Roadmap to QRET ANEM NEM Nodal Modelling Report Final

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

INFIGEN ENERGY Appendix 4D – Half Year Report 31 December 2017

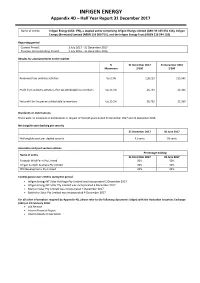

INFIGEN ENERGY Appendix 4D – Half Year Report 31 December 2017 Name of entity: Infigen Energy (ASX: IFN), a stapled entity comprising Infigen Energy Limited (ABN 39 105 051 616), Infigen Energy (Bermuda) Limited (ARBN 116 360 715), and the Infigen Energy Trust (ARSN 116 244 118) Reporting period Current Period: 1 July 2017 ‐ 31 December 2017 Previous Corresponding Period: 1 July 2016 ‐ 31 December 2016 Results for announcement to the market % 31 December 2017 31 December 2016 Movement $’000 $’000 Revenues from ordinary activities Up 2.5% 118,213 115,365 Profit from ordinary activities after tax attributable to members Up 25.1% 26,733 21,366 Net profit for the period attributable to members Up 25.1% 26,733 21,366 Dividends or distributions There were no dividends or distributions in respect of the half‐years ended 31 December 2017 and 31 December 2016. Net tangible asset backing per security 31 December 2017 30 June 2017 Net tangible asset per stapled security 41 cents 38 cents Associates and joint venture entities Percentage holding Name of entity 31 December 2017 30 June 2017 Forsayth Wind Farm Pty Limited 50% 50% Infigen Suntech Australia Pty Limited 50% 50% RPV Developments Pty Limited 32% 32% Control gained over entities during the period Infigen Energy NT Solar Holdings Pty Limited was incorporated 1 December 2017 Infigen Energy NT Solar Pty Limited was incorporated 4 December 2017 Manton Solar Pty Limited was incorporated 4 December 2017 Batchelor Solar Pty Limited was incorporated 4 December 2017 For all other information required -

Report: the Social and Economic Impact of Rural Wind Farms

The Senate Community Affairs References Committee The Social and Economic Impact of Rural Wind Farms June 2011 © Commonwealth of Australia 2011 ISBN 978-1-74229-462-9 Printed by the Senate Printing Unit, Parliament House, Canberra. MEMBERSHIP OF THE COMMITTEE 43rd Parliament Members Senator Rachel Siewert, Chair Western Australia, AG Senator Claire Moore, Deputy Chair Queensland, ALP Senator Judith Adams Western Australia, LP Senator Sue Boyce Queensland, LP Senator Carol Brown Tasmania, ALP Senator the Hon Helen Coonan New South Wales, LP Participating members Senator Steve Fielding Victoria, FFP Secretariat Dr Ian Holland, Committee Secretary Ms Toni Matulick, Committee Secretary Dr Timothy Kendall, Principal Research Officer Mr Terence Brown, Principal Research Officer Ms Sophie Dunstone, Senior Research Officer Ms Janice Webster, Senior Research Officer Ms Tegan Gaha, Administrative Officer Ms Christina Schwarz, Administrative Officer Mr Dylan Harrington, Administrative Officer PO Box 6100 Parliament House Canberra ACT 2600 Ph: 02 6277 3515 Fax: 02 6277 5829 E-mail: [email protected] Internet: http://www.aph.gov.au/Senate/committee/clac_ctte/index.htm iii TABLE OF CONTENTS MEMBERSHIP OF THE COMMITTEE ...................................................................... iii ABBREVIATIONS .......................................................................................................... vii RECOMMENDATIONS ................................................................................................. ix CHAPTER -

