Delhi Airports

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

India: Airport Security Screening for Passengers Departing on International Flights Research Directorate, Immigration and Refugee Board of Canada, Ottawa

Home > Research > Responses to Information Requests RESPONSES TO INFORMATION REQUESTS (RIRs) New Search | About RIR's | Help 14 April 2009 IND103120.E India: Airport security screening for passengers departing on international flights Research Directorate, Immigration and Refugee Board of Canada, Ottawa In 27 April 2009 correspondence, the Security Manager of Air India in Toronto stated the following in regard to airport security screening for passengers departing on international flights: … when the passenger approaches the check-in counter, his/her travel documents, such as passport, visa, ticket, etc. are checked by an airline check-in agent to verify the genuineness of the [documents] prior to the issuance of a boarding card. After obtaining the boarding card, the passenger goes through immigration checks where his/her passport/visa is thoroughly screened and their biographical data are stored into the computer by the government immigration officials. And, at this stage the passenger's data is matched with the suspected criminal databank. The Security Manager also stated that these screening procedures are generally similar at all airports (27 April 2009). The Bengaluru International Airport [Bangalore] website has a "security and passport control" section for international flight passengers that states that passengers, after acquiring their boarding pass, must proceed to the emigration check area where they are to complete "Visa formalities," after which they can proceed to the "international security control area," and then to the departure area (n.d.). Specific information on the security screening procedures within the emigration check area or the international security control area is not available on this airport website. -

Economic Overview of Delhi Sectoral Composition and Contribution the Analysis of Sectoral Growth in GSDP of Delhi at Constant Pr

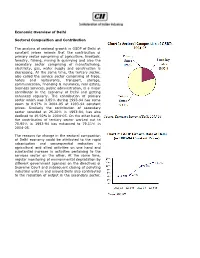

Economic Overview of Delhi Sectoral Composition and Contribution The analysis of sectoral growth in GSDP of Delhi at constant prices reveals that the contribution of primary sector comprising of agriculture, livestock, forestry, fishing, mining & quarrying and also the secondary sector comprising of manufacturing, electricity, gas, water supply and construction is decreasing. At the same time, the tertiary sector, also called the service sector comprising of trade, hotels and restaurants, transport, storage, communication, financing & insurance, real estate, business services, public administration, is a major contributor in the economy of Delhi and getting enhanced regularly. The contribution of primary sector which was 3.85% during 1993-94 has come down to 0.97% in 2004-05 at 1993-94 constant prices. Similarly the contribution of secondary sector recorded at 25.20% in 1993-94, has also declined to 19.92% in 2004-05. On the other hand, the contribution of tertiary sector worked out to 70.95% in 1993-94 has enhanced to 79.11% in 2004-05. The reasons for change in the sectoral composition of Delhi economy could be attributed to the rapid urbanisation and consequential reduction in agricultural and allied activities on one hand and substantial increase in activities pertaining to the services sector on the other. At the same time, regular monitoring of environmental degradation by different government agencies on the directives of Supreme Court and subsequent closing of polluting industrial units in and around Delhi also contributed to the reduction of output in the secondary sector. Delhi's service sector has expanded due in part to the large skilled English-speaking workforce that has attracted many multinational companies. -

