Human Capital Management Industry Update Winter 2019

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

TCPID Update February 2020

Update from the Trinity Centre for People with Intellectual Disabilities School of Education, Trinity College Dublin February 2020 Trinity College Dublin, The University of Dublin Update from the Trinity Centre for People with Intellectual Disabilities, School of Education, Trinity College Dublin February 2020 Dear Partners, Thank you all as always for your continued support for the Trinity Centre for People with Intellectual Disabilities. We now have more than 30 TCPID Business Partners and Business Patrons which is an incredible achievement and something that we are very grateful to you all for. Thanks to your very generous support, we are able to secure the future of the TCPID and create many exciting opportunities for our students and graduates. We launched our TCPID online mentor training programme at the end of last year. We hope that you have found it useful so far and we would greatly welcome any feedback that you may have at any stage. We are very much looking forward to continuing working with you all in 2020. Here are just a few of our highlights over the past few months here in the TCPID. With warmest thanks as always for your support, TCPID Pathways Coordinator Email: [email protected] Tel: 01 8963885 Please follow all our latest news on our website at www.tcd.ie/tcpid as well as on Facebook @InclusionTCD, Twitter @IDTCD Instagram inclusiontcd as well as on LinkedIn www.linkedin.com/school/inclusiontcd Trinity College Dublin, The University of Dublin ASIAP Graduation Dr. Mary-Ann O’Donovan, Course Coordinator and Assistant Professor in Intellectual Disability and Inclusion: Friday January 31st 2020 was a very proud day for all of us in the TCPID as it was graduation day for our Level 5 Certificate in Arts, Science and Inclusive Applied Practice. -

CPL Resources

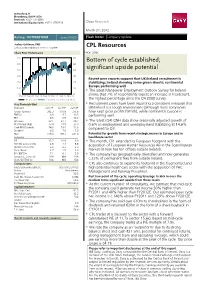

www.davy.ie Bloomberg: DAVY<GO> Research: +353 1 6148997 Institutional Equity Sales: +353 1 6792816 Davy Research March 21, 2012 Rating: OUTPERFORM Issued 30/06/09 Flash Note: Company update Joshua Goldman, PhD [email protected] / +353 1 6148997 CPL Resources Share Price Performance Price: 298c 350 300 Bottom of cycle established; 300 260 significant upside potential 250 220 200 180 Recent peer reports suggest that UK/Ireland recruitment is 150 140 stabilizing; Ireland showing some green shoots; continental Europe performing well 100 100 • The latest Manpower Employment Outlook Survey for Ireland 50 60 Mar 09 Sep 09 Mar 10 Sep 10 Mar 11 Sep 11 Mar 12 shows that 7% of respondents expect an increase in headcount, CPL price (c) Rel to ISEQ overall index (rhs) the highest percentage since the Q4 2008 survey. Key financials (€m) • Recruitment peers have been reporting a consistent message that Year end Jun12E Jun13F Jun14F UK/Ireland is a tough environment (although most companies Group Turnover 292.3 310.9 335.8 have kept gross profits flattish), while continental Europe is EBITDA 8.9 9.7 10.5 performing well. PBT 8.9 9.5 10.4 EPS Basic 23.1 27.1 29.7 • The latest (Q4) QNH data show seasonally adjusted growth of EPS Diluted (Adj) 23.4 27.5 30.0 0.6% in employment and unemployment stabilizing at 14.6% Cash EPS (Diluted) 24.9 29.0 31.6 compared to Q3. Dividend 6.0 7.0 7.0 NBV 179.0 198.7 221.0 Potential for growth from recent strategic moves in Europe and in Valuation healthcare sector P/E 12.7 10.9 9.9 • This month, CPL extended its European footprint with the FCF Yld (pre div) (%) 2.8 7.4 8.8 Dividend Yield (%) 2.0 2.3 2.3 acquisition of European Human Resources AB in the Scandinavian Price / Book 1.7 1.5 1.3 market (it now has ten offices outside Ireland). -

