Concept-Project-Information-Document-Integrated-Safeguards-Data-Sheet.Pdf

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Familiarisation Tour of Mpulungu, Zambia

THE ENVIRONMENTAL COUNCIL OF ZAMBIA Pollution Control and Other Measures to protect Biodiversity in Lake Tanganyika (RAF/92/G32) FAMILIARISATION TOUR OF MPULUNGU A COMBINED SOCIO-ECONO0MICS AND ENVIRONMNETAL EDUCATION TOUR CONDUCTED FROM 2/2/99 TO 3/3/99 Munshimbwe Chitalu Assistant National Co-ordinator Socio-economics Co-ordinator National Coordination Office LUSAKA ZAMBIA July 2000 M p u l u n g u Vi s i t R e p o r t , So c i o - E c o n o m i c s / E n v i r o n m e n t a l Ed u c a t i o n Contents List of Acronyms ii Foreword iii Executive summary iv 1 HIGHLIGHTS 1 1 Environmental Education Activities 1 2 Conservation and Development Committees 1 3 Activities of CDCs 2 4 National Project coordination 3 5 The team 3 6 Approach and salutations 3 2 THE TOUR IN MORE DETAIL 4 1 The Aim 4 2 Specific Objectives 4 3 Findings 4 3.1 Community Development Officer (CDO) 4 3.2 Department of Fisheries (DoF) 5 3.3 Immigration Department 7 3.4 Mpulungu District Council 7 3.5 Mpulungu Harbor Corporation Limited 8 3.6 Mr. Mugala 8 3.7 The Provincial Agricultural Co-ordination Office (PACO) 9 3.8 Police Service 9 3.9 Senior Chief Tafuna 9 3.10 Stratum 2 CDC 9 3.11 Village CDCs 10 3 CONCLUSIONS AND RECOMMENDATIONS 12 4 PROPOSED IMMEDIATE ACTIONS 14 Appendix I: Institutions and individuals visited 15 Appendix II: Itinerary 17 Appendix III: Resources 18 P A G E I M p u l u n g u Vi s i t R e p o r t , So c i o - E c o n o m i c s / E n v i r o n m e n t a l Ed u c a t i o n List of Acronyms AMIS Association of Micro-finance Institutions of Zambia ANSEC -

Towards a Regional Information Base for Lake Tanganyika Research

RESEARCH FOR THE MANAGEMENT OF THE FISHERIES ON LAKE GCP/RAF/271/FIN-TD/Ol(En) TANGANYIKA GCP/RAF/271/FIN-TD/01 (En) January 1992 TOWARDS A REGIONAL INFORMATION BASE FOR LAKE TANGANYIKA RESEARCH by J. Eric Reynolds FINNISH INTERNATIONAL DEVELOPMENT AGENCY FOOD AND AGRICULTURE ORGANIZATION OF THE UNITED NATIONS Bujumbura, January 1992 The conclusions and recommendations given in this and other reports in the Research for the Management of the Fisheries on Lake Tanganyika Project series are those considered appropriate at the time of preparation. They may be modified in the light of further knowledge gained at subsequent stages of the Project. The designations employed and the presentation of material in this publication do not imply the expression of any opinion on the part of FAO or FINNIDA concerning the legal status of any country, territory, city or area, or concerning the determination of its frontiers or boundaries. PREFACE The Research for the Management of the Fisheries on Lake Tanganyika project (Tanganyika Research) became fully operational in January 1992. It is executed by the Food and Agriculture organization of the United Nations (FAO) and funded by the Finnish International Development Agency (FINNIDA). This project aims at the determination of the biological basis for fish production on Lake Tanganyika, in order to permit the formulation of a coherent lake-wide fisheries management policy for the four riparian States (Burundi, Tanzania, Zaïre and Zambia). Particular attention will be also given to the reinforcement of the skills and physical facilities of the fisheries research units in all four beneficiary countries as well as to the buildup of effective coordination mechanisms to ensure full collaboration between the Governments concerned. -