Infigen Energy 2012 Annual Report and Agm Notice of Meeting

12 October 2012 INFIGEN ENERGY 2012 ANNUAL REPORT AND AGM NOTICE OF MEETING Infigen Energy (ASX: IFN) advises that the attached 2012 Annual Report and the Notice of Meeting relating to the Annual General Meetings of Infigen Energy to be held on Thursday, 15 November 2012, are being despatched to securityholders today. The 2012 Annual Report and AGM Notice of Meeting are also available at Infigen’s website (www.infigenenergy.com). ENDS For further information please contact: Richard Farrell, Investor Relations Manager Tel +61 2 8031 9900 About Infigen Energy Infigen Energy is a specialist renewable energy business. We have interests in 24 wind farms across Australia and the United States. With a total installed capacity in excess of 1,600MW (on an equity interest basis), we currently generate enough renewable energy per year to power over half a million households. As a fully integrated renewable energy business in Australia, we develop, build, own and operate energy generation assets and directly manage the sale of the electricity that we produce to a range of customers in the wholesale market. Infigen Energy trades on the Australian Securities Exchange under the code IFN. For further information please visit our website: www.infigenenergy.com INFIGEN ENERGY OUR GENERATION, YOUR FUTURE Annual Report 2012 INFIGEN ENERGY ANNUAL REPORT 2012 OUR GENERATION CONTINUES TO CONTRIBUTE TO THE TRANSITION TO LOW CARBON EMISSION ELECTRICITY, for yoUR FUTURE AND FUTURE GENERATIONS MIKE HUTCHINSON Chairman 1 INFIGEN ENERGY We strive to be recognised as the leading provider of renewable energy. We want to make a positive difference. Our focus is on customer needs. -

Wind Energy in NSW: Myths and Facts

Wind Energy in NSW: Myths and Facts 1 INTRODUCTION Wind farms produce clean energy, generate jobs and income in regional areas and have minimal environmental impacts if appropriately located. Wind farms are now increasingly commonplace and accepted by communities in many parts of the world, but they are quite new to NSW. To increase community understanding and involvement in renewable energy, the NSW Government has established six Renewable Energy Precincts in areas of NSW with the best known wind resources. As part of the Renewable Energy Precincts initiative, the NSW Department of Environment, Climate Change and Water (DECCW) has compiled the following information to increase community understanding about wind energy. The technical information has been reviewed by the Centre for Environmental and Energy Markets, University of NSW. The Wind Energy Fact Sheet is a shorter and less technical brochure based on the Wind Energy in NSW: Myths and Facts. The brochure is available for download at www.environment.nsw.gov.au/resources/climatechange/10923windfacts.pdf. For further renewable energy information resources, please visit the Renewable Energy Precincts Resources webpage at http://www.environment.nsw.gov.au/climatechange/reprecinctresources.htm. 2 CONTENTS CONTENTS ...............................................................................................................3 WIND FARM NOISE ..................................................................................................4 WIND TURBINES AND SHADOW FLICKER...........................................................11 -

National Greenpower Accreditation Program Annual Compliance Audit

National GreenPower Accreditation Program Annual Compliance Audit 1 January 2007 to 31 December 2007 Publisher NSW Department of Water and Energy Level 17, 227 Elizabeth Street GPO Box 3889 Sydney NSW 2001 T 02 8281 7777 F 02 8281 7799 [email protected] www.dwe.nsw.gov.au National GreenPower Accreditation Program Annual Compliance Audit 1 January 2007 to 31 December 2007 December 2008 ISBN 978 0 7347 5501 8 Acknowledgements We would like to thank the National GreenPower Steering Group (NGPSG) for their ongoing support of the GreenPower Program. The NGPSG is made up of representatives from the NSW, VIC, SA, QLD, WA and ACT governments. The Commonwealth, TAS and NT are observer members of the NGPSG. The 2007 GreenPower Compliance Audit was completed by URS Australia Pty Ltd for the NSW Department of Water and Energy, on behalf of the National GreenPower Steering Group. © State of New South Wales through the Department of Water and Energy, 2008 This work may be freely reproduced and distributed for most purposes, however some restrictions apply. Contact the Department of Water and Energy for copyright information. Disclaimer: While every reasonable effort has been made to ensure that this document is correct at the time of publication, the State of New South Wales, its agents and employees, disclaim any and all liability to any person in respect of anything or the consequences of anything done or omitted to be done in reliance upon the whole or any part of this document. DWE 08_258 National GreenPower Accreditation Program Annual Compliance Audit 2007 Contents Section 1 | Introduction....................................................................................................................... -

