results from the experimental work are presented. ITRODUCTION Coinage in the Late Roman Period suffered from severe debasement. -

A Handbook of Greek and Roman Coins

CORNELL UNIVERSITY LIBRARY BOUGHT WITH THE INCOME OF THE SAGE ENDOWMENT FUND GIVEN IN 1891 BY HENRY WILLIAMS SAGE Cornell University Library CJ 237.H64 A handbook of Greek and Roman coins. 3 1924 021 438 399 Cornell University Library The original of this book is in the Cornell University Library. There are no known copyright restrictions in the United States on the use of the text. http://www.archive.org/details/cu31924021438399 f^antilioofcs of glrcfjaeologj) anU Antiquities A HANDBOOK OF GREEK AND ROMAN COINS A HANDBOOK OF GREEK AND ROMAN COINS G. F. HILL, M.A. OF THE DEPARTMENT OF COINS AND MEDALS IN' THE bRITISH MUSEUM WITH FIFTEEN COLLOTYPE PLATES Hon&on MACMILLAN AND CO., Limited NEW YORK: THE MACMILLAN COMPANY l8 99 \_All rights reserved'] ©jcforb HORACE HART, PRINTER TO THE UNIVERSITY PREFACE The attempt has often been made to condense into a small volume all that is necessary for a beginner in numismatics or a young collector of coins. But success has been less frequent, because the knowledge of coins is essentially a knowledge of details, and small treatises are apt to be un- readable when they contain too many references to particular coins, and unprofltably vague when such references are avoided. I cannot hope that I have passed safely between these two dangers ; indeed, my desire has been to avoid the second at all risk of encountering the former. At the same time it may be said that this book is not meant for the collector who desires only to identify the coins which he happens to possess, while caring little for the wider problems of history, art, mythology, and religion, to which coins sometimes furnish the only key. -

3927 25.90 Brass 6 Obols / Sestertius 3928 24.91

91 / 140 THE COINAGE SYSTEM OF CLEOPATRA VII, MARC ANTONY AND AUGUSTUS IN CYPRUS 3927 25.90 brass 6 obols / sestertius 3928 24.91 brass 6 obols / sestertius 3929 14.15 brass 3 obols / dupondius 3930 16.23 brass same (2 examples weighed) 3931 6.72 obol / 2/3 as (3 examples weighed) 3932 9.78 3/2 obol / as *Not struck at a Cypriot mint. 92 / 140 THE COINAGE SYSTEM OF CLEOPATRA VII, MARC ANTONY AND AUGUSTUS IN CYPRUS Cypriot Coinage under Tiberius and Later, After 14 AD To the people of Cyprus, far from the frontiers of the Empire, the centuries of the Pax Romana formed an uneventful although contented period. Mattingly notes, “Cyprus . lay just outside of the main currents of life.” A population unused to political independence or democratic institutions did not find Roman rule oppressive. Radiate Divus Augustus and laureate Tiberius on c. 15.6g Cypriot dupondius - triobol. In c. 15-16 AD the laureate head of Tiberius was paired with Livia seated right (RPC 3919, as) and paired with that of Divus Augustus (RPC 3917 and 3918 dupondii). Both types are copied from Roman Imperial types of the early reign of Tiberius. For his son Drusus, hemiobols were struck with the reverse designs begun by late in the reign of Cleopatra: Zeus Salaminios and the Temple of Aphrodite at Paphos. In addition, a reverse with both of these symbols was struck. Drusus obverse was paired with either Zeus Salaminios, or Temple of Aphrodite reverses, as well as this reverse that shows both. (4.19g) Conical black stone found in 1888 near the ruins of the temple of Aphrodite at Paphos, now in the Museum of Kouklia. -

Downloaded on 2019-04-30T23:20:12Z

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by Cork Open Research Archive UCC Library and UCC researchers have made this item openly available. Please let us know how this has helped you. Thanks! Title Constantine I and a new Christian golden age: a secretly Christian reverse type identified? Author(s) Woods, David Publication date 2018-09 Original citation Woods, David (2018) 'Constantine I and a New Christian Golden Age: A Secretly Christian Reverse Type Identified?' Greek, Roman and Byzantine Studies, 58, pp. 366-388. Type of publication Article (peer-reviewed) Link to publisher's https://grbs.library.duke.edu/article/view/16063 version Access to the full text of the published version may require a subscription. Rights © 2018 David Woods. http://creativecommons.org/licenses/by/3.0/ Item downloaded http://hdl.handle.net/10468/7749 from Downloaded on 2019-04-30T23:20:12Z Constantine I and a New Christian Golden Age: A Secretly Christian Reverse Type Identified? David Woods HE PURPOSE of this paper is to explore the significance of a reverse type used on solidi struck in the name of T Constantine I (306–337) alone at the mints of Nico- media, Sirmium, Ticinum, and Trier during his vicennial year starting on 26 July 325.1 This type depicts what is usually described as two interlaced wreaths surrounded by the legend CONSTANTINVS AVG ( fig. 1).2 With the exception of the issue from Trier, Constantine used this type as part of the coinage struck for donatives as he stopped in the various mint-towns during the course of his journey from Nicomedia to Rome.3 The only minor variation between the mints is that the coins from Sirmium, Ticinum, and Trier always depict a single star cen- 1 The standard catalogue of the coinage of Constantine I remains Patrick M. -