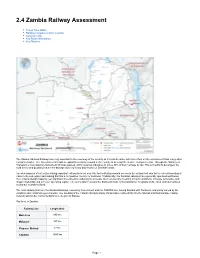

2.4 Zambia Railway Assessment

2.4 Zambia Railway Assessment Travel Time Matrix Railway Companies and Consortia Capacity Table Key Route Information Key Stations The Zambia National Railways are very important to the economy of the country as it is a bulk carrier with less effect on the environment than many other transport modes. The Government intends to expand its railway network in the country to develop the surface transport sector. Through the Ministry of Transport, a new statutory instrument (SI) was passed, which requires industries to move 30% of their carriage by rail. This is in a bid to decongest the road sector and possibly reduce the damage done by heavy duty trucks on Zambian roads. The development of rail routes linking important exit points is not only vital for facilitating smooth access to the outside but also for the overall boosting of trade in the sub-region and making Zambia a competitive country for business. Traditionally, the Zambian railways have generally operated well below their original design capacity, yet significant investment is underway to increase their volumes by investing in track conditions, increase locomotive and wagon availability and increase operating capital. The rail network remains the dominant mode of transportation for goods on the local and international routes but is under-utilized. The main railway lines are the Zambia Railways, owned by Government and the TAZARA line, linking Zambia with Tanzania, and jointly owned by the Zambian and Tanzanian governments. The opening of the Chipata-Mchinji railway link provides connectivity into the Malawi and Mozambique railway network and further connects Zambia to the port of Nacala. -

Maritime Trade on Lake Tanganyika Trade Opportunities for Zambia

Maritime Trade on Lake Tanganyika Trade Opportunities for Zambia Commissioned by the Netherlands Enterprise Agency Maritime Trade on Lake Tanganyika Trade Opportunities for Zambia Maritime Trade on Lake Tanganyika Trade Opportunities for Zambia Rotterdam, July 2019 Table of contents Preface 3 Abbreviations and Acronyms 4 1 Introduction 5 2 Transport and Logistics 10 3 International and Regional Trade 19 4 Trade Opportunities 29 5 Recommendations and Action Plan 41 References 48 Annex A Trade Statistics 50 Annex B Trade Potential 52 Annex C Maps 53 Maritime Trade on Lake Tanganyika 2 Preface This market study was prepared by Ecorys for the Netherlands Enterprise Agency (RVO). The study provides information on trade opportunities between the countries on the shores of Lake Tanganyika, with a particular focus on Zambia and the port in Mpulungu. As such this study fills a gap, as previous studies were mostly focused on the infrastructure and logistics aspects of maritime trade on Lake Tanganyika. *** The study was prepared by Michael Fuenfzig (team leader & trade expert), Mutale Mangamu (national expert), Marten van den Bossche (maritime transport expert). We also thank Niza Juma from Ecorys Zambia (PMTC) for her support. This study is based on desk research, the analysis of trade statistics, and site visits and interviews with stakeholders around Lake Tanganyika. In Zambia Lusaka, Kasama, Mbala and Mpulungu were visited, in Tanzania, Kigoma and Dar es Salaam, and in Burundi, Bujumbura. The study team highly appreciates all the efforts made by the RVO, the Netherlands Ministry of Foreign Affairs and other stakeholders. Without their cooperation and valuable contributions this report would not have been possible. -

(A) Village, Mbala District, Zambia

A project funded by the United Nations Development Programme/Global Environmen t Facility (UNDP/GEF) and executed by the United N ations Office f or Project Services (UNOPS) SOCIO-ECONOMIC SPECIAL STUDY Report No. 19 CHISANZA (A) Socio-economic study of Chisanza (A) village, Mbala District, Zambia Mpulungu February 2000 G. Munshimbwe Chitalu & Frighton Ng’andu Pollution control and other measures to protect biodiversity in Lake Tanganyika (RAF/92/G32) Lutte contre la pollution et autres mesures visant à protéger la biodiversité du lac Tanganyika (RAF/92/G32) The Lake Tanganyika Biodiversity Project Le Projet sur la Biodiversité du Lac has been formulated to help the four Tanganyika a été formulé pour aider les riparian states (Burundi, Congo, Tanzania quatre états riverains (Burundi, Congo, and Zambia) produce an effective and Tanzanie et Zambie) à élaborer un système sustainable system for managing and efficace et durable pour gérer et conserver conserving the biodiversity of Lake la diversité biologique du lac Tanganyika Tanganyika into the foreseeable future. It is dans un avenir prévisible. Il est financé par funded by the Global Environmental le FEM (Fonds pour l’Environnement Facility through the United Nations Mondial) par le biais du Programme des Development Programme. Nations Unies pour le Développement (PNUD) Burundi: L’Institut National pour l’Environnement et la Conservation de la Nature D R Congo: Le Ministère de l’Environnement et de la Conservation de la Nature Tanzania: Vice President’s Office, Division of Environment Zambia: Environment Council of Zambia Lake Tanganyika Biodiversity Project i Socio-Economic Special Study Report No. 19 Lake Tanganyika Biodiversity Project Socio-Economic Special Study Report Series Series editors: Dr. -

