The Indian Aviation Sector

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

669419-1 EFFICIENCY of AIRLINES in INDIA ABSTRACT This Paper Measures the Technical Efficiency of Various Airlines Operating In

Natarajan and Jain Efficiency of Airlines in India EFFICIENCY OF AIRLINES IN INDIA Ramachandran Natarajan, College of Business, Tennessee Technological University, Cookeville TN, 38505, U.S.A. E-Mail: [email protected] , Tel: 931-372-3001 and Ravi Kumar Jain, Icfai Business School, IFHE University, Hyderabad-501203 (AP) India. E-Mail: [email protected] , Mobile: 91+94405-71846 ABSTRACT This paper measures the technical efficiency of various airlines operating in India over a ten-year period, 2001-2010. For this, the Input Efficiency Profiling model of DEA along with the standard Data Envelopment Analysis (DEA) is used to gain additional insights. The study period is divided into two sub-periods, 2001-2005 and 2006-2010, to assess if there is any impact on the efficiency of airlines due to the significant entry of private operators. The study includes all airlines, private and publicly owned, both budget and full service, operating in the country offering scheduled services on domestic and international routes. While several studies on efficiency of airlines have been conducted globally, a research gap exists as to similar studies concerning airlines in India. This paper addresses that gap and thus contributes to the literature. Key Words: Airlines in India, DEA analysis, Input efficiency profiling, Productivity analysis, Technical efficiency. Introduction The civil aviation industry in India has come a long way since the Air Corporation Act was repealed in the year 1994 allowing private players to operate in scheduled services category. Several private players showed interest and were granted the status of scheduled carriers in the year 1995. However, many of those private airlines soon shut down. -

Aptech Aviation and Learning Academy Shyambazar Centre

APTECH AVIATION AND LEARNING ACADEMY SHYAMBAZAR CENTRE INDUSTRY CONNECT, ALLIANCES & PLACEMENT (ICAP) ACADEMIC YEAR 2020-21 For queries contact [email protected] / 9831000144 Foreword Aptech Shyambazar ensures that its students get enough guidance to get a job of their choice. The institute has an independent Industry Connect, Alliance and Placement Cell (ICAP) which constantly interacts with the leading recruiters in the corporate world and guides students through their career planning under the guidance and expertise of Aptech Limited. The Industry Connect, Alliance and Placement Cell (ICAP) services include career exploration, skill development, and identification of employment opportunities, job placement and on-going support. Rigorous training and counselling is undertaken regularly to hone on the skills of budding talent and give them the confidence to face the challenges of a corporate world. Imparting theoretical knowledge, developing analytical skills, strengthening communication skills, instilling problem solving and team-work abilities through case studies, research work, presentations etc. are few additional responsibilities of this cell. For queries contact [email protected] / 9831000144 Aptech Aviation and Learning Academy, Shyambazar – The Institute Here are few reasons why you should choose Aptech Aviation & Learning Academy, Shyambazar as your learning hub: Teaching and Management staff are >18 years experienced with the Education Industry Enriched with the latest curriculum Teaching staff is experienced and -

Liste-Exploitants-Aeronefs.Pdf

EN EN EN COMMISSION OF THE EUROPEAN COMMUNITIES Brussels, XXX C(2009) XXX final COMMISSION REGULATION (EC) No xxx/2009 of on the list of aircraft operators which performed an aviation activity listed in Annex I to Directive 2003/87/EC on or after 1 January 2006 specifying the administering Member State for each aircraft operator (Text with EEA relevance) EN EN COMMISSION REGULATION (EC) No xxx/2009 of on the list of aircraft operators which performed an aviation activity listed in Annex I to Directive 2003/87/EC on or after 1 January 2006 specifying the administering Member State for each aircraft operator (Text with EEA relevance) THE COMMISSION OF THE EUROPEAN COMMUNITIES, Having regard to the Treaty establishing the European Community, Having regard to Directive 2003/87/EC of the European Parliament and of the Council of 13 October 2003 establishing a system for greenhouse gas emission allowance trading within the Community and amending Council Directive 96/61/EC1, and in particular Article 18a(3)(a) thereof, Whereas: (1) Directive 2003/87/EC, as amended by Directive 2008/101/EC2, includes aviation activities within the scheme for greenhouse gas emission allowance trading within the Community (hereinafter the "Community scheme"). (2) In order to reduce the administrative burden on aircraft operators, Directive 2003/87/EC provides for one Member State to be responsible for each aircraft operator. Article 18a(1) and (2) of Directive 2003/87/EC contains the provisions governing the assignment of each aircraft operator to its administering Member State. The list of aircraft operators and their administering Member States (hereinafter "the list") should ensure that each operator knows which Member State it will be regulated by and that Member States are clear on which operators they should regulate. -