Infigen Energy Annual Report 2018

Annual Report 2019. Infigen Energy Image: Capital Wind Farm, NSW Front page: Run With The Wind, Woodlawn Wind Farm, NSW Contents. 4 About Infigen Energy 7 2019 Highlights 9 Safety 11 Chairman & Managing Director’s Report Directors’ Report 16 Operating & Financial Review 31 Sustainability Highlights 34 Corporate Structure 35 Directors 38 Executive Directors & Management Team 40 Remuneration Report 54 Other Disclosures 56 Auditor’s Independence Declaration 57 Financial Report 91 Directors’ Declaration 92 Auditor’s Report Additional Information 9 Investor Information 8 10 Glossary 1 10 4 Corporate Directory Infigen Energy Limited ACN 105 051 616 Infigen Energy Trust ARSN 116 244 118 Registered office Level 17, 56 Pitt Street Sydney NSW 2000 Australia +61 2 8031 9900 www.infigenenergy.com 2 Our Strategy. We generate and source renewable energy. We add value by firming. We provide customers with reliable clean energy. 3 About Infigen Energy. Infigen is leading Australia’s transition to a clean energy future. Infigen generates and sources renewable energy, increases the value of intermittent renewables by firming, and provides customers with clean, reliable and competitively priced energy solutions. Infigen generates renewable energy from its owned wind farms in New South Wales (NSW), South Australia (SA) and Western Australia (WA). Infigen also sources renewable energy from third party renewable projects under its ‘Capital Lite’ strategy. Infigen increases the value of intermittent renewables by firming them from the Smithfield Open Cycle Gas Turbine facility in Western Sydney, NSW, and its 25MW/52MWh Battery at Lake Bonney, SA, where commercial operations are expected to commence in H1FY20. Infigen’s energy retailing licences are held in the National Electricity Market (NEM) regions of Queensland, New South Wales (including the Australian Capital Territory), Victoria and South Australia. -

Draft Minutes of Meeting 8

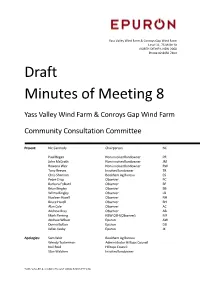

Yass Valley Wind Farm & Conroys Gap Wind Farm Level 11, 75 Miller St NORTH SYDNEY, NSW 2060 Phone 02 8456 7400 Draft Minutes of Meeting 8 Yass Valley Wind Farm & Conroys Gap Wind Farm Community Consultation Committee Present: Nic Carmody Chairperson NC Paul Regan Non-involved landowner PR John McGrath Non-involved landowner JM Rowena Weir Non-involved landowner RW Tony Reeves Involved landowner TR Chris Shannon Bookham Ag Bureau CS Peter Crisp Observer PC Barbara Folkard Observer BF Brian Bingley Observer BB Wilma Bingley Observer LB Noeleen Hazell Observer NH Bruce Hazell Observer BH Alan Cole Observer AC Andrew Bray Observer AB Mark Fleming NSW OEH (Observer) MF Andrew Wilson Epuron AW Donna Bolton Epuron DB Julian Kasby Epuron JK Apologies: Sam Weir Bookham Ag Bureau Wendy Tuckerman Administrator Hilltops Council Neil Reid Hilltops Council Stan Waldren Involved landowner YASS VALLEY & CONROYS GAP WIND FARM PTY LTD COMMUNITY CONSULTATION COMMITTEE Page 2 of 7 Absent: Councillor Ann Daniel Yass Valley Council Date: Thursday 23rd June 2016 Venue: Memorial Hall Annex, Comur Street, Yass Purpose: CCC Meeting No 8 Minutes: Item Agenda / Comment / Discussion Action 1 NC opened the Community Consultation Committee (CCC) meeting at 2:00 pm. - Apologies were noted as above. 2 Pecuniary or other interests - No declarations were made. 3 Minutes of Previous meeting No comments were received on the draft minutes of meeting number 7, which had been emailed to committee members. The draft minutes were accepted without changes and the finalised minutes will be posted on the project website. AW 4 Matters arising from the Previous Minutes JM raised that the planned quarterly meetings had not been occurring and that the previous meeting was in March 2014. -

