Ottawa Retail Report 4Q08 1

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Five Two by Food52 Lands at Nordstrom

FOR IMMEDIATE RELEASE FIVE TWO BY FOOD52 LANDS AT NORDSTROM Nordstrom is Evolving its At Home Assortment to Feature a Brand Partnership with Food52, a leading innovator in the food, cooking, and home space SEATTLE (October 9) – Nordstrom announced today a partnership with Five Two by Food52, introducing the kitchen and home brand’s cult-favorite collection of cookware, dishware and kitchen essentials to the Nordstrom At Home assortment. Each piece from the Five Two line is thoughtfully designed with feedback from Food52’s 24 million food-loving followers, and will be available on Friday, October 9 in select Nordstrom stores in the US and Canada, as well as online at Nordstrom.com (Nordstrom.ca). Great food isn’t just about ingredients, it’s about everything that makes a meal. Five Two at Nordstrom features a curated selection of products for kitchen, home, and life created exclusively with the Food52 community. A groundbreaking and award-winning kitchen and home brand and premier destination for kitchen and home enthusiasts, Food52 is for everyone who believes food is at the center of a well-lived life. “With our customers spending more time than ever at home, we are excited to be introducing Five Two by Food52 to inspire them in the kitchen, while making the experience of cooking seamless and fun,” said Olivia Kim, Nordstrom VP of Creative Projects and Home. “As part of our partnership, we’ll be giving customers access to a curated assortment of quality kitchen essentials, exclusive Food52 content and recipes for cooking at home, along with tips and tricks from Food52 experts, trusted home cooks, editors and more.” “Five Two is the ultimate customer-centric brand—the result of a deep, two-way conversation with the Food52 community about every little detail that makes their favorite kitchen and home go-to’s so special,” said Claire Chambers, Food52 Chief Commercial Officer. -

Map Artwork Property of WHERE™ Magazine © Concept Original De WHEREMC Magazine Lac Mahon Lac Lac- Lake Grand Des-Loups Lake Lake 105 307 Mayo R

F-12 5 Lac Leamy ST. RAYMOND Edmonton 50 ER GAMELIN EB Boul. du Casino GR Vers / To Montréal Rivière des Outaouais Île Kettle Island MONTCLAIR Boul. de la Carrière B Ottawa River is so n R IE N R U Vers / To O Parc de la F Gatineau P RO QUÉBEC Park M. D Laramée E R SAINT-RAYMOND Chauveau Émile-Bond OC KC LIF ONTARIO FE The Rockeries SA Parc de Les rocailles Université CRÉ Rockcliffe -CŒ du Québec UR Park en Outauais RCMP, Canadian PR OM Police College . D Boucherville K E GRC, Collège R ALEXANDRE-TACHÉ O canadien de police C Canada Aviation AYLMER ALLUMETTIÈRES K P C o Lac and Space Museum n L L t RCMP I M McKay F Musée de l’aviation et Aéroport de a Musical F c E de l’espace du Canada MAISONNEUVE d Lake Rockcliffe Ride Centre o P Parc n Airport SAINT-JOSEPH a Centre du K ld W Park -C Carrousel a Île Green M Y r . Jacques-Cartier t ackay O ie de la GRC r Island Monument B Brid CAPITAL SIGHTS r into ges P id M LUCERNE à la paix a g s ATTRACTIONS DE LA CAPITALE P pi e t Crichton R o n ? n i et au souvenir e o d N n au ea O t P u ByWard Market HE I Rivière des Outaouais . ML T C O Gatineau DR Stanley CK IA h Marché By V Parc X Parc New A a E L’ mp Brébeuf S Edinburgh E MONTCALM S Canadian Museum of History D U Park P . -

