Your Airlines. Where the American Dream Takes Flight

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

United Airlines Holdings Annual Report 2021

United Airlines Holdings Annual Report 2021 Form 10-K (NASDAQ:UAL) Published: March 1st, 2021 PDF generated by stocklight.com UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, DC 20549 FORM 10-K ☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2020 OR ☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from to Commission Exact Name of Registrant as Specified in its Charter, State of I.R.S. Employer File Number Principal Executive Office Address and Telephone Incorporation Identification No. Number 001-06033 United Airlines Holdings, Inc. Delaware 36-2675207 233 South Wacker Chicago, Illinois Drive, 60606 (872) 825-4000 001-10323 United Airlines, Inc. Delaware 74-2099724 233 South Wacker Chicago, Illinois Drive, 60606 (872) 825-4000 Securities registered pursuant to Section 12(b) of the Act: Title of Each Class Trading Symbol Name of Each Exchange on Which Registered United Airlines Holdings, Inc. Common Stock, $0.01 par value UAL The Nasdaq Stock Market LLC Preferred Stock Purchase Rights The Nasdaq Stock Market LLC United Airlines, Inc. None None None Securities registered pursuant to Section 12(g) of the Act: United Airlines Holdings, Inc. None United Airlines, Inc. None Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act United Airlines Holdings, Inc. Yes ☒ No ☐ United Airlines, Inc. Yes ☒ No ☐ Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. -

Air Jamaica Report

OFFICE OF THE CONTRACTOR GENERAL Special Report of Investigation and Monitoring Conducted into the Procurement Practices of Air Jamaica Limited (Formerly) Ministry of Finance and Planning EXECUTIVE SUMMARY The investigation into the Procurement and Contract award practices of Air Jamaica Limited was initiated by the Office of the Contractor General (OCG) on 2006 May 23. On 2006 May 16, the Office of the Contractor General received a letter from Mrs. Sharon Weber, who wrote on behalf of the Financial Secretary in the Ministry of Finance and Planning. The letter confirmed that Air Jamaica Limited was a Public Body by virtue of the Government’s one hundred percent (100%) ownership as stipulated by Part 1 (Section 2) of the Public Bodies Management and Accountability Act, 2001. Air Jamaica Limited has been through ownership changes over the last 15 years. Most recently - in 2004 December - the airline was reacquired by the Government of Jamaica following almost a decade of privately managed operations. Consequently, Air Jamaica Limited, as of 2004 December, is deemed to be a ‘public body’ as defined within the Contractor General Act (1983) and is required to adhere to the Government Procurement Guidelines. The investigation of the entity focused primarily on procurement activities between May 2005 and August 2008 and incorporated the OCG’s monitoring of the airline’s procurement activities up to, and including, August 2008. The period under review commences approximately six months after Air Jamaica Limited returned to the ambits of government control. It is perceived that this period should have provided the agency with some amount of __________________________________________________________________________________________ Air Jamaica Investigation Office of the Contractor-General 2008 September Page 1 of 33 time to acclimatize itself with stipulated government policies, thereby effecting a smooth transition from a private to a public entity as it relates to procurement practices. -

AWA AR Editoral

AMERICA WEST HOLDINGS CORPORATION Annual Report 2002 AMERICA WEST HOLDINGS CORPORATION America West Holdings Corporation is an aviation and travel services company. Wholly owned subsidiary, America West Airlines, is the nation’s eighth largest carrier serving 93 destinations in the U.S., Canada and Mexico. The Leisure Company, also a wholly owned subsidiary, is one of the nation’s largest tour packagers. TABLE OF CONTENTS Chairman’s Message to Shareholders 3 20 Years of Pride 11 Board of Directors 12 Corporate Officers 13 Financial Review 15 Selected Consolidated Financial Data The selected consolidated data presented below under the captions “Consolidated Statements of Operations Data” and “Consolidated Balance Sheet Data” as of and for the years ended December 31, 2002, 2001, 2000, 1999 and 1998 are derived from the audited consolidated financial statements of Holdings. The selected consolidated data should be read in conjunction with the consolidated financial statements for the respective periods, the related notes and the related reports of independent accountants. Year Ended December 31, (in thousands except per share amounts) 2002 2001(a) 2000 1999 1998 (as restated) Consolidated statements of operations data: Operating revenues $ 2,047,116 $ 2,065,913 $ 2,344,354 $ 2,210,884 $ 2,023,284 Operating expenses (b) 2,207,196 2,483,784 2,356,991 2,006,333 1,814,221 Operating income (loss) (160,080) (417,871) (12,637) 204,551 209,063 Income (loss) before income taxes and cumulative effect of change in accounting principle (c) (214,757) -

