The “Shell” Transport and Trading Company, P.L.C. About This Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Royal-Dutch-Shell-Fra-Oljemuseets-Årbok-2018.Pdf

Nor sk oljemuseum årbok 201 7 Årboken er Norsk Oljemuseums viktigste, årlige publikasjon. Den tar for seg et bredt spekter av aktuelle tema knyttet til petroleumsnæringen og museets virksomhet. Artiklene er skrevet både av museets egne ansatte og eksterne bidragsytere. Museets årsmelding og regnskap er også å finne i årboken. Norsk Oljemuseumoljemuseum Årbokårbok 20172018 Royal Dutch/Shell av Trude Meland hell har drevet sin verdensomspennende En gryende globalisering Svirksomhet i over 100 år og har bygget opp en Det hele startet i 1833 da Marcus Samuel sr. av verdens mest kjente merkevarer. Royal Dutch/ åpnet en liten forretning i Londons East End Shell som i dag er et multinasjonalt selskap med hvor han handlet med antikviteter, rariteter, hovedkontor i Haag og forretningsadresse i konkylier og dekorative skjell. Skjell og konkylier London, startet som en allianse i 1907. Da slo det var på moten i det viktorianske Storbritannia, og nederlandske Royal Dutch Petroleum Company forretningen var lukrativ.2 og britiske The «Shell» Transport and Trading Company seg sammen. Dette er historien om Den vokste til et blomstrende import- og hvordan Royal Dutch/Shell Group vokste seg eksportfirma, og Samuel organiserte en toveis til å bli et av verdens største foretak, men også handel mellom Storbritannia og det fjerne østen. om de to som startet det – den ene fra Londons Tekstiler og maskiner til å bygge opp en industri østkant, jødisk opprinnelse og ambisiøs. Den gikk fra Storbritannia, og i retur kom ris, kull, andre nederlender, med en hang for detaljer og silke, kobber og porselen. Antall handelspartnere tall. Mennene var Marcus Samuel jr. -

Due Diligence and Stronger Preventative Measures

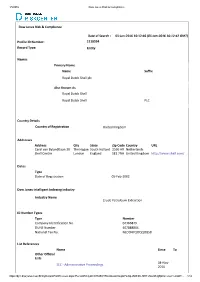

1/5/2016 Dow Jones Risk & Compliance Dow Jones Risk & Compliance Date of Search : 05‐Jan‐2016 16:12:46 (05‐Jan‐2016 16:12:42 GMT) Profile ID Number: 1118594 Record Type: Entity Names Primary Name Name Suffix Royal Dutch Shell plc Also Known As Royal Dutch Shell Royal Dutch Shell PLC Country Details Country of Registration United Kingdom Addresses Address City State Zip Code Country URL Carel van Bylandtlaan 30 The Hague South Holland 2596 HR Netherlands Shell Centre London England SE1 7NA United Kingdom http://www.shell.com/ Dates Type Date of Registration 05‐Feb‐2002 Dow Jones Intelligent Indexing Industry Industry Name Crude Petroleum Extraction ID Number Types Type Number Company Identification No. 04366849 DUNS Number 407888804 National Tax No. NLOO47QOQQOB58 List References Name Since To Other Official Lists 04‐Nov‐ SEC ‐ Administrative Proceedings 2010 https://djrc.dowjones.com/EntityDetailsPrintPreview.aspx?PersonEntityId=QTMSOYRLnQLwzr0sJpkYw3qLJMB3fUJ9Hf+Z6n/xBJgEpVx+Loo=%20&Pr… 1/12 1/5/2016 Dow Jones Risk & Compliance GAO (US) Report on Exporters of Refined Petroleum Products to Iran Sep‐2010 GAO (US) Report on firms to have Engaged in Commercial Activities in 23‐Mar‐ 03‐Aug‐ Iran’s Energy Sector 2010 2011 New Jersey Report to the Legislature regarding Investments in Iran ‐ 01‐Mar‐ 03‐Mar‐ Prohibited List 2012 2014 Close Associates/Related Entities Name Type Relation Raízen Combustiveis SA Entity Asset A/S Dansk Shell Entity Subsidiary CRI Catalyst Company Belgium NV Entity Subsidiary Equilon Enterprises Limited Liability Entity Subsidiary Company Nederlandse Aardolie Maatschappij BV Entity Subsidiary Pilipinas Shell Petroleum Corporation Entity Subsidiary Shell Australia Limited Entity Subsidiary Shell Bulgaria Single Person Joint Stock Entity Subsidiary Company Shell Canada Limited Entity Subsidiary Shell Compañía Argentina De Petróleo SA Entity Subsidiary Shell E&P Ireland Limited Entity Subsidiary Shell Eastern Petroleum (Private) Limited Entity Subsidiary Shell Energy North America (US) L.P. -

