Cash Flow 84 $ M 62

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

INFIGEN ENERGY Appendix 4D – Half Year Report 31 December 2017

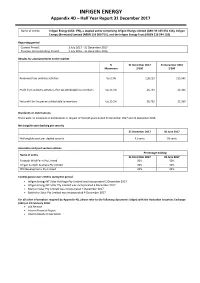

INFIGEN ENERGY Appendix 4D – Half Year Report 31 December 2017 Name of entity: Infigen Energy (ASX: IFN), a stapled entity comprising Infigen Energy Limited (ABN 39 105 051 616), Infigen Energy (Bermuda) Limited (ARBN 116 360 715), and the Infigen Energy Trust (ARSN 116 244 118) Reporting period Current Period: 1 July 2017 ‐ 31 December 2017 Previous Corresponding Period: 1 July 2016 ‐ 31 December 2016 Results for announcement to the market % 31 December 2017 31 December 2016 Movement $’000 $’000 Revenues from ordinary activities Up 2.5% 118,213 115,365 Profit from ordinary activities after tax attributable to members Up 25.1% 26,733 21,366 Net profit for the period attributable to members Up 25.1% 26,733 21,366 Dividends or distributions There were no dividends or distributions in respect of the half‐years ended 31 December 2017 and 31 December 2016. Net tangible asset backing per security 31 December 2017 30 June 2017 Net tangible asset per stapled security 41 cents 38 cents Associates and joint venture entities Percentage holding Name of entity 31 December 2017 30 June 2017 Forsayth Wind Farm Pty Limited 50% 50% Infigen Suntech Australia Pty Limited 50% 50% RPV Developments Pty Limited 32% 32% Control gained over entities during the period Infigen Energy NT Solar Holdings Pty Limited was incorporated 1 December 2017 Infigen Energy NT Solar Pty Limited was incorporated 4 December 2017 Manton Solar Pty Limited was incorporated 4 December 2017 Batchelor Solar Pty Limited was incorporated 4 December 2017 For all other information required -

Infigen Energy 2012 Annual Report and Agm Notice of Meeting

12 October 2012 INFIGEN ENERGY 2012 ANNUAL REPORT AND AGM NOTICE OF MEETING Infigen Energy (ASX: IFN) advises that the attached 2012 Annual Report and the Notice of Meeting relating to the Annual General Meetings of Infigen Energy to be held on Thursday, 15 November 2012, are being despatched to securityholders today. The 2012 Annual Report and AGM Notice of Meeting are also available at Infigen’s website (www.infigenenergy.com). ENDS For further information please contact: Richard Farrell, Investor Relations Manager Tel +61 2 8031 9900 About Infigen Energy Infigen Energy is a specialist renewable energy business. We have interests in 24 wind farms across Australia and the United States. With a total installed capacity in excess of 1,600MW (on an equity interest basis), we currently generate enough renewable energy per year to power over half a million households. As a fully integrated renewable energy business in Australia, we develop, build, own and operate energy generation assets and directly manage the sale of the electricity that we produce to a range of customers in the wholesale market. Infigen Energy trades on the Australian Securities Exchange under the code IFN. For further information please visit our website: www.infigenenergy.com INFIGEN ENERGY OUR GENERATION, YOUR FUTURE Annual Report 2012 INFIGEN ENERGY ANNUAL REPORT 2012 OUR GENERATION CONTINUES TO CONTRIBUTE TO THE TRANSITION TO LOW CARBON EMISSION ELECTRICITY, for yoUR FUTURE AND FUTURE GENERATIONS MIKE HUTCHINSON Chairman 1 INFIGEN ENERGY We strive to be recognised as the leading provider of renewable energy. We want to make a positive difference. Our focus is on customer needs. -