A 21St Century Powerhouse Dick Forsberg Head of Strategy, Avolon

An in-depth analysis of the Indian air travel market Dick Forsberg | July 2018India A 21st Century Powerhouse Dick Forsberg Head of Strategy, Avolon ACKNOWLEDGEMENTS The author would like to acknowledge FlightGlobal Ascend as the source of the fleet data and OAG, through their Traffic Analyser and Schedules Analyser products, as the source of the airline traffic and capacity data used in this paper. DISCLAIMER This document and any other materials contained in or accompanying this document (collectively, the ‘Materials’) are provided for general information purposes only. The Materials are provided without any guarantee, condition, representation or warranty (express or implied) as to their adequacy, correctness or completeness. Any opinions, estimates, commentary or conclusions contained in the Materials represent the judgement of Avolon as at the date of the Materials and are subject to change without notice. The Materials are not intended to amount to advice on which any reliance should be placed and Avolon disclaims all liability and responsibility arising from any reliance placed on the Materials. Dick Forsberg has over 45 years’ aviation industry experience, working in a variety of roles with airlines, operating lessors, arrangers and capital providers in the disciplines of business strategy, industry analysis and forecasting, asset valuation, portfolio risk management and airline credit assessment. As a founding executive and Head of Strategy at Avolon, his responsibilities include defining the trading cycle of the business, primary interface with the aircraft appraisal and valuation community, industry analysis and forecasting, driving thought leadership initiatives, setting portfolio risk management criteria and determining capital allocation targets. Prior to Avolon, Dick was a founding executive at RBS (now SMBC) Aviation Capital and previously worked with IAMG, GECAS and GPA following a 20-year career in the UK airline industry. -

Competition Issues in the Air Transport Sector in India

2009 StudyStudy on on ImpactCompetition of Trade Issues in Liberalisationthe Domestic in the Information Technology SectorSegment on Development of the Air Draft ReportTransport Sector in Administrative Staff College of India HyderabadIndia Revised Final Report 2007 Administrative Staff College of India, Hyderabad Competition Issues in the Air Transport Sector in India Table of Contents Sl.No Chapter Page No. 1. Introduction 1 2. ToR I 4 3. ToR II & III 15 4. ToR IV 29 5. ToR V 30 6. ToR VI & VII 43 7. ToR VIII 91 8. ToR IX 99 9. ToR X 120 10. ToR XI 121 11. Conclusions and Recommendations 126 12. References 129 ____________________________________________________asci research and consultancy ii Competition Issues in the Air Transport Sector in India List of Tables Table Title Page No. No. I.1 Calculation of HHI 12 I.2 Fleet Size of All Scheduled Airlines 12 I.3 Order for Airplanes 13 I.4 Net Profit/Loss incurred by Different Airlines 16 II.1 City Pair-wise Herfindahl index of Pax. Carried in 2006-07 28 17 II.2 Passenger Load Factor for Indian 22 II.3 Passenger Load Factor for Indian 25 II.4 Slots on Delhi-Mumbai Route 28 II.5 Average Age of Fleet 28 II.6 Fleet Size of All Scheduled Airlines 29 IV.1 Descriptive Statistics for Price Data: Delhi – Mumbai 30 IV.2 Taxes and Surcharges on Route : Delhi – Mumbai 32 IV.3 Taxes and Surcharges on Route : Mumbai – Delhi 32 IV.4 Pre merger (2006/07)-Delhi-Mumbai (passenger wise) 36 IV.5 Post Merger(2008) -Delhi Mumbai (slot wise) 36 IV.6 Pre merger (2006/07)-Delhi-Chennai (passenger wise) 37 IV.7 Post Merger(2008) -Delhi Chennai(slot wise) 37 IV.8 Pre merger (2006/07)-Bangalore-Chennai (passenger wise) 37 IV.9 Post Merger(2008) -Bangalore- Chennai(slot wise) 38 ____________________________________________________asci research and consultancy iii Competition Issues in the Air Transport Sector in India List of Figures Figure Title Page No. -

