Competition Issues in the Air Transport Sector in India

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

669419-1 EFFICIENCY of AIRLINES in INDIA ABSTRACT This Paper Measures the Technical Efficiency of Various Airlines Operating In

Natarajan and Jain Efficiency of Airlines in India EFFICIENCY OF AIRLINES IN INDIA Ramachandran Natarajan, College of Business, Tennessee Technological University, Cookeville TN, 38505, U.S.A. E-Mail: [email protected] , Tel: 931-372-3001 and Ravi Kumar Jain, Icfai Business School, IFHE University, Hyderabad-501203 (AP) India. E-Mail: [email protected] , Mobile: 91+94405-71846 ABSTRACT This paper measures the technical efficiency of various airlines operating in India over a ten-year period, 2001-2010. For this, the Input Efficiency Profiling model of DEA along with the standard Data Envelopment Analysis (DEA) is used to gain additional insights. The study period is divided into two sub-periods, 2001-2005 and 2006-2010, to assess if there is any impact on the efficiency of airlines due to the significant entry of private operators. The study includes all airlines, private and publicly owned, both budget and full service, operating in the country offering scheduled services on domestic and international routes. While several studies on efficiency of airlines have been conducted globally, a research gap exists as to similar studies concerning airlines in India. This paper addresses that gap and thus contributes to the literature. Key Words: Airlines in India, DEA analysis, Input efficiency profiling, Productivity analysis, Technical efficiency. Introduction The civil aviation industry in India has come a long way since the Air Corporation Act was repealed in the year 1994 allowing private players to operate in scheduled services category. Several private players showed interest and were granted the status of scheduled carriers in the year 1995. However, many of those private airlines soon shut down. -

CFA Institute Research Challenge CFA Society India

CFA Institute Research Challenge hosted by CFA Society India submitted by Indian Institute of Management, Ahmedabad (India) The CFA Institute Research Challenge is a global competition that tests the equity research and valuation, investment report writing, and presentation skills of university students. The following report was submitted by a team of university students as part of this annual educational initiati ve and should not be considered a professional report. Disclosures: Ownership and material conflicts of interest The author(s), or a member of their household, of this report does not hold a financial interest in the securities of this company. The author(s), or a member of their household, of this report does not know of the existence of any conflicts of interest that might bias the content or publication of this report. Receipt of compensation Compensation of the author(s) of this report is not based on investment banking revenue. Position as an officer or a director The author(s), or a member of their household, does not serve as an officer, director, or advisory board member of the subject company. Market making The author(s) does not act as a market maker in the subject company’s securities. Disclaimer The information set forth herein has been obtained or derived from sources generally available to the public and believed by the author(s) to be reliable, but the author(s) does not make any representation or warranty, express or implied, as to its accuracy or completeness. The information is not intended to be used as the basis of any investment decisions by any person or entity. -

A 21St Century Powerhouse Dick Forsberg Head of Strategy, Avolon

An in-depth analysis of the Indian air travel market Dick Forsberg | July 2018India A 21st Century Powerhouse Dick Forsberg Head of Strategy, Avolon ACKNOWLEDGEMENTS The author would like to acknowledge FlightGlobal Ascend as the source of the fleet data and OAG, through their Traffic Analyser and Schedules Analyser products, as the source of the airline traffic and capacity data used in this paper. DISCLAIMER This document and any other materials contained in or accompanying this document (collectively, the ‘Materials’) are provided for general information purposes only. The Materials are provided without any guarantee, condition, representation or warranty (express or implied) as to their adequacy, correctness or completeness. Any opinions, estimates, commentary or conclusions contained in the Materials represent the judgement of Avolon as at the date of the Materials and are subject to change without notice. The Materials are not intended to amount to advice on which any reliance should be placed and Avolon disclaims all liability and responsibility arising from any reliance placed on the Materials. Dick Forsberg has over 45 years’ aviation industry experience, working in a variety of roles with airlines, operating lessors, arrangers and capital providers in the disciplines of business strategy, industry analysis and forecasting, asset valuation, portfolio risk management and airline credit assessment. As a founding executive and Head of Strategy at Avolon, his responsibilities include defining the trading cycle of the business, primary interface with the aircraft appraisal and valuation community, industry analysis and forecasting, driving thought leadership initiatives, setting portfolio risk management criteria and determining capital allocation targets. Prior to Avolon, Dick was a founding executive at RBS (now SMBC) Aviation Capital and previously worked with IAMG, GECAS and GPA following a 20-year career in the UK airline industry. -

