Presentazione Standard Di Powerpoint

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Maranello World Spiel Maranello Mit Das Magazin Fürferraristi Gelungenes Facelift Portofino M

AUSGABE 4-2020 # 119 WORLD MARANELLO WORLD DAS MAGAZIN FÜR FERRARISTI MARANELLO MARANELLO MIT GROSSEM WEIHNACHTS GEWINN SPIEL Deutschland € 9,80 · Österreich € 11,50 · Schweiz CHF 15,70 · Luxemburg/Belgien € 11,80 · Italien 12,80 Deutschland € 9,80 · Österreich 11,50 Schweiz CHF 15,70 Luxemburg/Belgien FERRARI ROMA PORTOFINO M FORMEL 1 EVENTS 2020 ERSTE FAHREINDRÜCKE GELUNGENES FACELIFT 1000 GRANDS PRIX HISTORIC RACING MaranelloWorld4-20EberleinZW.indd 1 12.10.20 12:41 EDITORIAL Liebe Ferraristi, mit einem lachenden und einem weinenden Auge wird Sebastian Vettel am Ende der Saison die Scuderia Ferrari verlassen und ein neues Kapitel in seiner Motorsport-Biografie aufschlagen. 2015 war er zu Ferrari gekommen, als vierfacher Weltmeister im Red Bull Racing Team. Die Fußstapfen, in die er trat, waren dennoch riesig, denn Michael Schumacher hatte immerhin fünf Weltmeis- tertitel für die Roten geholt, Doch die Epoche Schumi lag zehn Jah- re zurück, und außerdem galten seit Einführung der 1,6-Liter-Tur- bomotoren mit zusätzlichem Elektroantrieb völlig andere Regeln. Ferrari war bei der technischen Entwicklung ganz vorne dabei und genoss einen klaren Favoritenstatus. Mit seinem ersten Sieg im zweiten Rennen für die Scuderia schürte Sebastian Vettel große Hoffnungen, doch mehr als zwei Vize-Weltmeistertitel hinter Le- wis Hamilton im überragenden Mercedes (2017 und 2018) waren für den Heppenheimer in den sechs Jahren nicht drin. In der vor- letzten Saison verschlechterte sich die Bilanz der Scuderia zuse- hends, und doch kam die Meldung von seinem Rücktritt Mitte Mai 2020 einigermaßen überraschend. Sebastian verhält sich wie ein englischer Gentleman, der mit steifer Oberlippe die letzten Grands Prix der Corona-Saison 2020 mit Anstand über die Bühne bringt und sich trotz offensichtlicher Defizite von Team und Arbeitsge- rät mit Kritik vornehm zurückhält. -

THE FERRARI WORLD TOURISM EXPERIENCE in ABU DHABI Esekong Andrew-Essien, Ph.D Depart

International Journal of Humanitatis Theoreticus. Vol. 3. (Issue: 1); May, 2020 ARTS & TECHNOLOGY IN THE MARKETING MIX: THE FERRARI WORLD TOURISM EXPERIENCE IN ABU DHABI Esekong Andrew-Essien, Ph.D Department of Theatre, Film & Carnival Studies University of Calabar, Calabar, Nigeria Abstract The functions of arts have long grown beyond the realm of aesthetics to diversified utilitarian roles. In some parts, this evolution was fast-tracked and has been sustained by technology, which is often engaged to simplify processes of production and to enhance value and access to artistic products. In this paper, the art and technology binary are evaluated in the context of marketing of products to tourists at Ferrari World, a popular tourist attraction in Abu Dhabi, United Arab Emirates. To theorize the use of art and technology in tourism marketing, the paper uses Butler’s Tourism Area Life Cycle Theory, which illustrates the stages of development of tourism products, and from the domain of Marketing, the paper uses Michael Porter’s Five Forces Model to evaluate the intensity of competition, profitability and attractiveness of products and ideas. Case studies are drawn from the architectural layout, products on display, service schedule and the performances at Ferrari World. Analysis is done towards finding the exact points of connection between the arts and other elements of the marketing mix; the subsisting strength and weaknesses of the Ferrari World concept, the impact on patronage, and the sustainability of the art and technology marketing plan. Key Words: Arts, Technology, Marketing Mix & Tourism. Introduction Quite often, the ultimate aim of production, whether of goods, services or ideas is to make profit, which could be monetary or otherwise. -