Management Discussion & Analysis Report

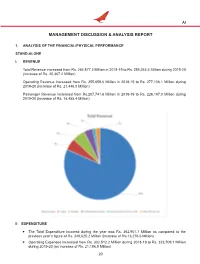

AI MANAGEMENT DISCUSSION & ANALYSIS REPORT 1. ANALYSIS OF THE FINANCIAL/PHYSICAL PERFORMANCE STAND-ALONE I. REVENUE Total Revenue increased from Rs. 264,877.2 Million in 2018-19 to Rs. 285,244.4 Million during 2019-20 (increase of Rs. 20,367.2 Million) Operating Revenue increased from Rs. 255,659.6 Million in 2018-19 to Rs. 277,106.1 Million during 2019-20 (increase of Rs. 21,446.5 Million) Passenger Revenue increased from Rs.207,741.6 Million in 2018-19 to Rs. 226,197.0 Million during 2019-20 (increase of Rs. 18,455.4 Million) II EXPENDITURE The Total Expenditure incurred during the year was Rs. 362,901.7 Million as compared to the previous year’s figure of Rs. 349,625.2 Million (increase of Rs.13,276.5 Million) Operating Expenses increased from Rs. 302,512.2 Million during 2018-19 to Rs. 323,709.1 Million during 2019-20 (an increase of Rs. 21,196.9 Million) 20 AI There was an increase in staff cost by 7% from Rs.30,052.3 Million in 2018-19 to Rs. 32,253.7 Million during 2019-20. Fuel cost decreased by 6% from Rs.100,344.6 Million in 2018-19 to Rs. 93,992.7 Million during 2019-20. Net impact of Rs 20,130.5 Million, due to applicability of “IND AS 116 – LEASES”. CONSOLIDATED I. REVENUE Total Revenue increased from Rs.298,111.5 Million in 2018-19 to Rs.328,306.2 Million during 2019-20, an increase of 10.1%. -

Swift E-Bulletin Edition 22/20-21 Week – December 14Th to December 18Th

Swift e-Bulletin Edition 22/20-21 Week – December 14th to December 18th Quote for the week: "Things work out best for those who make the best of how things work out." - John Wooden Introduction We welcome you to our weekly newsletter! The ‘Swift e-Bulletin’ - weekly newsletter, covers all regulatory updates and critical judgements passed during the week. We hope that you liked our previous editions and found it to be of great value in its content. We want this newsletter to be valuable for you so, please share your feedback and suggestions to help us improve. In the wake of COVID-19, we all are witnessing many relaxations, exemptions and amendments to the various legislations by regulatory authorities to ease out the operations during this time of crisis. Further, various regulatory authorities have been proactive in bringing significant regulatory changes in recent challenging times. This week’s newsletter covers various Circulars/notifications issued by certain regulatory authorities such as, the Ministry of Corporate Affairs (“MCA”), the Securities and Exchange Board of India (“SEBI”) and the Reserve Bank of India (“RBI”), and critical judgements and orders passed by the National Company Law Tribunal (“NCLT”), SEBI, Supreme Court and High Court. We have prepared a comprehensive summary for quick reference of the aforesaid updates and Judgements / orders issued during the week of December 14, 2020 to December 18, 2020. Thank you, Swift Team 1 Table of Contents REGULATORY UPDATES ........................................................................................................ 3 MCA UPDATES ....................................................................................................................... 3 1. MCA amends the Companies (Compromises, Arrangements and Amalgamations) Rules, 2016 vide Gazette Notification dated December 17, 2020 ............................ -

Will Trump Presidency Impact Business Aviation?

