Bangladesh Bank Requirements

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

MIRPUR PAPERS, Volume 22, Issue 23, November 2016

ISSN: 1023-6325 MIRPUR PAPERS, Volume 22, Issue 23, November 2016 MIRPUR PAPERS Defence Services Command and Staff College Mirpur Cantonment, Dhaka-1216 Bangladesh MIRPUR PAPERS Chief Patron Major General Md Saiful Abedin, BSP, ndc, psc Editorial Board Editor : Group Captain Md Asadul Karim, psc, GD(P) Associate Editors : Wing Commander M Neyamul Kabir, psc, GD(N) (Now Group Captain) : Commander Mahmudul Haque Majumder, (L), psc, BN : Lieutenant Colonel Sohel Hasan, SGP, psc Assistant Editor : Major Gazi Shamsher Ali, AEC Correspondence: The Editor Mirpur Papers Defence Services Command and Staff College Mirpur Cantonment, Dhaka – 1216, Bangladesh Telephone: 88-02-8031111 Fax: 88-02-9011450 E-mail: [email protected] Copyright © 2006 DSCSC ISSN 1023 – 6325 Published by: Defence Services Command and Staff College Mirpur Cantonment, Dhaka – 1216, Bangladesh Printed by: Army Printing Press 168 Zia Colony Dhaka Cantonment, Dhaka-1206, Bangladesh i Message from the Chief Patron I feel extremely honoured to see the publication of ‘Mirpur Papers’ of Issue Number 23, Volume-I of Defence Services Command & Staff College, Mirpur. ‘Mirpur Papers’ bears the testimony of the intellectual outfit of the student officers of Armed Forces of different countries around the globe who all undergo the staff course in this prestigious institution. Besides the student officers, faculty members also share their knowledge and experience on national and international military activities through their writings in ‘Mirpur Papers’. DSCSC, Mirpur is the premium military institution which is designed to develop the professional knowledge and understanding of selected officers of the Armed Forces in order to prepare them for the assumption of increasing responsibility both on staff and command appointment. -

Company Profile

Nogor Solutions Limited Enabling ICT Solutions for you Company Profile Nogor Solutions Limited House No. 69 (4th floor), Road No. 08, Block-D, Niketon, Gulshan-1, Dhaka-1212. Web: www.nogorsolutions.com Nogor Solutions Limited Enabling ICT Solutions for you Profile of NOGOR Solutions Limited INTRODUCTION The revolution of the IT industry has a great influence on the development of modern civilization. Believing this development as an art the NOGOR Solutions Limited, one of the leading IT firms in Bangladesh is creating some success stories to contribute in the global IT industry. In this era of globalization, IT solutions like software solutions, web development and networking are some basic needs for organizational development and businesses are getting dependent on these everywhere. For this reason, organizations that do not have IT infrastructure are facing problem to compete with those who have a strong lead in the IT world. Considering all these facts, NOGOR Solutions Limited started its business in 2009 to provide the highest level of professional service to the organizations and individuals to create a strong IT infrastructure. Now it has become a recognized IT solution provider which has been providing anything on desktop, web, in networking & in developing any software without any complication to clients worldwide. Being in IT business for over 7 years now, it has a skilled expert team with good experience in Web and Software development. NOGOR Solutions Limited are providing various ICT Services for last 7 years in Bangladesh and also earn foreign remittance by offshore software Development for the various countries like, UK, USA, Canada and Australia. -

