Mass Transit Rail

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Railway Network

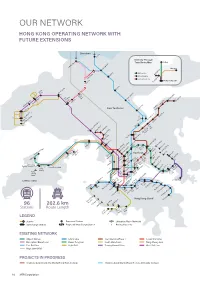

Railway Network Railways play a vital role in serving the transport needs of COVID-19 pandemic. By end 2020, the AEL carries about Hong Kong. They account for about 39 per cent of domestic 8 400 passenger trips per day. public transport by end 2020. Light Rail: Light Rail is a local transportation network Existing Network: The existing railway network in Hong which started operation in 1988 to meet the transport needs of Kong has a total route length of about 263 kilometres. The the residents in the northwest New Territories. It now has a Legislative Council passed in June 2007 the Rail Merger route length of about 36 km with 68 stops. By end 2020, it Ordinance which provides the legal framework for the carries an average of about 305 600 passenger trips every post-merger corporation to operate both the Mass Transit day. It has four interchange stations in Yuen Long, Tin Shui Railway (MTR) system and Kowloon-Canton Railway (KCR) Wai, Siu Hong and Tuen Mun to facilitate passenger system. The post-merger Corporation, i.e. the MTR interchange between the Light Rail and West Rail Line Corporation Limited (MTRCL) has been granted a 50-year networks. franchise to operate the MTR and KCR systems with effect from December 2, 2007. Other fixed track systems include the Hong Kong Section of Guangzhou-Shenzhen-Hong Tramway and the Peak Tram. Kong Express Rail Link (XRL): The Hong Kong section of the XRL, commissioned in September 2018, is a 26-km long MTR: MTR is a heavily patronized railway network underground rail corridor connecting Hong Kong with the consisting of 10 heavy rail lines, Airport Express and the Hong national high-speed rail network. -

Pre-Feasibility Study on Yangon Circular Railway Modernization Project

32mm Republic of the Union of Myanmar Yangon Regional Government PROJECT FOR COMPREHENSIVE URBAN TRANSPORT PLAN OF THE GREATER YANGON (YUTRA) Pre-Feasibility Study on Yangon Circular Railway Modernization Project Final Report January 2015 Japan International Cooperation Agency (JICA) ALMEC Corporation Oriental Consultants Co., Ltd Nippon Koei Co., Ltd EI JR 14-208 The exchange rate used in the report is: US$ 1.00 = MMK 1,000.00 Project for Comprehensive Urban Transport Plan of the Greater Yangon (YUTRA) Pre-Feasibility Study on Yangon Circular Railway Modernization Project FINAL REPORT TABLE OF CONTENTS 1 UPPER PLANNING, COMPREHENSION OF THE CURRENT ISSUE 1.1 CURRENT SITUATION AND ISSUE OF TRANSPORT SECTOR IN THE GREATER YANGON .................. 1-1 1.1.1 GENERAL ............................................................................................................ 1-1 1.1.2 MAIN TRANSPORT COMPONENTS ......................................................................... 1-2 1.1.3 TRANSPORT DEMAND CHARACTERISTICS ............................................................. 1-9 1.2 CURRENT SITUATION AND ISSUE OF RAILWAY SECTOR IN THE GREATER YANGON ...................... 1-11 1.2.1 RAILWAY IN GREATER YANGON ........................................................................... 1-11 1.2.2 CURRENT SITUATION AND ISSUES ........................................................................ 1-13 1.3 COMPREHENSION OF THE CURRENT UPPER PLANNING AND POLICY OF RAILWAY SECTOR IN YANGON REGION .................................................................................................................... -

