The Fundamentals of EDA for the Financial Community 2013

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

GS40 0.11-Μm CMOS Standard Cell/Gate Array

GS40 0.11-µm CMOS Standard Cell/Gate Array Version 1.0 January 29, 2001 Copyright Texas Instruments Incorporated, 2001 The information and/or drawings set forth in this document and all rights in and to inventions disclosed herein and patents which might be granted thereon disclosing or employing the materials, methods, techniques, or apparatus described herein are the exclusive property of Texas Instruments. No disclosure of information or drawings shall be made to any other person or organization without the prior consent of Texas Instruments. IMPORTANT NOTICE Texas Instruments and its subsidiaries (TI) reserve the right to make changes to their products or to discontinue any product or service without notice, and advise customers to obtain the latest version of relevant information to verify, before placing orders, that information being relied on is current and complete. All products are sold subject to the terms and conditions of sale supplied at the time of order acknowledgement, including those pertaining to warranty, patent infringement, and limitation of liability. TI warrants performance of its semiconductor products to the specifications applicable at the time of sale in accordance with TI’s standard warranty. Testing and other quality control techniques are utilized to the extent TI deems necessary to support this war- ranty. Specific testing of all parameters of each device is not necessarily performed, except those mandated by government requirements. Certain applications using semiconductor products may involve potential risks of death, personal injury, or severe property or environmental damage (“Critical Applications”). TI SEMICONDUCTOR PRODUCTS ARE NOT DESIGNED, AUTHORIZED, OR WAR- RANTED TO BE SUITABLE FOR USE IN LIFE-SUPPORT DEVICES OR SYSTEMS OR OTHER CRITICAL APPLICATIONS. -

High-Level Synthesis Tools for Xilinx Fpgas

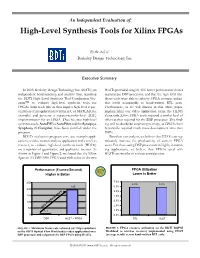

An Independent Evaluation of: High-Level Synthesis Tools for Xilinx FPGAs By the staff of Berkeley Design Technology, Inc. Executive Summary In 2009, Berkeley Design Technology Inc. (BDTI), an HLSTs provided roughly 40X better performance than a independent benchmarking and analysis firm, launched mainstream DSP processor, and that the high-level syn- the BDTI High-Level Synthesis Tool Certification Pro- thesis tools were able to achieve FPGA resource utiliza- gram™ to evaluate high-level synthesis tools for tion levels comparable to hand-written RTL code. FPGAs. Such tools take as their input a high-level repre- Furthermore, as we will discuss in this white paper, sentation of an application (written in C or MATLAB, for implementing our video application using the HLSTs example) and generate a register-transfer-level (RTL) along with Xilinx FPGA tools required a similar level of implementation for an FPGA. Thus far, two high-level effort as that required for the DSP processor. This find- synthesis tools, AutoESL’s AutoPilot and the Synopsys ing will no doubt be surprising to many, as FPGAs have Synphony C Compiler, have been certified under the historically required much more development time than program. DSPs. BDTI’s evaluation program uses two example appli- Based on our analysis, we believe that HLSTs can sig- cations, a video motion analysis application and a wireless nificantly increase the productivity of current FPGA receiver, to evaluate high-level synthesis tools (HLSTs) users. For those using DSP processors in highly demand- on a number of quantitative and qualitative metrics. As ing applications, we believe that FPGAs used with shown in Figure 1 and Figure 2, we found that the Xilinx HLSTs are worthy of serious consideration. -