Employing People with Intellectual and Developmental Disabilities

Employing People with Intellectual and Developmental Disabilities A Report by the Institute for Corporate Productivity (i4cp) Talent that drives business results pg. 7 A ready pool of ideal workers pg. 10 A good fit that exceeds expectations pg. 12 Fewer challenges and more support than expected pg. 16 Employers featured: In partnership with: Peers. Research. Tools. Data. © 2014 by the Institute for Corporate Productivity (i4cp). All rights reserved. No part of this publication may be reproduced, distributed, or transmitted in any form or by any means, including photocopying, recording, or other electronic or mechanical methods, without the prior written permission of the publisher, except in the case of brief quotations embodied in critical reviews and certain other noncommercial uses permitted by copyright law. For permission requests, write to i4cp.com/contact. i4cp RESEARCH Chief Research and Marketing Officer: Kevin Martin Senior Vice President of Research: Jay Jamrog Senior Researcher: Joe Jamrog Data Analyst and Survey Manager: Andrew Dixon i4cp EDITORIAL Managing Editor & Director of Research Services: Lorrie Lykins Creative Director & Senior Editor: Eric Davis Employing People with Intellectual and Developmental Disabilities FOREWORD Anthony Kennedy Shriver For over 25 years, Best Buddies International has focused its efforts on the inclusion of individuals with intellectual and developmental disabilities (IDD). Tremendous progress has been made in creating opportunities for friendships between people with and without IDD in middle schools, high schools, and colleges. Further expansion has taken place with our Citizens program, and people in communities around the world are experiencing the gifts that come from building meaningful relationships with people with IDD. -

Scheme Document. the Scheme Meeting Will Start at 12 Noon on That Date and the EGM at 12.15 P.M

174368 Proof 6 Tuesday, November 24, 2020 22:39 THIS DOCUMENT IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTION. If you are in any doubt about the contents of this Scheme Document and what action you should take, you should consult your stockbroker, bank manager, solicitor, accountant or other independent financial adviser who, if you are taking advice in Ireland, is authorised or exempted under the European Union (Markets in Financial Instruments) Regulations 2017 (S.I. No. 375 of 2017) or the Investment Intermediaries Act 1995 (as amended) or, if you are taking such advice in the United Kingdom, is authorised pursuant to the Financial Services and Markets Act 2000 of the United Kingdom or, if you are taking advice elsewhere, is an appropriately authorised independent financial adviser. If you have sold or otherwise transferred all your Cpl Shares, please send this Scheme Document and the accompanying documents at once to the purchaser or transferee, or to the stockbroker, bank or other agent through whom the sale or transfer was effected for delivery to the purchaser or transferee. The release, publication or distribution of this Scheme Document in or into jurisdictions other than Ireland and the United Kingdom may be restricted by law and therefore persons into whose possession this Scheme Document comes should inform themselves about and observe such restrictions. Any failure to comply with these restrictions may constitute a violation of the securities laws of any such jurisdiction. To the fullest extent permitted by applicable Law, the companies involved in the Acquisition disclaim any responsibility or liability for the violation of any such restrictions by any person. -