Centre Tower, Suite 901 Toronto, on M8X 2X3 416-486-6440 Tel

Innisdale Secondary School - Civics- Ottawa 2018 Tour ID: 24807 Ottawa November 8, 2018 to November 11, 2018 Day One - Thursday, November 08, 2018 9:00 PM One-way school bus transfer One-way school bus transfer on a 47 passenger Sample Itinerary school bus. This is a sample itinerary that is completely customizable to meet your school's specific needs. The order of your activities and final cost of your Day Two - Friday, November 09, 2018 actual tour will vary depending on the activities 7:30 AM American Breakfast Buffet at the Hotel and meal plan you choose and the availability of sites. 8:30 AM Board your motor coach and depart for your next 7:00 AM Arrival at your school of a washroom equipped, activity. climate controlled, highway motor coach. 9:00 AM Visit the Canadian Museum of History 7:30 AM Board your motor coach and depart. Appropriate The building itself is an architectural masterpiece rest and meal stops will be made en route. and one of Canada's most popular and most visited museums. Journey through 1,000 years of Take Highway #407 to and from your destination. Canada’s history in life-size settings and experience the richness of Canada’s past. 2:00 PM Guided Tour at the Supreme Court of Canada 10:30 AM Visit Parliament Hill (tour information not The Supreme Court of Canada has been Canada's available) highest court of appeal since 1949. This tour will Situated on a cliff overlooking the Ottawa River, familiarize you with the Canadian judicial system the Parliament Buildings are historical monuments, and how the decisions made by the Supreme Court architectural treasures, and an important national Justices affect all Canadians. -

I FOREIGN HIGH-END RETAILERS IN

FOREIGN HIGH-END RETAILERS IN CANADA, WHERE NEXT? by Nicole Serrafero Bachelor of Science, Environmental Management and GIS University of Toronto Mississauga, Mississauga, ON Advanced Diploma, GIS for Business Concentration Nova Scotia Community College COGS Campus, Lawrencetown, NS A Major Research Paper presented to Ryerson University in partial fulfillment of the requirements for the degree of Master of Spatial Analysis in the program of Spatial Analysis Toronto, Ontario, Canada, 2017 © Nicole Serrafero, 2017 i Authors Declaration I hereby declare that I am the sole author of this MRP. This is a true copy of the MRP, including any required final revisions. I authorize Ryerson University to lend this MRP to other institutions or individuals for the purpose of scholarly research. I further authorize Ryerson University to reproduce this MRP by photocopying or by other means, in total or in part, at the request of other institutions or individuals for the purpose of scholarly research. I understand that my MRP may be made electronically available to the public. ii Foreign high-end retailers in Canada, where next? Master of Spatial Analysis, 2017 Nicole Serrafero, Spatial Analysis, Ryerson University Abstract Foreign high-end retailers have started to establish their brands in Canada. There are several locations across Canada that contain a significant number of them. Using these existing established high-end retail locations, this paper presents potential new locations for these high-end retailers to expand into. The paper deals with six of the major census metropolitan areas (CMA) in Canada: Toronto, Montreal, Vancouver, Calgary, Edmonton, and Ottawa. The demographic and household spending data at the census tract level were used to represent potential customers. -

CANADIAN SHOPPING CENTRE STUDY 2019 Sponsored By

CANADIAN SHOPPING CENTRE STUDY 2019 Sponsored by DECEMBER 2019 RetailCouncil.org “ helps Suzy Shier drive traffic and sales!” Faiven T. | Marketing Coordinator | Suzy Shier Every retailer pays significantly for marketing opportunities through their leases. However, 90% of retailers never take advantage of the benefits of these investments. Every shopping center promotes their retailers’ marketing campaigns to millions of consumers to drive traffic and sales to their retailers. Engagement Agents helps retailers drive more traffic and sales, while saving money, time and resources by making it easy to take advantage of their al ready-paid-for marketing dollars! Learn more at www.EngagementAgents.com. Also, read our article on pag e 25 of this Study! Sean Snyder, President [email protected] www.EngagementAgents.com 1.416.577.7326 CANADIAN SHOPPING CENTRE STUDY 2019 Table of Contents 1. Introduction ......................................................................................................................................................1 2. Executive Summary ........................................................................................................................3 3. T op 30 Shopping Centres in Canada by Sales Per Square Foot ...................................................................................................5 3a. Comparison: 2019 Canadian Shopping Centre Productivity Annual Sales per Square Foot vs. 2018 and 2017 ...............................................8 3b. Profile Updates on Canada’s -