Introduction to Intel® FPGA IP Cores

Introduction to Intel® FPGA IP Cores Updated for Intel® Quartus® Prime Design Suite: 20.3 Subscribe UG-01056 | 2020.11.09 Send Feedback Latest document on the web: PDF | HTML Contents Contents 1. Introduction to Intel® FPGA IP Cores..............................................................................3 1.1. IP Catalog and Parameter Editor.............................................................................. 4 1.1.1. The Parameter Editor................................................................................. 5 1.2. Installing and Licensing Intel FPGA IP Cores.............................................................. 5 1.2.1. Intel FPGA IP Evaluation Mode.....................................................................6 1.2.2. Checking the IP License Status.................................................................... 8 1.2.3. Intel FPGA IP Versioning............................................................................. 9 1.2.4. Adding IP to IP Catalog...............................................................................9 1.3. Best Practices for Intel FPGA IP..............................................................................10 1.4. IP General Settings.............................................................................................. 11 1.5. Generating IP Cores (Intel Quartus Prime Pro Edition)...............................................12 1.5.1. IP Core Generation Output (Intel Quartus Prime Pro Edition)..........................13 1.5.2. Scripting IP Core Generation.................................................................... -

NOTICE of ANNUAL MEETING of STOCKHOLDERS April 23, 2001 ______

NOTICE OF ANNUAL MEETING OF STOCKHOLDERS April 23, 2001 ________________ To the Stockholders of Synopsys, Inc.: NOTICE IS HEREBY GIVEN that the Annual Meeting of Stockholders of Synopsys, Inc., a Delaware corporation (the “Company”), will be held on Monday, April 23, 2001, at 4:00 p.m., local time, at the Company’s principal executive offices at 700 East Middlefield Road, Mountain View, California 94043, for the following purposes: 1. To elect eight directors to serve for the ensuing year or until their successors are elected. 2. To approve an amendment to the Company’s Employee Stock Purchase Plan and International Employee Stock Purchase Plan to increase the number of shares of Common Stock reserved for issuance thereunder by 1,200,000 shares. 3. To approve an amendment to the 1992 Stock Option Plan to extend the term of the Plan from January 2002 to January 2007. 4. To ratify the appointment of KPMG LLP as independent auditors of the Company for fiscal year 2001. 5. To transact such other business as may properly come before the meeting or any adjournment or adjournments thereof. The foregoing items of business are more fully described in the Proxy Statement accompanying this Notice. Only stockholders of record at the close of business on February 26, 2001 are entitled to notice of and to vote at the meeting. All stockholders are cordially invited to attend the meeting in person. However, to assure your representation at the meeting, you are urged to sign and return the enclosed proxy (the “Proxy”) as promptly as possible in the envelope enclosed. -

IEEE 802.3Da SPMD TF Meeting May 19, 2021 Prepared by Peter Jones

IEEE 802.3da SPMD TF meeting May 19, 2021 Prepared by Peter Jones Presentations posted at: https://www.ieee802.org/3/da/index.html Agenda/Admin - Chad Jones All times in Pacific Time (PT) 7:01am: The Chair reviewed the agenda in https://www.ieee802.org/3/da/public/051921/8023da_agenda_051921.pdf. The Chair asked if there were any corrections or additions to the agenda. There being no corrections or additions, the agenda stands approved. The Chair asked if anyone hasn’t had a chance to review the minutes for April 21, 2021. None responded. The Chair asked if there were any change to be made to the April 21, 2021 minutes. None responded. The April 21, 2021 minutes were approved by unanimous consent. 7:09am: Call for patents was made, no one responded. 7:14am: opening agenda slides complete. The meeting moves on to presentations. Presentations/Discussion. 7:14am: LTspice Model Validation Chris DiMinico, MC Communications/PHY-SI LLC/SenTekse/Panduit Bob Voss, Panduit Paul Wachtel, Panduit 7:21am: presentation done, start of Q&A. 7:30am: Q&A done. 7:30am: Startup sequence Michael Paul, ADI 8.05am: presentation & Q&A done. 8:05am: Editors comments George Zimmerman, CME Consulting/various 8:28am: Closing remarks Next meeting: May 26, 2021 , 7:00am PT. Meeting closed – 8:31am PT Attendees (from Webex + emails) Name Employer Affiliation Attended 05/19 Alessandro Ingrassia Canova Tech Canova Tech y Anthony New Prysmian Group Prysmian Group y Bernd Horrmeyer Phoenix Contact Phoenix Contact y Bob Voss Panduit Corp. Panduit Corp. y Brian Murray Analog Devices Inc. -