Infigen Energy Annual Report 2018

Annual Report 2019. Infigen Energy Image: Capital Wind Farm, NSW Front page: Run With The Wind, Woodlawn Wind Farm, NSW Contents. 4 About Infigen Energy 7 2019 Highlights 9 Safety 11 Chairman & Managing Director’s Report Directors’ Report 16 Operating & Financial Review 31 Sustainability Highlights 34 Corporate Structure 35 Directors 38 Executive Directors & Management Team 40 Remuneration Report 54 Other Disclosures 56 Auditor’s Independence Declaration 57 Financial Report 91 Directors’ Declaration 92 Auditor’s Report Additional Information 9 Investor Information 8 10 Glossary 1 10 4 Corporate Directory Infigen Energy Limited ACN 105 051 616 Infigen Energy Trust ARSN 116 244 118 Registered office Level 17, 56 Pitt Street Sydney NSW 2000 Australia +61 2 8031 9900 www.infigenenergy.com 2 Our Strategy. We generate and source renewable energy. We add value by firming. We provide customers with reliable clean energy. 3 About Infigen Energy. Infigen is leading Australia’s transition to a clean energy future. Infigen generates and sources renewable energy, increases the value of intermittent renewables by firming, and provides customers with clean, reliable and competitively priced energy solutions. Infigen generates renewable energy from its owned wind farms in New South Wales (NSW), South Australia (SA) and Western Australia (WA). Infigen also sources renewable energy from third party renewable projects under its ‘Capital Lite’ strategy. Infigen increases the value of intermittent renewables by firming them from the Smithfield Open Cycle Gas Turbine facility in Western Sydney, NSW, and its 25MW/52MWh Battery at Lake Bonney, SA, where commercial operations are expected to commence in H1FY20. Infigen’s energy retailing licences are held in the National Electricity Market (NEM) regions of Queensland, New South Wales (including the Australian Capital Territory), Victoria and South Australia. -

Reliability Impacts of Increased Wind Generation in the Australian National Electricity Grid

Reliability Impacts of Increased Wind Generation in the Australian National Electricity Grid Mehdi Mosadeghy B.Sc., M.Sc. A thesis submitted for the degree of Doctor of Philosophy at The University of Queensland in 2015 School of Information Technology and Electrical Engineering Abstract Wind power penetration has been consistently growing and it has been rapidly becoming a significant generation technology in many countries. However, the intermittent and variable nature of wind energy is a major barrier in wind power commitment. Wind speed fluctuations and unpredictability can affect the operation and reliability of power systems. Therefore, the impact of integrating large volume of wind generators on the system reliability needs to be carefully investigated and the reliability contributions of wind farms require to be evaluated for better integration of wind energy sources. Because of intermittency and variability of wind energy, conventional reliability evaluation methods are not applicable and different techniques have been developed to model wind generators. However, most of these methods are time-consuming or may not be able to capture time dependency and correlations between renewable resources and load. Therefore, this research intends to improve the existing reliability methods and proposes a faster and simpler approach. In this approach, wind power and electricity demand are being modelled as time-dependent clusters, which not only can capture their time-dependent attributes, but also is able to keep the correlations between the data sets. To illustrate the effectiveness of this framework, the proposed methodology has been applied to the IEEE reliability test system. In addition, the developed technique is validated by comparing results with the sequential Monte Carlo technique. -