A SUPPLEMENT TO REGIONAL CONNECTIVITY SCHEME: UDAN LAUNCHED p3 SP’S AVIATION 11/2016 Volume 2 • issue 4 WWW.SPS-AVIATION.COM/BIZAVINDIASUPPLEMENT Pilatus PC-24 made its first public display of the twinjet at the NBAA 2016 PAGE 18 Will Trump Presidency Impact Business Aviation? VIKING TWIN OTTER SERIES 400 : UNMATCHED COMFORT AND VERSATILITY & PERFORMANCE FLEXIBILITY: LINEAGE 1000E P 12 P 15 CABIN ALTITUDE: 3,255 FT* • PASSENGERS: UP TO 19 • PANORAMIC WINDOWS: 14 OPTIMIZED COMFORT Space where you need it. Comfort throughout. The uniquely shaped cabin of the all-new Gulfstream G500™ is optimized to provide plentiful elbow, shoulder and headroom. The bright and quiet interior is filled with 100 percent fresh air pressurized to a cabin altitude lower than any other business jet. And with the new Gulfstream cabin design process that offers abundant cabin configurations, you can create your own masterpiece. For more information, visit gulfstreamg500.com. +91 98 182 95755 | ROHIT KAPUR [email protected] | Gulfstream Authorized Sales Representative TOLL FREE 1800 103 2003 +65 6572 7777 | JASON AKOVENKO [email protected] | Regional Vice President *At the typical initial cruise altitude of 41,000 ft CONTENTS Volume 2 • issue 4 On the cover: According to Ed Bolen NBAA President and CEO. this year’s NBAA-BACE was a resounding success. He said, “The activity level was high, and the enthusiasm was strong. Equally important, the show provided a reminder of the industry’s size and significance in the US and around the world.” -

Offsetting in the Aviation Sector

Offsetting in the aviation sector Evaluating voluntary offset programs of major airlines Elizabeth Zelljadt 10 October 2016 Contact information Elizabeth Zelljadt Fellow Ecologic Institut E-Mail: [email protected] Tel: (+1) 413 210 8663 Contents Introduction ........................................................................................................................................... 1 1 Context of findings: the need for a transparent, robust registry ............................................ 2 2 Spectrum of initiatives ................................................................................................................. 3 3 Offsetting data – analysis of trends ........................................................................................... 6 3.1 Trends among project types ................................................................................................. 7 3.2 Project overlap – implications for future volumes ................................................................. 9 3.3 Project integrity – implications for future accounting and standardization ......................... 10 3.4 Next steps ........................................................................................................................... 10 4 Offset program and project profiles by carrier ....................................................................... 11 Air France/KLM ........................................................................................................................... -

Strategy Embedded Value of Tata Sons in Group

EQUITY RESEARCH India | Equity Strategy Strategy Exhibit 1 - Value of Tata Group Embedded Value of Tata Sons in Group Cos companies holding in Tata Sons Value of holdings in Tata Sons based Value of holdings in Tata Company Name Market Cap (Rs mn) 6 October 2020 on listed investment (Rs mn) Sons (as % of Mcap) Tata Chemicals 78,478 198,704 253.2 Tata Power 172,069 129,525 75.3 The Indian Hotels Company 120,353 87,347 72.6 Key Takeaway Tata Steel 434,912 240,203 55.2 Tata Motors 445,242 240,203 53.9 Financial troubles at the Shapoorji Palanji (SP) group, which holds an 18% stake in . Tata Consumer Products 463,754 34,065 7.3 Source: Company annual reports, Jefferies Tata Sons – the group hold co – has triggered debate on Tata Sons' worth. Tata Sons’ holdings across 14 listed cos works out to US$100bn+. SP group's reported asking price is c.20% higher. Several listed Tata group cos hold a stake in Tata Sons. For Tata Chem, Indian Hotels, Tata Power, Tata Steel and Tamo the value of investment in Tata Sons is more than 50% of the market cap. This report is intended for [email protected]. Unauthorized distribution prohibited. Stress at the SP group prompting likely Tata Sons breakup. The SP group's weak liquidity situation was made clear recently when on 25th Sep'20 it defaulted on a Union Bank owned Rs2bn commercial paper. Earlier, the group had tried to pledge part of its 18.4% shareholding in Tata Sons to shore up funding for its own businesses; but the same was stayed by the Supreme court (next hearing 28th October). -