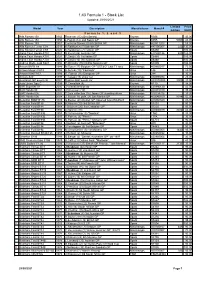

Stock List Updated 28/09/2021

1:43 Formula 1 - Stock List Updated 28/09/2021 Limited Price Model Year Description Manufacturer Manuf # Edition (AUD) F o r m u l a 1 , 2 a n d 3 Alfa Romeo 158 1950 Race car (25) (Oro Series) Brumm R036 35.00 Alfa Romeo 158 1950 L.Fagioli (12) 2nd Swiss GP Brumm S055 5000 40.00 Alfa Romeo 159 1951 Consalvo Sanesi (3) 6th British GP Minichamps 400511203 55.00 Alfa Romeo Ferrari C38 2019 K.Raikkonen (7) Bahrain GP Minichamps 447190007 222 135.00 Alfa Romeo Ferrari C39 2020 K.Raikkonen (7) Turkish GP Spark S6492 100.00 Alpha Tauri Honda AT01 2020 D.Kvyat (26) Austrian GP Minichamps 417200126 400 125.00 Alpha Tauri Honda AT01 2020 P.Gasly (10) 1st Italian GP Spark S6480 105.00 Alpha Tauri Honda AT01 2020 P.Gasly (10) 7th Austrian GP Spark S6468 100.00 Andrea Moda Judd S921 1992 P.McCathy (35) DNPQ Monaco GP Spark S3899 100.00 Arrows BMW A8 1986 M.Surer (17) Belgium GP "USF&G" Last F1 race Minichamps 400860017 75.00 Arrows Mugen FA13 1992 A.Suzuki (10) "Footwork" Onyx 146 25.00 Arrows Hart FA17 1996 R. Rosset (16) European GP Onyx 284 30.00 Arrows A20 1999 T.Takagi (15) show car Minichamps 430990084 25.00 Australian GP Event car 2001 Qantas AGP Event car Minichamps AC4010300 3000 40.00 Auto Union Tipo C 1936 R.Gemellate (6) Brumm R110 38.00 BAR Supertec 01 2000 J.Villeneuve test car Minichamps 430990120 40.00 BAR Honda 03 2001 J.Villeneuve (10) Minichamps 400010010 35.00 BAR Honda 005 2003 T.Sato collection (16) Japan GP standing driver Minichamps 518034316 35.00 BAR Honda 006 2004 J. -

Formula Uno Auto Collection 2015 Periodicita': Settimanale

FORMULA UNO AUTO COLLECTION 2015 PERIODICITA': SETTIMANALE PREZZO 1A USCITA€ 3,99 PREZZO 2A USCITA € 8,99 PREZZO USCITE SUCCESSIVE € 12,99 NUMERO USCITE PREVISTE: 200* *L’Editore si riserva la facoltà di variare il numero delle uscite periodiche complessive, nonché di modificare l’ordine e la sequenza delle singole uscite, comunicando con adeguato anticipo gli eventuali cambiamenti che saranno apportati al piano dell’opera. N° USCITA DATA EDICOLA Pilota Vettura 1 30/03/15 AYRTON SENNA McLAREN MP 4/4 - 1989 2 17/04/15 NIKI LAUDA FERRARI 312 T2 -1977 3 04/05/15 FERNANDO ALONSO RENAULT R25 -2005 4 18/05/15 LEWIS HAMILTON McLAREN MP 4/23 - 2008 5 01/06/15 EMERSON FITTIPALDI LOTUS 72 D - 1972 6 15/06/15 MICHAEL SCHUMACHER FERRARI F2001 - 2001 7 29/06/15 NELSON PIQUET BRABHAM BT 49 - 1981 8 13/07/15 ALAIN PROST WILLIAMS FW 15 C - 1993 9 27/07/15 AYRTON SENNA TOLEMAN TG 184 -1984 10 10/08/15 CARLOS PACE BRABHAM BT 44 B -1975 11 27/08/15 MICHAEL SCHUMACHER JORDAN 191 -1991 12 10/09/15 NIGEL MANSELL WILLIAMS FW 14B -1992 13 24/09/15 LEWIS HAMILTON MERCEDES F1 W05 - 2014 14 15/10/15 JENSON BUTTON BRAWN GP 01 -2009 15 29/10/15 SEBASTIAN VETTEL RED BULL RB9 - 2013 16 12/11/15 CLAY REGAZZONI FERRARI 312 B3 - 1975 17 26/11/15 MICHAEL SCHUMACHER BENETTON B 194 -1994 18 10/12/15 MICHAEL SCHUMACHER FERRARI F2002 -2002 19 24/12/15 VITTORIO BRAMBILLA MARCH 751 -1975 20 07/01/16 AYRTON SENNA McLAREN MP 4/8 -1993 21 21/01/16 SEBASTIAN VETTEL TORO ROSSO STR 3 -2008 22 04/02/16 JACKIE STEWART TYRRELL 006 - 1973 23 18/02/16 KIMI RAIKKONEN FERRARI F2007 -2007 -