Manpowergroup Employment Outlook Survey Global

ManpowerGroup Employment Outlook Survey Global Q1 2018 SMART JOB NO: 16003 QUARTER 1 2018 CLIENT: MANPOWERGROUP SUBJECT: MEOS Q118 – GLOBAL – TWO COLOUR – A4 SIZE: A4 DOC NAME: 16003_Global_2COL_A4_Q118 PAGE: 1 ARTWORK SIZE: 297mm x 210mm DATE: 23.11.17 87 CHARTERHOUSE STREET • LONDON EC1M 6HJ • TEL +44 (0)20 7553 4744 ManpowerGroup interviewed nearly 59,000 employers across 43 countries and territories to forecast labor market activity in Quarter 1 2018. All participants were asked, “How do you anticipate total employment at your location to change in the three months to the end of March 2018 as compared to the current quarter?” (Additional details on page 2) Contents Global Employment Outlook 1 International Comparisons – Americas 3 International Comparisons – Asia Pacific 7 International Comparisons – EMEA 10 About the Survey 17 About ManpowerGroup® 18 Global Employment Outlook SMART JOB NO: 16003 QUARTER 1 2018 CLIENT: MANPOWERGROUP SUBJECT: MEOS Q118 – GLOBAL – TWO COLOUR – A4 SIZE: A4 DOC NAME: 16003_Global_2COL_A4_Q118 PAGE: 2 ARTWORK SIZE: 297mm x 210mm DATE: 23.11.17 87 CHARTERHOUSE STREET • LONDON EC1M 6HJ • TEL +44 (0)20 7553 4744 Global Employment Outlook Qtr on Qtr Change Yr on Yr Change Quarter 1 2018 Q4 2017 to Q1 2018 Q1 2017 to Q1 2018 Quarter 1 2018 Net Employment Outlook % -15-10 -5 0510 15 20 25 30 35 40 45 Americas Taiwan +25% Argentina 9 (8)1 2 (0)1 2 (2)1 Japan +24% Brazil 5 (6)1 4 (4)1 13 (13)1 India +22% Canada 8 (11)1 2 (1)1 2 (1)1 United States +19% Colombia 5 (9)1 -2 (2)1 -1 (0)1 + Costa Rica 20 (18)1 3 (-1)1 -

Hrexecutive.Com September 2019

SEPTEMBER 2019 • $ 8 . 9 5 Chief People Officer David Fairhurst is playing a key role as the storied brand adapts to a changing business. McDonald’s PAGE 14 New Golden Age What Drives The Case for a HR’s Elite: Tech Adoption? Specialty-Drug Strategy Class of 2018 Page 18 Page 25 Page 28 H9-19p01_FC.indd 1 8/8/2019 2:09:35 PM B:10.625” T:10.25” S:9.375” B:13.875” S:12.75” T:13.5” “I’m working for beauty that begins with nature.” — Valerie Vilbon, Boutique Manager L’Occitane en Provence The things we work for are what define us. At ADP we’re designing a better way to work, so you can achieve what you’re working for. HR, Talent, Time Management, Benefits & Payroll. Informed by data and designed for people. Learn more at design.adp.com ADP, the ADP logo, and Always Designing for People are trademarks of ADP, LLC. H9-19p02_ADP.indd 2 8/5/2019 2:42:51 PM HN16425_ADP168_M02.indd Created: 6-18-2019 5:32 PM 1_Final Path:Premedia:Prepress:_ADP:2019:16425_ADP168:Final:Prepress:HN16425_ADP168_M02.indd Modified:6-19-2019 10:19 AM Proof Job Description Mechanical Specifications Colors Font Families Contacts Initial Date Billing#: HN16425 Artist: Jorge.Soto Cyan Taub Sans (Light, Regular Italic, Regular, Medium; OpenType) Studio Manager H. WEINTRAB/M. JOHNSON Labor: HN16425 Previous: Chin.Liew Magenta Proofreader None Proofreading: HN16425 Bleed: 10.625” x 13.875” Yellow Print Producer Arianna Talan OOP: HN16425 Trim: 10.25” x 13.5” Black Account Executive None Tracking#: ADP168_M02 Safety: 9.375” x 12.75” Art Director None Client: ADP Viewing: None Copywriter None Brand: None Gutter: None Product: None Scale: None Media: Magazine Final Size10.25 x 13.5 Caption: L’Occitane Links Mode PPI Links Mode PPI Production Notes ADP_ADP168_01b_SW_LOccitane_a0561_V1.tif 1672 ppi CMYK None adp_logo_tagline_0111.eps RELEASE_STAMP.ai Please contact Arianna Talan at 212.886.4100 with any questions regarding these materials. -