Central University of Punjab, Bathinda, Punjab

Central University of Punjab, Bathinda, Punjab Course Scheme For M.A. (History) 1 CENTRE FOR SOUTH AND CENTRAL ASIAN STUDIES (Including Historical Studies) Course structure-M.A. IN HISTORY % Weightage Semester I Marks Paper Course Title L T P Cr A B C D E Code HST. 501 Research F 4 0 0 4 25 25 25 25 100 Methodology HST. 503 Indian Political C 4 0 0 4 25 25 25 25 100 Thought HST. 504 Pre-History and C 4 0 0 4 25 25 25 25 100 Proto-History of India HST. 505 Ancient India C 4 0 0 4 25 25 25 25 100 (600BCE-300CE) HST. XXX Elective Course I E* 4 0 0 4 25 25 25 25 100 IDC. XXX Inter- E 2 0 0 2 15 10 10 15 50 Disciplinary/Open (O)** Elective HST. 599 Seminar C 0 0 0 2 15 10 10 15 50 TOTAL SEM I - 24 24 - 600 Elective Courses (Opt any one courses within the department) HST. 511 Art and Architecture E* 4 0 0 4 25 25 25 25 100 of Ancient India HST. 512 Early State and E* 4 0 0 4 25 25 25 25 100 Society in Ancient India Interdisciplinary Course/Open Elective Offered (For other Centers) HST. 521 Harrappan E 2 0 0 2 15 10 10 15 50 Civilization (O)** HST. 522 Religion in Ancient E 2 0 0 2 15 10 10 15 50 India (O)** 2 Semester II % Weightage Marks Paper Course Title L T P Cr A B C D E Code HST. -

Study on Airport Ownership and Management and the Ground Handling Market in Selected Non-European Union (EU) Countries

Study on airport DG MOVE, European ownership and Commission management and the ground handling market in selected non-EU countries Final Report Our ref: 22907301 June 2016 Client ref: MOVE/E1/SER/2015- 247-3 Study on airport DG MOVE, European ownership and Commission management and the ground handling market in selected non-EU countries Final Report Our ref: 22907301 June 2016 Client ref: MOVE/E1/SER/2015- 247-3 Prepared by: Prepared for: Steer Davies Gleave DG MOVE, European Commission 28-32 Upper Ground DM 28 - 0/110 London SE1 9PD Avenue de Bourget, 1 B-1049 Brussels (Evere) Belgium +44 20 7910 5000 www.steerdaviesgleave.com Steer Davies Gleave has prepared this material for DG MOVE, European Commission. This material may only be used within the context and scope for which Steer Davies Gleave has prepared it and may not be relied upon in part or whole by any third party or be used for any other purpose. Any person choosing to use any part of this material without the express and written permission of Steer Davies Gleave shall be deemed to confirm their agreement to indemnify Steer Davies Gleave for all loss or damage resulting therefrom. Steer Davies Gleave has prepared this material using professional practices and procedures using information available to it at the time and as such any new information could alter the validity of the results and conclusions made. The information and views set out in this report are those of the authors and do not necessarily reflect the official opinion of the European Commission. -

Making Cities Work: Policies and Programmes in India

Making Cities Work: Policies and Programmes in India Debolina Kundu Arvind Pandey Pragya Sharma Published in 2019 Cover photo: Busy market street near Jama Masjid in New Delhi, India All rights reserved. No part of this report may be reproduced in any form by an electronic or mechanical means, including information storage and retrieval systems, without permission from the publishers. This peer-reviewed publication is suported by the GCRF Centre for Sustainable, Healthy and Learning Cities and Neighbourhoods (SHLC). The contents and opinions expressed in this report are those of the authors. Although the authors have made every effort to ensure that the information in this report was correct at press time, the authors do not assume and hereby disclaim any liability to any party for any loss, damage, or disruption caused by errors or omissions, whether such errors or omissions result from negligence, accident, or any other cause. SHLC is funded via UK Research and Innovation as a part of the Global Challenges Research Fund (Grant Reference Number: ES/P011020/1). SHLC is an international consortium of nine research partners as follows: University of Glasgow, Khulna University, Nankai University, National Institute of Urban Affairs, University of the Philippines Diliman, University of Rwanda, Ifakara Health Institute, Human Sciences Research Council and the University of Witwatersand Making Cities Work: Policies and Programmes in India Authors Debolina Kundu Arvind Pandey Pragya Sharma Research Assistance Sweta Bhusan Biswajit Mondal Baishali -