Bangladesh-Army-Journal-61St-Issue

With the Compliments of Director Education BANGLADESH ARMY JOURNAL 61ST ISSUE JUNE 2017 Chief Editor Brigadier General Md Abdul Mannan Bhuiyan, SUP Editors Lt Col Mohammad Monjur Morshed, psc, AEC Maj Md Tariqul Islam, AEC All rights reserved by the publisher. No part of this publication may be reproduced or transmitted in any form or by any means without prior permission of the publisher. The opinions expressed in the articles of this publication are those of the individual authors and do not necessarily reflect the policy and views, official or otherwise, of the Army Headquarters. Contents Editorial i GENERATION GAP AND THE MILITARY LEADERSHIP CHALLENGES 1-17 Brigadier General Ihteshamus Samad Choudhury, ndc, psc MECHANIZED INFANTRY – A FUTURE ARM OF BANGLADESH ARMY 18-30 Colonel Md Ziaul Hoque, afwc, psc ATTRITION OR MANEUVER? THE AGE OLD DILEMMA AND OUR FUTURE 31-42 APPROACH Lieutenant Colonel Abu Rubel Md Shahabuddin, afwc, psc, G, Arty COMMAND PHILOSOPHY BENCHMARKING THE PROFESSIONAL COMPETENCY 43-59 FOR COMMANDERS AT BATTALION LEVEL – A PERSPECTIVE OF BANGLADESH ARMY Lieutenant Colonel Mohammad Monir Hossain Patwary, psc, ASC MASTERING THE ART OF NEGOTIATION: A MUST HAVE ATTRIBUTE FOR 60-72 PRESENT DAY’S BANGLADESH ARMY Lieutenant Colonel Md Imrul Mabud, afwc, psc, Arty FUTURE WARFARE TRENDS: PREFERRED TECHNOLOGICAL OUTLOOK FOR 73-83 BANGLADESH ARMY Lieutenant Colonel Mohammad Baker, afwc, psc, Sigs PRECEPTS AND PRACTICES OF TRANSFORMATIONAL LEADERSHIP: 84-93 BANGLADESH ARMY PERSPECTIVE Lieutenant Colonel Mohammed Zaber Hossain, AEC USE OF ELECTRONIC GADGET AND SOCIAL MEDIA: DICHOTOMOUS EFFECT ON 94-113 PROFESSIONAL AND SOCIAL LIFE Major A K M Sadekul Islam, psc, G, Arty Editorial We do express immense pleasure to publish the 61st issue of Bangladesh Army Journal for our valued readers. -

Flood Risk Management in Dhaka a Case for Eco-Engineering

Public Disclosure Authorized Flood Risk Management in Dhaka A Case for Eco-Engineering Public Disclosure Authorized Approaches and Institutional Reform Public Disclosure Authorized People’s Republic of Bangladesh Public Disclosure Authorized • III contents Acknowledgements VII Acronyms and abbreviations IX Executive Summary X 1 · Introduction 2 Objective 6 Approach 8 Process 9 Organization of the report 9 2 · Understanding Flood Risk in Greater Dhaka 10 disclaimer Demographic changes 13 This volume is a product of the staff of the International Bank for River systems 13 Reconstruction and Development/ The World Bank. The findings, interpretations, and conclusions expressed in this paper do not necessarily Monsoonal rain and intense short-duration rainfall 17 reflect the views of the Executive Directors of The World Bank or the Major flood events and underlying factors 20 governments they represent. The World Bank does not guarantee the accuracy of the data included in this work. The boundaries, colors, denominations, and Topography, soil, and land use 20 other information shown on any map in this work do not imply any judgment Decline of groundwater levels in Dhaka on the part of The World Bank concerning the legal status of any territory or the 27 endorsement or acceptance of such boundaries. Impact of climate vulnerability on flood hazards in Dhaka 28 copyright statement Flood vulnerability and poverty 29 The material in this publication is copyrighted. Copying and/or transmitting Summary 33 portions or all of this work without permission may be a violation of applicable law. The International Bank for Reconstruction and Development/ The World Bank encourages dissemination of its work and will normally grant permission to 3 · Public Sector Responses to Flood Risk: A Historical Perspective 34 reproduce portions of the work promptly. -

