Mayora Indah Tbk (MYOR) Overweight

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Ulker Gida HOLD

Equity Research - TURKEY June 27, 2007 Confectionery ULKER TI Initiating Coverage Ulker Gida HOLD NEUTRAL FLAVOUR Market Value We initiate coverage of Ulker Gida with a HOLD rating, as we Close (TRY / $)* 5.65 / 4.28 believe current price levels largely reflect the Company’s Current MCap.* TRY 1362 mn prospects. The key elements of our recommendation may be Target Value summarised as follows: 1) Moderate topline growth -- We expect Target Price (TRY) TRY 6.45 Ulker Gida’s topline to grow slightly above Turkey’s GDP within Upside (Downside) 14% 2007-2016. Note that, with a conservative approach, our model Capitalisation excludes potentially value-accretive plans that are on the Company’s agenda, due to a lack of crucial data. 2) Conservative Enterprise Val. TRY 1343 mn improvement in EBITDA margin -- We expect the EBITDA margin Net Debt TRY 121 mn improvement to be 0.4 pp on average within 2008-2016, due to the Minority Interest TRY 184 mn Company’s moderate pricing policy. 3) Fair valuation -- Our 12- Financial Assets TRY 325 mn month per share target price of TRY6.45 represents 14% upside. Number of Shares 241 mn Although the stock is trading at a 15% average discount to its Free Float 29% international peers based on 2007E/2008E P/E and EV/EBITDA Performance multiples, our DCF model points to 11% upside. Avg. Daily Vol. $5.2 mn Topline growth slightly above GDP -- The biscuit consumption level per capita Life H/L ($) 6.10 / 0.20 52w H/L (TRY) 6.19 / 2.95 in Turkey, which is mostly related with GDP per capita level and consumption habits, is significantly below European norms. -

Tuesday July 30, 1996

7±30±96 Tuesday Vol. 61 No. 147 July 30, 1996 Pages 39555±39838 federal register 1 II Federal Register / Vol. 61, No. 147 / Tuesday, July 30, 1996 SUBSCRIPTIONS AND COPIES PUBLIC Subscriptions: Paper or fiche 202±512±1800 FEDERAL REGISTER Published daily, Monday through Friday, Assistance with public subscriptions 512±1806 (not published on Saturdays, Sundays, or on official holidays), by General online information 202±512±1530 the Office of the Federal Register, National Archives and Records Administration, Washington, DC 20408, under the Federal Register Single copies/back copies: Act (49 Stat. 500, as amended; 44 U.S.C. Ch. 15) and the Paper or fiche 512±1800 regulations of the Administrative Committee of the Federal Register Assistance with public single copies 512±1803 (1 CFR Ch. I). Distribution is made only by the Superintendent of Documents, U.S. Government Printing Office, Washington, DC FEDERAL AGENCIES 20402. Subscriptions: The Federal Register provides a uniform system for making Paper or fiche 523±5243 available to the public regulations and legal notices issued by Assistance with Federal agency subscriptions 523±5243 Federal agencies. These include Presidential proclamations and For other telephone numbers, see the Reader Aids section Executive Orders and Federal agency documents having general applicability and legal effect, documents required to be published at the end of this issue. by act of Congress and other Federal agency documents of public interest. Documents are on file for public inspection in the Office of the Federal Register the day before they are published, unless earlier filing is requested by the issuing agency. -

Laporan Praktik Kerja Lapangan Pada Divisi Candy

LAPORAN PRAKTIK KERJA LAPANGAN PADA DIVISI CANDY PT.MAYORA INDAH JATAKE 1 HANIFAH RAHMAWATI WIJAYA 8143154838 Laporan Praktik Kerja Lapangan ini ditulis untuk memenuhi salah satu persyaratan mendapatkan Gelar Ahli Madya pada Fakultas Ekonomi Universitas Negeri Jakarta PROGRAM STUDI DIII ADMINISTRASI PERKANTORAN FAKULTAS EKONOMI UNIVERSITAS NEGERI JAKARTA 2018 LEMBAR EKSEKUTIF Hanifah Rahmawati Wijaya. 8143154838. Laporan Praktik Kerja Lapangan pada Divisi Candy PT. Mayora Indah Jatake 1 . Program Studi D3 Administrasi Perkantoran, Fakultas Ekonomi, Universitas Negeri Jakarta. 2018. Laporan Praktik Kerja Lapangan ini dibuat sebagai gambaran hasil selama satu bulan praktikan melakukan kegiatan Praktik Kerja Lapangan. Tujuan utama dari kegiatan Praktik Kerja Lapangan ini agar praktikan mendapat pengalaman dan mengenal untuk beradaptasi dalam dunia kerja sesuai dengan bidang praktikan yaitu Administrasi Perkantoran. Praktikan melakukan kegiatan PKL pada Divisi Candy PT. Mayora Indah Jatake 1 departemen Administrasi Produksi dan Administrasi Payroll. Yang berlokasi di Jalan Telesonik Jatake 1 Tangerang dimulai pada tanggal 15 Januari 2018 sampai dengan 15 Februari 2018. Pekerjaan yang praktikan lakukan selama kegiatan Praktik Kerja Lapangan antara lain Mengarsipkan dokumen , Menggandakan Dokumen, Mengoreksi data, dan Mengoperasikan Libre Office. Dalam pelaksanaan kegiatan Praktik Kerja Lapangan, praktikan menghadapi beberapa kendala yang menghambat kinerja praktikan. Kendala yang dihadapi adalah sulitnya menemukan kembali arsip pada administrasi -