Byzantine Coinage

BYZANTINE COINAGE Philip Grierson Dumbarton Oaks Research Library and Collection Washington, D.C. © 1999 Dumbarton Oaks Trustees for Harvard University Washington, D.C. All rights reserved Printed in the United States of America Second Edition Cover illustrations: Solidus of Justinian II (enlarged 5:1) ISBN 0-88402-274-9 Preface his publication essentially consists of two parts. The first part is a second Tedition of Byzantine Coinage, originally published in 1982 as number 4 in the series Dumbarton Oaks Byzantine Collection Publications. Although the format has been slightly changed, the content is fundamentally the same. The numbering of the illustrations,* however, is sometimes different, and the text has been revised and expanded, largely on the advice and with the help of Cécile Morrisson, who has succeeded me at Dumbarton Oaks as advisor for Byzantine numismatics. Additions complementing this section are tables of val- ues at different periods in the empire’s history, a list of Byzantine emperors, and a glossary. The second part of the publication reproduces, in an updated and slightly shorter form, a note contributed in 1993 to the International Numismatic Commission as one of a series of articles in the commission’s Compte-rendus sketching the histories of the great coin cabinets of the world. Its appearance in such a series explains why it is written in the third person and not in the first. It is a condensation of a much longer unpublished typescript, produced for the Coin Room at Dumbarton Oaks, describing the formation of the collection and its publication. * The coins illustrated are in the Dumbarton Oaks and Whittemore collections and are re- produced actual size unless otherwise indicated. -

Roman Coins Elementary Manual

^1 If5*« ^IP _\i * K -- ' t| Wk '^ ^. 1 Digitized by Google Digitized by Google Digitized by Google Digitized by Google Digitized by Google Digitized by Google PROTAT BROTHERS, PRINTBRS, MACON (PRANCi) Digitized by Google ROMAN COINS ELEMENTARY MANUAL COMPILED BY CAV. FRANCESCO gNECCHI VICE-PRBSIDENT OF THE ITALIAN NUMISMATIC SOaETT, HONORARY MEMBER OF THE LONDON, BELGIAN AND SWISS NUMISMATIC SOCIBTIES. 2"^ EDITION RKVISRD, CORRECTED AND AMPLIFIED Translated by the Rev<> Alfred Watson HANDS MEMBF,R OP THE LONDON NUMISMATIC SOCIETT LONDON SPINK & SON 17 & l8 PICCADILLY W. — I & 2 GRACECHURCH ST. B.C. 1903 (ALL RIGHTS RF^ERVED) Digitized by Google Arc //-/7^. K.^ Digitized by Google ROMAN COINS ELEMENTARY MANUAL AUTHOR S PREFACE TO THE ENGLISH EDITION In the month of July 1898 the Rev. A. W. Hands, with whom I had become acquainted through our common interests and stud- ieSy wrote to me asking whether it would be agreeable to me and reasonable to translate and publish in English my little manual of the Roman Coinage, and most kindly offering to assist me, if my knowledge of the English language was not sufficient. Feeling honoured by the request, and happy indeed to give any assistance I could in rendering this science popular in other coun- tries as well as my own, I suggested that it would he probably less trouble ii he would undertake the translation himselt; and it was with much pleasure and thankfulness that I found this proposal was accepted. It happened that the first edition of my Manual was then nearly exhausted, and by waiting a short time I should be able to offer to the English reader the translation of the second edition, which was being rapidly prepared with additions and improvements. -

The Servilian Triens Reconsidered*

CRISTIANO VIGLIETTI THE SERVILIAN TRIENS RECONSIDERED* for Nicola Parise «In ancient societies, greater value was attached to conspicuous consumption than to increased production, or to the painful acquisition of more wealth». M.I. Finley (in HOPKINS 1983a, p. xiv) In the second volume of Studi per Laura Breglia, published in 1987, French historian Hubert Zehnacker gave – for the first time – systematic consideration1 to the meaning of a fascinating but challenging passage of Pliny the Elder’s Natural History: Unum etiamnum aeris miraculum non omittemus. Servilia familia inlustris in fastis trientem aereum pascit auro, argento, consumentem utrumque. origo atque natura eius incomperta mihi est. verba ipsa de ea re Messallae senis ponam: «Serviliorum familia habet trientem sacrum, cui summa cum cura magnificentiaque sacra quotannis faciunt. quem ferunt alias crevisse, alias decrevisse videri et ex eo aut honorem aut deminutionem familiae significare». (Plin. Nat. 34. 38. 137)2 We must not neglect to mention one other remarkable fact related to copper. The Servilian family, so illustrious in the lists of magistrates, nourishes with gold and silver a copper triens, which feeds on both. I was not able to verify its origin and nature; but I will relate the very words of the story as told by old Messalla: «The family of the Servilii is in possession of a sacred triens, to which they offer sacrifice yearly, with the greatest care and veneration; they say that the triens sometimes seems to increase and sometimes to decrease, and that this indicates the honour or diminishing of the family». Pliny thus concludes the first section of his thirty‐fourth Book, dedicated to copper and its alloys3, with an extraordinary and miraculous tale (miraculum)4 that for all its difficulty of * Unless otherwise stated, all the translations are mine.