The Rouse Compan Y

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

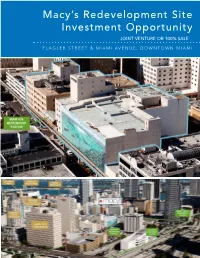

Macy's Redevelopment Site Investment Opportunity

Macy’s Redevelopment Site Investment Opportunity JOINT VENTURE OR 100% SALE FLAGLER STREET & MIAMI AVENUE, DOWNTOWN MIAMI CLAUDE PEPPER FEDERAL BUILDING TABLE OF CONTENTS EXECUTIVE SUMMARY 3 PROPERTY DESCRIPTION 13 CENTRAL BUSINESS DISTRICT OVERVIEW 24 MARKET OVERVIEW 42 ZONING AND DEVELOPMENT 57 DEVELOPMENT SCENARIO 64 FINANCIAL OVERVIEW 68 LEASE ABSTRACT 71 FOR MORE INFORMATION, CONTACT: PRIMARY CONTACT: ADDITIONAL CONTACT: JOHN F. BELL MARIANO PEREZ Managing Director Senior Associate [email protected] [email protected] Direct: 305.808.7820 Direct: 305.808.7314 Cell: 305.798.7438 Cell: 305.542.2700 100 SE 2ND STREET, SUITE 3100 MIAMI, FLORIDA 33131 305.961.2223 www.transwestern.com/miami NO WARRANTY OR REPRESENTATION, EXPRESS OR IMPLIED, IS MADE AS TO THE ACCURACY OF THE INFORMATION CONTAINED HEREIN, AND SAME IS SUBMITTED SUBJECT TO OMISSIONS, CHANGE OF PRICE, RENTAL OR OTHER CONDITION, WITHOUT NOTICE, AND TO ANY LISTING CONDITIONS, IMPOSED BY THE OWNER. EXECUTIVE SUMMARY MACY’S SITE MIAMI, FLORIDA EXECUTIVE SUMMARY Downtown Miami CBD Redevelopment Opportunity - JV or 100% Sale Residential/Office/Hotel /Retail Development Allowed POTENTIAL FOR UNIT SALES IN EXCESS OF $985 MILLION The Macy’s Site represents 1.79 acres of prime development MACY’S PROJECT land situated on two parcels located at the Main and Main Price Unpriced center of Downtown Miami, the intersection of Flagler Street 22 E. Flagler St. 332,920 SF and Miami Avenue. Macy’s currently has a store on the site, Size encompassing 522,965 square feet of commercial space at 8 W. Flagler St. 189,945 SF 8 West Flagler Street (“West Building”) and 22 East Flagler Total Project 522,865 SF Street (“Store Building”) that are collectively referred to as the 22 E. -

Mary Ann E. Mears 903 Poplar Hill Road Baltimore, Maryland 21210 Phone: 410 435-2265 Website: Email: [email protected]

Mary Ann E. Mears 903 Poplar Hill Road Baltimore, Maryland 21210 Phone: 410 435-2265 Website: www.maryannmears.com email: [email protected] COMMISSIONS: 2015 Petal Play, Columbia Downtown Project, Parcel D, West Promenade, Columbia, MD (interactive, painted aluminum, stainless, water, text, and lighting,14 pieces from 2’ to 28’ height) 2014 Reston Rondo, Reston Town Center, Reston, VA (painted aluminum 18’ h) 2013 Aeriads, Private Residence, Annapolis, MD (exterior relief, painted aluminum 13’ x 3’x 5”) 2013 Charispiral, Spaulding Rehabilitation Hospital, Boston, MA (exterior, painted aluminum, 17’x13’x 8’) 2011 Spun Grace, St. Agnes Hospital, Baltimore, MD (suspended, moving, painted aluminum, 12’x 40’x 30’) 2010 Calla Pods, Private Residence, Baltimore MD (exterior, painted aluminum, 4 forms 3’h - ‘6-6” h) 2009 Lotus Columns, Silver Spring, MD (exterior, eight column forms, stainless 14’ 8”-16’ h) 2009 Sun Drops, Private Residence, Baltimore MD (exterior, painted aluminum, 3 forms 4’h - 5’ h) 2008 Leaps and Bounds, University of Central Florida, Orlando (interior relief, ptd. aluminum 15’x 28’) 2006 Callooh Callay, Millenium Bike Trail, Anne Arundel County, MD (painted aluminum 16’ h) 2004 Floating Garden, Cheverly Health Center, commissioned by the Prince George’s County Revenue Authority, MD (suspended, ptd. aluminum and stainless, 20’x 36’x 44’) 2003 Gyre and Gimble, Betty Ann Krahnke Intermission Terrace, Imagination Stage, Bethesda Academy of Performing Arts, MD (site extends length of a city block, stainless and painted aluminum) -