The Motor Valley

Modena Bologna THE MOTOR VALLEY DAY 1 the “Red Cars”: here in 1943 the most prestigious car in- BOLOGNA dustry in the world was founded. Ferrari, a symbol of high Arrival in Bologna and meet with English speaking assistant. technology and passion for car speed, innovation and tech- Transfer to your hotel and check-in. Dinner and overnight. nical know-how. Stop and visit Museo Ferrari. Completely DAY 2 renovated and now with more exhibition space, it antici- DUCATI - LAMBORGHINI pates the museum of the future: not just a collection of Hotel breakfast. Morning departure to Borgo Panigale (a di- the past, but an extraordinary experience of the world of strict of Bologna) for the visit at the Museum and Fabric of Ferrari, where the historical cars and history are the pretext Ducati Motors to learn more about the 90 years story of the to understand and get to know today’s models, Formula 1 company, word famous for it’s style, performance and rese- content and technology and the outlook towards the future. arch of perfection. You will have the possibility to visit the This experience is offered via the cars, big screens and films, fabric and see how a Ducati cycle “born” but also to know interactive tools such as the explanation of the Grand Prix the fabric life of people working there. Lunch on your own. pit wall and the possibility to turn into a Formula 1 driver In the afternoon a similar experience you will live, visiting on board of a semi-professional simulator (for payment). -

Product Information

Product Information May 2019 Product Information Product Marketing and Communication No. 02/2019 Maranello, May 2019 Dear All, This Information Document describes the main characteristics of the Ferrari SF90 STRADALE in terms of target clients, performance and technological content. Best regards, Cordiali saluti, Matteo Turconi All Personalization & Atelier Communications are available on the MODISCS portal May 2019 Product Information Pag PRODUCT CONCEPT AND CLIENT PROFILE 4 MAIN INNOVATIONS AND PERFORMANCE 11 POWERTRAIN 13 VEHICLE DYNAMICS 22 AERODYNAMICS 29 STYLE 39 ASSETTO FIORANO 48 MAIN OPTIONALS AND ILLUSTRATIONS 51 7 YEARS MAINTENANCE 59 TECHNICAL SPECIFICATIONS 61 Index All Personalization & Atelier Communications are available on the MODISCS portal May 2019 Product concept and client profile 4 All Personalization & Atelier Communications are available on the MODISCS portal May 2019 PRODUCT & CLIENT INNOVATIONS POWERTRAIN VEHICLE DYNAMICS AEREODYNAMICS STYLE ASSETTO FIORANO PRODUCT CONCEPT “The best Ferrari ever built is the next one” is a phrase that sums up Enzo Ferrari’s philosophy in a nutshell. That same philosophy continues to drive every Ferrari technician as they tackle the design of each new car, be it a Formula 1 or a road-going model. The pressure to constantly achieve the impossible gave us with the courage to venture down a previously-unexplored avenue and open an important new chapter in the Prancing Horse’s glorious history: the era of the series production Ferrari hybrid. This paradigm shift is being ushered in by the SF90 STRADALE, a car so extreme it is an authentic production supercar in its own right, a whole new benchmark in terms of its performance and innovative content not just with regard to the Ferrari range, but also its competitors. -