1702 ONC FEBRUARY NEWSLETTER Public.Pdf

Ottawa Newcomers’ Club !!! !!!! !! !!!!!!!!!!!!!!!! !!!!!!!! A MESSAGE FROM THE PRESIDENT With the 2017 celebrations and Winterlude and all the regular ONC activities we have lots to do and lots to celebrate this year! If you haven't been down to Winterlude you must go! One year there was a massive ice castle display from Harbin, China in front of city hall. If nothing else - go for the Beaver Tails, you won't be disappointed! It is now the time of year that we start to look for replacements for the Board. This means that our Nominating Committee will be in full swing soon. !Our club operates on volunteer labour so please say “yes” if asked. !It's a great way to make new friends and to help keep the club operating at the same time!! A MESSAGE FROM THE VICE-PRESIDENT Although many of our members become “snowbirds” at this time of year all activities in ONC continue on schedule & provide us with great opportunities to connect with one another. Nothing is better to take away the wintery chill than a fun time with friends, so continue to enjoy all the activities that suit you. As always we thank our members who volunteer their time to make these activities possible. As we head into spring we begin to think about who might be willing to become a convenor for next year. If there is an activity that you might enjoy convening or co-convening, speak to the current group facilitator. ONC needs your enthusiasm, creative ideas, & energy to continue being such a successful club. -

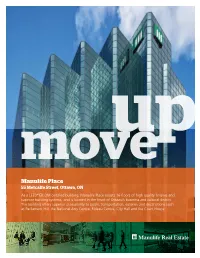

Manulife Place

moveup Manulife Place 55 Metcalfe Street, Ottawa, ON As a LEED® EB:OM certified building, Manulife Place boasts 16 floors of high quality finishes and superior building systems, and is located in the heart of Ottawa’s business and cultural district. The building offers superior accessibility to public transportation, eateries and destinations such as Parliament Hill, the National Arts Centre, Rideau Centre, City Hall and the Court House. Manulife Place 55 Metcalfe Street, Ottawa, ON moveup Building Overview ■■ 16 storey Class A+ office building totaling 327,000 SF ■■ On-site tenant-exclusive conference centre ■■ 3 level parking garage ■■ On-site cafeteria with catering services available ■■ Bicycle parking ■■ On-site car wash service ■■ 24-hour, on-site security ■■ Awarded LEED® Gold EB:OM designation (2013 and 2017) ■■ Private on-site shower facilities Questions? Contact: Louis-Bernard Bonneau, Leasing Director T: 613.238.6599 E: [email protected] Stephanie Lui, Leasing Manager T: 613.369.5584 E: [email protected] Manulife Place 55 Metcalfe Street, Ottawa, ON moveup A Superior Location Manulife Place is ideally located in the heart of Ottawa’s business and cultural district. ■■ Located at the corner of Queen Street and Metcalfe Street ■■ Within walking distance to Parliament Hill, the National Arts Centre, Rideau Centre (shopping mall), City Hall and the ■■ Convenient access to several retail, dining and hotel amenities Court House ■■ Close proximity to future LRT station KING EDWARD AVE National Gallery of Canada -

On Sparks Street

126 Sparks Street Ottawa, ON K1P 5B6 613-237-6373 [email protected] 126sparks.com Exclusive Furnished Flats and Lofts on Sparks Street 126 Sparks offers an unbeatable location in the heart of Ottawa’s historic business and retail district - just steps from Parliament Hill. The 35 exclusive furnished flats and lofts offer spacious one bedroom and one bedroom + den floor plans with private terraces overlooking the Sparks Street promenade. We specialize in flexible long and short term rentals to meet your needs. Our goal is to provide turn-key living with all the comforts of home that cater to a busy professional. Your Neighbourhood Your Destination 126 Sparks lays its foundation on Ottawa’s most storied street. Centre of business since the horse-drawn carriage. Home to Canada’s earliest parliamentarians. Its social heritage lives on today. 126 Sparks offers an enviable location with direct access to the shops and restaurants on the Sparks Street promenade in the central business district. You are also steps from Parliament Hill, ByWard Market, Elgin Street, the National Arts Centre, Rideau Centre and Major’s Hill Park. Experience all that the area has to offer on the nearby bicycle paths along the Rideau Canal. Your Amenities Map data ©2015 Google We make you feel at home – even when you are far from home - in our spacious executive 126 Sparks Street flats and lofts. You can settle into one of 35 fully furnished flats or lofts providing a boutique Ottawa, ON K1P 5B6 experience for short or extended stays. From the North: From Rue Laurier, head south toward Rue Marston. -