National Transportation System in the Republic of Zambia

World Maritime University The Maritime Commons: Digital Repository of the World Maritime University World Maritime University Dissertations Dissertations 1990 National transportation system in the Republic of Zambia Febby Mtonga WMU Follow this and additional works at: https://commons.wmu.se/all_dissertations Recommended Citation Mtonga, Febby, "National transportation system in the Republic of Zambia" (1990). World Maritime University Dissertations. 877. https://commons.wmu.se/all_dissertations/877 This Dissertation is brought to you courtesy of Maritime Commons. Open Access items may be downloaded for non- commercial, fair use academic purposes. No items may be hosted on another server or web site without express written permission from the World Maritime University. For more information, please contact [email protected]. WMU LIBRARY WORLD MARITIME UNIVERSITY Malmo ~ Sweden THE NATIONAL TRANSPORTATION SYSTEM IN THE REPUBLIC OF ZAMBIA by Febby Mtonga Zambia A paper submitted to the faculty of the World Maritime University in partial fulfillment of the requirements for the award of a MASTER OF SCIENCE DEGREE in GENERAL MARITIME ADMINISTRATION The views and contents expressed in this paper reflect entirely those of my own and are not to be construed as necessarily endorsed by the University Signed: Date : 0 5 I 11 j S O Assessed by: Professor J. Mlynarcz] World Maritime University Ilf Co-assessed by: U. 2).i TABLE OF CONTENTS 1 PREFACE i ACKNOWLEDGEMENT ii ABBREVIATIONS ... LIST OF MAPS AND APPENDICES iv CHAPTER 1 M • O • o Profile of the Republic of Zambia 1 1.1.0 Geographical Location of Zambia 1.2.0 Population 1.3.0 The Economy 1.3.1 Mining 1.3.2 Agriculture 3 1.3.3 Manufacturing 4 1.3.4 Transportation 7 1. -

Analysis of Zambia Railway Sector – Structural Deficiencies & the Way Forward

Source: hhttps://www.dailynation.info/zrl-gets-850m-fillip/ Source: ANALYSIS OF ZAMBIA RAILWAY SECTOR – STRUCTURAL DEFICIENCIES & THE WAY FORWARD ANALYSIS OF ZAMBIAANALYSIS RAILWAY SECTOR – STRUCTURAL DEFICIENCIES & THE WAY FORWARDJune | 20191 PREPARED BY: TABLE OF CONTENTS RESEARCH: Albert Kasoma (Senior Researcher) with the support of Bernadette Deka Zulu (Executive Abbreviations and Acronyms 4 Director) Introduction 6 TECHNICAL REVIEW: Brief History of Rail Transport in Zambia 9 Chileshe Chaunga (Senior Researcher) Zambian Railways Limited. 11 TAZARA 12 EDITORIAL TEAM: Key Challenges with Railway Transport in Zambia 17 Brian Sambo Mwila (Communication Specialist) Layout and Design Melody M. Simukali (Head Communications and Grants) Editorial Market share 19 Government Interventions to Increase Rail Freight 20 Lessons from Other Countries -Railways Models in Africa 21 Way forward; Structural and Management Systems to make the Rail Sector Profitable 24 Creation of the Railway Development 25 Decentralisation 25 Private Participation 26 Service Contracts 26 Infrastructure Construction and Maintenance 26 Equipment Ownership and Leasing 27 Management Contracts 28 Private Operations of Trains 29 Full Private Ownership 29 Public-Private Partnership 30 Conclusion 31 Recommendations 32 References 34 This document and trademark(s) contained herein are protected by the laws of The Republic of Zambia. This electronic representation of PMRC intellectual property is provided for non- commercial use only. Unauthorized posting of PMRC electronic documents to a non-PMRC website is prohibited. PMRC electronic documents are protected under copyright law. Permission is required from PMRC to reproduce, or reuse in another form, any of our research documents for commercial use. For information on reprint and linking permissions, please see PMRC Permissions . -