2020 Milwaukee Business Journal Insert

COMMUNITY PARTNER RECOGNITION 2020 COMMUNITY CAMPAIGN Every year, thousands of organizations support United Way’s Publication Sponsor: Community Campaign through workplace campaigns, corporate gifts, sponsorships, and more. We thank everyone who helped create lasting change in our community. You are the example of what it means to Live United. THANK YOU 2020 COMMUNITY CAMPAIGN ALL-STARS TOTAL COMBINED GIVING $4.8 MILLION $3.6 MILLION $3.4 MILLION $3.2 MILLION $2.5 MILLION $2.3 MILLION $1.8 MILLION $1.7 MILLION $1.6 MILLION $1 MILLION $1 MILLION UnitedWayGMWC.org Thank you to all the organizations who ran a workplace campaign and/or supported 2020 TOTAL COMBINED GIVING United Way with a sponsorship, in-kind donation, corporate gift, foundation gift, or treasury gift. SUPER STARS Meijer GUARDIAN raSmith Michael Best & Friedrich LLP Regal Beloit Corporation - Grafton $500,000 - $999,999 Milwaukee County $10,000 - $24,999 Rite Hite Corporation Foundation Milwaukee Journal Sentinel Rogers Behavioral Health Foundation Children’s Wisconsin Advicent Pieper Electric, Inc./Ideal Mechanical RSM US LLP Foley & Lardner LLP AHEAD R&R Insurance Services, Inc. Ruekert & Mielke, Inc. GE Healthcare Alight Solutions State of Wisconsin S & C Electric Company Harley-Davidson Motor Company American Red Cross STRATTEC Security Corporation salesforce.com Johnson Financial Group in Southeastern Wisconsin Target Schlossmann’s Automotive Group ManpowerGroup Anderson Packaging, LLC University of Wisconsin - Milwaukee School District of Waukesha MGIC Investment Corporation Avaya, Inc. UW Credit Union Sentry Equipment Corp. Quarles & Brady LLP Briohn Building Corporation von Briesen & Roper, s.c. ServiceNow, Inc. U.S. Bank Carroll University Wells Fargo Shorewest Realtors Check Point Sikich LLP CIBC Cleary Gull SoftwareONE, Inc. -

University of Wisconsin-Milwaukee Is Committed to and Community, and Learn a New STUDENTS Global Engagement Through Its Curriculum, Research Activities, Language

A WORLD-CLASS UNIVERSITY UNIVERSITY OF WISCONSIN MILWAUKEE ONE OF ONLY TWO PUBLIC UNIVERSITIES IN WISCONSIN OFFERING DOCTORAL FIVE FORTUNE 500 DEGREES TOP 131 welcomeNOTABLE UWM CORPORATIONS RESEARCH UNIVERSITIES ALUMNI INCLUDE IN MILWAUKEE CARNEGIE CLASSIFICATION OF INSTITUTIONS OF HIGHER EDUCATION SATYA NADELLA NORTHWESTERN MUTUAL RANKED #4 IN (CEO of Microsoft) MANPOWERGROUP HIGHEST PERCENTAGE OF LUIS ARREAGA WEC ENERGY GROUP ENGINEERING DOCTORAL (U.S. ambassador) HARLEY-DAVIDSON DEGREES AWARDED TO FOREIGN NATIONALS MITCH WHITMORE ROCKWELL AUTOMATION 1,000+ (Olympic speedskater) BY SCHOOL THE AMERICAN SOCIETY OF UNDERGRADUATE KIMBERLEY CHONGYON MOTLEY ENGINEERING EDUCATION IN 2017 (First foreign lawyer working in Afghanistan) RESEARCH JIM RYGIEL OPPORTUNITIES (Academy Award-winner, visual effects for Lord of the Rings) 30,000 works of art at the 800 MILWAUKEE + ART MUSEUM MUSICAL ACTS PERFORM AT SUMMERFEST, one of the largest music festivals in the world UWM.EDU uwm and milwaukee WELCOME Milwaukee is the largest city in Wisconsin with a regional population of 1.5 million people and the center of business, industry and culture in the state. The city is known for its year-round festivals, beautiful lakefront, friendly community and historic architecture. UWM is located in a quiet, safe and attractive residential area and is within walking distance of Lake Michigan. Milwaukee’s downtown is a short car or bus ride away. All UWM students have access to the B.O.S.S. safe ride pick- up service, which provides students with secure transportation every day, and U-PASS, a transit program through the Milwaukee County bus system. From outdoor concerts and film festivals to food trucks and 24-hour bike races, there’s always something to see and do in Milwaukee. -