Columbia Archives Ephemera-Memorabilia-Artifacts Collection

Columbia Archives Ephemera-Memorabilia-Artifacts Collection James W. Rouse's "Photo James W. Rouse's Fishing James W. Rouse's Ice Skates, Shoot" Eyeglasses, n.d. Pole, n.d. n.d. Desk Pen Set Presented to Shovel for Cherry Hill Mall Shovel for The Rouse James W. Rouse from the Expansion Ground Breaking, Company Headquarters Young Columbians, 1975 1976 Ground Breaking, 1972 Whistle Nancy Allison Used Cross Keys Inn Ashtray, n.d. Waterside Restaurant to Summon James W. Rouse Ashtray, n.d. to Meetings, n.d. Columbia Bank and Trust People Tree Ashtray, 1968 Clyde's Restaurant Ashtray, Company Ashtray, 1968 n.d. Columbia All Star Swim Head Ski and Sportswear Columbia Volksmarch Club Meet Badge, n.d. Company Badge, n.d. Badge for Columbia's 20th Birthday, 1987 Columbia Volksmarch Club Town Center 25th Columbia Bank and Trust Badge, 1986 Anniversary Products, 1999 Company Moneybag, n.d. The Mall in Columbia 40th Produce Galore Bag for Kings Contrivance Village Anniversary Shopping Bag, Coffee Beans, 2008 Center Shopping Bag, n.d. 2011 Wilde Lake Village Green Columbia Aquatics Owen Brown Interfaith Holiday Shopping Bag, n.d. Association Swim Bag, n.d. Center Token Noting Surplus Budget, ca. 1984 Hickory Ridge Village Columbia 20th Birthday Rotary Club of Columbia Center Ball, n.d. Balloon, 1987 Town Center Banner, n.d. Rotary Club of Columbia Sewell's Orchards Fruit Sewell's Orchards Fruit Banner, n.d. Basket, n.d. Basket, n.d. www.ColumbiaArchives.org Page 1 Columbia Archives Ephemera-Memorabilia-Artifacts Collection "Columbia: The Next Columbia Voyage Wine Columbia 20th Birthday America Game", 1982 Bottle, 1992 Chateau Columbia Wine Bottle, 1986 Columbia 20th Birthday Santa Remembers Me ™ Merriweather Park at Champagne Bottle, 1987 Bracelet from the Mall Symphony Woods Bracelet, in Columbia, 2007 2015 Anne Dodd for Howard Columbia Gardeners Bumper Columbia Business Card County School Board Sticker, 1974 Case, n.d. -