Men's & Women's Basketball Championship

2020 MEn’S & WOMEn’S BaSKETBaLL CHaMPIOnSHIP InFORMaTIOn BULLETIn #3 2020 Men’s & Women’s Basketball National Championship University of Ottawa & Carleton University - March 5-8, 2020 Bulletin #3 SECTION 1: GENERAL INFORMATION 1. ORGANIZING COMMITTEE POSITION NAME PHONE E-MAIL Committee President Susan Hylland 343-998-8616 [email protected] Jennifer Brenning 613-314-4453 [email protected] Athletic Director Susan Hylland 343-998-8616 [email protected] Jennifer Brenning 613-314-4453 [email protected] Coordinator Valerie Hughes 613-222-9279 [email protected] Student-athlete Danika Smith 613-462-8951 [email protected] services Medical services Nadine Smith 613-520-2600 [email protected] ext.5623 Sponsorship Matthew Bennett 613-232-6767 [email protected] x8814 Communications Michele Dion 613-562-5800 [email protected] x2413 Logistics - event Valerie Hughes 613-222-9279 [email protected] Ticketing Eric Childers 613-232-6767 [email protected] x8405 Awards & Ceremonies Bianca Lapensee 514-475-9733 [email protected] U SPORTS - Manager Scott Ring 905-508-3000 #244 [email protected] National Champs Cell : 416-553-6121 2020 Men’s & Women’s Basketball National Championship University of Ottawa & Carleton University - March 5-8, 2020 Bulletin #3 2. SCHEDULE OF EVENTS *All times are local Monday March 2nd, 2020 18:00-21:30 Players Clinic (Community) TD Place Tuesday March 3rd, 2020 19:00-21:00 3 on 3 Tournament – Ravens’ Nest 20:00-22:30 Group Sales – TD Place Wednesday March 4th, 2020 19:00- 22:00 All-Canadian Reception – Canadian Museum of History 19:00-21:00 3-Point Contest (Community) – TD Place Thursday March 5th, 2020 19:45 Opening Ceremony – TD Place Friday March 6th, 2020 17:00-20:00 Basketball Injuries: Prevention and Management – TD Place – Otto’s Saturday March 7th, 2020 8:00-22:00 Juel Basketball – Uottawa 12:00-16:00 Coach School – TD Place – Media Centre 11:00-13:00 VIP Sponsor Reception – TD Place – Otto’s Club Sunday March 8th, 2020 8:00-22:00 Juel Basketball 3. -

Ottawa Duration: 3 Days, 2 Nights Dates: June 12 – June 14, 2019 Tour Centre: Molloy-6665

COURTICE NORTH SCHOOL Destination: Ottawa Duration: 3 days, 2 nights Dates: June 12 – June 14, 2019 Tour Centre: Molloy-6665 Ottawa: Three Day Spring Tour Final itinerary prepared for Courtice North School DAY 1 - WEDNESDAY, JUNE 12 seems to be a set of clues that may help their 9:00 am Motorcoach to arrive at school escape. The faster they can work together to solve 9:30 am Board the bus the puzzle, the sooner they will be able to escape! Travel to Ottawa 5:30 pm Walk to your next activity 12:30 pm Meet your Keating Tour Guide in Kingston at 6:00 pm Holocaust Monument First Canada Inn, 1 First Canada Court, Kingston (1-613- • The Holocaust Monument recognizes the Holocaust 541-1111). (From the 401, exit at Division Street, Exit # and the incredible contribution Holocaust Survivors 617) have made to Canada. You can enter the Lunch at own expense monument. Within the lower area you will see 2:30 pm Orienteering Rally on Parliament Hill images and facts about the Holocaust, including six • Explore the statues and learn about the monuments photographic landscapes of Holocaust sites painted in Parliament Hill's open-air gallery by joining an on the walls, and a 21-panel interpretive exhibit. orienteering rally. You can also ascend to an upper terrace to see 3:30 pm Board the bus amazing views of the surrounding city and Peace 4:00 pm Check into hotel Tower. 5:00 pm Board the bus 6:30 pm Board the bus 5:30 pm Night at the Nature Museum visit 7:00 pm Dinner at Tuckers Marketplace • The natural world takes on a whole new persona 8:00 pm Tour Director led walking tour when the sun goes down. -