BIG CHALLENGES BIG SOLUTIONS 2121 Pennsylvania Avenue, NW Washington, DC 20433 USA IFC FINANCIALS and PROJECTS 2014

2014 2014 IFC Financials and Projects 2014 CREATING OPPORTUNITY WHERE IT’S NEEDED MOST BIG CHALLENGES BIG SOLUTIONS 2121 Pennsylvania Avenue, NW Washington, DC 20433 USA IFC FINANCIALS AND PROJECTS 2014 202 473 3800 ifc.org Big Challenges. Solutions. 2014 2014 TABLE OF CONTENTS MANAGEMENT’S DISCUSSION AND ANALYSIS 2 Executive Summary 2 Client Services 5 Liquid Assets 11 Funding Resources 11 Risk Management 13 Critical Accounting Policies 18 Results of Operations 20 Governance and Control 26 CONSOLIDATED FINANCIAL STATEMENTS AND INTERNAL CONTROL REPORTS 30 Management’s Report Regarding Effectiveness of Internal Control over External Financial Reporting 30 Auditors’ Report on Management’s Assertion on Effectiveness of Internal Control over External Financial Reporting 32 Consolidated Balance Sheets 34 Consolidated Income Statements 35 Consolidated Statements of Comprehensive Income 36 Consolidated Statements of Changes in Capital 37 Consolidated Statements of Cash Flows 39 Consolidated Statement of Capital Stock and Voting Power 41 Notes to Consolidated Financial Statements 42 Independent Auditors’ Report 100 PROJECT COMMITMENTS 103 INVESTMENT PORTFOLIO — CUMULATIVE GROSS COMMITMENTS BY REGION 124 NOTES AND DEFINITIONS 128 IFC Financials and Projects 2014 2 MANAGEMENT’S DISCUSSION AND ANALYSIS I. EXECUTIVE SUMMARY and other derivative instruments. The Management’s Discussion and Analysis contains forward looking statements which may be International Finance Corporation (IFC or the Corporation) is the identified by such terms as “anticipates,” “believes,” “expects,” largest global development institution focused on the private sec- “intends,” “plans” or words of similar meaning. Such statements tor in developing countries. Established in 1956, IFC is owned by involve a number of assumptions and estimates that are based on 184 member countries, a group that collectively determines its poli- current expectations, which are subject to risks and uncertainties cies. -

Kim Teck Cheong Consolidated Berhad

KIM TECK CHEONG CONSOLIDATED BERHAD PRESS RELEASE FOR IMMEDIATE RELEASE KIM TECK CHEONG SECURES DISTRIBUTORSHIP FOR KOPIKO AND OTHER PRODUCTS KOTA KINABALU, MALAYSIA – 13 MARCH 2017 Kim Teck Cheong Distribution Sdn Bhd, a wholly-owned subsidiary company of Kim Teck Cheong Consolidated Berhad (“KTC” or the “Group”) was appointed by Premium United Foods Sdn Bhd as a distribution partner to distribute a range of products such as coffee candy, coffee, chocolate, biscuits and other products. The agreement allows Kim Teck Cheong Distribution Sdn Bhd to distribute products under the brand names of Kopiko, Choki Choki, Danisa Butter Cookies and others. Key products to be distributed include the following: 1. Kopiko Products 2. Choki Choki KIM TECK CHEONG CONSOLIDATED BERHAD 3. Danisa Butter Cookies “KTC continues to strive for more sole distributorships. We strongly believe that product diversity and product quality will enable our Group to value add to all our consumers and expand our distribution channels. We will continue to increase our distributorships and distribution points,” commented Mr. Dexter Lau, Executive Director of KTC. ***** About Premium United Foods Sdn Bhd Premium United Foods Sdn Bhd (“PUF”) was incorporated on 27 April 1991. The company is principally engaged in distribution of confectioneries and beverages in Malaysia. The company has several distributors that supply to over 10,000 retail outlets across Peninsular and East Malaysia. The company provides a wide range of quality products such as coffee, candy, chocolate, biscuits and wafers which are well-known household brands such as Kopiko Coffee Candy, Kopiko coffee, Choki-Choki chocolate paste, Danisa Butter Cookies, Roma coconut biscuits, Slai O Lai jam filled biscuits and Go Cheese Wafers. -