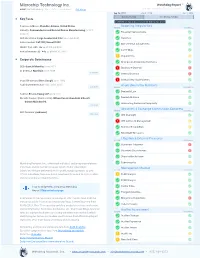

Microchip Technology Inc

Microchip Technology Inc. Watchdog Report ™ MCHP (NASDAQ Global) | CIK:827054 | United States | SEC llings The new model for duciary analysis Sep 24, 2021 Jan 1, 2020 Jan 1, 2016 RECENT PERIOD HISTORICAL PERIOD Key Facts 10-Q led on Aug 3, 2021 for period ending Jun 2021 Business address: Chandler, Arizona, United States Reporting Irregularities RECENT HISTORICAL Industry: Semiconductor and Related Device Manufacturing (NAICS Financial Restatements 334413) SEC ler status: Large Accelerated Filer as of Jun 2021 Revisions Index member: S&P 500, Russell 1000 Out of Period Adjustments Market Cap: $45.3b as of Sep 24, 2021 Late Filings Annual revenue: $5.44b as of Mar 31, 2021 Impairments Corporate Governance Changes in Accounting Estimates CEO: Ganesh Moorthy since 2021 Disclosure Controls CFO: Eric J. Bjornholt since 2009 1st level Internal Controls Board Chairman: Steve Sanghi since 1993 Critical / Key Audit Matters Audit Committee Chair: NOT AVAILABLE Anomalies in the Numbers 2nd level RECENT HISTORICAL Benford's Law Auditor: Ernst & Young LLP since 2001 Outside Counsel (most recent): Wilson Sonsini Goodrich & Rosati Beneish M-Score Osborn Maledon PA Accounting Disclosure Complexity 3rd level Securities & Exchange Commission Concerns RECENT HISTORICAL SEC Reviewer: (unknown) 4th level SEC Oversight SEC Letters to Management Revenue Recognition Non-GAAP Measures Litigation & External Pressures RECENT HISTORICAL Signicant Litigation Securities Class Actions Shareholder Activism Watchdog Research, Inc., offers both individual and group subscriptions, Cybersecurity data feeds and/or custom company reports to our subscribers. Management Review Subscribe: We have delivered 300,000 public company reports to over RECENT HISTORICAL 27,000 individuals, from over 9,000 investment rms and to 4,000+ public CEO Changes company corporate board members. -

Xilinx XAPP107: Synopsys/Xilinx High Density Design Methodology Using

Product Obsolete/Under Obsolescence Application Note 3 0 Synopsys/Xilinx High Density Design Methodology Using FPGA Compiler™ XAPP107 August 6, 1998 (Version 1.0) 03*Written by: Bernardo Elayda & Ramine Roane Summary This paper describes design practices to synthesize high density designs (i.e. over 100k gates), composed of large functional blocks, for today’s larger Xilinx FPGA devices using the Synopsys FPGA Compiler. The Synopsys FPGA Compiler version 1998.02, Alliance Series 1.5, and the XC4000X family were used in preparing the material for this application note. Introduction designs preserving some levels of hierarchy will lead to better placement routing results and shorter compile times. For smaller designs, optimal quality of results can often be achieved by ungrouping hierarchical boundaries (compile The designer must determine which trade-offs to make to -ungroup_all). For high density designs, designers tra- meet his design goals and timing requirements. ditionally partition their circuits into small 5-10k gate mod- High density designs require greater selectivity on which ules. With todays version of FPGA Compiler (1998.02) and hierarchical boundaries to eliminate for synthesis. Flatten- currently available workstation hardware it is no longer nec- ing a 150k gate design can lead to long compile times, and essary to partition a design into small 5K to 10K blocks for compromise results. The following guidelines will help in efficient synthesis. In fact, artificial partitioning the design choosing which blocks to flatten in a large design: can worsen optimization results by breaking paths into sep- 1. Eliminating boundaries between combinatorial blocks arate partitions and preventing FPGA Compiler from being allows the synthesis tool to optimize glue logic across able to optimize the entire path. -