Elevated Railway Structures and Urban Life

DEGREE PROJECT IN THE BUILT ENVIRONMENT, SECOND CYCLE, 15 CREDITS STOCKHOLM, SWEDEN 2018 Urban movers – elevated railway structures and urban life HANS VILJOEN TRITA TRITA-ABE-MBT-18414 KTH ROYAL INSTITUTE OF TECHNOLOGY SCHOOL OF ARCHITECTURE AND THE BUILT ENVIRONMENT www.kth.se urban movERS ELEVATED RAILWAY STRUCTURES AND URBAN LIFE Hans Viljoen 2 3 abstract index Elevated railway structures (ERS) urban type, an infrastructural type 1. BACKGROUND has for more than a century been and other typologies. 39 types of evolving as an urban archetype. Pre- ERS interventions are described as 2. PROBLEMATISING ERS sent in various forms in cities across the result of a global literary and ex- the globe, to transport the increasing periential search of various instances 3. THEORISING ERS URBAN MOVERS number of citizens, ERS are urban in- of ERS and projects that seek their ELEVATED RAILWAY frastructures that perform a vital role urban integration. It is a search for 4. POTENTIALISING ERS STRUCTURES AND in curbing congestion and pollution the potentials of ERS to contribute URBAN LIFE that plague cities so often. In spite of to urban life and urban form, beyond 5. CONCLUSION their sustainable transport benefits, their main transport function - po- First published in 2018. ERS are often viewed negatively as tentializing ERS. 6. REFERENCES written by Hans Viljoen. noisy, ugly and severing urban form, amongst other problems which will #elevated railway structures, 7. PICTURE CREDITS contact: [email protected] be elaborated on - problematising #elevated transit structures, #urban ERS. A theorisation of these prob- typologies, #urban infrastructures, Final presentation: 07.06.2018 #transport, #railways Examiner: Tigran Haas lems follows, looking at ERS as an Supervisor: Ryan Locke AG218X Degree Project in Urban Studies, Second Cycle 15.0 credits Master’s Programme in Urbanism Studies, 60.0 credits School of Architecture and the Built Environment KTH Royal Institute of Technology Stockholm, Sweden Telephone: +46 8 790 60 00 Cover image. -

Evaluation Summary

Evaluation Summary 1. Outline of the Project Country: Project title: Socialist Republic of Vietnam The technical assistance project to strengthen the capacity of regulator and to establish operation & maintenance company of metropolitan railway lines in Hanoi city Sector: Transportation Cooperation scheme: Technical Cooperation Division in charge: Total cost (at the time of evaluation): 320 million yen Transportation and ICT Group, Infrastructure and Peace Building Department Period of (R/D): Partner country’s implementing organization: cooperation February 2013 – February Hanoi Metro One-member Limited Liability Company 2015 (HMC), Hanoi Department of Transportation (DOT), (Extension): Hanoi Metropolitan Railway Management Board March 2013 – February (MRB) 2016 Supporting organization in Japan: Tokyo Metro co,. Ltd., Japan International consultants for Transportation co., Ltd. Related cooperation: Study for special assistance for project implementation of the construction of Line 2 (JICA), Urban railway transport administration advisor (Ministry of land, Infrastructure, Transport and Tourism) 1-1 Background of the Project In Hanoi, the capital of Vietnam, the volume of road traffic has been increasing rapidly in recent years as the population increases. Problems such as increased traffic congestion, lowered traffic safety, and air pollution interfere with urban activities. In the future, the traffic problems will become increasingly serious; therefore, it is necessary to establish an urban railway system for the sustainable development of the City. Under the situation, JICA conducted a comprehensive urban development program in Hanoi capital city of the Socialist Republic of Vietnam (ended in March 2007). As a result of the study, a master plan was prepared on the transportation and traffic sector targeting 2020, which includes the construction of an urban mass rapid transit system in Hanoi. -

Transport Infrastructure and Traffic Review

Transport Infrastructure and Traffic Review Planning Department October 2016 Hong Kong 2030+ 1 TABLE OF CONTENTS 1 PREFACE ........................................................... 1 5 POSSIBLE TRAFFIC AND TRANSPORT 2 CHALLENGES ................................................... 2 ARRANGEMENTS FOR THE STRATEGIC Changing Demographic Profile .............................................2 GROWTH AREAS ............................................. 27 Unbalanced Spatial Distribution of Population and Synopsis of Strategic Growth Areas ................................. 27 Employment ........................................................................3 Strategic Traffic and Transport Directions ........................ 30 Increasing Growth in Private Vehicles .................................6 Possible Traffic and Transport Arrangements ................. 32 Increasing Cross-boundary Travel with Pearl River Delta Region .......................................................................7 3 FUTURE TRANSPORT NETWORK ................... 9 Railways as Backbone ...........................................................9 Future Highway Network at a Glance ................................11 Connecting with Neighbouring Areas in the Region ........12 Transport System Performance ..........................................15 4 STRATEGIC DEVELOPMENT DIRECTIONS FROM TRAFFIC AND TRANSPORT PERSPECTIVE ................................................. 19 Transport and Land Use Optimisation ...............................19 Railways Continue to be -