TANZANIA OIL and GAS ALMANAC TANZANIA OIL and GAS ALMANAC Print Edition June 2015

TANZANIA OIL AND GAS ALMANAC TANZANIA TANZANIA OIL AND GAS ALMANAC Print edition June 2015 A Reference Guide published by the Friedrich-Ebert-Stiftung Tanzania and OpenOil Tanzania Oil and Gas Almanac A Reference Guide published by the Friedrich-Ebert-Stiftung Tanzania and OpenOil EDITORIAL Abdallah Katunzi – Chief Editor Marius Siebert – Deputy Editor PUBLISHED BY Friedrich-Ebert-Stiftung P.O Box 4472 Mwai Kibaki Road Plot No. 397 Dar es Salaam, Tanzania Telephone: 255-22-2668575/2668786 Email: [email protected] PRINTED BY FGD Tanzania Ltd P.O. Box 40331 Dar es Salaam Disclaimer While all efforts have been made to ensure that the information contained in this book has been obtained from reliable sources, FES (Tanzania) bears no responsibility for oversights or omissions. ©Friedrich-Ebert-Stiftung, 2015 ISBN: 978-9987-483-36-5 A commercial resale of this publication is strictly prohibited unless the Friedrich-Ebert-Stiftung gives explicit and written approval beforehand. PREFACE With an estimated gas reserve of more than 55 trillion cubic feet (Tcf), Tanzania readies itself to join the gas economy. Large multinational oil companies are currently exploring natural gas and oil in various parts of Tanzania – both offshore and onshore. Despite these huge discoveries, there is little publicly available information on natural gas on a wide range of issues. Consequently, the Friedrich-Ebert-Stiftung (FES), Tanzania, with the technical support of OpenOil– a Berlin based organisation – created the Tanzania Oil and Gas Almanac as a living database for publicly available information around the country’s Oil and Gas sector. It has been created to significantly increase the stock of information available in local contexts among extractive stakeholders including civil society organizations, government, journalists and companies. -

Royal Dutch Shell 2007 Annual Review

Delivery and growth Royal Dutch Shell plc Annual Review and Summary Financial Statements 2007 Delivery and growth are the basis for our success. We aim to SELECTED FINANCIAL DATA deliver major new energy projects, top-quality operational e selected financial data set out below is derived, in part, from performance and competitive returns while investing in new the Consolidated Financial Statements. e selected data should developments to secure the growth of our business . be read in conjunction with the Summary Consolidated Financial Delivery is doing what we say. Growth is our future . Statements and related Notes, as well as the Summary Operating and Financial Review in this Review. With effect from 2007, wind and solar activities, which were previously reported withi n Other industry segments, are reported within the Gas & Power segment and Oil Sands activities, which were previously reported within the Exploration & Production segment, are reported as a separate segment. During 2007, the hydrogen and CO 2 coordination activities were moved from Other industry segments to the Oil Products segment and all other activities within Other industry segments are now reported within the Corporate segment. CONSOLIDATED STATEMENT OF INCOME DATA $ million 2007 2006 2005 Revenue 355,782 318,845 306,731 Income from continuing operations 31,926 26,311 26,568 Income/(loss) from discontinued operations ––(307) Income for the period 31,926 26,311 26,261 Income attributable to minority interest 595 869 950 Income attributable to shareholders of Royal Dutch -

2005 Annual Report on Form 20-F

United States Securities and Exchange Commission Washington, D.C. 20549 FORM 20-F Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 For the fiscal year ended December 31, 2005 Commission file number 1-32575 Royal Dutch Shell plc (Exact name of registrant as specified in its charter) England and Wales (Jurisdiction of incorporation or organisation) Carel van Bylandtlaan 30, 2596 HR, The Hague, The Netherlands tel. no: (011 31 70) 377 9111 (Address of principal executive offices) Securities Registered Pursuant to Section 12(b) of the Act Title of Each Class Name of Each Exchange on Which Registered American Depositary Receipts representing Class A ordinary shares of the New York Stock Exchange issuer of an aggregate nominal value €0.07 each American Depositary Receipts representing Class B ordinary shares of the New York Stock Exchange issuer of an aggregate nominal value of €0.07 each Securities Registered Pursuant to Section 12(g) of the Act None Securities For Which There is a Reporting Obligation Pursuant to Section 15(d) of the Act None Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report. Outstanding as of December 31, 2005: 3,817,240,213 Class A ordinary shares of the nominal value of €0.07 each. 2,707,858,347 Class B ordinary shares of the nominal value of €0.07 each. Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. -