ALFA OCCIDENTALE Issue 42, November 2020

ALFA OCCIDENTALE Issue 42, November 2020 At the “Bend Classic” on 5-6 September 2020, three 105-series Alfas were seen competing in the Classic Production class. Shown in the top photo is Kerry Gascoigne’s 1969 GTV 1750, while some hot competition between Sean Rowland’s 1969/70 Giulia GTV and Ron Guppy’s 1972 GTV 2000 is seen in the lower photo. The Bend had scheduled a locals-only race meeting, but on Fathers’ Day weekend, while social distancing and state border restrictions still remained in South Australia due to Covid-19. That might seem a recipe destined for limited success, but car racing had been on hold for six months at SA’s ‘The Bend Motorsport Park’. Over seventy entries signed up in six categories for two days of timed sprints on the new 3.41km West Circuit, while the public took full advantage of free spectator admission. (Photos from an article appearing in www.VeloceToday.com on 22nd September 2020) Alfa Occidentale is the electronic magazine of the 1 Alfa Romeo Owners Club of Australia (Western Australian Division) ALFA OCCIDENTALE Issue 42, November 2020 This is the 42nd edition of ALFA OCCIDENTALE – the electronic magazine of the Alfa Romeo Owners Club of Australia (Western Australian Division). It includes the latest updates to the WA Alfa Club’s upcoming program for 4th quarter 2020. CONTENTS OF ALFA OCCIDENTALE #4 2 Contents and 2020/21 Committee contact details. Page 2 October/November 2020 update on AROCA WA’s activities. Page 3 Como Classic Car Show held on Sunday 4th October. -

Descriptionpm Passo Della Cisa

List Time of PM 1.1 (PASSO DELLA CISA 1' RILEV) 1 / 4 No. Driver/Co-Driver Car Year/Coef Start / Stop Actual / Imp. Scarto Penalty Table Points 501 NATAF Oren Ferrari 250 GT Berlinetta Luss 1963 17:46'27 1'58 A 24 24 95 GLUKHOVA Ludmila 1,00 17:48'25 2'22 502 CZUBALA Sebastian Ferrari 330 GTC 1967 18:15'50 2'16 A 6 6 291 PODWOJEWSKI Pawel 1,00 18:18'06 2'22 503 FABBRIS Romana Ferrari Dino 246 GT 1971 17:53'35 2'15 A 7 7 272 GABETTI Cristina 1,00 17:55'50 2'22 505 DUVILLA Olivier Ferrari 512 BB 1983 17:50'04 2'24 R 2 2 370 VERDEAUX Sébastien 1,00 17:52'28 2'22 506 FAINI Eugenio Enrico Ferrari 328 GTS 1987 17:37'33 2'17 A 5 5 310 KARAKULOVA Yuliya 1,00 17:39'50 2'22 508 CERUTTI Roberto Ferrari F110 AB E 1990 17:38'14 2'22 0 420 ZOBBIO Ruggero 1,00 17:40'36 2'22 509 HERREN Bruno Ferrari 348 TB 1992 18:01'31 2'15 A 7 7 272 JAEGGI Kurt 1,00 18:03'46 2'22 510 PETERSEN Michael Christian Ferrari 348 TB/TS 1993 17:39'40 2'24 R 2 2 370 SUNDRANI Karima 1,00 17:42'04 2'22 511 MOLINARI Gioel Ferrari F50 1996 18:20'43 1'31 A 51 51 38 TOSTI Massimo 1,00 18:22'14 2'22 512 BITTNER Matthias Ferrari 550 MARANELLO 1996 17:40'19 2'24 R 2 2 370 BITTNER Thomas 1,00 17:42'43 2'22 513 EICHHORN Jürgen Ferrari 456 GT 1999 17:43'35 2'20 A 2 2 370 EICHHORN Moritz 1,00 17:45'55 2'22 515 NICOLI Roberto Ferrari 360 Challenge Stradale 2004 17:39'27 2'33 R 11 11 217 FESTA Diana Elettra 1,00 17:42'00 2'22 516 VAN BROUWERSHAVEN Johannes Ferrari F430 Spider 2005 17:55'20 2'25 R 3 3 350 KONINGS Mark Jozeph 1,00 17:57'45 2'22 517 DEN HARTOG Johan Ferrari 575 SUPERAMERICA 2006 -