Colors for Bathroom Accessories

DUicau kji oLctnufcirus DEC 6 1937 CS63-38 Colors (for) Bathroom Accessories U. S. DEPARTMENT OF COMMERCE DANIEL C. ROPER, Secretary NATIONAL BUREAU OF STANDARDS LYMAN J. BRIGGS, Director COLORS FOR BATHROOM ACCESSORIES COMMERCIAL STANDARD CS63-38 Effective Date for New Production, January I, 1938 A RECORDED STANDARD OF THE INDUSTRY UNITED STATES GOVERNMENT PRINTING OFFICE WASHINGTON : 1S37 For sale by the Superintendent of Documents, Washington, D. C. Price 5 cents U. S. Department of Commerce National Bureau of Standards PROMULGATION of COMMERCIAL STANDARD CS63-38 for COLORS FOR BATHROOM ACCESSORIES On April 30, 1937, at the instance of the National Retail Dry Goods Association, a general conference of representative manufacturers, dis- tributors, and users of bathroom accessories adopted seven commercial standard colors for products in this field. The industry has since ac- cepted and approved for promulgation by the United States Depart- ment of Commerce, through the National Bureau of Standards, the standard as shown herein. The standard is effective for new production from January 1, 1938. Promulgation recommended. I. J. Fairchild, Chief, Division of Trade Standards. Promulgated. Lyman J. Briggs, Director, National Bureau of Standards. Promulgation approved. Daniel C. Roper, Secretary of Commerce. II COLORS FOR BATHROOM ACCESSORIES COMMERCIAL STANDARD CS63-38 PURPOSE 1 . Difficulty in securing a satisfactory color match between articles purchased for use in bathrooms, where color harmony is essential to pleasing appearance, has long been a source of inconvenience to pur- chasers. This difficulty is greatest when items made of different materials are produced by different manufacturers. Not only has this inconvenienced purchasers, but it has been a source of trouble and loss to producers and merchants through slow turnover, multiplicity of stock, excessive returns, and obsolescence. -

Alderwood Altamonte Mall Apache Mall Augusta Mall Baybrook Mall

Official Rules - New Year Fitness Resolution Sweepstakes NO PURCHASE NECESSARY TO ENTER OR WIN. This promotion is not administered by, sponsored, endorsed, or associated with Facebook or Instagram. This Sweepstakes is solely sponsored by General Growth Services, Inc. (“GGSI” or "Sponsor"), it is a national Sweepstakes marketeD at each of the Participating Malls (“Participating Malls”) referenceD-below. DATES: Enter once between January 15, 2018 3:00 PM CST and February 9, 2018 11:59 PM CST (“Promotional Period”). Limit one entry per person. ENTRY: Visit a Participating Mall’s Facebook (“FB”) page, and look for the Sweepstakes message we post and answer the questions on our timeline. ELIGIBILITY: The Sweepstakes is open to legal residents of the 50 United States or D.C., age 18 or older. Employees and officers of GGSI and their respectiVe parent and subsidiary companies and affiliates are not eligible to enter or win. Immediate family members and household members of such indiViduals are also not eligible to enter or win. "Immediate family members" shall mean parents, step-parents, legal guardians, children, step-children, siblings, step-siblings, or spouses. "Household members" shall mean those people who share the same residence at least three months a year. PRIZE/WINNER SELECTION/ODDS: Winner will be selected in a random drawing. The odds of winning depend on the total number of entries receiVed nationally. One Grand Prize winner to receiVe a $100 GGP Gift Card. CLAIMING PRIZE: Winner will be notified (“Win Notification”) Via FB by the Sponsor and will haVe 4 days after the Win Notification to contact the Sponsor. -

2018 Graduation Information

2018 GRADUATION INFORMATION Graduates and Families, Our 2018 Graduation Ceremony is almost here! DATE: Thursday, July 12, 2018 at 3 p.m. LOCATION: Comerica Theatre ADDRESS: 400 W. Washington St., Phoenix, AZ 85003 Please review the following information about the ceremony, which includes directions to Comerica Theatre, an area map, a list of local hotels and restaurants, frequently asked questions and helpful post-graduation information. All graduates must arrive between 11 a.m - 12:15 p.m. to check in. Cap and gown distribution will also take place during this time for students who have not already recieved these items. A rehearsal and final review of event details by our staff will begin at 12:15 p.m. for all graduates that are partcipating in the ceremony. Please arrive at the scheduled time to ensure that we can rehearse and begin the ceremony on time. Guests will be seated once the theater doors are opened at approximately 2 p.m. The ceremony will begin promptly at 3 p.m., so we ask that all guests find their seats prior to this time. If you have any questions regarding the ceremony, please email us at [email protected] or contact your guidance counselor. We look forward to celebrating this special occasion with you—what an accomplishment! Sincerely, Primavera Faculty and Staff 2471 N. Arizona Ave PHONE 480.456.6678 Chandler, AZ 85225 TOLL FREE 877.877.4628 ChoosePrimavera.com FAX 480.355.2100 2018 Graduation Information DIRECTIONS COMERICA THEATRE 400 W. Washington St., Phoenix, AZ 85003 comericatheater.com Directions from Interstate 17: EXIT on Jefferson St. -