Climate Policies in Transport Sector of Vietnam And

MINISTRY OF TRANSPORT TRANSPORT DEVELOPMENT AND STRATEGY INSTITUTE URBAN PUBLIC TRANSPORT SYSTEM IN VIETNAM Presenter: Le Thi Thanh Nhan (MSc) Energy Efficiency in Emerging Economies Training Week for Southest Asia Jakarta, 16 to 20 July, 2018 Vietnam at a glance Population: 93.5 million people Urban population: 32.3 million people Urbanization rate: 34.5% Urban contribution: 70 - 75% of the GDP Vietnam at a glance • There are 788 urban areas in the whole Viet Nam, including 02 special urban areas (Ha Noi, HCMC) Several figures: 2.9 million automobiles 46 million motorbikes 492 motorbike/1000 population • The competitive index of Vietnam transport infrastructures ranked the 67th of the 138 countries in 2015-2016 period • The urbanization process growths very fast (3.4% per year) resulting in higher and higher traffic demands, and a boom of individual vehicles (i.e. cars, motorbikes) in large urban areas, and severe status of traffic congestion Urban Public Transport in Vietnam Conventional bus BRT Metro River bus Urban Public Transport in Vietnam Conventional bus 61/63 provinces have public bus system with total passenger transported: more than 1 billion/year Structure of bus routes in cities in 2015 Urban Public Transport in Vietnam River bus Operating in Ho Chi Minh City with 01 route 10,8km Metros Under construction in 02 cities are Ha Noi and Ho Chi Minh City MRT system in Hanoi Hanoi: ( Decision 1259/2011/QD-TTg) 8 metro lines with 318 km Line 2A and 3: under construction Line 2A: 13.1 km elevated, 12 stations Line 3: 12.5 km (8.5 km elevated, 4 km underground, 12 stations MRT system in HCMC HCMC: (Decision 568/2013/QD-TTg) 08 metro lines (1, 2, 3a, 3b, 4, 4b, 5, 6) 03 tram lines/1 monorail line (T) 01 elevated rail line (E) MRT Line 1, 2, 5: Under construction BRT system in Hanoi . -

Hong Kong Government's Policy Address 2020

Hong Kong Government’s Policy Address 2020 Key Takeaways primarily relevant to the Real Estate and Infrastructure sector November 25, 2020 Summary Authors/Presenters This year’s Policy Address was delivered today (25th November 2020) amidst the backdrop of a changing and dynamic environment. The Chief Executive (“CE”) has set out a variety of key initiatives to address the city’s land Andrew MacGeoch and housing supply, infrastructure, the environment, Co-Author collaboration with the Greater Bay Area (“GBA”), and HK’s Partner and Regional Practice Group Leader - Real Estate ongoing role as an international financial center. We set Asia out a list of key takeaways below highlighting primarily Hong Kong [email protected] those aspects involving real estate and infrastructure. OPENING This year’s Policy Address was delivered today (25th November 2020) amidst the backdrop of a changing and dynamic environment. The Chief Executive (“CE”) has set out a variety of key initiatives to address the city’s land and housing supply, infrastructure, the environment, collaboration with the Greater Bay Area (“GBA”), and HK’s ongoing role as an international financial center. We set Page 1 of 11 out a list of key takeaways below highlighting primarily those aspects involving real estate and infrastructure. LAND SUPPLY Increasing land supply is a top priority of the Government. Glenn Haley At present, the Government has identified new land supply Co-Author with a total area of 90 hectares along the Northern Link, Partner Hong Kong including the San Tin / Lok Ma Chau Development Node. [email protected] Further initiatives to support the increase of land supply include: Development of Siu Ho Wan Depot Site. -

Trams Der Welt / Trams of the World 2021 Daten / Data © 2021 Peter Sohns Seite / Page 1