Download File

Cover and section photo credits Cover Photo: “Untitled” by Nurus Salam is licensed under CC BY-SA 2.0 (Shangu River, Bangladesh). https://www.flickr.com/photos/nurus_salam_aupi/5636388590 Country Overview Section Photo: “village boy rowing a boat” by Nasir Khan is licensed under CC BY-SA 2.0. https://www.flickr.com/photos/nasir-khan/7905217802 Disaster Overview Section Photo: Bangladesh firefighters train on collaborative search and rescue operations with the Bangladesh Armed Forces Division at the 2013 Pacific Resilience Disaster Response Exercise & Exchange (DREE) in Dhaka, Bangladesh. https://www.flickr.com/photos/oregonmildep/11856561605 Organizational Structure for Disaster Management Section Photo: “IMG_1313” Oregon National Guard. State Partnership Program. Photo by CW3 Devin Wickenhagen is licensed under CC BY 2.0. https://www.flickr.com/photos/oregonmildep/14573679193 Infrastructure Section Photo: “River scene in Bangladesh, 2008 Photo: AusAID” Department of Foreign Affairs and Trade (DFAT) is licensed under CC BY 2.0. https://www.flickr.com/photos/dfataustralianaid/10717349593/ Health Section Photo: “Arsenic safe village-woman at handpump” by REACH: Improving water security for the poor is licensed under CC BY 2.0. https://www.flickr.com/photos/reachwater/18269723728 Women, Peace, and Security Section Photo: “Taroni’s wife, Baby Shikari” USAID Bangladesh photo by Morgana Wingard. https://www.flickr.com/photos/usaid_bangladesh/27833327015/ Conclusion Section Photo: “A fisherman and the crow” by Adnan Islam is licensed under CC BY 2.0. Dhaka, Bangladesh. https://www.flickr.com/photos/adnanbangladesh/543688968 Appendices Section Photo: “Water Works Road” in Dhaka, Bangladesh by David Stanley is licensed under CC BY 2.0. -

Armed Forces War Course-2013 the Ministers the Hon’Ble Ministers Presented Their Vision

National Defence College, Bangladesh PRODEEP 2013 A PICTORIAL YEAR BOOK NATIONAL DEFENCE COLLEGE MIRPUR CANTONMENT, DHAKA, BANGLADESH Editorial Board of Prodeep Governing Body Meeting Lt Gen Akbar Chief Patron 2 3 Col Shahnoor Lt Col Munir Editor in Chief Associate Editor Maj Mukim Lt Cdr Mahbuba CSO-3 Nazrul Assistant Editor Assistant Editor Assistant Editor Family Photo: Faculty Members-NDC Family Photo: Faculty Members-AFWC Lt Gen Mollah Fazle Akbar Brig Gen Muhammad Shams-ul Huda Commandant CI, AFWC Wg Maj Gen A K M Abdur Rahman R Adm Muhammad Anwarul Islam Col (Now Brig Gen) F M Zahid Hussain Col (Now Brig Gen) Abu Sayed Mohammad Ali 4 SDS (Army) - 1 SDS (Navy) DS (Army) - 1 DS (Army) - 2 5 AVM M Sanaul Huq Brig Gen Mesbah Ul Alam Chowdhury Capt Syed Misbah Uddin Ahmed Gp Capt Javed Tanveer Khan SDS (Air) SDS (Army) -2 (Now CI, AFWC Wg) DS (Navy) DS (Air) Jt Secy (Now Addl Secy) A F M Nurus Safa Chowdhury DG Saquib Ali Lt Col (Now Col) Md Faizur Rahman SDS (Civil) SDS (FA) DS (Army) - 3 Family Photo: Course Members - NDC 2013 Brig Gen Md Zafar Ullah Khan Brig Gen Md Ahsanul Huq Miah Brig Gen Md Shahidul Islam Brig Gen Md Shamsur Rahman Bangladesh Army Bangladesh Army Bangladesh Army Bangladesh Army Brig Gen Md Abdur Razzaque Brig Gen S M Farhad Brig Gen Md Tanveer Iqbal Brig Gen Md Nurul Momen Khan 6 Bangladesh Army Bangladesh Army Bangladesh Army Bangladesh Army 7 Brig Gen Ataul Hakim Sarwar Hasan Brig Gen Md Faruque-Ul-Haque Brig Gen Shah Sagirul Islam Brig Gen Shameem Ahmed Bangladesh Army Bangladesh Army Bangladesh Army Bangladesh -