Creating Impact – Achieving Results

30% Club Ireland CEO & Chairs Third Annual Conference Creating Impact – Achieving Results 25 January 2017 #30pcImpact National Gallery of Ireland Clare Street, Dublin 2 3.45pm Registration 4pm Seminar 6:15-7.30pm Reception & Networking @30percentclubIE www.30percentclub.org 30% Club Ireland Creating Impact Achieving Results 25 January 2017 2 Creating Impact Achieving Results 25 January 2017 Agenda 4.00pm Opening Remarks An Tánaiste and Minister for Justice and Equality, Frances Fitzgerald TD 4.15pm Welcome Marie O’Connor, Partner, PwC, Country Lead, 30% Club Ireland 4.25pm Painting the Picture: Research Update 2016 Facilitator: Conor O’Leary, Group Company Secretary, Greencore Anne-Marie Taylor, Management Consultant - Women in Management and Women on Boards: the Irish picture Darina Barrett, Partner, KPMG - The Think Future Study 2016 Dr Sorcha McKenna, Partner, McKinsey – Women Matter: Women in the Workplace 2016 4.45pm Sasha Wiggins introduces Lady Barbara Judge Sasha Wiggins, CEO, Barclays Bank Ireland introduces Lady Barbara Judge, Chair, Institute of Directors 5.00pm Taking Action Facilitator: Melíosa O’Caoimh, Senior Vice President, Northern Trust Anne Heraty, CEO, CPL Resources and President of Ibec Gareth Lambe, Head of Facebook Ireland Pat O’Doherty, CEO, ESB Brian O’Gorman, Managing Partner, Arthur Cox 5.25pm Leadership Commitment and Accountability - Perspective of the Chair Facilitator: Bríd Horan, Former Deputy CEO, ESB Rose Hynes, Chair, Shannon Group and Origin Enterprises Gary Kennedy, Chair, Greencore Gary McGann, Chair, Paddy Power Betfair 5.45pm Diplomacy, Diaspora and Diversity Anne Anderson, Ambassador of Ireland to the United States 6.00pm Future Plans & Closing Remarks Carol Andrews, Global Head of Client Service and Prime Custody (AIS), BNY Mellon Please note that this is an on the record event and views expressed are not necessarily representative of all 30% Club members. -

2020.11.05 Q3 FY12/20 Presentation1.93MB

Financial Results for the 3rd Quarter of Fiscal Year Ending December 31, 2020 November 2020 OUTSOURCING Inc. Securities Code: 2427/TSE 1st Section Copyright (C) 2020 OUTSOURCING Inc. All Rights Reserved. Contents ⚫ P. 2 Our Group’s Social Responsibility and Significance ⚫ P. 5 Consolidated Financial Results for 3Q FY12/20 (IFRS) ⚫ P. 19 The Revised Full-Year Consolidated Financial Forecasts (IFRS) and Dividend Forecast ⚫ P. 25 Status of Group Companies Whose Goodwill is Recorded on OS Account ⚫ P. 37 The Group’s Advantage in Discovering New Demands in Response to COVID-19 ⚫ P. 42 Acquisition Announcement Made on November 4, 2020 ⚫ P. 44 Reference Materials Copyright (C) 2020 OUTSOURCING Inc. All Rights Reserved. 1 Our Group’s Social Responsibility and Significance Copyright (C) 2020 OUTSOURCING Inc. All Rights Reserved. 2 Our Group’s Social Responsibility and Significance New Initiatives in Social Responsibility Due to large, worldwide changes caused by rapid globalization, significant changes have been starting to occur in what the society demands from HR service companies and their roles in society. By redefining our management philosophy, we as the Outsourcing Group will create a framework that will allow us to contribute widely to society through our business activities. Group Mission Management Philosophy Vision of a society to be achieved through our businesses Universal principles for realizing our group mission that underpin our group’s business activities Compliance Implementation Execution Execution Sustainability Policy Business Vision Upward spiral through the Code of Conduct power of employees Business Policy (individual) and the power of the company (unity) Copyright (C) 2020 OUTSOURCING Inc. -