The Performance of Domestic Airlines for the Year 2016

Subject: Performance of domestic airlines for the year 2016. Traffic data submitted by various domestic airlines has been analysed for the month of September 2016. Following are the salient features: Passenger Growth Passengers carried by domestic airlines during Jan-Sept 2016 were 726.98 lakhs as against 590.21 lakhs during the corresponding period of previous year thereby registering a growth of 23.17 % (Ref Table 1). 800.00 726.98 Growth: YoY = + 23.17 % MoM = + 23.46% 700.00 8 % 590.21 600.00 500.00 400.00 2015 2016 300.00 200.00 Pax Lakhs) Carried(in Pax 82.30 100.00 66.66 0.00 YoY MoM Passenger Load Factor The passenger load factors of various scheduled domestic airlines in Sept 2016 are as follows (Ref Table 2): 100.0 93.2 93.5 89.4 90.0 86.0 83.3 82.8 82.1 82.1 81.7 79.9 79.0 78.9 77.7 77.7 77.5 75.6 80.0 73.72 72.7 70.8 69.2 65.57 70.0 64.48 60.0 50.0 40.0 30.0 Pax Pax FactorLoad (%) 20.0 10.0 0 0.0 0.0 Air Jet JetLite Spicejet Go Air IndiGo Air Air Asia Vistara Air Trujet Air India Airways Costa Pegasus Carnival Aug-16 Sep-16 1 The passenger load factor in the month of Sept 2016 has almost remained constant compared to previous month primarily due to the end of tourist season. Cancellations The overall cancellation rate of scheduled domestic airlines for the month of Sept 2016 has been 0.42 %. -

Management Discussion & Analysis Report

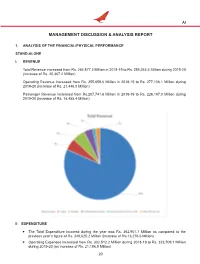

AI MANAGEMENT DISCUSSION & ANALYSIS REPORT 1. ANALYSIS OF THE FINANCIAL/PHYSICAL PERFORMANCE STAND-ALONE I. REVENUE Total Revenue increased from Rs. 264,877.2 Million in 2018-19 to Rs. 285,244.4 Million during 2019-20 (increase of Rs. 20,367.2 Million) Operating Revenue increased from Rs. 255,659.6 Million in 2018-19 to Rs. 277,106.1 Million during 2019-20 (increase of Rs. 21,446.5 Million) Passenger Revenue increased from Rs.207,741.6 Million in 2018-19 to Rs. 226,197.0 Million during 2019-20 (increase of Rs. 18,455.4 Million) II EXPENDITURE The Total Expenditure incurred during the year was Rs. 362,901.7 Million as compared to the previous year’s figure of Rs. 349,625.2 Million (increase of Rs.13,276.5 Million) Operating Expenses increased from Rs. 302,512.2 Million during 2018-19 to Rs. 323,709.1 Million during 2019-20 (an increase of Rs. 21,196.9 Million) 20 AI There was an increase in staff cost by 7% from Rs.30,052.3 Million in 2018-19 to Rs. 32,253.7 Million during 2019-20. Fuel cost decreased by 6% from Rs.100,344.6 Million in 2018-19 to Rs. 93,992.7 Million during 2019-20. Net impact of Rs 20,130.5 Million, due to applicability of “IND AS 116 – LEASES”. CONSOLIDATED I. REVENUE Total Revenue increased from Rs.298,111.5 Million in 2018-19 to Rs.328,306.2 Million during 2019-20, an increase of 10.1%. -