Capital Wind Farm 2 Pty Limited

Capital 2 Wind Farm - Modification No. 4 (MP 10_0135 MOD 4) Response to Submissions 1. INTRODUCTION Capital Wind Farm 2 Pty Ltd (CWF2PL), the proponent of the approved Capital 2 Wind Farm, forms part of the Infigen Group (Infigen). The approved Capital 2 Wind Farm (Approved Project) is located in the New South Wales (NSW) Southern Tablelands, approximately 17 kilometres (km) north-east of the Bungendore township. The Capital 2 Wind Farm will include up to 41 wind turbines, each with up to 3.5 Megawatt (MW) capacity, and associated infrastructure. The approved Capital 2 Wind Farm is in close proximity to Infigen’s existing Capital and Woodlawn Wind Farms. Project Approval for the Capital 2 Wind Farm was granted to CWF2PL on 1 November 2011 under Part 3A of the NSW Environmental Planning and Assessment Act 1979 (EP&A Act). Modification 4 seeks approval to extend the project approval for a further 5 years, for the reasons outlined in the Modification 4 application which was lodged with the Department of Planning and Environment (DPE) on the 16th of September 2016. The DPE publicly exhibited the Modification 4 application for the Capital 2 Wind Farm (MP10_0135 MOD 4) from Friday 23rd September 2016 to Monday 10th October 2016. The exhibition was advertised in local and regional newspapers, and the Modification application was made available on the DPE's website, and at the following locations: The Department of Planning and Environment: o Information Centre, 23-33 Bridge Street, Sydney, until 30 September 2016; o Information Centre 320 Pitt Street, Sydney, from 4 October 2016; Queanbeyan-Palerang Regional Council: o Bungendore office; o Queanbeyan office; and The Nature Conservation Council. -

Roadmap to QRET ANEM NEM Nodal Modelling Report Final

Centre for Policy Futures 31 July 2020 National electricity market nodal modelling final report 2020 Dr Phillip Wild, Centre for Policy Futures University of Queensland Contents Executive Overview .............................................................................................................................. 5 1 Introduction ........................................................................................................................................ 8 2 Scope and Objectives of the Electricity Market Modelling Project ............................................... 9 2.1 Research Question ......................................................................................................................... 9 2.2 Rationale for Research Question .................................................................................................. 9 2.2.1 Complexity of implementation of Queensland’s Renewable Energy Target. ................................. 9 2.2.2 Existing modelling shortcomings .................................................................................................... 9 2.3 Research proposal ........................................................................................................................ 10 3 Wholesale market modelling approach ......................................................................................... 11 3.1 ANEM model .................................................................................................................................. 11 3.2 -

Infigen Energy Annual Report 2017

INFIGEN ENERGY ANNUAL REPORT 2017 Infigen Energy Level 17, 56 Pitt Street Sydney NSW 2000 Australia +61 2 8031 9900 www.infigenenergy.com CONTENTS About 3 Infigen Energy 3 2017 Highlights 5 Chairman and Managing Director’s Report 7 Management 10 Corporate Structure 12 Directors’ Report 13 Directors 13 Operating and Financial Review 18 Remuneration Report 33 Other Disclosures 48 Auditor’s Independence Declaration 50 Financial Report 51 Directors’ Declaration 117 Auditor’s Report 118 Governance 125 Additional Information 129 Investor Information 129 Glossary 134 Corporate Directory 135 2 INFIGEN ENERGY 2017 ANNUAL REPORT ABOUT INFIGEN ENERGY Infigen Energy (Infigen) is an active participant in the Australian energy market. It is a developer, owner and operator of generation assets delivering energy solutions to Australian businesses and large retailers. Infigen has 557 MW of installed generation capacity across New South Wales, South Australia and Western Australia with a further 113 MW under construction in New South Wales. It sells the electricity and Large-scale Generation Certificates through a combination of medium and long-term contracts and through the spot market. Infigen is looking to diversify and expand its customer base and will grow its generation portfolio in response to strong price and investment signals. In the short term it is targeting expansion in New South Wales and entry into the Victorian and Queensland regions of the National Electricity Market. “Infigen is transitioning to a business that seeks to deliver a range of products and solutions to different customers and balance risk, price and tenor. Delivery of this strategy will be supported by a portfolio of supply options that includes existing and new generation, long-term offtake agreements with third parties, and acquiring physical and financial firming products. -