United States Court of Appeals for the DISTRICT of COLUMBIA CIRCUIT

USCA Case #11-1018 Document #1351383 Filed: 01/06/2012 Page 1 of 12 United States Court of Appeals FOR THE DISTRICT OF COLUMBIA CIRCUIT Argued November 8, 2011 Decided January 6, 2012 No. 11-1018 REPUBLIC AIRLINE INC., PETITIONER v. UNITED STATES DEPARTMENT OF TRANSPORTATION, RESPONDENT On Petition for Review of an Order of the Department of Transportation Christopher T. Handman argued the cause for the petitioner. Robert E. Cohn, Patrick R. Rizzi and Dominic F. Perella were on brief. Timothy H. Goodman, Senior Trial Attorney, United States Department of Transportation, argued the cause for the respondent. Robert B. Nicholson and Finnuala K. Tessier, Attorneys, United States Department of Justice, Paul M. Geier, Assistant General Counsel for Litigation, and Peter J. Plocki, Deputy Assistant General Counsel for Litigation, were on brief. Joy Park, Trial Attorney, United States Department of Transportation, entered an appearance. USCA Case #11-1018 Document #1351383 Filed: 01/06/2012 Page 2 of 12 2 Before: HENDERSON, Circuit Judge, and WILLIAMS and RANDOLPH, Senior Circuit Judges. Opinion for the Court filed by Circuit Judge HENDERSON. KAREN LECRAFT HENDERSON, Circuit Judge: Republic Airline Inc. (Republic) challenges an order of the Department of Transportation (DOT) withdrawing two Republic “slot exemptions” at Ronald Reagan Washington National Airport (Reagan National) and reallocating those exemptions to Sun Country Airlines (Sun Country). In both an informal letter to Republic dated November 25, 2009 and its final order, DOT held that Republic’s parent company, Republic Airways Holdings, Inc. (Republic Holdings), engaged in an impermissible slot-exemption transfer with Midwest Airlines, Inc. (Midwest). -

My Personal Callsign List This List Was Not Designed for Publication However Due to Several Requests I Have Decided to Make It Downloadable

- www.egxwinfogroup.co.uk - The EGXWinfo Group of Twitter Accounts - @EGXWinfoGroup on Twitter - My Personal Callsign List This list was not designed for publication however due to several requests I have decided to make it downloadable. It is a mixture of listed callsigns and logged callsigns so some have numbers after the callsign as they were heard. Use CTL+F in Adobe Reader to search for your callsign Callsign ICAO/PRI IATA Unit Type Based Country Type ABG AAB W9 Abelag Aviation Belgium Civil ARMYAIR AAC Army Air Corps United Kingdom Civil AgustaWestland Lynx AH.9A/AW159 Wildcat ARMYAIR 200# AAC 2Regt | AAC AH.1 AAC Middle Wallop United Kingdom Military ARMYAIR 300# AAC 3Regt | AAC AgustaWestland AH-64 Apache AH.1 RAF Wattisham United Kingdom Military ARMYAIR 400# AAC 4Regt | AAC AgustaWestland AH-64 Apache AH.1 RAF Wattisham United Kingdom Military ARMYAIR 500# AAC 5Regt AAC/RAF Britten-Norman Islander/Defender JHCFS Aldergrove United Kingdom Military ARMYAIR 600# AAC 657Sqn | JSFAW | AAC Various RAF Odiham United Kingdom Military Ambassador AAD Mann Air Ltd United Kingdom Civil AIGLE AZUR AAF ZI Aigle Azur France Civil ATLANTIC AAG KI Air Atlantique United Kingdom Civil ATLANTIC AAG Atlantic Flight Training United Kingdom Civil ALOHA AAH KH Aloha Air Cargo United States Civil BOREALIS AAI Air Aurora United States Civil ALFA SUDAN AAJ Alfa Airlines Sudan Civil ALASKA ISLAND AAK Alaska Island Air United States Civil AMERICAN AAL AA American Airlines United States Civil AM CORP AAM Aviation Management Corporation United States Civil -