Revised ICE CAPADES MINI REUNION Itinerary for WINTERLUDE (Ottawa, Canada)

Revised ICE CAPADES MINI REUNION itinerary for WINTERLUDE (Ottawa, Canada) February 8th to 10th, 2008 - Official Hotel NOVOTEL (33 Nicholas Street - downtown Ottawa) Friday, February 8th 6 pm to 8 pm Meet & Greet "Welcome Cocktail Party" Hosted by Lynn Nightingale & Stephan Klovan "Gallery Bar" - off main lobby of NOVOTEL Hotel (downtown Ottawa) Dress: Casual Join us for drinks & yummy appetizers (Note: Local media will be covering this event with reporters & photographers!) 2008 WINTERLUDE "Goodie Bags" will be given out at this party! 8 pm to 11 pm Dinner "Trio Cafe" (formerly "Cafe Nicole") - next to "Gallery Bar" Excellent new menu! Wide variety of great entrees. 11 pm to 2 am Complimentary VIP admission to "Mardis Gras Party" "SUITE 34" - 34 Clarence Street, Byward Market, Ottawa Located less then a short 5 minute walk from the hotel! (This is the poshest nightclub in the National Capital!) Join us for drinks & dance the night away, with the "beautiful people"! Saturday, February 9th Morning on own to shop & explore Otttawa! 12 Noon - 2 pm Luncheon at "LE CAFE" located in the National Arts Centre Within a 5 minute walk from the NOVOTEL, this excellent restaurant is right beside the Rideau Canal and overlooks all the skaters, etc. Great lunch menu features soups, salads and light entrees. 2 pm - 4 pm Skating Party on the RIDEAU CANAL "The World's Largest Skating Rink"!!! Starts in front of the National Arts Centre at Rideau Street, right beside the "American Express Snowbowl" Bring your skates to lunch and then immediately afterwards, you can hop on the Canal for a lovely skate. -

The Meeting Spot of Choice for Political

Ottawa’s Landmark Meeting Location For over 75 years IN THE HEART OF DOWNTOWN OTTAWA the meeting spot of choice Lord Elgin represents that rare occurrence when for political, corporate, conveniences, comfort, service and style come together cultural and social to deliver meetings at another level communities in Ottawa. Business thrives at Lord and conference facilities, include Elgin with major government seven boardrooms and seven departments, crown conference rooms, most with corporations, corporate natural lighting. headquarters and Ottawa’s largest convention facility – Grill 41 Restaurant serves up the 192,000 square foot Shaw internationally influenced cuisine Centre a 5-minute walk away. and a Starbucks Café is on-site. Guests can relax and rejuvenate Lord Elgin guests enjoy 353 in the indoor lap pool, whirlpool, rooms and 2 suites bathed in the sauna and fitness centre. natural light and meticulously renovated in 2017. Lord Elgin’s 13,000 square feet of meeting LordElginHotel.ca 100 Elgin Street, Ottawa, ON K1P 5K8 | Tel: (613) 235-3333 Toll Free: 1-(800) 267-4298 (Canada & US) | Fax: (613) 235-3223 CONVENIENCE, COMFORT, SERVICE IN LANDMARK STYLE Board Rooms Lord Elgin Offers Steps Outside Lord Elgin • 13,000 Square Feet of • National Arts Centre Meeting & Conference Space • Shaw Centre • Ideal for groups from 10 – 250 • Confederation Park • 2 Ballroom Options (all season festivals) • 7 Meeting Room Options • Rideau Centre • 8 Boardroom Options (Over 180 Shops) • Business Centre • Rideau Canal • Meeting Professionals On Staff • Parliament Hill • Hi-Speed Internet in All Rooms • Sparks Street Mall • Free local calls (Canada’s largest • 355 Newly Renovated Rooms pedestrian mall) • 2 Luxurious Suites • National Gallery of Canada • Grill 41 Restaurant • Byward Market • Outdoor Patio (prime entertainment area) • Starbucks Café • Elgin Street 200 400, 500 600, 700, 800 • Lap Pool, Sauna, Whirlpool (restaurant row) & Fitness Room Capacities MEETING Rooms * Includes space for Audio-Visual Presentations EVENTS Function Room Sq.