2013 Cws Summit - Berlin Delegates by Company

2013 CWS SUMMIT - BERLIN DELEGATES BY COMPANY Countries associated with Summit delegates and Staffing Industry AstraZeneca Pharmaceuticals LP | Hone, Victoria - Global Analysts personnel denote country of residence and not individual Resourcing - UK nationality, nor area of job responsibility Atos | Arnold, Andreas - Procurement Line Manager - Germany A Atos | Campserveux, Anna - Staffing, Subcontractors & Indirects Purchasing Manager - France ABB Inc | Kaneberg, Mats - Country Contract Manager - Sweden Atos | Kromer, Christian - Commodity Manager, Strategic Buyer - ABB Inc | Lindell, Tony - Contract Manager Staffing Services - Germany Sweden Atos | Lawrenson, Ian - Global Buyer, Contingent Workforce - UK ABB Management Services Ltd | Baechli, Roland - Country Supply Atos Origin | Aylott, Martin - Global Category Manager Staffing Chain Manager - Switzerland Services - UK ABB Management Services Ltd | Schmid, Thomas - Head Global B Contracted Services Commodity - Switzerland ABN AMRO Bank | Henselmans, Marc - Team Manager External Babcock International | Waters, Naomi - Procurement, Group HR Staffing - Netherlands Category - UK ABN AMRO Bank | Neher, Frank - Category Manager - Baker Hughes | Schwalbe, Martin - Senior Staffing Representative Netherlands - Germany Adecco Group France | Koch, Yann - International Account Balfour Beatty | Lee, Nick - Resourcing & HR Business Partner - Director - France UK Advantage xPO | Browne, Karen - President, Advantage xPO - USA Bank of America | LeBret, Kerry - Vendor Relationship Manager - Advantage -

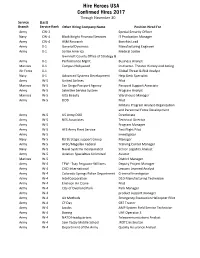

30 Nov Hires Report

Hire Heroes USA Confirmed Hires 2017 Through November 30 Service (Last) Branch Service Rank Other Hiring Company Name Position Hired For Army CW-2 Special Security Officer Navy CW-4 Black Knight Financial Services IT Production Manager Army CW-4 ASM Research Benefits Lead Army 0-1 General Dynamics Manufacturing Engineer Army 0-1 Scribe America Medical Scribe Gwinnett County Office of Strategy & Army 0-1 Performance Mgmt. Business Analyst Marines 0-1 Campus Hollywood Instructor- Theater History and Acting Air Force 0-1 Global Threat & Risk Analyst Navy 0-1 Advanced Systems Development Help Desk Specialist Army W-5 United Airlines Pilot Marines W-5 San Diego Passport Agency Passport Support Associate Army W-5 Selective Service System Program Analyst Marines W-5 Ulta Beauty Warehouse Manager Army W-5 DOD Pilot Military Program Analyst-Organization and Personnel Force Development Army W-5 US Army DOD Directorate Army W-5 NES Associates Technical Director Army W-5 Program Manager Army W-5 AFS Army Fleet Service Test Flight Pilot Army W-5 Investigator Navy W-5 R3 Strategic support Group Manager Army W-5 AFSC/Magellan Federal Training Center Manager Navy W-5 Naval Systems Incorporated Senior Logistics Analyst Army W-5 Aviation Specialties Unlimited Aviator Marines W-5 District Manager Army W-4 TFW - Tsay Ferguson-Williams Deputy Project Manager Army W-4 CACI International Lessons Learned Analyst Army W-4 Colorado Springs Police Department Criminal Investigator Army W-4 Intel Corporation D1D Manufacturing Technician Army W-4 Erickson Air Crane