Royal Dutch Shell - Wikipedia, the Free Encyclopedia Royal Dutch Shell from Wikipedia, the Free Encyclopedia

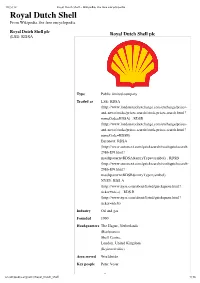

10/5/12 Royal Dutch Shell - Wikipedia, the free encyclopedia Royal Dutch Shell From Wikipedia, the free encyclopedia Royal Dutch Shell plc Royal Dutch Shell plc (LSE: RDSA Type Public limited company Traded as LSE: RDSA (http://www.londonstockexchange.com/exchange/prices- and-news/stocks/prices-search/stock-prices-search.html? nameCode=RDSA) , RDSB (http://www.londonstockexchange.com/exchange/prices- and-news/stocks/prices-search/stock-prices-search.html? nameCode=RDSB) Euronext: RDSA (http://www.euronext.com/quicksearch/resultquicksearch- 2986-EN.html? matchpattern=RDSA&entryType=symbol) , RDSB (http://www.euronext.com/quicksearch/resultquicksearch- 2986-EN.html? matchpattern=RDSB&entryType=symbol) NYSE: RDS.A (http://www.nyse.com/about/listed/quickquote.html? ticker=rds.a) , RDS.B (http://www.nyse.com/about/listed/quickquote.html? ticker=rds.b) Industry Oil and gas Founded 1900 Headquarters The Hague, Netherlands (Headquarters) Shell Centre, London, United Kingdom (Registered office) Area served Worldwide Key people Peter Voser (CEO) en.wikipedia.org/wiki/Royal_Dutch_Shell 1/16 10/5/12 Royal Dutch Shell - Wikipedia, the free encyclopedia (CEO) Jorma Ollila (Chairman) Products Petroleum, natural gas, and other petrochemicals Revenue US$ 470.171 billion (2011)[1] Operating US$ 55.660 billion (2011)[1] income Profit US$ 31.185 billion (2011)[1] Total assets US$ 345.257 billion (2011)[1] Total equity US$ 169.517 billion (2011)[1] Employees 90,000 (2011)[1] Subsidiaries List Website Shell.com (http://www.shell.com) (http://www.londonstockexchange.com/exchange/prices-and-news/stocks/prices-search/stock-prices- search.html?nameCode=RDSA) , RDSB (http://www.londonstockexchange.com/exchange/prices-and- news/stocks/prices-search/stock-prices-search.html?nameCode=RDSB) ), commonly known as Shell, is a Dutch–British multinational oil and gas company headquartered in The Hague, Netherlands and with its registered office in London, United Kingdom.[2] It is the world's second largest company by 2011 revenues and one of the six oil and gas "supermajors". -

Rapportering Og Revisjon Av Olje- Og Gassreserver

NORGES HANDELSHØYSKOLE Bergen, 18.06.2007 Rapportering og revisjon av olje- og gassreserver med utgangspunkt i Shell-skandalen 2004. Olav Søvik Olsen Veileder: Professor Aasmund Eilifsen Utredning i fordypningsområdet: Økonomisk styring NORGES HANDELSHØYSKOLE Denne utredningen er gjennomført som et ledd i masterstudiet i økonomisk-administrative fag ved Norges Handelshøyskole og godkjent som sådan. Godkjenningen innebærer ikke at høyskolen innestår for de metoder som er anvendt, de resultater som er fremkommet eller de konklusjoner som er trukket i arbeidet. Masteroppgave Rapportering og revisjon av olje- og gassreserver Sammendrag Denne utredningen starter med å presentere oljeselskapet Royal Dutch Shell og deretter tar den for seg Shell sin skandale i 2004 vedrørende rapportering av olje- og gassreserver. Det fokuseres her på hvordan toppledelsen til Shell håndterte situasjonen, samt hvilke rapporteringsregelverk som var gjeldende. Etter dette tar utredningen for seg hvordan rapporteringen av olje- og gassreserver foregår og hvilke rammeverk for rapportering som er det beste i dag. Det kommer frem av denne innsikten at rammeverket til Society of Petroleum Engineers (SPE) er et av de mest brukte og anerkjente i oljebransjen, og det gis eksempler på hvordan estimering av olje- og gassreserver foregår etter dette rammeverket. Til slutt i oppgaven presenteres det ulike moment som er viktige for en attestasjon/revisjon av et oljeselskaps olje- og gassreserver. Ved utarbeidelsen av disse momentene blir hovedsakelig ulike revisjonsstandarder, -