UNCTAD/LDC/115 20 July 2001

UNCTAD/LDC/115 20 July 2001 ENGLISH ONLY TRADE AND DEVELOPMENT BOARD Fifth Meeting of Governmental Experts from Land-locked and Transit Developing Countries and Representatives of Donor Countries and Financial and Development Institutions New York, 30 July - 3 August 2001 REVIEW OF PROGRESS IN THE DEVELOPMENT OF TRANSIT TRANSPORT SYSTEMS IN EASTERN AND SOUTHERN AFRICA Report prepared by InfraAfrica (Pty) Ltd UNCTAD consultant * / _________________ * / The views expressed in this study are those of the author and do not necessarily reflect the views of the UNCTAD secretariat or of any official administration. The designations employed and the presentation of the material do not imply the expression of any opinion whatsoever on the part of the secretariat of the United Nations concerning the legal status of any country, territory, city or area, or of its authorities, or concerning the delimitation of its frontiers or boundaries. 2 CONTENTS INTRODUCTION ................................................................................................................. 3-4 I. Objectives and scope of report..................................................................................... 4-5 II. Approach and methodology........................................................................................... 5-6 III. Layout of report.................................................................................................................6 IV. Inventory of transit-transport systems and facilities................................................... -

Republic of Zambia Report of the Committee on Parastatal Bodies on the Examination of the Annual Reports for the Tanzania Zambia

REPUBLIC OF ZAMBIA REPORT OF THE COMMITTEE ON PARASTATAL BODIES ON THE EXAMINATION OF THE ANNUAL REPORTS FOR THE TANZANIA ZAMBIA RAILWAY AUTHORITY FOR THE YEARS ENDED 2017 AND 2018 FOR THE FOURTH SESSION OF THE TWELFTH NATIONAL ASSEMBLY APPOINTED ON 21ST SEPTEMBER, 2017 Printed by the National Assembly of Zambia REPORT OF THE COMMITTEE ON PARASTATAL BODIES ON THE EXAMINATION OF THE ANNUAL REPORTS FOR THE TANZANIA ZAMBIA RAILWAY AUTHORITY FOR THE YEARS ENDED 2017 AND 2018 FOR THE FOURTH SESSION OF THE TWELFTH NATIONAL ASSEMBLY APPOINTED ON 21ST SEPTEMBER, 2017 Table of Contents 1.0 Composition of the Committee ...................................................................................................... 1 2.0 Functions of the Committee ........................................................................................................... 1 3.0 Meetings of the Committee ............................................................................................................ 2 4.0 Procedure Adopted by the Committee ........................................................................................... 2 5.0 Arrangement of the Report ............................................................................................................ 2 PART I .......................................................................................................................................................... 2 Consideration of the Topical Issue: Examination of the Annual Reports of the Tanzania-Zambia Railway Authority, for the -

Mpulungu, Zambia 2008 District Education Profile

Zambia 2008 District Profile for Mpulungu At a glance Basic School Grades GoalGoalsActual 1-9 10-12 Value Female Pupils 9,548 179 NIR 80% 63% Male Pupils 9,668 259 NER 110% 117% Survival to G9 50% 15% Teachers 268 24 Pupil-Teacher Ratio 60 71 Schools 73 3 Teacher Attrition Rate 5% 25% Classrooms 275 35 % Teachers Qualified 50% 78% Textbooks 69,000 4,312 Pupil-Book Ratio 1 3.2 ANALYSIS 1.1 Overview Mpulungu District with the only port in Zambia, is located in the northern part of the Northern Province of the Republic of Zambia. The district shares local boundaries with Mbala in the east, Mporokoso in the south and Kaputa in the south-west. It shares international boundaries with Tanzania in the north-east and DRC in the west and Burundi in the north-west .It is 203 km from provincial headquarters (kasama) The Office of the District Education Board Secretary (DEBS) was established in 1998. Being new, the district faces a number of challenges that affect the provision of quality education. These include poor infrastructure: out of 36 GRZ schools and 36 community schools, only 9 schools are in permanent structure; the rest are in pole and mud or dilapidated. However, in 2008 the district was given K1, 620,000, 000 by the Government t o construct 27 new classrooms, which now are completed. Other challenges are early marriages, staff shortage, transport impediments, devotion to fishing or selling fish by children at the expense of learning and long distances to and from full basic schools which are very few, very poor or non-available at all in some areas. -