Sports Facilities, Redevelopment, and the Centrality of Downtown Areas: Observations and Lessons from Experiences in a Rustbelt and Sunbelt City Mark S

Marquette Sports Law Review Volume 10 Article 7 Issue 2 Spring Sports Facilities, Redevelopment, and the Centrality of Downtown Areas: Observations and Lessons from Experiences in a Rustbelt and Sunbelt City Mark S. Rosentraub Follow this and additional works at: http://scholarship.law.marquette.edu/sportslaw Part of the Entertainment and Sports Law Commons Repository Citation Mark S. Rosentraub, Sports Facilities, Redevelopment, and the Centrality of Downtown Areas: Observations and Lessons from Experiences in a Rustbelt and Sunbelt City, 10 Marq. Sports L. J. 219 (2000) Available at: http://scholarship.law.marquette.edu/sportslaw/vol10/iss2/7 This Symposium is brought to you for free and open access by the Journals at Marquette Law Scholarly Commons. For more information, please contact [email protected]. SPORTS FACILITIES, REDEVELOPMENT, AND THE CENTRALITY OF DOWNTOWN AREAS: OBSERVATIONS AND LESSONS FROM EXPERIENCES IN A RUSTBELT AND SUNBELT CITY MARK S. ROSENTRAUB* I. INTRODUCTION The engines of wealth and economic activity for cities have changed. In the past, center cities were manufacturing, industrial, retail, and ser- vice centers. Today, while industrial output is still important for the eco- nomic health of some cities, consumption, recreation, tourism, and the provision of services are now the principal engines of urban wealth.' In- surance, banking, legal and financial services joined with experiential consumption, traditional retailing, and various forms of entertainment define the new focus for core cities that try to maintain their centrality in a regional economy. This transformation has been continental in scope, as center cities have dedicated substantial amounts of their urban space to these activi- ties. -

Expectations of Store Personnel Managers - Regarding Appropriate Dress for Female Retail Buyers

EXPECTATIONS OF STORE PERSONNEL MANAGERS - REGARDING APPROPRIATE DRESS FOR FEMALE RETAIL BUYERS By JANA KAY GOULD It Bachelor of Science in Home Economics Oklahoma State University Stillwater, Oklahoma 1978 Submitted to the Faculty of the Graduate College of the Oklahoma State University in partial fulfillment of the requirements for the Degree of MASTER OF SCIENCE July, 1981 .. ' ' ' ·~ . ' ' ; EXPECTATIONS OF STORE PERSONNEL MANAGERS REGARDING APPROPRIATE DRESS FOR FEMALE RETAIL BUYERS Thesis Approved: Dean of Graduate College ii 1089'731 ACKNOWLEDGMENTS The writer wishes to express sincere appreciation to Dr. Grovalynn Sisler, Head, Department of Clothing, Textiles and Merchandising, for her encouragement, assistance and support during the course of this study and in preparation of this thesis. Appreciation is also ex tended to Dr. Janice Briggs and Dr. Elaine Jorgenson for their support and guidance during this study and in the preparation of this manu script. A very grateful acknowledgment is extended to Dr. William Warde for his valuable assistance in the computer analysis of the data and to Mrs. Mary Lou Whee.ler for typing the final manuscript. iii TABLE OF CONTENTS Chapter Page I. INTRODUCTION 1 Purpose and Objectives 2 Hypotheses . 3 Assumptions and Limitations 3 Definition of Terms . 4 I I. REV I EH OF LITERATURE . 5 Influence of Clothing on First Impressions 5 Women in the Work Force . • • • 7 Clothing as a Factor in Career Success 9 Characteristics of Fashion Leaders 10 Summary • . • . 12 III. RESEARCH PROCEDURES 13 Type of Research Design ..•.••• 13 Development of the Instrument • 14 Population for the Study 14 Method of Data Analysis • 15 IV. -