2008 Annual Report and Form 20-F for the Year Ended December 31, 2008 Contact Information

ROYAL DUTCH SHELL PLC ANNUAL REPORT AND FORM 20-F FOR THE YEAR ENDED DECEMBER 31, 2008 DELIVERY & GROWTH REPORT ANNUAL REPORT AND FORM 20-F FOR THE YEAR ENDED DECEMBER 31, 2008 OUR BUSINESS With around 102,000 employees in more than 100 countries and DOWNSTREAM territories, Shell helps to meet the world’s growing demand for Our Oil Sands business, the Athabasca Oil Sands Project, extracts energy in economically, environmentally and socially bitumen – an especially thick, heavy oil – from oil sands in responsible ways. Alberta, western Canada, and converts it to synthetic crude oils that can be turned into a range of products. UPSTREAM Our Exploration & Production business searches for and recovers Our Oil Products business makes, moves and sells a range of oil and natural gas around the world. Many of these activities petroleum-based products around the world for domestic, are carried out as joint venture partnerships, often with national industrial and transport use. Its Future Fuels and CO2 business oil companies. unit develops biofuels and hydrogen and markets the synthetic fuel and products made from the GTL process. It also leads Our Gas & Power business liquefies natural gas and transports company-wide activities in CO2 management. With around it to customers across the world. Its gas to liquids (GTL) process 45,000 service stations, ours is the world’s largest single-branded turns natural gas into cleaner-burning synthetic fuel and other fuel retail network. products. It develops wind power to generate electricity and is involved in solar power technology. It also licenses our coal Our Chemicals business produces petrochemicals for industrial gasification technology, enabling coal to be used as a chemical customers. -

Filed by Royal Dutch Shell Plc

Filed by Royal Dutch Shell plc This communication is filed pursuant to Rule 425 under The Securities Act of 1933, as amended, and deemed filed pursuant to Rule 14d-2 of the Securities Exchange Act of 1934, as amended. Subject Company: Royal Dutch Petroleum Company Commission File Number: 001-03788 Date: October 28, 2004 THE FOLLOWING IS AN EMPLOYEE FACT SHEET THAT WAS POSTED ON WWW.SHELL.COM ON OCTOBER 28, 2004. EMPLOYEE FACT SHEET Royal Dutch Shell Not for release to, or publication or distribution in, in whole or in part, into Canada or Japan. — One, single tier Board; One Non-Executive Chairman; One Chief Executive; One Headquarters — Simplified ownership and market profile — Delivers clarity, simplicity, efficiency and accountability — Rigorous evaluation process taking into account shareholders, stakeholders and employees — One Company; Many Strengths Simplified structure The Group’s two parent companies, Royal Dutch Petroleum Company (RD) and Shell Transport and Trading plc. (ST&T), will unify under one new parent company, Royal Dutch Shell plc. — One listed UK parent company for the Group, Royal Dutch Shell plc. — A single tier board chaired by a single Non Executive Chairman. Aad Jacobs, currently Chairman of the Supervisory Board of Royal Dutch will be the first non-executive Chairman. — A Chief Executive with full executive authority and empowered to drive strategy implementation, operational delivery and cultural change. Jeroen van der Veer, currently Chairman of the Committee of Managing Directors, assumes this role with immediate effect. — Board initially to comprise 5 Executive Directors and 10 Non Executive Directors (a reduction from the current combined 16 Non-Executives). -