www.blickpunktstrab.net – Trams der Welt / Trams of the World 2021 Daten / Data © 2021 Peter Sohns Seite / Page 1 Algeria ... Alger (Algier) ... Metro ... 1435 mm Algeria ... Alger (Algier) ... Tram (Electric) ... 1435 mm Algeria ... Constantine ... Tram (Electric) ... 1435 mm Algeria ... Oran ... Tram (Electric) ... 1435 mm Algeria ... Ouragla ... Tram (Electric) ... 1435 mm Algeria ... Sétif ... Tram (Electric) ... 1435 mm Algeria ... Sidi Bel Abbès ... Tram (Electric) ... 1435 mm Argentina ... Buenos Aires, DF ... Metro ... 1435 mm Argentina ... Buenos Aires, DF - Caballito ... Heritage-Tram (Electric) ... 1435 mm Argentina ... Buenos Aires, DF - Lacroze (General Urquiza) ... Interurban (Electric) ... 1435 mm Argentina ... Buenos Aires, DF - Premetro E ... Tram (Electric) ... 1435 mm Argentina ... Buenos Aires, DF - Tren de la Costa ... Tram (Electric) ... 1435 mm Argentina ... Córdoba, Córdoba ... Trolleybus Argentina ... Mar del Plata, BA ... Heritage-Tram (Electric) ... 900 mm Argentina ... Mendoza, Mendoza ... Tram (Electric) ... 1435 mm Argentina ... Mendoza, Mendoza ... Trolleybus Argentina ... Rosario, Santa Fé ... Heritage-Tram (Electric) ... 1435 mm Argentina ... Rosario, Santa Fé ... Trolleybus Argentina ... Valle Hermoso, Córdoba ... Tram-Museum (Electric) ... 600 mm Armenia ... Yerevan ... Metro ... 1524 mm Armenia ... Yerevan ... Trolleybus Australia ... Adelaide, SA - Glenelg ... Tram (Electric) ... 1435 mm Australia ... Ballarat, VIC ... Heritage-Tram (Electric) ... 1435 mm Australia ... Bendigo, VIC ... Heritage-Tram -

GMT Global Metro Projects Report 2018.Qxp

GLOBAL METRO PROJECTS REPORT 2018 The continued growth of the metrorail sector across the world has reinforced its role in urban transportation and boosted the order book of many construction contractors and equipment suppliers. The sector has benefited from favourable government policies, public investment and recognition as the mode of choice for transport authorities interested in providing sustainable urban mobility solutions for Smart Cities. The industry has many opportunities because the existing lines and rolling stock need renewal and upgrade; there is a strong pipeline of projects which are in approval or planning phase and new business segments such as asset management, support for complex construction and operations planning have opened up in the services sector. Transport authorities are keen to improve service reliability, operations efficiency and environmental sustainability of the existing metrorail systems as well as lower costs and implementation timelines of upcoming systems. New technology has enabled greater engagement with the customers through integrated electronic ticketing and Wi-Fi, demand-based and flexible service for crowd management, real-time passenger alerts, low downtime due to predictive maintenance and increased lifespan of assets. The transport authorities adopting best practices in these areas receive the benefits of enhanced image and high ridership. The Global Metro Projects Report 2018 assesses the current metrorail sector and identifies upcoming opportunities. It provides updated information on 100 metro projects from 52 countries representing over 80 per cent of the world's gross domestic product. The report is comprehensive in its coverage of opportunities in the development of new lines, extension and upgrades of existing lines, rolling stock procurement and refurbishment, power and communication systems upgrades, fare systems, as well as station construction and refurbishment. -

May 2018'S Green Infrastructure Investment Opportunities

GREEN INFRASTRUCTURE INVESTMENT OPPORTUNITIES INDONESIA Published by the Climate Bonds Initiative Developed in partnership with Pembiayaan Investasi Non-Anggaran Pemerintah (PINA), a project of the National Development Planning Agency (BAPPENAS), and PT. EBA Indonesia. Green Infrastructure Investment Opportunities, Indonesia Contents This report highlights green infrastructure investment 3 Executive summary opportunities in Indonesia 4 Indonesia’s green infrastructure: an This report has been prepared to support “green”, are presented in a pipeline of opportunity for change Indonesia’s mission to develop low-carbon opportunities for investment in 2018-2019. and climate-resilient infrastructure. It Priorities for investment beyond 2019 are 5 Enabling infrastructure highlights green infrastructure investment also covered. investments will boost growth opportunities, with the aim of facilitating The report is part of a research series 7 Opportunities in global green engagement on this topic between project which will investigate green infrastructure finance owners and developers, and investors. investment opportunities in ASEAN 13 Green infrastructure investment The report is intended for a wide range (Association of Southeast Asian Nations) opportunities of stakeholders in Indonesia and abroad, member countries. including domestic and international 14 Transport In developing this report the Climate investors, companies and developers, 17 Energy Bonds Initiative consulted the Indonesian and relevant Indonesian Government 21 Water and waste -