Food Processing Ingredients Update 2016

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY Required Report - public distribution Date: 12/20/2016 GAIN Report Number: ID1639 Indonesia Food Processing Ingredients Food Processing Ingredients Update Approved By: Ali Abdi Prepared By: Fahwani Y. Rangkuti and Thom Wright Report Highlights: The Indonesian food processing market offers opportunities for U.S. food and ingredient suppliers with an estimated 2017 population of 261 million. In 2015, the product value of Indonesia’s large and medium food and beverage processing industry was $92.3 billion (IDR 1,238 trillion). The Indonesian food processing industry produces food products catering to all levels of consumers. Several factors contributing to the growth of the food processing industry are the introduction of new flavors and products with variant package sizes, a growing middle class, aggressive promotional activities, the growth of modern retail outlets, and growing health awareness. U.S. exporters face competition from neighboring ASEAN countries, China, Australia, New Zealand, and Europe. Post: Jakarta Executive Summary: I. MARKET SUMMARY The Indonesian food processing industry offers significant market potential for U.S. food and ingredient suppliers, serving a population of 261 million people in 2017. In 2015, the product value of Indonesia’s large and medium food and beverage processing industry was estimated at IDR1, 238 trillion ($92.3 billion). The value of raw materials used by large and medium processors in 2015 was IDR 791.8 trillion ($59.0 billion). According to the National Statistical Agency (BPS), there were approximately 5,700 large and medium- sized food production companies with 765,000 employees and 1.61 million micro and small scale food production companies with 3.75 million employees in 2015. -

Innovate Indonesia Unlocking Growth Through Technological Transformation March Section Section Section Section Section Section

INNOVATE INDONESIA UNLOCKING GROWTH THROUGH TECHNOLOGICAL TRANSFORMATION MARCH SECTION SECTION SECTION SECTION SECTION SECTION Innovate Indonesia Unlocking Growth Through Technological Transformation New technologies present governments with opportunities and challenges in a range of key policy areas such as employment, competitiveness, equity, and sustainability. A consensus is that the national The critical role of An in-depth understanding government can play an important role in stimulating innovation. This report explores policy options to A multidisciplinary study technology transformation of technology and Indonesia’s position in the A “deep dive” into facilitate Indonesia’s technological transformation and unlock its economic growth potential. integrating evidence in boosting Indonesia’s sector-specifi c opportunities technological transformation Industry 4.0 in Five pillars for and expertise… economic development and challenges journey Indonesia policy action About the Asian Development Bank ADB is committed to achieving a prosperous¥ inclusive¥ resilient¥ and sustainable Asia and the Pacifi c¥ Economic analysis, Variety of technologies The government has taken important Photonics steps to support technology while sustaining its e orts to eradicate extreme poverty¦ Established in §¨©©¥ it is owned by ©ª members review of previous • • Bio transformation, including: Advanced —¬¨ from the region¦ Its main instruments for helping its developing member countries are policy dialogue¥ studies and guidance from academic • Nano • -