Royal Dutch Petroleum Company the “Shell” Transport N.V

Royal Dutch Summ CVR 18/2/04 19:47 Page 1 Statement of General Business Principles Royal Dutch Petroleum Company The “Shell” Transport N.V. Koninklijke Nederlandsche Petroleum Maatschappij and Trading Company, p.l.c. Fundamental principles that govern how Annual Report and Accounts 2003 Royal Dutch Petroleum Company Annual Report and Accounts 2003 each Shell company conducts its affairs. Available at www.shell.com/sgbp Tell Shell N.V. Koninklijke Nederlandsche Petroleum Maatschappij Tell us what you think about Shell, our performance, our reports or the issues we face. Join the global debate – we The Shell Report 2003 Summary Annual Report and Accounts 2003 Meeting the energy challenge – our progress in contributing to sustainable development value your views. Visit www.shell.com/tellshell or e-mail us at [email protected] Annual Report and Accounts 2003 The Shell Report 2003 The Annual Reports and Accounts of Royal Dutch Meeting the energy challenge – our progress Contact any of the addresses below Petroleum Company and The “Shell” Transport in contributing to sustainable development. for copies of publications: and Trading Company, p.l.c. Available at www.shell.com/shellreport Shell International B.V. Available at www.shell.com/annualreport FSK Division, PO Box 162 2501 AN The Hague The Netherlands Tel: +31 (0)70 377 4540 Royal Dutch Petroleum Company The “Shell” Transport Fax: +31 (0)70 377 3115 N.V. Koninklijke Nederlandsche Petroleum Maatschappij and Trading Company, p.l.c. Summary Annual Report and Accounts 2003 Summary Annual -

Royal Dutch Petroleum Company N.V

Annual Report and Accounts 2004 Royal Dutch Petroleum Company N.V. Koninklijke Nederlandsche Petroleum Maatschappij About this report Welcome to the Annual Report and Accounts 2004 for Royal Dutch Petroleum Company. In this report you will find information relating to the Royal Dutch/Shell Group of Companies on pages 6 to 103, including a review of the 2004 operational and financial performance of the businesses. On pages 1 to 5 and 104 to 136, you will find information about Royal Dutch Petroleum Company, one of the Parent Companies of the Royal Dutch/Shell Group. Shell’s operations The Royal Dutch/Shell Group of Companies consists of the upstream businesses of Exploration & Production and Gas & Power and the downstream businesses of Oil Products and Chemicals. We also have interests in other industry segments such as Renewables and EXPLORATION Hydrogen. For more information & PRODUCTION 16GAS & POWER 22 on Shell’s operations, see pages 8 and 9 of this report. OIL PRODUCTS 26CHEMICALS 30 OTHER INDUSTRY SEGMENTS 32 ROYAL DUTCH 104 1 What’s in this report Report structure Royal Dutch Petroleum Company Royal Dutch Petroleum Company owns 60% of the Royal Dutch/Shell Group. Throughout this report, page markers 2 Message to shareholders are used to identify sections that relate to these entities: 4 Financial highlights Royal Dutch Petroleum Company 5 Unification of Royal Dutch and Shell Transport Royal Dutch/Shell Group Royal Dutch/Shell Group The companies in which Royal Dutch Petroleum Company and The “Shell” Transport and Trading Company, p.l.c. directly or indirectly own investments 6 The Boards of the Parent Companies are separate and distinct entities. -

28150.Pdf (644.7Kb)

Explaining the Human Rights Strategy of Transnational Corporations - A Social Constructivist Perspective Kristian Holst Department of Political Science UNIVERSITY OF OSLO Spring 2005 ii Explaining the Human Rights Strategy of TNCs iii Acknowledgements The road leading to the conclusion of this thesis has been full of twists and turns. Along the way, there have been a number of people who have been there to give me the necessary drive and back-up to reach my goal. Firstly, I would like to thank Jeffrey T. Checkel for lending a hand at a crucial stage of the process. I would also like to thank my fellow students who through the years have made the time at the University of Oslo a memorable one, and shared their insights on issues ranging from political science, to making Creme Brulée and the meaning of life. These include Jonas (member of the ‘glass cage think-tank’), Haakon, Christopher, Nils, Hallvard, Elisabeth, Erling, Ingunn, Hilde, the Bandy gang and all the rest of you. I would also like to thank Marit and Arne Holst for believing in me and for being there. This also goes for the rest of my family and friends who have wittingly or unwittingly been a part of this effort. Finally, I would like to thank Kristin – for your encouragement and understanding, endless patience and invaluable support. Oslo, June 2005 Kristian Holst iv Explaining the Human Rights Strategy of TNCs Acronyms AGM Annual General Meeting (Shell) AIUK Amnesty International United Kingdom ATCA Alien Tort Claims Act CMD Committee of Managing Directors (Shell) ECCR Ecumenical