Cash Flow 84 $ M 62

29 September 2014 INFIGEN ENERGY – FY14 ANNUAL FINANCIAL REPORT Infigen Energy (ASX: IFN) advises that the attached Annual Financial Report for the Infigen Energy Group for the year ended 30 June 2014, which includes the Annual Financial Report for Infigen Energy Trust, was despatched to securityholders today. The report is also available on Infigen’s website: www.infigenenergy.com ENDS For further information please contact: Richard Farrell, Investor Relations Manager Tel +61 2 8031 9900 About Infigen Energy Infigen Energy is a specialist renewable energy business. We have interests in 24 wind farms across Australia and the United States. With a total installed capacity in excess of 1,600MW (on an equity interest basis), we currently generate enough renewable energy per year to power over half a million households. For personal use only As a fully integrated renewable energy business, we develop, build, own and operate energy generation assets and directly manage the sale of the electricity that we produce to a range of customers in the wholesale market. Infigen Energy trades on the Australian Securities Exchange under the code IFN. For further information please visit our website: www.infigenenergy.com INFIGEN ENERGY INFIGEN | ANNUAL REPORT 2014 INFIGEN ENERGY ANNUAL REPORT 2014 For personal use only For personal use only A LEADING SPECIALIST RENEWABLE ENERGY BUSINESS CONTENTS 02 Business Highlights 51 Directors’ Report 04 About Us 56 Remuneration Report 06 Chairman’s Report 68 Auditor’s Independence Declaration 08 Managing Director’s Report 69 Financial Statements 12 Management Discussion and Analysis 75 Notes to Financial Statements 33 Safety and Sustainability 137 Directors’ Declaration 38 Infigen Board 138 Independent Auditor’s Report 40 Infigen Management 140 Additional Investor Information For personal use only 42 Corporate Governance Statement 143 Glossary 43 Corporate Structure 145 Corporate Directory All references to $ is a reference to Australian dollars and all years refer to financial year ended 30 June unless specifically marked otherwise. -

Kyoto Energypark

Kyoto energypark Appendix K(i) Duponts Property Research Land Value Impact Assessment for Kyoto Energy Park (December 2008) pamada LAND VALUE IMPACT ASSESSMENT – KYOTO ENERGY PARK KEY INSIGHTS LAND VALUE IMPACT ASSESSMENT FOR KYOTO ENERGY PARK Prepared for KEY INSIGHTS December 2008 1 LAND VALUE IMPACT ASSESSMENT – KYOTO ENERGY PARK KEY INSIGHTS INTRODUCTION Duponts has been engaged by Key Insights Pty Ltd to assess the impact on land values of the Kyoto Energy Park at Mountain Station and Middlebrook Station, via Scone. Duponts has made this assessment based on a review of literature on the matter, information of the development gained from the proponent, an informal inspection of the local area, our knowledge of land values in the Scone region and our knowledge of the impact developments of this nature have on land values. BACKGROUND EXISTING WIND FARMS IN NSW There are currently four wind farms operating in NSW including Blayney Wind Farm, Crookwell Wind Farm, Hampton Wind Park and Kooragang Island. In total they generate enough electricity to supply power to approximately 6,000 homes annually. Kooragang Island Crookwell Wind Farm Blayney Wind Farm Hampton Wind Park In 1997 Energy Australia installed 1 wind turbine on Kooragang Island, on the northern side of Newcastle harbour. The wind turbine provides 600kW of energy to Energy Australia’s Pure Energy customers. Crookwell Wind farm has 8 wind turbines located in the southern tablelands of NSW. Opened in 1998 it was the first grid-connected wind farm in Australia. The wind farm has a total capacity of 4.8 MW. The wind farm is currently owned by Eraring Energy. -

Flyers Creek Wind Farm Pty Ltd

VOLUME I Flyers Creek Wind Farm Pty Ltd Flyers CreekWIND FARM Environmental Assessment Environmental CHAPTER 1 Introduction 1. Introduction 1.1 Background This Environmental Assessment has been prepared by Aurecon on behalf of the proponent, Flyers Creek Wind Farm Pty Ltd, for the proposed development of a wind farm and associated ancillary infrastructure. The Environmental Assessment supports a Project Application lodged by proponent under the Environmental Planning and Assessment Act, 1979 (EP&A Act). The project site is located in the Central Western Region of New South Wales (NSW) approximately 20 kilometres south of Orange and 200 kilometres west of Sydney, NSW (Figures 1.1 and 1.2). A project application based on an initial conceptual project layout was lodged with the NSW Department of Planning on 15 December 2008. Subsequently on 19 January 2009, the Director- General of the Department of Planning prescribed specific requirements for the scope and content of the Environmental Assessment (Appendix A). On the 11 November 2009, the NSW Minister for Planning declared the proposed Flyers Creek Wind Farm to be a ‘Critical Infrastructure’ project (under Section 75C of the Environmental Planning and Assessment Act, 1979) (Appendix B) being a project that is essential for the State and economic reasons and for social and environmental reasons. This Environmental Assessment based on the updated project design addresses the Director- General’s requirements and provides a description of the currently proposed project, the existing environment and planning context, an assessment of the potential environmental impacts of the project, the measures proposed to mitigate those impacts, justification of the project and the consultation undertaken and proposed in the future for the project. -