Infigen's Customers and Markets

INFIGEN’S CUSTOMERS AND MARKETS FACT SHEET Infigen is a business that Markets Infigen operates in delivers a range of energy Infigen is a licenced energy retailer in the National Electricity Market (NEM) regions solutions through a diverse of Queensland, New South Wales, (including the Australian Capital Territory), sales strategy to commercial Victoria and South Australia. The company has wind generation assets in New and industrial (C&I) customers South Wales, South Australia and Western Australia. Infigen is also developing (>10,000MWh/year) and large options for firming in the NEM to support its business strategy. electricity retailers. Each state in the NEM differs in wholesale market liquidity, availability of firming, transmission, and state based emission targets and investment initiatives. While interconnectors enable limited interregional energy transmission, the volatility of regional spot prices and future prices are taken into account when determining options to offer to energy customers. A Multi-Channel Route to Market strategy Infigen’s Multi-Channel Route to Market strategy balances price, tenor and risk. Central to the sales strategy is the response to emerging opportunities and new challenges accompanying the evolving energy market. Channel Value for Infigen Value for Customer Spot market sales • Market price received for uncontracted production (merchant) • No production risk – no penalties associated with non-production • Deep and liquid forward derivative market – a number of particpants and platforms e.g. ASX futures -

Woodlawn Wind Farm Operational Environmental Management Plan

Woodlawn Wind Farm Operational Environmental Management Plan Document Control The Infigen Energy (Infigen) Operations Manager is responsible for the revision and update of this Operation Environmental Management Plan (OEMP) for Woodlawn Wind Farm (Woodlawn). A new revision date is required with any updates or revisions, and will be circulated to those on the Email Distribution List once the revision has been approved by the Infigen General Manager Energy Market Operations (GMEMO). This OEMP will be reviewed formally on an annual basis by the Operations Manager in consultation with the Infigen Health, Safety & Environment (HSE) Manager and Infigen Site Manager for Woodlawn, and other stakeholders as required. Review may also take place immediately after any significant incident or change to the activities, products or services or material changes in the operating conditions. Document History AU-OM-13-MAN-WOOD-21-1 (Old document number) Date Author Version Revision Notes Approval 21/05/2013 Senvion 1 Update to Senvion template. CL Reference to Capital and Woodlawn ERP 12/12/2013 Senvion 2 PKT Updated WHS legislation Rebranded to Suzlon 04/07/2014 Suzlon 3 Updated to reflect Infigen requested changes in 3.7 PKT plus added new section 3.9 “Stock Management” WOOW1-OEMP Revision Notes (include whether changes are Date Author Version Approval considered minor or significant updates) Infigen – A. Changed from Suzlon document to Infigen document 07/01/2015 4.0 Milne and Changed from Senvion to SEA 03/06/2016 A.McCormack 5.0 Updated to reflect new contract as Woodlawn RB Infigen - J 02/06/2017 6.0 Changed from Suzlon to Service Provider. -

Support October 8, 2020

1 of 145 Public Correspondence Item 7- Support October 8, 2020 San Diego Planning Commission, My late wife, Frankie Thibodeau, was always a strong advocate of renewable energy and firmly believed in the economic and environmental benefits it will serve for our local community. To that end, I am writing today to continue her legacy and show my support of the Campo Wind clean energy project being proposed by Terra-Gen LLC in partnership with the Campo Kumeyaay Tribe, here in San Diego. We know that wind energy is clean, renewable, and effective. The Campo Wind project alone will generate enough energy for over 70,000 area residents – a sizeable number that will also help in achieving California’s ambitious renewable energy mandate target by 2045. Further, and equally important, this project will be a significant economic investment in the Campo Tribe and its members. The wind farm will provide the Tribe with a reliable source of income that will elevate their standard of living, create short-and-long-term employment opportunities, as well as generate revenue for local businesses. We have an untapped opportunity here to make a significant impact on our environment, the Tribe, and the community as a whole. Wind farms make sense to me - they boost local economies and significantly reduce carbon emissions – so I encourage Country officials to carefully consider these benefits and join me in supporting the Campo Wind project. Regards, Wayne Thibodeau 39990 Roadrunner Ln Boulevard, CA 91905 (619) 766-9105 2 of 145 Stephen Greifzu 2405 Sage Drive Campo, CA 91906 619 255 5788 To Whom It May Concern, I am sending this letter as a show of strong support for the Campo Wind Project being proposed by Terra-Gen, in San Diego. -