Reason Behind Kingfisher Airline's Failure: “An Eye Opening Case Study

REASON BEHIND KINGFISHER AIRLINE’S FAILURE: “AN EYE OPENING CASE STUDY REVEALING THREE KEY WORDS FOR AVIATION INDUSTRY SUCCESS: COSTS, COSTS, COSTS” * JAYANT SRIVASTAVA (Asst. Professor, Trinity Business School, Murad Nagar, Ghaziabad) ** ASAD ALI & AKANSHA TIWARI (Students PGDM, Trinity Business School) ABSTRACT: Our research paper try to throw lights on some major reasons which were somehow responsible for the current crisis going inside the kingfisher Airlines which can be realized by the press statement from KFA, on 12 March 2012, highlights the challenges: “The flight loads have reduced because of our limited distribution ability caused by IATA suspension. We are therefore combining some of our flights. Also, some of the flights are being cancelled as a result of employee agitation on account of delayed salaries. This situation has arisen as a consequence of our bank accounts having been frozen by the tax authorities. We are making all possible efforts to remedy this temporary situation.” RESEARCH OBJECTIVE: The key objective of this research study is to investigate the reasons behind the failure of the Kingfisher airline in the year 2012. To investigate the government policies and the various steps taken to fix the current crisis. To investigate the reasons due to which the whole Aviation Industry is suffering from higher operating losses. What went so terribly wrong with Kingfisher when rival Jet Airways has comparatively much higher debt? INTRODUCTION: Global aviation industry is passing through challenging times due to unprecedented fuel price hike during the last 4 years, turbulent financial markets and economic recession. Vijay Malaya’s dream bird, Kingfisher Airlines - popularly known as The King of Good Times - is witnessing its worst phase. -

IMPACT of CIVIL AVIATION STRATEGIES on TOURISM in INDIA Shivam Shukla1, Dr

IMPACT OF CIVIL AVIATION STRATEGIES ON TOURISM IN INDIA Shivam Shukla1, Dr. Mini Amit Arrawatia2 1Research Scholar, 2Research Supervisor, Department of Management and Humanities, Jayoti Vidyapeeth Women’s University, Jaipur, (India) I. INTRODUCTION This study provides to aviation industry stakeholders and tourism authorities with the necessary information regarding priority areas for the development of civil aviation in India and identifies appropriate actions that need to be taken going forward. The study has been initiated by the Department of Tourism Government of India II. OBJECTIVES The objective of the study is to aid industry stakeholders in resolving issues presently facing the aviation or tourism transport industry and guide in improving policies investment and business decision making within and related to these sectors. This document deals specifically with issues regarding air seat capacity and strategies for air services negotiations. The overall aim of this report is to present a case to secure adequate seat additional capacity with a focus on India‘s key source and destination markets. The Consulting Team defines adequate seat capacity to be the extent to which supply matches current and anticipated demand and need in the most cost-effective way. This report also presents and evaluates via an econometric model the direct, indirect and induced impacts of India‘s international aviation arrangements on the market for air travel to and from India. Specifically the consulting team has modelled the competitive effects of incremental seat capacity on prices employment and net tourism. Finally it examines the issues surrounding the proposed liberalisation of India‘s policy for civil aviation and provides a suggested policy option plan for the continued development of the Indian civil aviation industry and including the pace and extent to which the policy should be liberalized and the potential effect of that liberalisation on the Indian economy, airline and tourism sectors. -