'Airports Authority of India (Aai)' Committee on Public

1 'AIRPORTS AUTHORITY OF INDIA (AAI)' MINISTRY OF CIVIL AVIATION COMMITTEE ON PUBLIC UNDERTAKINGS (2020-21) FIRST REPORT (SEVENTEENTH LOK SABHA) LOK SABHA SERCRTARIAT NEW DELHI FIRST REPORT COMMITTEE ON PUBLIC UNDERTAKINGS (2020-21) (SEVENTEENTH LOK SABHA) AIRPORTS AUTHORITY OF INDIA MINISTRY OF CIVIL AVIATION Presented to Lok Sabha on 29.01.2021 Laid in Rajya Sabha on 29.01.2021 LOK SABHA SECRETARIAT NEW DELHI January, 2021/ Magha, 1942 (Saka ) ii CONTENTS Page (i) COMPOSITION OF THE COMMITTEE (2020-21) (vi) (ii) COMPOSITION OF THE COMMITTEE (2019-20) (vii) (iii) INTRODUCTION (viii) (iv) ACRONYMS (ix) REPORT PART-I Chapter-I Introduction (i) Brief history of Indian Aviation 1 (ii) Airport Authority of India 1 (iii) Board of Directors 2 (iv) Organization structure 3 (v) Agencies operating at airports 3 (vi) Memorandum of Understanding 4 Chapter-II Physical Performance of AAI 5 (i) Airports managed by AAI 5 (ii) Volume of Air Traffic at Airports 6 (iii) Future Growth in Air Traffic 7 (iv) Cargo growth 9 (v) Creation of Civil Aviation infrastructure 10 (vi) Runway expansion project at Udaipur Airport 11 Chapter-III Financial Performance 12 (i) Revenue from Aeronautical and Non-Aeronautical Services 12 and Other Sources (ii) Profit and Loss Account 13 (iii) Joint Ventures – DIAL and MIAL 17 (iv) Measures taken to improve the functions and profitability 26 Chapter-IV Organisational Matters 28 (i) Granting of Navratna Status to AAI 28 (ii) Human Resource Management 31 (iii) Pilots training facilities 33 (iv) ATC Training facilities 34 (v) -

Annual Report of AAI 2017-18

Hkkjrh; foekuiÙku izkf/dj.k AIRPORTS AUTHORITY OF INDIA rd Annual Report 23 2 0 1 7 - 1 8 Hon'ble Prime Minister Shri Narendra Modi flagging off the first UDAN Flight under Regional Connectivity Scheme (RCS) on Shimla - Delhi sector at Jubbarhati, Shimla Airport. Shri Suresh Prabhu, Union Minister of Civil Aviation, addressing the "Civil Aviation Research Organisation" (CARO) event at Hyderabad C O N T E N T S Highlights 2017-18 02 About AAI 08 General Information 10 Brief Profile of Board Members, Chief Vigilance Officer and KMP 11 Board's Report 14 Corporate Governance Report 23 Management Discussion & Analysis (MD&A) 27 Annexure 3 to Board's Report 52 Annual Report on CSR Activities 57 Sustainability Report 67 Financial Statements of AAI & Auditor's Report thereon 70 Financial Statements of CHIAL & Auditor's Report thereon 110 Financial Statements of AAICLAS Company Ltd. & Auditor's Report thereon 148 Surat Airport Hkkjrh; foekuiÙku izkf/dj.k AIRPORTS AUTHORITY OF INDIA Signing of MoU between AAI and the French Civil Aviation Authority to further the active technical cooperation programme between India and France. S T Signing of MoU H between AAI and G I Uttarakhand Civil Aviation L Development Authority for the Development of H Aviation Sector G in Uttarakhand. I H Signing of MoU between AAI and Honeywell technology Solutions Lab Pvt. Ltd. in the field of aviation technologies, systems and procedures. 02 23rd Annual Report 2017-18 Hkkjrh; foekuiÙku izkf/dj.k AIRPORTS AUTHORITY OF INDIA Signing of MoU between AAI and Government of Haryana for development of civil aviation infrastructure in the State. -