District 413 Zambia Directory

LIONSLIONSLIONS CLUBSCLUBSCLUBS INTERNATIONALINTERNATIONALINTERNATIONAL DISTRICTDISTRICTDISTRICT 413413413 -- ZAMBIAZAMBIAZAMBIA DISTRICTDISTRICT DIRECTORYDIRECTORY 20182018 -- 1919 are rich in heritage and pride The International Association of Lions Clubs began as the dream of Chicago businessman Melvin Jones.. He believed that local business clubs should expand their horizons from purely professional concerns to the betterment of their communities and the world at large.. Today, our “We Serve” motto continues, represented by more volunteers in more places than any other service club organization in the world. We are friends, neighbors and leaders ready to help our communities grow and thrive.. Melvin Jones lionsclubs.org For information on a club in your area contact: [email protected] Our mission is to empower volunteers to serve their communities, meet humanitarian needs, encourage peace and promote international understanding through Lions clubs. Contents Distict Governor’s Message 1 International President’s Message 2 International President’s Office 3 ISAAME Secretariat 4 District Governor’s Office 5 Global Action Team 7 Council of Past District Governors 8 Region Chairpersons 11 Zone Chairpersons 12 District Committee Chairpersons 15 Leo District 24 Leo District President’s Office 25 District Clubs 26 Melvin Jones Fellows 39 Loyal Toasts 44 Lions Code of Ethics 45 Lions Clubs International Purposes 46 Past District Governors 47 Lions Funeral service / Necrology 48 DISTRICT 413 GOVERNOR DR. GEORGE SM BANDA As Lions how can we build on our already impressive legacy? It's simple, we will do what Lions have always done. We will get creative and reach within our communities, clubs and selves to discover a new level of service. -

Botswana Namibia Zimbabwe Mozambique Malawi Zambia

2230’0"E 250’0"E 2730’0"E 300’0"E 3230’0"E 350’0"E Luaco Cossa Mutenge Satshigoia Kalamba Katenta Masala Kitale Kabu Lukanga Lukanga-Petit Nonda Lenge Mupanga Kibalange Simba Sumbawanga Kitagasa Tanangozi Ihimbe Ma Malosa Mwanza Kiwala Mwenge Kaulu Tshuwana Kabambi Kimenkinda Kawakwa Kalongo Lubondaie Tuite Kalangali Malaji Saylonga Mutombo-Mukulu Lubende Kansonge Makoko Kiponzelo Iheme Uwindi Chicunda Sa-Zeca Tshiwana Kanonda Kabwe Katanda Kalebwe Goi Keta Kitobwe Kabala Msia Lake Rukwa Samaca Maludi Luvunda Kambangu Kalundwe Kole Kasole Bunda Kabanza Balanga Lake Rukwa Kamalondo Tshifinga Tshipasa Mato Kikindwe Kishiale Tshisongo Mwene-Ndua Seya Mwilambwe Mulombi KiabulaMalemba Nkulu Kipia Mandwe Kasunga Pito Ulete Tsh i t u m ba Mwine-Kombo Zaila Kitumbe Kipembe Kange Sangwe Mwange LakeLake TanganyikaTanganyika Luia Tshau Songa Kilamba Lukila Kivumbu LacLac ZimbamboZimbambo Nambia Kimpalapala Kalambo Uleia Mbeya Dabaga Mukelange-Lumbu Kaditshi Kasumbwe Kampunga Kako Bulundu Kabudji Kalembwe Pongo Karinde Sakalilo Wasa Verssimo Sarmento Tshibangu Bwamuyembe Ngombe Luniemu Kabutulu Niemba Kabanze Kibala Djobo Kondolo Muhaga Lunda Norte Pandamwila Kilemba LacLac KalumbeKalumbe Kapumfi Kitagalu Iringa Kakunji Kabeba Kalema Muleba Kafungo-Kazadi Boto Masangu Kikondja Kikunka Kintshia Mwema Mukebo Shiebele Puta Kikongo Wamikonko Sonji Madibira Lumiko Bomalangombe Caua Katapakishi Sumba-Luwai Kasokola Muonda Kirambo Capaia Tsh i t a zu Kafungo-Dianda Lubinda-Mukoko Lac Lunda Katwawa Kisele Mgeta Mundu-a-Mwele Kamutoi Kamundu Muzika Lac Lunda