Brookfield Properties' Retail Group Overview

Retail Overview Brookfield Properties’ Retail Group Overview We are Great Gathering Places. We embrace our cultural core values of Humility, Attitude, Do The Right Thing, H Together and Own It. HUMILITY Brookfield Properties’ retail group is a company focused A ATTITUDE exclusively on managing, leasing, and redeveloping high- quality retail properties throughout the United States. D DO THE RIGHT THING T TOGETHER O HEADQUARTERS CHICAGO OWN IT RETAIL PROPERTIES 160+ STATES 42 INLINE & FREESTANDING GLA 68 MILLION SQ FT TOTAL RETAIL GLA 145 MILLION SQ FT PROFORMA EQUITY MARKET CAP $20 BILLION PROFORMA ENTERPRISE VALUE $40 BILLION Portfolio Map 2 7 1 4 3 5 3 6 2 1 2 1 1 2 1 3 3 3 1 1 2 4 1 2 1 3 2 1 1 10 4 2 5 1 4 10 2 3 3 1 48 91 6 5 6 2 7 6 4 5 11 7 4 1 1 1 2 2 2 5 7 1 2 1 2 1 1 1 1 6 1 3 5 3 4 15 19 2 14 11 1 1 3 2 1 2 1 1 3 6 2 1 3 4 18 2 17 3 1 2 1 3 2 2 5 3 6 8 2 1 12 9 7 5 1 4 3 1 2 1 2 16 3 4 13 3 1 2 6 1 7 9 1 10 5 4 2 1 4 6 11 5 3 6 2 Portfolio Properties 1 2 3 3 3 1 7 4 Offices 13 12 2 Atlanta, GA 7 3 1 1 Chicago, IL Baltimore, MD 8 5 2 Dallas, TX 4 Los Angeles, CA 6 New York, NY 8 2 9 5 Property Listings by State ALABAMA 7 The Oaks Mall • Gainesville 3 The Mall in Columbia • Columbia (Baltimore) 9 Brookfield Place • Manhattan WASHINGTON 8 Pembroke Lakes Mall • Pembroke Pines 4 Mondawmin Mall • Baltimore 10 Manhattan West • Manhattan 1 Riverchase Galleria • Hoover (Birmingham) 1 Alderwood • Lynnwood (Seattle) 5 Towson Town Center • Towson (Baltimore) 11 Staten Island Mall • Staten Island 2 The Shoppes at Bel Air • Mobile (Fort Lauderdale) -

Events, Places and Things and Their Place in Lehi History

Events, Places and Things and their Place in Lehi History Abel John Evans Law Offices ● The Lehi Commercial and Savings Bank was the Law Offices of Abel John Evans in 1905. Adventureland Video ● Established in the Old Cooperative building at 197 East State in 1985. Alahambra Saloon ● This was a successful saloon ran by Ulysses S. Grant(not the President) for a few short years in the Hotel Lehi (Lehi Hotel) In 1891 through approximately 1895. ● The address was 394 West Main Street. American Fork Canyon Power Plant ● When the power plant was closed, one of the cabins was sold to Robert and Kathleen Lott in 1958 and it is their home today at 270 North 300 East American Fork Canyon Railroad ● Railroad that took men to the mines in American Fork Canyon ● Henry Thomas Davis helped build the railroad in American Fork Canyon American Savings and Loan Company ● Company founded by Lehi man John Franklin Bradshaw A.O.U.W. Lodge ● A.O.U.W. Lodge met in an upper room at the Lehi Commercial and Savings Bank in 1895. ● It stands for Ancient Order of United Workmen ● The AOUW was a breakoff of the Masons. Arley Edwards Barbershop ● Opened a barbershop in 195152 in the Steele Building at 60 West Main. Athenian Club ● The Athenian Club was organized on December 27, 1909 at the home of Emmerrette Smith. She was elected the first President ● Julia Child was elected vice President and Jane Ford was elected Secretary. ● There was a charter membership of 20 members ● The colors of the club were yellow and white ● They headed the drive for a Public Library. -