Food Processing Ingredients

Required Report: Required - Public Distribution Date: March 26, 2021 Report Number: ID2021-0013 Report Name: Food Processing Ingredients Country: Indonesia Post: Jakarta Report Category: Food Processing Ingredients Prepared By: Novi Yuningsih Approved By: Garrett Mcdonald Report Highlights: Indonesia currently imports 62 percent of raw materials for its growing food processing industry. The market presents significant opportunities for a range of U.S. agricultural products, including soybeans, wheat, dairy, distillers’ grains, fresh fruit, and beef and beef products. De-spite tariff disadvantages, the U.S. remains Indonesia’s largest supplier of agricultural products, exporting nearly $3 billion of products in 2020. THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY Post: Jakarta Market Fact Sheet: Indonesia Food Service Industry Executive Summary The foodservice sector’s total contribution to GDP was about $23 billion (Rp319.5 trillion) in 2020. The Indonesia is the fourth most populous nation in the world, with a population of approximately 270 sector is dominated by small restaurants and street- million in 2020. Fifty-six percent of the population is side restaurants known as warungs. on Java island, one of the most densely populated Quick Facts for 2020 areas in the world. In 2020, Indonesia’s GDP Agricultural Product Imports: $19.4 billion reached $1,055 billion and GDP/capita reached U.S. Share (16%) – $3.0 billion $3,907(est.). Indonesia is a major producer of rubber, Consumer-Oriented Product Imports: $6.3 billion palm oil, coffee, and cocoa. In 2020, agricultural U.S. -

Mayora Indah (MYOR) : Mengambil Keuntungan Dari Beberapa Berita Positif"

Indonesia | Riset Retail | 12 Januari 2021 Review Dow Jones kemarin malam.. Wall Street kompak memerah pada akhir perdagangan Senin (11/1) lantaran investor melakukan aksi ambil untung setelah Wall Street mencetak rekor pekan lalu, di tengah penantian musim laporan keuangan. Indeks Dow Jones Industrial Average melemah 89,28 poin atau 0,29% ke 31.008,69, S&P 500 turun 25,07 poin atau 0,66% ke 3.799,61 dan Nasdaq Composite melorot 165,55 poin atau 1,25% ke 13.036,43. Dari 11 sektor utama di indeks S&P 500, sektor kebijakan konsumen dan layanan komunikasi mencatatkan persentase penurunan terbesar. -Kontan Ideas of the day | Trendspotter Indeks Harga Saham Gabungan (IHSG) Resistance 2 6430 Resistance 1 6402 Support 1 6330 Support 2 6290 Saham UNTR Saham MIKA Saham TOWR Resistance 2 : 27450 Resistance 2 : 2900 Resistance 2 : 1005 Resistance 1 : 27000 Resistance 1 : 2860 Resistance 1 : 975 Support 1 : 26550 Support 1 : 2820 Support 1 : 960 Support 2 : 26100 Support 2 : 2720 Support 2 : 945 Mayora Indah (MYOR) : Mengambil keuntungan dari beberapa berita positif" • Penjualan 4Q20F kemungkinan menurun karena melemahnya ekspor kemungkinan besar tidak diimbangi oleh penjualan lokal yang kuat. Margin yang berisiko, kemungkinan mendorong laba bersih (NP) turun sekitar 30-40% secara year-on-year (yoy). • Kami memangkas EPS sebesar 2-7% di FY20-22F mencerminkan asumsi penjualan yang lemah, dengan potensi risiko negatif ke margin karena melonjaknya harga komoditas. • Sementara fundamental MYOR yang kuat, kinerja harga saham outperformed, naik c.40% secara yoy, menunjukkan banyak berita positif yang dihargai. Kami Downgrade ke Hold dari Add dengan target harga ke Rp2,900/lembar. -