Ferrari: Under the Skin Tour Proposal

Ferrari: Under the Skin Tour proposal FERRARI: UNDER THE SKIN, DESIGN MUSEUM, 2017, PHOTOGRAPHY BY LUKE HAYES FERRARI: UNDER THE SKIN 2 Contents Exhibition summary 3 Exhibition structure 4 What are they saying? 10 Exhibition details 11 Terms and conditions 12 Contact 13 The Design Museum Touring Programme The Design Museum Touring Exhibitions Programme was set up in 2002 with an aim to bring design exhibitions to audiences around the UK and internationally. Since then, the Museum has toured more than 120 exhibitions to 99 venues in 27 countries worldwide. In May 2018, The Design Museum was awarded the title of European Museum of the Year and commended by the panel for its effort in developing ‘an important democratic and multi-layered intercultural dialogue, with a significant social impact in the community’. The Design Museum touring exhibitions range in size from 150 to 1000 square metres and cover all areas of design – architecture, fashion, furniture, graphics, product, and more. FERRARI: UNDER THE SKIN 2 FERRARI: UNDER THE SKIN, DESIGN MUSEUM, 2017, PHOTOGRAPHY BY LUKE HAYES Exhibition summary What makes a myth? How does a car acquire an immortal name? What makes its creator an enigma and a legend? Today, building a brand is a calculated and knowing process, but Ferrari arose from far more subtle and organic processes that matched different times. In an Italy ravaged by the Second World War, Enzo Ferrari and a small team decided to create the perfect racing machine. The exhibition, developed together with Ferrari, explores its powerful personality, the seldom-seen design process, manufacturing, its racing history, and the way Ferrari’s famous clientele helped establish its reputation. -

Lernpaket Mythos Ferrari

L Lernpaket für Lehrer und Schüler Weltkulturerbe Völklinger Hütte Europäisches Zentrum für Kunst und Industriekultur Lernpaket66302 Völklingen für Lehrer / Saar und Schüler Redaktion: Peter Backes, Frank Krämer, Jeanette Wagner Tel. 06898/9100-159, Fax 06898/9100-111 [email protected] Weltkulturerbe Völklinger Hütte Europäisches Zentrum für Kunst und Industriekultur Generaldirektor Prof. Dr. Meinrad Maria Grewenig Mythos Ferrari – Fotografien Günther Raupp 22. September 2012 bis 20. Januar 2013, täglich ab 10Uhr Lernpaket für Lehrer und Schüler Inhalt 1. Ausstellungsdaten und Service für Schulen S.3 2. Vorwort S.5 3. Ferrari Chronik S.7 4. Biografie Günther Raupp S.11 5. Die Autos S.13 6. Unterrichtsvorschläge S.67 7. Quellentexte S.81 8. Ferrari ABC S.91 9. Katalog zur Ausstellung S.95 10. Ausstellungen und Museen S.95 11. Literatur S.96 12. Filme und Serien S.100 13. Links S.101 Impressum Weltkulturerbe Völklinger Hütte Europäisches Zentrum für Kunst und Industriekultur 66302 Völklingen / Saar Redaktion: Peter Backes, Dorothée Fellinger, Frank Krämer, Jeanette Wagner Tel. 06898/9100-159, Fax 06898/9100-111 [email protected] Seite 2 Weltkulturerbe Völklinger Hütte Europäisches Zentrum für Kunst und Industriekultur Generaldirektor Prof. Dr. Meinrad Maria Grewenig 1. Ausstellungsdaten und Service für Schulen Öffnungszeiten Erzhalle, täglich von 10 bis 19 Uhr Ermäßigt 10,00 € Normal 12,00 € Familien (2 Erwachsene mit Kindern und Jugendlichen bis 16 Jahre) 25,00 € Kinder und Jugendliche 3,00 € Kinder und Jugendliche im Klassenverband 3,00 € Gebuchte Führung 80,00 € (plus ermäßigten Eintritt) (max. 30 Personen, Dauer der Führung ca. 1,5 Stunden). Jahreskarten Jahreskarten Kinder/ Schüler 6,00 € Erwachsene 25,00 € Familien 55,00 € Sonderkonditionen für Schulen Schulklassenführung im Bonuspaket zum Preis von 100 Euro inkl. -