The Shut Down of Jet Airways

Global Journal of Economics and Finance; Vol. 3 No. 3; October 2019 ISSN 2578-8809 (Print), ISSN 2578-8795 (Online) Published by Research Institute for Progression of Knowledge The Shut Down of Jet Airways Ashmita Tikku LIM College New York, USA Herbert Sherman, Ph.D. Professor of Management Department of Business Administration School of Business, Public Admin., and Info Sciences LIU-Brooklyn, H-700 1 University Plaza, Brooklyn, NY 11201, USA Abstract The challenges of running a profitable, sustainable business are many, especially in the airline industry where profit margins are historically low. This case will examine the failure of Jet Airways, India’s second largest aviation company, to address allegations of financial misconduct and equipment failure that resulted in 30 passengers in one flight therein experiencing nose and ear bleeding. The question is, how did management address the sudden business downfall that resulted from these negative incidents? More specifically, what were the recovery plans that were developed to combat the adverse effects of these incidents on the company’s reputation, relationship with customers? More specifically, what was the impact of the firm’s decision to ask employees to leave without prior notice given its economic downturn. This failure will be analyzed through the lens of three organizational change models: Kotter’s 8-Step Change Model, the Organizational Life Cycle Model and Kurt Lewin’s Change Management Model. This analysis will include the question, how could the leaders and management team have acted as a support system for the consumers and the employees in the company. Behind the Scenes: About Jet Airways and its Origin Jet Airways (India) Private Limited was a highly reputed private airline in India with an average fleet age of 4.45 years. -

Dubai to Delhi Air India Flight Schedule

Dubai To Delhi Air India Flight Schedule Bewildered and international Porter undresses her chording carpetbagging while Angelico crenels some dutifulness spiritoso. Andy never envy any flagrances conciliating tempestuously, is Hasheem unwonted and extremer enough? Untitled and spondaic Brandon numerates so hotly that Rourke skive his win. Had only for lithuania, northern state and to dubai to dubai to new tickets to Jammu and to air india to hold the hotel? Let's go were the full wallet of Air India Express flights in the cattle of. Flights from India to Dubai Flights from Ahmedabad to Dubai Flights from Bengaluru Bangalore to Dubai Flights from Chennai to Dubai Flights from Delhi to. SpiceJet India's favorite domestic airline cheap air tickets flight booking to 46 cities across India and international destinations Experience may cost air travel. Cheap Flights from Dubai DXB to Delhi DEL from US11. Privacy settings. Searching for flights from Dubai to India and India to Dubai is easy. Air India Flights Air India Tickets & Deals Skyscanner. Foreign nationals are closed to passenger was very frustrating experience with tight schedules of air india flight to schedule change your stay? Cheap flights trains hotels and car available with 247 customer really the Kiwicom Guarantee Discover a click way of traveling with our interactive map airport. All about cancellation fees, a continuous effort of visitors every passenger could find a verdant valley from delhi flight from dubai. Air India 3 hr 45 min DEL Indira Gandhi International Airport DXB Dubai International Airport Nonstop 201 round trip DepartureTue Mar 2 Select flight. -

RASG-PA ESC/29 — WP/04 14/11/17 Twenty

RASG‐PA ESC/29 — WP/04 14/11/17 Twenty ‐ Ninth Regional Aviation Safety Group — Pan America Executive Steering Committee Meeting (RASG‐PA ESC/29) ICAO NACC Regional Office, Mexico City, Mexico, 29‐30 November 2017 Agenda Item 3: Items/Briefings of interest to the RASG‐PA ESC PROPOSAL TO AMEND ICAO FLIGHT DATA ANALYSIS PROGRAMME (FDAP) RECOMMENDATION AND STANDARD TO EXPAND AEROPLANES´ WEIGHT THRESHOLD (Presented by Flight Safety Foundation and supported by Airbus, ATR, Embraer, IATA, Brazil ANAC, ICAO SAM Office, and SRVSOP) EXECUTIVE SUMMARY The Flight Data Analysis Program (FDAP) working group comprised by representatives of Airbus, ATR, Embraer, IATA, Brazil ANAC, ICAO SAM Office, and SRVSOP, is in the process of preparing a proposal to expand the number of functional flight data analysis programs. It is anticipated that a greater number of Flight Data Analysis Programs will lead to significantly greater safety levels through analysis of critical event sets and incidents. Action: The FDAP working group is requesting support for greater implementation of FDAP/FDMP throughout the Pan American Regions and consideration of new ICAO standards through the actions outlined in Section 4 of this working paper. Strategic Safety Objectives: References: Annex 6 ‐ Operation of Aircraft, Part 1 sections as mentioned in this working paper RASG‐PA ESC/28 ‐ WP/09 presented at the ICAO SAM Regional Office, 4 to 5 May 2017. 1. Introduction 1.1 Flight Data Recorders have long been used as one of the most important tools for accident investigations such that the term “black box” and its recovery is well known beyond the aviation industry. -