The Lockdown to Contain the Coronavirus Outbreak Has Disrupted Supply Chains

JOURNALISM OF COURAGE SINCE 1932 The lockdown to contain the coronavirus outbreak has disrupted supply chains. One crucial chain is delivery of information and insight — news and analysis that is fair and accurate and reliably reported from across a nation in quarantine. A voice you can trust amid the clanging of alarm bells. Vajiram & Ravi and The Indian Express are proud to deliver the electronic version of this morning’s edition of The Indian Express to your Inbox. You may follow The Indian Express’s news and analysis through the day on indianexpress.com DAILY FROM: AHMEDABAD, CHANDIGARH, DELHI, JAIPUR, KOLKATA, LUCKNOW, MUMBAI, NAGPUR, PUNE, VADODARA JOURNALISM OF COURAGE SATURDAY, AUGUST 22, 2020, NEW DELHI, LATE CITY, 16 PAGES SINCE 1932 `6.00 (`8 PATNA &RAIPUR, `12 SRINAGAR) WWW.INDIANEXPRESS.COM THE EDITORIAL PAGE OFFICIAL NOTE TO MEA NAGATALKS: BRIDGINGTHE AswithPak, NARRATIVEDIVIDE BY SANJIB BARUAH PAGE 8 selectChina BUSINESSASUSUAL entitiesface BY UNNY extravisascan Official:Tie-ups of Indian universities, institutionsare alsounder review SUSHANTSINGH The fire spread quickly, with smoke enveloping the powerhouse and the four storeysofthe plantthat lie underground, in Srisailam on Thursdaynight. PTI NEWDELHI,AUGUST21 AS SINO-INDIAN relations re- Bihar polls: In main tense following lackof Nine killed in Telangana powerhouse fire progress in talksonresolving the Thesteps, border situation in Ladakh, the EC guidelines, government is placing visasfor thesignal Five engineers among dead,survivors personsconnected to certain last hour of Red flags raised over dam’s poor Chinese think tanks, business EVER SINCE Beijing pre- saytheystayedbacktocontrolfire fora and advocacygroups under cipitated acrisis along voting day for the “requirement of prior the LACinLadakh, Delhi neers, including awoman engi- upkeep, fundscrunch in 2states screening/clearance”. -

230 Th Report T T Culture

REPORT NO. 230 PARLIAMENT OF INDIA RAJYA SABHA DEPARTMENT-RELATED PARLIAMENTARY STANDING COMMITTEE ON TRANSPORT, TOURISM AND CULTURE TWO HUNDRED THIRTIETH REPORT Issues related to Security at Airports in India (Presented to the Rajya Sabha on 21st December, 2015) (Laid on the Table of Lok Sabha on 21st December, 2015) Rajya Sabha Secretariat, New Delhi December, 2015/Agrahayana, 1937 (Saka) Hindi version of this publication is also available PARLIAMENT OF INDIA RAJYA SABHA DEPARTMENT-RELATED PARLIAMENTARY STANDING COMMITTEE ON TRANSPORT, TOURISM AND CULTURE TWO HUNDRED THIRTIETH REPORT Issues related to Security at Airports in India (Presented to the Rajya Sabha on 21st December, 2015) (Laid on the Table of Lok Sabha on 21st December, 2015) Rajya Sabha Secretariat, New Delhi December, 2015/ Agrahayana, 1937 (Saka) Website : http://rajyasabha.nic.in E-mail : [email protected] C O N T E N T S PAGES 1. COMPOSITION OF THE COMMI TEE............................................................................. (i)⎯(ii) 2. INTRODUTION............................................................................................ (iii) 3. ACRNYMS........................................................................................................(iv)⎯(v) 4. REPORT................................................................................................... ....... 23 5. RECOMMENDATIONS/OBSERVATION/CONCLUSIONS-AT A GLANCE....................................24⎯28 6. MINUTES ....................................................................................................... -