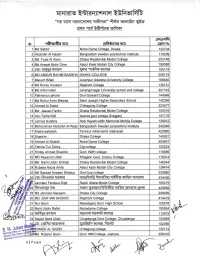

Unclaimed Deposit Statement for Bank's Website-As on 31.12.2020

SL Name of Branch Present Address Permanent Address Account Type Name of Account/ Beneficiary Account/Instrument No. Father's Name Amount BB Cheque Amount Date of Transfer Remarks No. 1 SKB Branch Law Chamber, Amin Court, 5th Floor, 62-63 Motijheel C/A, Dhaka. NA Current Account Graham John Walker 0003-0210001547 NA 130,569.00 130,569.00 18-Aug-14 2 SKB Branch NA NA NA Grafic System Pvt. Ltd. PAA00014522 NA 775.00 3 SKB Branch NA NA NA Elesta Security Services Ltd. PAA00015444 NA 4,807.00 5,582.00 22-Nov-15 4 SKB Branch 369,New North Goran Khilgaon,Dhaka. Vill-Maziara, PO-Jibongonj Bazar, Nabinagar, Brahman Baria Savings Account Farida Iqbal 0003-0310010964 Khondokar Iqbal Hossain 1,212.00 5 SKB Branch Dosalaha Villa, Sec#6,Block#D,Road#9, House# 11,Mirpur ,Dhaka. Vill-Balurchar, PO-Baksha Nagar,PS-Nababgonj,Dist-Dhaka. Savings Account Md. Shah Alam 0003-0310009190 Late Abdur Razzak 975.00 6 SKB Branch H#26(2nd floor)Road# 111,Block-F,Banani,Dhaka. Vill- Chota Khatmari,PO-Joymonirhat, PS-Bhurungamari,Dist-Kurigram. Savings Account S.M. Babul Akhter 0003-0310014077 Md. Amjad Hossain 782.00 7 SKB Branch 135/1,1st Floor Malibag,Dhaka. Vill-Bhairabdi,PO-Sultanshady,PS-Araihazar,Dist-Narayangonj. Savings Account Mohammad Mogibur Rahman 0003-0310012622 Md. Abdur Rashid 416.00 14,951.00 6-Jun-16 8 SKB Branch A-1/16,Sonali Bank Colony, Motijheel,Dhaka. 12/2,Nabin Chanra Goshwari Road, Shampur, Dhaka. Savings Account Salina Akter Banu 0003-0310012668 Md. Rahmat Ali 966.00 9 SKB Branch Cosmos Center 69/1,New Circular Road,Malibage,Dhaka. -

A Professional Journal of National Defence College Volume 6 Number

A Professional Journal of National Defence College Volume 6 Number 1 June 2007 National Defence College Bangladesh EDITORIAL BOARD Chief Patron Lieutenant General Abu Tayeb Muhammad Zahirul Alam, rcds,psc Editor-in-Chief Air Commodore Mahmud Hussain, ndc, psc Associate Editors Captain M Anwarul Islam, (ND), afwc, psc, BN Lieutenant Colonel Md Abdur Rouf, afwc, psc Assistant Editor CSO-3 Md Nazrul Islam Editorial Advisors Dr. Fakrul Islam Ms. Shuchi Karim DISCLAMER The analysis, opinions and conclusions expressed or implied in this Journal are those of the authors and do not necessarily represent the views of the NDC, Bangladesh Armed Forces or any other agencies of Bangladesh Government. Statements of fact or opinion appearing in NDC Journal are solely those of the authors and do not imply endorsement by the editors or publisher. ISSN: 1683-8475 INITIAL SUBMISSION Initial Submission of manuscripts and editorial correspondence should be sent to the National Defence College, Mirpur Cantonment, Dhaka-1216, Bangladesh. Tel: 88 02 8059488, Fax: 88 02 8013080, Email : [email protected]. Authors should consult the Notes for Contributions at the back of the Journal before submitting their final draft. The editors cannot accept responsibility for any damage to or loss of manuscripts. Subscription Rate (Single Copy) Individuals : Tk 300 / USD 10 (including postage) Institutions : Tk 375 / USD 15 (including postage) Published by the National Defence College, Bangladesh All rights reserved. No part of this publication may be reproduced, stored in retrieval system, or transmitted in any form, or by any means, electrical, photocopying, re- cording, or otherwise, without the prior permission of the publisher. -