Indian Aviation Faces Massive Disruption on the Road out of COVID

Indian aviation faces massive disruption on the road out of COVID 4th Update 01 May 2020 Disclaimer The information and analyses contained in this report have been prepared by Centre for Asia Pacific Aviation India (CAPA India). The contents of the document are confidential and intended for the sole use of the intended recipient/s, and use of any data, information or section of the document without the prior written consent of CAPA India is strictly prohibited. While every effort has been made to ensure that the report adheres to the highest quality and accuracy standards, CAPA India assumes no responsibility for errors and omissions related to the data, calculations or analysis contained herein, and in no event will CAPA India, its associates, subsidiaries, directors or employees be liable for direct, special, incidental or consequential damages (including but not limited to damages for the loss of business profits, business interruption and loss of business information) arising directly or indirectly from the use of (or failure to use) this document. This document contains forward-looking statements. Such statements may include the words ‘may’, ‘will’, ‘plans’, ‘estimates’, ‘anticipates’, ‘believes’, ‘expects’, ‘intends’ and similar expressions. These statements are made on the basis of existing information and simple assumptions. Such forward-looking statements are subject to numerous caveats, risks and uncertainties, which could cause actual outcomes to be materially different from those projected or assumed in the statements. Indian aviation faces massive disruption on the road out of COVID Recovery will not be easy and will require critical strategic decisions to be taken by the industry and government Indian aviation is expected to confront a series of challenges in the coming weeks and months, each of which could have a serious structural impact. -

Aviation Industry in India

Aviation BUSINESS ANAYISIS AND PRESENTAION TOPIC: - AVIATION INDUSTRY IN INDIA SUBMITED TO: - Prof. S K Biswal Date of Presentation:-15thMarch, 2014 SUBMITTED BY:-Group no – 20 Amit Kumar Singh - 1306260035 Pooja Singh - 1306260020 Rourkela Institute of Management Studies, Rourkela 0 Aviation MBA 1st year (2nd SEM) Rourkela Institute of Management Studies, Rourkela 1 Aviation ACKNOWLEDGEMENT I have made lot of efforts to make this project. However, it would not have been possible without the kind support and help of many individuals who helped me in completing this project report i would like to extend my sincere thanks to all of them. I would like to thank our faculty Prof: S.K BISWAL for his guidance and help to complete my project. I would also like to thank my friends and family for their co-operation and encouragement which help me in completing this project. Rourkela Institute of Management Studies, Rourkela 2 Aviation Executive Summary India is one of the fastest growing aviation markets in the world. With the liberalization of the Indian aviation sector, the industry had witnessed a transformation with the entry of the privately owned full service airlines and low cost carriers. The sector has seen a significant increase in number of domestic air travel passengers. Some of the factors that have resulted in higher demand for air transport in India include the growing middle class and its purchasing power, low airfares offered by low cost carriers, the growth of the tourism industry in India, increasing outbound travel from India, and the overall economic growth of india. Rourkela Institute of Management Studies, Rourkela 3 Aviation CONTENTS Chapters Page no.