1 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26

Case 5:19-cv-02082-LHK Document 48 Filed 06/26/19 Page 1 of 9 1 2 3 4 5 6 7 8 UNITED STATES DISTRICT COURT 9 NORTHERN DISTRICT OF CALIFORNIA 10 SAN JOSE DIVISION 11 12 SYNOPSYS, INC., Case No. 19-CV-02082-LHK 13 Plaintiff, ORDER GRANTING PRELIMINARY INJUNCTION 14 v. 15 INNOGRIT, CORP., 16 Defendant. 17 United States District Court District United States Northern District of California District Northern 18 On April 23, 2019, the Court denied Plaintiff’s ex parte application for a temporary 19 restraining order. ECF No. 16 at 6. However, the Court also ordered Defendant to show cause why 20 a preliminary injunction should not issue. Id. The Court permitted the parties to brief whether a 21 preliminary injunction is appropriate here. Before the Court is the question of whether to impose a 22 preliminary injunction in the instant case. Having considered the parties’ submissions, the relevant 23 law, and the record in this case, the Court GRANTS a preliminary injunction. 24 I. BACKGROUND 25 Factual Background 26 Plaintiff is a provider of electronic design automation (“EDA”). ECF No. 39 (first 27 amended complaint, or “FAC”) at ¶ 8. EDA refers to “using computers to design, verify, and 28 1 Case No. 19-CV-02082-LHK ORDER GRANTING PRELIMINARY INJUNCTION Case 5:19-cv-02082-LHK Document 48 Filed 06/26/19 Page 2 of 9 1 simulate the performance of electronic circuits.” Id. Plaintiff has invested substantial sums of 2 money in designing EDA software, and offers a variety of software applications to purchasers. -

GS30 Product Overview

GS30 0.15-µm CMOS Standard Cell/Gate Array Version 1.0 February, 2001 Copyright Texas Instruments Incorporated, 2001 The information and/or drawings set forth in this document and all rights in and to inventions disclosed herein and patents which might be granted thereon disclosing or employing the materials, methods, techniques, or apparatus described herein are the exclusive property of Texas Instruments. No disclosure of information or drawings shall be made to any other person or organization without the prior consent of Texas Instruments. IMPORTANT NOTICE Texas Instruments and its subsidiaries (TI) reserve the right to make changes to their products or to discontinue any product or service without notice, and advise customers to obtain the latest version of relevant information to verify, before placing orders, that information being relied on is current and complete. All products are sold subject to the terms and conditions of sale supplied at the time of order acknowledgement, including those pertaining to warranty, patent infringement, and limitation of liability. TI warrants performance of its semiconductor products to the specifications applicable at the time of sale in accordance with TI’s standard warranty. Testing and other quality control techniques are utilized to the extent TI deems necessary to support this war- ranty. Specific testing of all parameters of each device is not necessarily performed, except those mandated by government requirements. Certain applications using semiconductor products may involve potential risks of death, personal injury, or severe property or environmental damage (“Critical Applications”). TI SEMICONDUCTOR PRODUCTS ARE NOT DESIGNED, AUTHORIZED, OR WAR- RANTED TO BE SUITABLE FOR USE IN LIFE-SUPPORT DEVICES OR SYSTEMS OR OTHER CRITICAL APPLICATIONS. -