The Many Challenges Facing Civil Aviation in India (Robert S

India Law News A quarterly newsletter of the India Committee VOLUME 4, ISSUE 3, FALL ISSUE 2013 THE MANY CHALLENGES FACING CIVIL CIVIL AVIATION IN INDIA—THE VIEW FROM AVIATION IN INDIA 30,000 FEET By Robert S. Metzger By VivekLall ndia has experienced extraordinary growth in ndian aviation has great underlying potential. civil aviation over the past decade and is However, the market continues to under-perform forecast to be on of the world’s largest aviation due to structural issues and the business models markets in just a few years. To achieve (and afford) the of almost all the major carriers are under stress. promise of civil aviation, India faces challenges posed by national and state policies, law, regulation and The fiscal and cost environment in which the civil practice. Crucial questionsare presented to policy aviation sector is operating has turned particularly makers, regulators, business leaders and to lawyers hostile at present as a result of stubbornly high fuel who advise them. prices compounded by a sharp depreciation of the Rupee and a punitive ad valorem sales tax. Civil aviation in India may be taken as a study in contrasts. Despite extraordinary growth in traffic, most There is a need to take a holistic view of the sector of India’s airlines are in a precarious condition. and address concerns of all the stakeholders and all aspects of the civil aviation business. continued on page 8 continued on page 6 SAVE THE DATE (FEBRUARY 13-15, 2014 – NEW DELHI, INDIA) Come join your colleagues from the United States and India, ABA Section of International Law Leadership, ABA Leadership, and Leadership from Major Indian Bar Associations, government officials, and prominent Indian business personalities at a jointly sponsored conference of the American Bar Association Section of International Law India Committee, Society of Indian Law Firms, and the Bar Association of India, as well as the Indian Services Export Promotion Council to be held in New Delhi, India. -

Final Report

Final Report 5 The Economics of Resettling – A Case 0 0 for in Situ Slum Upgradation 2 Centre for Urban and Regional Excellence Director : Dr.Ranu Khosla [email protected] New Delhi www.cureindia.org ANNEXURE I: SAMPLE SIZE ........................................................................................................ 6 ANNEXURE II: DEMOGRAPHIC PROFILE ................................................................................... 7 ANNEXURE III: INCOME................................................................................................................ 8 ANNEXURE IV: EXPENDITURE .................................................................................................. 11 ANNEXURE V: HOUSING ............................................................................................................ 15 ANNEXURE VI: DISTANCE AND TRANSPORTATION.............................................................. 16 ANNEXURE VII: LOANS .............................................................................................................. 17 ANNEXURE VIII: EDUCATION .................................................................................................... 18 ANNEXURE IX: LEVEL OF SERVICE ......................................................................................... 20 ANNEXURE X: POVERTY............................................................................................................ 25 ANNEXURE XI: QUALITATIVE ANALYSIS THROUGH PLA TECHNIQUES ........................... -

{Replace with the Title of Your Dissertation}

Uneven Absorption: World-Class Delhi, Domestic Workers and the Water that Makes Them A DISSERTATION SUBMITTED TO THE FACULTY OF UNIVERSITY OF MINNESOTA BY Heather Elaine O’Leary IN PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR THE DEGREE OF DOCTOR OF PHILOSOPHY William O. Beeman August 2014 © Heather Elaine O’Leary 2014 i Acknowledgements I gratefully acknowledge that this study could not have been completed without the help of my kin—the family I was born into and those who graciously adopted me and this project in countless ways throughout my pursuit of answers. *** Generous support was granted by: Fulbright Foundation United States Department of Education: Foreign Language and Area Studies Program University of Minnesota: Department of Anthropology Graduate School: Graduate Research Partnership Program Interdisciplinary Doctoral Fellowship Program Interdisciplinary Center for the study of Global Change Wenner-Gren Foundation ii Dedication This dissertation is dedicated to P.D. and the women and girls of Delhi; | iii Informants and Name Meanings The names and identifying characteristics of collaborators have been changed to protect their anonymity, unless they wished to be named. The new names all were selected to reflect the cultural background and character of the collaborator. I chose to select common names that have meaning in Hindi, Urdu, Sanskrit, and English that are tied in with the theme of water. Some are direct, like Sanskrit “Jeevika,” which means water, while others like “Anita” derive from Urdu as the name of a goddess of water, but also reflect her role in the community with its Sanskrit meaning “a leader without guile.” Some names, like “Piyush,” are near interpretations of the theme.