2011 Economic Report

2011 ECONOMIC REPORT We Connect the World A4A airlines and their affiliates transport more than 90 percent of all U.S. airline passenger and cargo traffic. Airlines for America ® Contents A4A Members ................................................... 2 Members: Operating and Financial Results ....................... 3 Safety Trend ...................................................... 5 U.S. Airline Rankings ..................................... 7-9 Employees and Operating Revenues ............ 7 Aircraft Departures/Passengers Enplaned ....8 Cargo/Passenger Traffic and Capacity ......... 9 Top U.S. City Pairs by O&D Passengers .........11 Revenue Collected per Passenger ................. 12 Airport Passengers/Cargo and Departures .... 14 Profitability ....................................................... 16 U.S. Passenger Airline Costs vs. Inflation ...... 17 Fuel Expense per Passenger Mile .................. 18 Passengers Enplaned ..................................... 19 Domestic Capacity Trend ................................ 20 Customer Service ........................................... 22 Federal Aviation Taxes .................................... 24 U.S. Export Value by Transport Mode ............ 26 Associate Member: Noise Reduction .............................................. 28 Fuel Efficiency Gains ...................................... 29 Report Content Unless otherwise noted, the data provided in this report reflects the worldwide operations of all U.S. passenger and cargo airlines as recorded by the Bureau of Transportation -

Export Guide to the Consumer Food Market September 1997 Prepared for the U.S. Department of Agriculture by Fintrac Inc

Haiti Export Guide to the Consumer Food Market September 1997 Prepared for the U.S. Department of Agriculture by Fintrac Inc. This guide is one of ten individual guides available (not including a summary guide), covering the following countries and territories: Aruba and Curacao; the Bahamas; Barbados; British Territories, comprising Anguilla, the British Virgin Islands, the Cayman Islands, and the Turks and Caicos; the Dominican Republic; Guadeloupe and Martinique; Haiti; Jamaica; and the Organization of Eastern Caribbean States, comprising Antigua and Barbuda, Dominica, Grenada, St. Kitts-Nevis, and St. Vincent and the Grenadines. For more information, contact USDA/FAS offices in the Dominican Republic and Miami: Kevin Smith, Agricultural Counselor (for the Dominican Republic, Jamaica, and Haiti) Mailing Address: American Embassy Santo Domingo, Dominican Republic (FAS) Unit 5530 APO AA 34041 Other Mailing Address: Leopoldo Navarro #1 Apt. 4 Santo Domingo, Dominican Republic Tel: 809-688-8090 Fax: 809-685-4743 e-mail: [email protected] . Margie Bauer, Director (for all other countries covered by these guides) Mailing Address: Caribbean Basin Agricultural Trade Office USDA/FAS 909 SE 1st Avenue, Suite 720 Miami, FL 33131 Tel: 305-536-5300 Fax: 305-536-7577 e-mail: [email protected] List of Abbreviations Used BVI British Virgin Islands CARICOM Caribbean Community (comprised of Antigua & Barbuda, the Bahamas, Barbados, Belize, Dominica, Grenada, Guyana, Haiti, Jamaica, Montserrat, St. Kitts-Nevis, St. Lucia, St. Vincent & the -