MOTOR VALLEY TOURS the Signature Edition at CASA MARIA LUIGIA the PERFECT BALANCE BETWEEN SLOW FOOD and FAST CARS MOTOR VALLEY: EMILIA’S BEATING HEART

Under the patronage of MOTOR VALLEY TOURS the signature edition at CASA MARIA LUIGIA THE PERFECT BALANCE BETWEEN SLOW FOOD AND FAST CARS MOTOR VALLEY: EMILIA’S BEATING HEART Motor Valley is the charming place where the world’s fastest cars are born, a place of “slow food and fast cars” as the great chef Massimo Bottura likes to say. Ferrari, Maserati, Pagani, Lamborghini, Dallara and Ducati factories and museums are located within a few kilometers from Modena and its not-to-be-missed Piazza Grande, a UNESCO World Heritage Site. HIGHLIGHTS Motor Valley Tours will allow you to discover all this beauty while driving a legendary car, an icon of the “Dolce Vita”, in an absolutely one-of-a-kind bespoke edition: experiencing the amazing hospitality of Massimo Bottura and his wife Lara at Casa Maria Luigia. Canossa Events makes its fleet of Abarth 595 Cabriolets available for this tour. A fleet of unique cars, specially designed by Lapo Elkann’s creative genius and Garage Italia craftsmens’ skilled hands. Or you can use your own collector’s car. DAY 1 TUESDAY 20th OCTOBER 2020 15.00 Check in at Casa Maria Luigia Enjoy your “home away from home” 16.30 The heart of Modena, a UNESCO World Heritage: ♦ il Duomo di Modena ♦ il Palazzo Ducale ♦ Piazza Grande e Piazza Roma ♦ exclusive visit of Torre Ghirlandina and Teatro Luciano Pavarotti 20.00 “Francescana” dinner at Casa Maria Luigia Overnight stay at Casa Maria Luigia DAY 2 WEDNESDAY 21st OCTOBER 2020 09.00 Emilian breakfast at Casa Maria Luigia 10.30 Discover Horacio Pagani’s great adventure 13.00 -

The Ferraris (And Ourselves) a Rest, Before Heading to the Museo Ferrari to Experience the Passion, Innovation and Technology Used to Create These Iconic Cars

Starting in Milan we will spend three unforgettable days driving an incredible Ferrari line-up through some of Italy’s best driving routes. First the convoy will head north and conquer what is probably the most romanticised and well-documented driving road in the world – Stelvio Pass. The Stelvio zigzags its way up the Italian Alps in Parco Nazionale dello Stelvio and is the highest paved mountain pass in the world! With 60 hairpins overlooking a spectacular landscape, this road is a ‘must do’ for anyone who lives and breathes the thrill of driving! From here we will take sections of the renowned Dolomite Road south towards the sparkling Mediterranean, then continue on to the home of Ferrari – Maranello. Our route will also allow you to experience and enjoy Italy’s spectacularly dramatic and diverse scenery. From emotive alpine roads with rugged, craggy cliffs, sharp hairpins, and limestone walls, to the lazy winds and bends of the Mediterranean coastal drive, and the rolling hills, medieval towers and vineyards that define Italy, this drive will undoubtedly challenge any avid Ferrari fan while stealing your breath away! Once we arrive in Maranello/Modena we will give the Ferraris (and ourselves) a rest, before heading to the Museo Ferrari to experience the passion, innovation and technology used to create these iconic cars. We will also visit the architectural masterpiece that is the recently completed Enzo Ferrari Museum; a Museum that celebrates the life and work of the Grand Master himself! Along the Tour we will stay in five and four star historic chateaus and converted castles.