SKI 2020 Full Year Investor Presentation

31 DECEMBER 2020 FULL YEAR RESULTS TUESDAY, 23 FEBRUARY 2021 INFRASTRUCTURE FOR THE FUTURE SPARK INFRASTRUCTURE – AT A GLANCE ASX-listed owner of leading essential energy infrastructure MARKET Distribution Transmission Renewables $ CAPITALISATION(1) 3.6bn S&P/ASX 100 Victoria Power Networks TransGrid Bomen Solar Farm and SA Power Networks (NSW) (NSW) REGULATED AND CONTRACTED ASSET 49% 15% 100% $ BASE (PROPORTIONAL) SPARK INFRASTRUCTURE SPARK INFRASTRUCTURE SPARK INFRASTRUCTURE 6.7bn OWNERSHIP OWNERSHIP OWNERSHIP $18.7bn $ $ $ TOTAL ELECTRICITY NETWORK 11.03bn 7.52bn 0.17bn AND GENERATION ASSETS(2) REGULATED ASSET BASE REGULATED AND CONTRACTED ASSET BASE CONTRACTED ASSET BASE SUPPLYING 5.0m+ WAGGA HOMES AND BUSINESSES WAGGA, 80% 17% 3% NSW 5,400 SKI PROPORTIONAL SKI PROPORTIONAL SKI PROPORTIONAL EMPLOYEES ASSET BASE(3) ASSET BASE(3) ASSET BASE(3) (1) As at 19 February 2021. Balance sheet and other information as at 31 December 2020 (2) Spark Infrastructure has proportional interests in $18.7bn of total electricity network and contracted generation assets (3) Pro forma Spark Infrastructure I Investor Presentation I February 2021 2 INFRASTRUCTURE FOR THE FUTURE FINANCIAL HIGHLIGHTS Solid earnings and growth delivered by high quality energy network businesses Underlying Look- FY2020 Regulated Contracted through EBITDA(1) Distribution asset base(1) asset base(2) $ 13.5cps $6.4bn $294m 862m +2.1cps franking Up 3.3% Up 13.4% Up 2.4% FY2021 Growth FFO/ Distribution capital Net debt(5) (3) guidance expenditure(4) 12.5cps $231m 12.4% + ~25% franking -

Accelerating Clean Energy Investment Backing Technology and Innovation to Transform Our Economy

Accelerating clean energy investment Backing technology and innovation to transform our economy 2020 2019 2018 2017 2016 8b 7. 2 2015 2014 2013 b .0 4 2 2 .2 b 3 . 3 2 . b 5 b 5 . 7 b b 0 . 9 1 11.0b Annual Report 2019–20 The CEFC is a specialist investor with a deep sense of purpose: to be at the forefront of Australia’s successful transition to a low carbon economy. We invest in new and emerging technologies and opportunities on behalf of all Australians, operating with the support of the Australian Government. As a specialist investor we have a clear focus on clean energy to deliver benefits for generations to come. Our approach is founded on our shared values: to make a positive impact, to collaborate with others, to champion integrity and to embrace innovation. 2019–20 highlights New CEFC investment commitments of more than $1 billion, supporting investments with a combined value of $4.2 billion in the year to 30 June 2020 CEFC finance extended to new areas of the economy, delivering Australia’s first dedicated green bond fund, the first CEFC green home loan and a material uplift in the capacity of Australia’s largest battery New investment commitments of just over $13 million in three cleantech innovators, as well as increased investment of $3.4 million in two other portfolio companies to accelerate their growth More than $187 million in CEFC wholesale finance to support some 6,700 smaller scale investments in clean energy projects, including in agribusiness, manufacturing, property and transport Continued strong financial performance despite the challenging economic environment, with almost $942 million in CEFC finance recycled through repayments, sales and redemptions over the year, to be available for further investment.