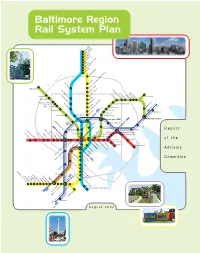

Baltimore Region Rail System Plan Report

Baltimore Region Rail System Plan Report of the Advisory Committee August 2002 Advisory Committee Imagine the possibilities. In September 2001, Maryland Department of Transportation Secretary John D. Porcari appointed 23 a system of fast, convenient and elected, civic, business, transit and community leaders from throughout the Baltimore region to reliable rail lines running throughout serve on The Baltimore Region Rail System Plan Advisory Committee. He asked them to recommend the region, connecting all of life's a Regional Rail System long-term plan and to identify priority projects to begin the Plan's implemen- important activities. tation. This report summarizes the Advisory Committee's work. Imagine being able to go just about everywhere you really need to go…on the train. 21 colleges, 18 hospitals, Co-Chairs 16 museums, 13 malls, 8 theatres, 8 parks, 2 stadiums, and one fabulous Inner Harbor. You name it, you can get there. Fast. Just imagine the possibilities of Red, Mr. John A. Agro, Jr. Ms. Anne S. Perkins Green, Blue, Yellow, Purple, and Orange – six lines, 109 Senior Vice President Former Member We can get there. Together. miles, 122 stations. One great transit system. EarthTech, Inc. Maryland House of Delegates Building a system of rail lines for the Baltimore region will be a challenge; no doubt about it. But look at Members Atlanta, Boston, and just down the parkway in Washington, D.C. They did it. So can we. Mr. Mark Behm The Honorable Mr. Joseph H. Necker, Jr., P.E. Vice President for Finance & Dean L. Johnson Vice President and Director of It won't happen overnight. -

A Legal-Empirical Study of the Unauthorized Use of Credit Cards

University of Miami Law Review Volume 21 Number 4 Article 5 7-1-1967 A Legal-empirical Study of the Unauthorized Use of Credit Cards Daniel E. Murray Follow this and additional works at: https://repository.law.miami.edu/umlr Recommended Citation Daniel E. Murray, A Legal-empirical Study of the Unauthorized Use of Credit Cards, 21 U. Miami L. Rev. 811 (1967) Available at: https://repository.law.miami.edu/umlr/vol21/iss4/5 This Leading Article is brought to you for free and open access by the Journals at University of Miami School of Law Institutional Repository. It has been accepted for inclusion in University of Miami Law Review by an authorized editor of University of Miami School of Law Institutional Repository. For more information, please contact [email protected]. A LEGAL-EMPIRICAL STUDY OF THE UNAUTHORIZED USE OF CREDIT CARDS DANIEL E. MURRAY* I. INTRODUCTION ........................................................... 811 II. THE CREDIT CARD IN THE COURTS .......................................... 814 A. The Two-Party Credit Arrangement .................................... 814 B. The Three-Party Credit Card Arrangement ............................. 817 III. EMPIRICAL INVESTIGATION ................................................. 824 A. Two-Party Credit Card Arrangements .................................. 825 1. THE DEPARTMENT STORE ............................................ 825 B. Three-Party Credit Card Arrangements ................................ 827 1. THE OIL COMPANIES ...............................................