Save a Turbine Engine: Serve It Water

Clare Leavens Award Joe Chase Award Aviall High Achievement Award Transport Canada Approved for R/T Save a turbine engine: serve it water Minimum equipment lists and dispatch deviation guides PAMA and AME news February -March 2015 Volume 13/Issue 5 Publication Mail Agreement No. 0041039024 and Return Undeliverable Canadian Addresses to Alpha Publishing Group (2004) Inc. Unit 7, 11771 Horseshoe Way, Richmond, BC, V7A 4V4 email: [email protected] $7.95 AMU-OFC-IFC.indd 1 1/29/15 7:28 PM AMU-OFC-IFC.indd 2 1/29/15 7:28 PM In perspective: Departments the P&WC PT6 nd here some of you thought Gran- 4 Upcoming Events dad put a lot of miles and years on his good ol’ Harley Flathead 45. Hah! 6 STCs & New Products AThat was nothing. Pratt & Whitney Canada 8 Industry Forum recently tweeted out that its venerable PT6 turbine has now clocked 400 million hours 20 AME Association of flight operation. and PAMA News Four hundred million! What does that 39 Classified even mean? Let’s calculate (roughly): There are 8,760 hours in any 365-day year. Di- 42 AMU Chronicles vide 400 million by 8,760 and you get By Sam Longo 45,662.100456621. Round that number off — without fac- toring in Leap, Aztec or dog years (this is al- Features ready getting too complicated for my lousy math)—and you’re now standing at 46,000 10 subscribe and download at www.amumagazine.com AMU is viewable online: years of service. Did I just do that right? As- Save a Turbine Engine: Serve it Water 10 suming I did (and that’s a big ask, I know) By Mike Broderick then we can break down that history into bite-sized pieces. -

1995 Annual Report

Southwest Airlines Co. 1995 Annual Report OUR 6 SECRETS OF SUCCESS Table of Contents Consolidated Highlights ..................................................................2 Introduction .....................................................................................3 Letter to Shareholders.....................................................................4 1. Stick To What You’re Good At ....................................................4 2. Keep It Simple .............................................................................8 3. Keep Fares Low, Costs Lower ..................................................10 4. Treat Customers Like Guests....................................................12 5. Never Stand Still .......................................................................14 6. Hire Great People .....................................................................16 Looking Ahead ..............................................................................18 Destinations ..................................................................................20 Financial Review ...........................................................................21 Management’s Discussion and Analysis .......................................21 Consolidated Financial Statements...............................................27 Report of Independent Auditors ....................................................39 Quarterly Financial Data ...............................................................40 Common Stock Price Ranges -

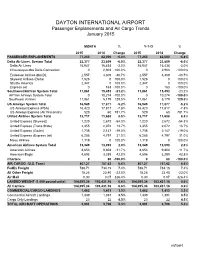

DAYTON INTERNATIONAL AIRPORT Passenger Enplanements and Air Cargo Trends January 2015

DAYTON INTERNATIONAL AIRPORT Passenger Enplanements and Air Cargo Trends January 2015 MONTH % Y-T-D % 2015 2014 Change 2015 2014 Change PASSENGER ENPLANEMENTS 77,253 82,000 -5.8% 77,253 82,000 -5.8% Delta Air Lines, System Total 22,377 23,809 -6.0% 22,377 23,809 -6.0% Delta Air Lines 15,947 16,434 -3.0% 15,947 16,434 -3.0% Chautauqua dba Delta Connection 0 2,903 -100.0% 0 2,903 -100.0% Endeavor Airlines dba DL 2,557 4,309 -40.7% 2,557 4,309 -40.7% Skywest Airlines (Delta) 1,526 0 100.0% 1,526 0 100.0% Shuttle America 2,347 0 100.0% 2,347 0 100.0% Express Jet 0 163 -100.0% 0 163 -100.0% Southwest/AirTran System Total 11,861 15,453 -23.2% 11,861 15,453 -23.2% AirTran Airways System Total 0 10,274 -100.0% 0 10,274 -100.0% Southwest Airlines 11,861 5,179 129.0% 11,861 5,179 129.0% US Airways System Total 16,949 17,877 -5.2% 16,949 17,877 -5.2% US Airways Express (PSA) 16,420 17,817 -7.8% 16,420 17,817 -7.8% US Airways Express (Air Wsconsin) 529 60 781.7% 529 60 781.7% United Airlines System Total 12,717 11,688 8.8% 12,717 11,688 8.8% United Express (Skywest) 1,220 2,672 -54.3% 1,220 2,672 -54.3% United Express (Trans State) 2,355 2,072 13.7% 2,355 2,072 13.7% United Express (GoJet) 1,738 2,147 -19.0% 1,738 2,147 -19.0% United Express (Express Jet) 6,285 4,797 31.0% 6,285 4,797 31.0% Mesa Airlines 1,119 0 100.0% 1,119 0 100.0% American Airlines System Total 13,349 13,093 2.0% 13,349 13,093 2.0% American Airlines 8,653 9,804 -11.7% 8,653 9,804 -11.7% American Eagle 4,696 3,289 42.8% 4,696 3,289 42.8% Charters 0 80 -100.0% 0 80 -100.0% AIR CARGO (U.S. -