Govt Unlikely to Trim GST on Automobiles

FRIDAY • AUGUST 27, 2021 MUMBAI ₹10 • Pages 10 • Volume 28 • Number 238 AUTO FOCUS DATA FOCUS RAISING THE RED FLAG On the 50th anniversary of the Covidrelated health claims in just the The independent auditors of Tata Sons original Countach, Lamborghini’s first five months of FY22 have already have expressed concerns over AirAsia futuristic hybrid makes its debut p7 topped claims of whole of FY21 p2 India’s ability to sustain as a going concern p2 Bengaluru Chennai Coimbatore Hubballi Hyderabad Kochi Kolkata Madurai Malappuram Mangaluru Mumbai Noida Thiruvananthapuram Tiruchirapalli Tirupati Vijayawada Visakhapatnam Regd. TN/ARD/14/09-11, RNI No. 55320/94 Boeing MAX 737 HIGHER FAMILY PENSION, NPS Govt unlikely to trim to fly again in India PSBs to make ₹21,300crore OUR BUREAU New Delhi, August 26 The DirectorateGeneral of GST on automobiles Civil Aviation (DGCA) on additional provision yearly Top official says sop Thursday allowed Boeing MAX8 aircraft to fly again in To soften impact, not needed as sales the country. On account of two have picked up, no fatal accidents, the regulator will seek special RBI had halted operation of this dispensation to inventory buildup type of planes with effect from March 2019. spread it over 5 years OUR BUREAU As on date, SpiceJet is the New Delhi, August 26 only Indian carrier using Boe SHISHIR SINHA The government is unlikely to ing 737 MAXaircraft; it has 13 in New Delhi, August 26 ation of the 11 th bipartite set 2018, it was decided that for a oblige any time soon the auto Tax burden a singleclass configuration Public sector banks will have tlement on wage revision of Central government em mobile industry’s demand for each with capacity to carry 189 to set aside an additional public sector bank employ ployee, the mandatory con ■ lowering the Goods & Services All automobiles attract GST between 18% and 28% passengers. -

Public Disclosures March 2021 -Breaklink.Xlsx

PERIODIC DISCLOSURES FORM NL-31 RELATED PARTY TRANSACTIONS TATA AIG GENERAL INSURANCE COMPANY LIMITED IRDAI Registration No. 108, dated January 22, 2001 ( ₹ in Lakhs) CONSIDERATION PAID / RECEIVED NATURE OF RELATIONSHIP WITH CORRESPONDING UP TO THE SL.NO. NAME OF THE RELATED PARTY DESCRIPTION OF TRANSACTION FOR THE UP TO THE THE COMPANY QUARTER OF THE QUARTER OF THE QUARTER QUARTER PRECEEDING YEAR PRECEEDING YEAR 1 AIG MEA INVESTMENTS AND SERVICES LLC JOINT VENTURE PROMOTER SHARE CAPITAL RECEIVED - - - 2,261 2 AIG MEA INVESTMENTS AND SERVICES LLC JOINT VENTURE PROMOTER SECURITIES PREMIUM RECEIVED - - - 2,939 3 AirAsia (India) Limited FELLOW SUBSIDIARIES PREMIUM BOOKED 5 6 0 0 4 ARROW INFRAESTATE PRIVATE LIMITED FELLOW SUBSIDIARIES PREMIUM BOOKED - 4 - - 5 AURORA INTEGRATED SYSTEM PRIVATE LIMITED FELLOW SUBSIDIARIES PREMIUM BOOKED 0 1 0 1 6 DHARAMSHALA ROPEWAY LIMITED FELLOW SUBSIDIARIES PREMIUM BOOKED - 22 10 21 7 EWART INVESTMENTS LIMITED FELLOW SUBSIDIARIES PREMIUM BOOKED 4 4 3 3 8 GURGAON CONSTRUCT WELL PRIVATE LIMITED FELLOW SUBSIDIARIES PREMIUM BOOKED - 2 - - 9 GURGAON REALTECH LIMITED FELLOW SUBSIDIARIES PREMIUM BOOKED 9 23 5 20 10 INFINITI RETAIL LIMITED FELLOW SUBSIDIARIES CLAIMS INCURRED 190 257 17 205 11 INFINITI RETAIL LIMITED FELLOW SUBSIDIARIES PREMIUM BOOKED 129 133 442 621 12 INTERNATIONAL INFRABUILD PRIVATE LIMITED FELLOW SUBSIDIARIES PREMIUM BOOKED - 7 - - 13 INTERNATIONAL INFRABUILD PRIVATE LIMITED FELLOW SUBSIDIARIES CLAIMS INCURRED 1 1 - - 14 KRIDAY REALTY PRIVATE LIMITED FELLOW SUBSIDIARIES PREMIUM BOOKED - 1 0 1 15 TATA ADVANCED SYSTEMS LIMITED FELLOW SUBSIDIARIES AMOUNT DUE TO THE ENTITY 0 1 - - 16 MMP MOBI WALLET PAYMENT SYSTEMS LIMITED (W.E.F. 02.02.2017) FELLOW SUBSIDIARIES COST OF SERVICES - - - (0) 17 MMP MOBI WALLET PAYMENT SYSTEMS LIMITED (W.E.F.