Gpu-Accelerated Applications

GPU-ACCELERATED APPLICATIONS Test Drive the World’s Fastest Accelerator – Free! Take the GPU Test Drive, a free and easy way to experience accelerated computing on GPUs. You can run your own application or try one of the preloaded ones, all running on a remote cluster. Try it today. www.nvidia.com/gputestdrive GPU-ACCELERATED APPLICATIONS Accelerated computing has revolutionized a broad range of industries with over five hundred applications optimized for GPUs to help you accelerate your work. CONTENTS 1 Computational Finance 2 Climate, Weather and Ocean Modeling 2 Data Science and Analytics 4 Deep Learning and Machine Learning 7 Federal, Defense and Intelligence 8 Manufacturing/AEC: CAD and CAE COMPUTATIONAL FLUID DYNAMICS COMPUTATIONAL STRUCTURAL MECHANICS DESIGN AND VISUALIZATION ELECTRONIC DESIGN AUTOMATION 15 Media and Entertainment ANIMATION, MODELING AND RENDERING COLOR CORRECTION AND GRAIN MANAGEMENT COMPOSITING, FINISHING AND EFFECTS EDITING ENCODING AND DIGITAL DISTRIBUTION ON-AIR GRAPHICS ON-SET, REVIEW AND STEREO TOOLS WEATHER GRAPHICS 22 Medical Imaging 22 Oil and Gas 23 Research: Higher Education and Supercomputing COMPUTATIONAL CHEMISTRY AND BIOLOGY NUMERICAL ANALYTICS PHYSICS SCIENTIFIC VISUALIZATION 33 Safety & Security 35 Tools and Management Computational Finance APPLICATION NAME COMPANY/DEVELOPER PRODUCT DESCRIPTION SUPPORTED FEATURES GPU SCALING Accelerated Elsen Secure, accessible, and accelerated back- * Web-like API with Native bindings for Multi-GPU Computing Engine testing, scenario analysis, risk analytics Python, R, Scala, C Single Node and real-time trading designed for easy * Custom models and data streams are integration and rapid development. easy to add Adaptiv Analytics SunGard A flexible and extensible engine for fast * Existing models code in C# supported Multi-GPU calculations of a wide variety of pricing transparently, with minimal code Single Node and risk measures on a broad range of changes asset classes and derivatives. -

Libero Soc Design Flow User Guide

SmartFusion®2, IGLOO®2, RTG4™ Libero® SoC Design Flow User Guide Introduction Microchip Libero System-on-Chip (SoC) design suite offers high productivity with its comprehensive, easy to learn, easy to adopt development tools for designing with Microchip’s power efficient flash FPGAs, SoC FPGAs, and Rad- Tolerant FPGAs. To access datasheets and silicon user guides, visit www.microsemi.com, select the relevant product family and click the Documentation tab. Tutorials, Application Notes, Development Kits & Boards are listed in the Design Resources tab. Click the following links for additional information: • Libero SoC– Learn more about Libero SoC including Release Notes, a complete list of devices/packages, and timing and power versions supported in this release. • Programming – Learn more about Programming Solutions. • Power Calculators – Find XLS-based estimators for device families. • Licensing – Learn more about Libero licensing. © 2020 Microchip Technology Inc. User Guide DS00003765A-page 1 SmartFusion®2, IGLOO®2, RTG4™ Table of Contents Introduction.....................................................................................................................................................1 1. Libero SoC v12.6 Overview.................................................................................................................... 6 1.1. Welcome to Microchip Libero SoC v12.6..................................................................................... 6 1.2. Libero SoC Design Flow - SmartFusion2, IGLOO2, and RTG4................................................ -

EDA Software Support

EDA Software Support ® January 1998, ver. 7 Introduction Seamless design flow and high-quality integration of third party EDA tools are essential to the continued success of programmable logic devices (PLDs). Thus, Altera has established the Altera Commitment to Cooperative Engineering Solutions (ACCESSSM) program. Through the ACCESS program, Altera and key EDA vendors jointly develop and market next-generation high-level design tools and methodologies. Altera provides EDA partners with critical technical information and assistance, and ACCESS partners dedicate resources to ensure the best quality design results for Altera architectures. The ACCESS program provides a total solution that allows designers to generate and verify multiple design revisions in a single day, greatly reducing the product development cycle. Altera has been a leader in support of industry standards, such as EDIF, VHDL, Verilog HDL, VITAL, and the library of parameterized modules (LPM). Altera has also made a commitment to support current ACCESS partner design flows. f For more information on software support provided by Altera, see the MAX+PLUS II Programmable Logic Development System & Software Data Sheet in this data book. This document identifies the type of product(s) available from each ACCESS partner, i.e., design entry, compilation/synthesis, and simulation/verification. These products either support Altera devices directly or provide an interface to the MAX+PLUS II development software. In addition, the MAX+PLUS® II software contains the necessary interfaces and libraries to support many EDA tools. Altera recommends contacting EDA software manufacturers directly for details on product features, specific device support, and product availability. Table 1 lists third-party tool support for Altera devices.