Unsuccessful Registrations

Unsuccessful Registrations Mirza Moinuddin Dhaka Changes (An English Medium School) A-Level Hasan Siam Dhaka Shahriar Hoque HURDCO International School A-Level Dhaka Tasnim Rafa Changes (An English Medium School) A-Level SHIBAJI Dhaka THE STUDY TOWN A-Level SAMAJDER GOLAM Dhaka govt titumir college O-Level MURSHEED Serat Mahmud Dhaka Mirzapur Cadet College XI Saad Azmain Rashid Dhaka Notre Dame College Dhaka XI Raiyan Shirajum Munira Dhaka Viqarunnisa Noon College XI Oyshi Dhaka Zedan Mirzapur cadet college XI Mahmuda Akther Savar cantonment public school and Dhaka XI Orpita college Dhaka Tanjila hasan Banglabazar govt. Girl's high school SSC Fateha Akter Dhaka Viqarunnisa Noon School & College SSC Moontaha Abdullah Siham Dhaka St.Joseph Higher Secondary School X Rahman Dhaka Aryan Changes(An enhglish medium school) IX Chattagram Avvarul hyder A-Level Chattagram Majdi talal International Hope School Bangladesh O-Level Chattagram Md. Maftun chy Presidency International School Chittagong O-Level Chattagram NAFISA HOQUE Presidency International School VII LABIBA MOIN Chattagram PRESIDENCY INTERNATIONAL SCHOOL VII SMITA Bangladesh Mahila Shamity Girls'High Chattagram Tahmida Tahrin VII School and College Chattagram Abrar Islam Presidency International School VII Sajeduzzzaman Chattagram Chattogram Cantonment Public College XI Akib Chattagram Ahad Bin Azad Govt. City College XI Sayeda Nusrat Chattagram Chattogram Cantonment Public College XI Jahan Chattagram TahmidJahangir Cantonment English School and College XI SUNANDA Chattagram Dr. Khastagir -

A Professional Journal of National Defence College Volume 17

A Professional Journal of National Defence College Volume 17 Number 1 April 2018 National Defence College Bangladesh EDITORIAL BOARD Chief Patron Lieutenant General Chowdhury Hasan Sarwardy, BB, SBP, BSP, ndc, psc, PhD Editor-in-Chief Air Commodore M Mortuza Kamal, GUP, ndc, psc, GD(P) Editor Colonel (Now Brigadier General) A K M Fazlur Rahman, afwc, psc Associate Editors Brigadier General Md Rafiqul Islam, SUP, ndc, afwc, psc Lieutenant Colonel A S M Badiul Alam, afwc, psc, G+, Arty Assistant Editors Assistant Director Md Nazrul Islam Lecturer Farhana Binte Aziz ISSN: 1683-8475 All rights reserved. No part of this publication may be reproduced, stored in retrieval system, or transmitted in any form, or by any means, electrical, photocopying, recording, or otherwise, without the prior permission of the publisher. Published by the National Defence College, Bangladesh Design & Printed by : ORNATE CARE 87, Mariam Villa (2nd Floor), Nayapaltan, Dhaka-1000, Bangladesh Cell: 01911546613, E-mail: [email protected] DISCLAIMER The analysis, opinions and conclusions expressed or implied in this Journal are those of the authors and do not necessarily represent the views of the NDC, Bangladesh Armed Forces or any other agencies of Bangladesh Government. Statement, fact or opinion appearing in NDC Journal are solely those of the authors and do not imply endorsement by the editors or publisher. iii CONTENTS Page College Governing Body vi Vision, Mission and Objectives of the College vii Foreword viii Editorial ix Faculty and Staff x Abstracts xi -