Policies and Prospects for Renewable Energy in New South Wales Briefing Paper No 6/2014 by Andrew Haylen

Policies and prospects for renewable energy in New South Wales Briefing Paper No 6/2014 by Andrew Haylen RELATED PUBLICATIONS Electricity prices, demand and supply in NSW, NSW Parliamentary Research Service Briefing Paper 03/2014 by Andrew Haylen A tightening gas market: supply, demand and price outlook for NSW, NSW Parliamentary Research Service Briefing Paper 04/2014 by Andrew Haylen Wind Farms: regulatory developments in NSW, NSW Parliamentary Research Service e-brief 13/2012, by Nathan Wales and Daniel Montoya Key Issues in Energy, Background Paper 4/2014, by Daniel Montoya and Nathan Wales ISSN 1325-5142 ISBN 978-0-7313-1926-8 October 2014 © 2014 Except to the extent of the uses permitted under the Copyright Act 1968, no part of this document may be reproduced or transmitted in any form or by any means including information storage and retrieval systems, without the prior consent from the Manager, NSW Parliamentary Research Service, other than by Members of the New South Wales Parliament in the course of their official duties. Policies and prospects for renewable energy in New South Wales by Andrew Haylen NSW PARLIAMENTARY RESEARCH SERVICE Gareth Griffith (BSc (Econ) (Hons), LLB (Hons), PhD), Manager, Politics & Government/Law .......................................... (02) 9230 2356 Daniel Montoya (BEnvSc (Hons), PhD), Senior Research Officer, Environment/Planning ......................... (02) 9230 2003 Lenny Roth (BCom, LLB), Senior Research Officer, Law ....................................................... (02) 9230 2768 Alec Bombell (BA, LLB (Hons)), Research Officer, Law .................................................................. (02) 9230 3085 Tom Gotsis (BA, LLB, Dip Ed, Grad Dip Soc Sci) Research Officer, Law .................................................................. (02) 9230 2906 Andrew Haylen (BResEc (Hons)), Research Officer, Public Policy/Statistical Indicators ................. -

Discussion Paper on Renewable Energy Policy in the Planning And

From: Andrew Lothian To: SA Planning Commission Subject: ACK"D 22/8 - LH to save in KNET - Renewable Energy Policy Date: Thursday, 22 August 2019 11:37:44 AM Attachments: Wind farm report.pdf Discussion Paper on Proposed Changes to Renewable Energy Policy in the Planning and Design Code I have a particular interest in the visual impact of wind farms, having conducted several surveys, using public preferences, of their visual impact, both here in South Australia and interstate. I attach a copy of the report of the 2018 survey which showed a high level of support for wind farms, even in areas of relatively high landscape quality. I note that the Discussion Paper states: “current planning policies do not specifically restrict solar farms from being developed in more environmentally sensitive zones or where landscape character attributes are more prominent and worthy of greater protections.” While this relates to solar farms, it should apply equally to wind farms. The Paper also states: “The Significant Landscape Protection Overlay will identify significant landscapes in which wind farms are discouraged.” South Australia’s coast is an important landscape resource with areas of the high landscape quality including the west coast of Eyre Peninsula, parts of Kangaroo Island and the South East. I conducted research to measure and map the State’s coastal viewscapes for the Coast Protection Board and the report is available at my website: www.scenicsolutions.world/projects There is a real risk that in the future, large scale wind farms will become viable on the west coast of Eyre Peninsula and as this contains some of South Australia’s most outstanding landscapes, this would affect them adversely.