Addressing Climate Change in Transport

Addressing Climate Change in Transport Volume 1: Pathway to Low-Carbon Transport Vietnam Transport Knowledge Series Supported by AUSTRALIA–WORLD BANK GROUP STRATEGIC PARTNERSHIP IN VIETNAM and NDC PARTNERSHIP SUPPORT FACILITY Addressing Climate Change in Transport Volume 1: Pathway to Low-Carbon Transport Jung Eun Oh, Maria Cordeiro, John Allen Rogers, Khanh Nguyen Daniel Bongardt, Ly Tuyet Dang, Vu Anh Tuan FINAL REPORT September 2019 © 2019 The World Bank and Deutsche Gesellschaft für Internationale Zusammenarbeit GmbH 1818 H Street NW, Washington DC 20433 Telephone: 202-473-1000; Internet: www.worldbank.org This work is a product of the staff of The World Bank and the Deutsche Gesellschaft für Internationale Zusammenarbeit (GIZ) with external contributions. The findings, interpretations, and conclusions expressed in this work do not necessarily reflect the views of The World Bank and its Board of Executive Directors. The World Bank or GIZ does not guarantee the accuracy or completeness of information in this document, and cannot be held responsible for any errors, omissions or losses, which emerge from its use. The boundaries, colors, denominations and other information as shown on any map in this work do not imply any judgment on the part of The World Bank or GIZ concerning the legal status of any territory or the endorsement or acceptance of such boundaries. Nothing herein shall constitute or be considered to be a limitation upon or waiver of the privileges and immunities of The World Bank, all of which are specifically reserved. All queries on rights and licenses should be addressed to the Publishing and Knowledge Division, The World Bank, 1818 H Street NW, Washington DC 20433, USA; fax: 202-522-2625; email: [email protected]. -

Our Network Hong Kong Operating Network with Future Extensions

OUR NETWORK HONG KONG OPERATING NETWORK WITH FUTURE EXTENSIONS Shenzhen Lo Wu Intercity Through Train Route Map Beijing hau i C Lok Ma Shanghai Sheung Shu g Beijing Line Guangzhou Fanlin Shanghai Line Kwu Tung Guangdong Line n HONG KONG SAR Dongguan San Ti Tai Wo Long Yuen Long t Ping 48 41 47 Ngau a am Tam i Sh i K Mei a On Shan a Tai Po Marke 36 K Sheungd 33 M u u ui Wa W Roa Au Tau Tin Sh 49 Heng On y ui Hung Shui Ki g ng 50 New Territories Tai Sh Universit Han Siu Ho 30 39 n n 27 35 Shek Mu 29 Tuen Mu cecourse* e South Ra o Tan Area 16 F 31 City On Tuen Mun n 28 a n u Sha Ti Sh n Ti 38 Wai Tsuen Wan West 45 Tsuen05 Wa Tai Wo Ha Che Kung 40 Temple Kwai Hing 07 i 37 Tai Wa Hin Keng 06 l Kwai Fong o n 18 Mei Fo k n g Yi Diamond Hil Kowloon Choi Wa Tsin Tong n i King Wong 25 Shun Ti La Lai Chi Ko Lok Fu d Tai Si Choi Cheung Sha Wan Hung Sau Mau Ping ylan n ay e Sham Shui Po ei Kowloon ak u AsiaWorld-Expo B 46 ShekM T oo Po Tat y Disn Resort m Po Lam Na Kip Kai k 24 Kowl y Sunn eong g Hang Ha Prince n Ba Ch o Sungong 01 53 Airport M Mong W Edward ok ok East 20 K K Toi ong 04 To T Ho Kwa Ngau Tau Ko Cable Car n 23 Olympic Yau Mai Man Wan 44 n a Kwun Ti Ngong Ping 360 19 52 42 n Te Ti 26 Tung Chung East am O 21 L Tung Austi Yau Tong Tseung Chung on Whampo Kwan Tung o n Jordan Tiu g Kowl loo Tsima Hung 51 Ken Chung w Sh Hom Leng West Hong Kong Tsui 32 t Tsim Tsui West Ko Eas 34 22 ha Fortress10 Hill Hong r S ay LOHAS Park ition ew 09 Lantau Island ai Ying Pun Kong b S Tama xhi aus North h 17 11 n E C y o y Centre Ba Nort int 12 16 Po 02 Tai