Developments

Highlights: Camp Conditions: • UN agencies will visit Bhasan Char to conduct a technical study of Bhasan Char, which will evaluate its ‘technical, security, and financial’ feasibility to serve as an additional locale for Rohingyas. The plan to move some Rohingya to the island has been delayed until after the Government of Bangladesh gets the “green light” from the UN. High-level Statements: • USAID officials have condemned Myanmar’s inaction in creating conditions conducive to a voluntary, safe and dignified return of the Rohingya. • India has made multiple statements about Rohingya repatriation today, through its Foreign Minister Subrahmanyam Jaishankar, who wrote a letter to the Foreign Minister of Bangladesh, and through Prime Minister Narendra Modi, who had a bilateral meeting with Myanmar State Counsellor Aung San Suu Kyi on the margins of ASEAN summit in Bangkok. International Events: • At the end of Asean’s biannual summit last week, Asean’s 10 member countries unanimously supported the formation of an ad hoc support team to carry out the recommendations of preliminary needs. That includes continued communication and consultation with affected communities, such as the Rohingya refugees in Bangladesh. Country Visits: • USAID deputy administrator Bonnie Glick and acting assistant secretary of State Alice G. Wells visited Bangladesh November 5-7. In a statement following a visit by two top US officials to Bangladesh, the country also underscored that it would continue its efforts to bring an end to the refugee crisis. Developments: A dozen dead, fishermen missing after cyclone Bulbul lashes Bangladesh and India Reuters (November 10) At least 13 people were killed in Bangladesh and India after cyclone Bulbul lashed coastal areas this weekend, though prompt evacuations saved many lives and the worst is over. -

16R{19Ffiebffie'

:16r{19ffieBffiE' "qg {[6{ <tqEtmrt{ -ilftEs'f" tr-s q{flt{ AtT ereN "rr(tfr"fmrvtfu$t ,gq,{qf8 gGtrffi{{rq SI "r-ftr,Etaqrq GtI6r {i 1 Md Sabbir Notre Dame Colleqe, Dhaka 122734 2 Abdullah Al Hasan Banqladesh sweden polvtechnic lnstitute 115239 J Md. Fuad AlAlam Dhaka Residential Model Colleqe 203148 4 Md.Anayet Kobir Ome Abdul Kadir Mollah Citv Colleqe 1 99088 5 Cil3 IIIIGI<-{NF[ uqqrrrcF-osrdrq 105174 b MD.ABDUR RAHIM BADSHA DHAKA COLLEGE 228119 7 Masum Billah Jurainpur Adarsha U niversity College 168440 B Md.Rockv Hossain Raishahi Colleoe 1351 31 I Md Ariful lslam Jahanqirnaoar Universitv school and colleqe 307743 10 Fatima tus iahara Govt Edward Colleqe 144048 11 Md RuhulAmin Biswas Saint Joseph Hiqher Secondary School 142356 12 Ahmed Al Sabid Chittaoono Colleoe 223577 13 Md. Jeesan Fardin Dhaka Residential Model Colleqe 1 50316 14 Abu Talha Rafi lslamia qovt colleqe,Siraiqani 147176 15 Lamiya Sultana Hazi Kevamuddin Memorial Mohila Colleqe 128912 16 Mohammad Abdullah Al Reaz Banqladesh Sweden polytechnic lnstitute 242046 17 Khalid saifullah Ta'mirul millat kamil madrasah 422660 18 Shamim Dhaka Colleqe 140261 19 Ahmed Al Shahik Notre Dame Colleqe 505801 20 Fatima TuzZohra Ctg college 120224 21 Hridav Ahmed Shadhin Govt. KMH colleqe 1 1 8985 22 MD Neyamot Ullah Khilqaon Govt. Colonv Colleqe 178314 23 Md. Naim Uddin Shihab Dhaka Residential Model Colleqe 148344 24 Rubaba Nazia Anita Abdul kadir Mollah Citv Colleqe 136474 25 Md Sazzad Hossan Shabuz Govt kup colleqe 230880 ,$ -26 mrc frq'erH 5fir<F'K \Il\9tq<il\9 e.railt\Blt {tqht}il atI\crt \thflrl 434456 Jannatul Ferdous Dipti Raiuk Uttara Model College 155219 flP q1s4 -c9a Rne{rta{s 1r <uil;[ frfrffTT s"rR-4 nl'Grlqr, SFI{[ 428858 Sr,o F2e Md.Jannatul Nayeem Dhaka Citv Colleqe 208456 FJ 30 MD.