Overview and Trends

9310-01 Chapter 1 10/12/99 14:48 Page 15 1 M Overview and Trends The Transportation Research Board (TRB) study committee that pro- duced Winds of Change held its final meeting in the spring of 1991. The committee had reviewed the general experience of the U.S. airline in- dustry during the more than a dozen years since legislation ended gov- ernment economic regulation of entry, pricing, and ticket distribution in the domestic market.1 The committee examined issues ranging from passenger fares and service in small communities to aviation safety and the federal government’s performance in accommodating the escalating demands on air traffic control. At the time, it was still being debated whether airline deregulation was favorable to consumers. Once viewed as contrary to the public interest,2 the vigorous airline competition 1 The Airline Deregulation Act of 1978 was preceded by market-oriented administra- tive reforms adopted by the Civil Aeronautics Board (CAB) beginning in 1975. 2 Congress adopted the public utility form of regulation for the airline industry when it created CAB, partly out of concern that the small scale of the industry and number of willing entrants would lead to excessive competition and capacity, ultimately having neg- ative effects on service and perhaps leading to monopolies and having adverse effects on consumers in the end (Levine 1965; Meyer et al. 1959). 15 9310-01 Chapter 1 10/12/99 14:48 Page 16 16 ENTRY AND COMPETITION IN THE U.S. AIRLINE INDUSTRY spurred by deregulation now is commonly credited with generating large and lasting public benefits. -

Columbus Regional Airport Authority

COLUMBUS REGIONAL AIRPORT AUTHORITY - PORT COLUMBUS INTERNATIONAL AIRPORT TRAFFIC REPORT October, 2009 11/24/2009 Airline Enplaned Passengers Deplaned Passengers Enplaned Air Mail Deplaned Air Mail Enplaned Air Freight Deplaned Air Freight Landings Landed Weight Air Canada Jazz - Regional 1,385 1,432 0 0 0 0 75 2,548,600 Air Canada Jazz Totals 1,385 1,432 0 0 0 0 75 2,548,600 AirTran 16,896 16,563 0 0 0 0 186 20,832,000 AirTran Totals 16,896 16,563 0 0 0 0 186 20,832,000 American 13,482 13,047 10,256 13,744 0 75 120 14,950,000 American Connection - Chautauqua 0 0 0 0 0 0 0 0 American Eagle 22,258 22,818 0 0 2,497 3,373 550 24,434,872 American Totals 35,740 35,865 10,256 13,744 2,497 3,448 670 39,384,872 Continental 5,584 5,527 24,724 17,058 6,085 12,750 57 6,292,000 Continental Express - Chautauqua 4,469 4,675 0 0 477 0 110 4,679,500 Continental Express - Colgan 2,684 3,157 0 0 0 0 69 4,278,000 Continental Express - CommutAir 1,689 1,630 0 0 0 0 64 2,208,000 Continental Express - ExpressJet 3,821 3,334 0 0 459 1,550 100 4,122,600 Continental Totals 18,247 18,323 24,724 17,058 7,021 14,300 400 21,580,100 Delta 14,640 13,970 0 0 9,692 38,742 119 17,896,000 Delta Connection - Atlantic SE 2,088 2,557 0 1 369 2 37 2,685,800 Delta Connection - Chautauqua 13,857 13,820 0 0 0 0 359 15,275,091 Delta Connection - Comair 1,890 1,802 0 0 0 0 52 2,444,000 Delta Connection - Mesa/Freedom 0 0 0 0 0 0 0 0 Delta Connection - Pinnacle 0 0 0 0 0 0 0 0 Delta Connection - Shuttle America 4,267 4,013 0 0 0 0 73 5,471,861 Delta Connection - SkyWest 0 0 0 0