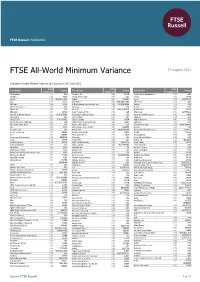

FTSE All-World Minimum Variance

2 FTSE Russell Publications 19 August 2021 FTSE All-World Minimum Variance Indicative Index Weight Data as at Closing on 30 June 2021 Index Index Index Constituent Country Constituent Country Constituent Country weight (%) weight (%) weight (%) 3M Company 0.1 USA Ajinomoto Co 0.05 JAPAN Annaly Capital Management 0.07 USA 3M India 0.02 INDIA Akamai Technologies 0.14 USA Anritsu 0.03 JAPAN a2 Milk 0.03 NEW ZEALAND Akbank 0.01 TURKEY Ansell 0.02 AUSTRALIA A2A 0.01 ITALY Akzo Nobel 0.02 NETHERLANDS ANSYS Inc 0.08 USA ABB India 0.04 INDIA Al Rajhi Banking & Investment Corp 0.04 SAUDI ARABIA Anthem 0.08 USA Abbott Laboratories 0.09 USA Albemarle 0.06 USA Aon plc 0.09 USA AbbVie Inc 0.11 USA Alcon AG 0.02 SWITZERLAND Aozora Bank 0.03 JAPAN ABC-Mart 0.03 JAPAN Aldar Properties PJSC 0.02 UAE APA Group 0.02 AUSTRALIA Abdullah Al Othaim Markets 0.04 SAUDI ARABIA Alexandria Real Estate Equity 0.09 USA Apollo Hospitals Enterprise 0.04 INDIA Abiomed Inc 0.11 USA Alexion Pharm 0.12 USA Apple Inc. 0.09 USA Aboitiz Power 0.02 PHILIPPINES Alfresa Holdings 0.02 JAPAN Applied Materials 0.06 USA Abu Dhabi Commercial Bank 0.02 UAE Alibaba Pictures Group (P Chip) 0.02 CHINA Aptiv PLC 0.04 USA Abu Dhabi Islamic Bank 0.03 UAE Align Technology Inc 0.05 USA Arab National Bank 0.03 SAUDI ARABIA ACC 0.04 INDIA Alimentation Couche-Tard B 0.02 CANADA Aramark 0.04 USA Accenture Cl A 0.09 USA Alinma Bank 0.04 SAUDI ARABIA Arca Continental SAB de CV 0.03 MEXICO Accton Technology 0.03 TAIWAN A-Living Services (H) 0.02 CHINA Arcelik 0.01 TURKEY Acer 0.04 TAIWAN Alkem Laboratories -

MAYORA RESULT for the PERIOD ENDED 30 June 2021

Company Release |30 July 2021 MAYORA RESULT FOR THE PERIOD ENDED 30 June 2021 Share (as of 30 June 2021) PT MAYORA INDAH TBK (MYOR), one of the Last Price 2,320 largest FMCG Company in Indonesia with Market Cap. 51.9 Tn presence more than 100 countries around the world, reported its unaudited consolidated financial statement for the period ended 30 June 2021 Financial Highlights (IDR Bn) 1H20 1H21 Var The Company recorded an increase in the Revenue 11.082 13.154 18.7% Revenue as impact of Economic recovery both Gross Profit 3.379 3.593 6.3% local and export market despite there’s a second wave COVID-19 in Indonesia and several export Operating Profit 1.216 1.246 2.4% destination countries. Company revenue grew by Net Profit 962 960 (0.2%) 18.7% yoy to IDR 12.2 Tn from IDR 11.1 Tn. Product mix, Increase in raw material as impact of Cash 3.448 3.741 8.5% increase in commodity prices and increase in Debt 4.328 3.846 (12.2%) packaging material resulted stable Company Net NET Debt 880 105 Profit to IDR 960 Bn compared to last year. NET DER 0.08x 0.01x Going forward, Mayora will focus on the Right things (Right SKU, Right Geography, and Right Contact Channel), preparing adjustment price per gram if PT MAYORA INDAH TBK necessary to maintain our profitability, and more Gedung Mayora selective in advertising & promotions activities. Jl. Tomang Raya Kav 21 – 23 Jakarta Barat Various strategic initiatives and innovations Phone : +62 (21) 806 377 04 carried out by the Company will improved our dominations in the market and financial Email : [email protected] performance. -

Mayora Indah

Indonesia Company Guide Mayora Indah Version 5 | Bloomberg: MYOR IJ | Reuters: MYOR.JK Refer to important disclosures at the end of this report DBS Group Research . Equity 16 Nov 2017 HOLD Wait for better entry point Last Traded Price ( 15 Nov 2017): Rp2,060 (JCI : 5,972.30) Price Target 12-mth: Rp2,000 (-3% downside) (Prev Rp1,800) Cutting earnings forecast; Hold call unchanged. We cut our net profit forecasts by 9%/7% for FY17F/18F following lower than Analyst expected results in 9M17. 2017 has been a challenging year for Tiesha PUTRI +6221 30034931 [email protected] Andy SIM CFA +65 6682 3718 [email protected] consumer companies in general given the subdued demand environment with low-end consumers cutting spending on non- What’s New basic F&B items. Our recent meeting with management suggests that Mayora Indah (MYOR) has seen its domestic and Cutting FY17F/18F earnings forecast by 9%/7% following weaker than expected 9M17 results export sales improving recently. On the margin side, the company sees some support from lower coffee price. We expect Management targets 10% revenue growth in FY18 earnings growth to pick up in FY18 as household demand improves while soft commodity price trends remain favourable Risk of further consensus’ earnings downgrade looms for MYOR. However, we think the valuation is rich at 30x PE Maintain Hold with a higher TP of Rp2,000 after rolling 18F and we see downside risk to consensus’ earnings forecast over valuation base to 2018 following the weaker than expected results. Maintain Hold.