Chapter 9. PORT PLAN

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Iranshah Udvada Utsav

HAMAZOR - ISSUE 1 2016 Dr Nergis Mavalvala Physicist Extraordinaire, p 43 C o n t e n t s 04 WZO Calendar of Events 05 Iranshah Udvada Utsav - vahishta bharucha 09 A Statement from Udvada Samast Anjuman 12 Rules governing use of the Prayer Hall - dinshaw tamboly 13 Various methods of Disposing the Dead 20 December 25 & the Birth of Mitra, Part 2 - k e eduljee 22 December 25 & the Birth of Jesus, Part 3 23 Its been a Blast! - sanaya master 26 A Perspective of the 6th WZYC - zarrah birdie 27 Return to Roots Programme - anushae parrakh 28 Princeton’s Great Persian Book of Kings - mahrukh cama 32 Firdowsi’s Sikandar - naheed malbari 34 Becoming my Mother’s Priest, an online documentary - sujata berry COVER 35 Mr Edulji Dinshaw, CIE - cyrus cowasjee Image of the Imperial 39 Eduljee Dinshaw Road Project Trust - mohammed rajpar Custom House & bust of Mr Edulji Dinshaw, CIE. & jameel yusuf which stands at Lady 43 Dr Nergis Mavalvala Dufferin Hospital. 44 Dr Marlene Kanga, AM - interview, kersi meher-homji PHOTOGRAPHS 48 Chatting with Ami Shroff - beyniaz edulji 50 Capturing Histories - review, freny manecksha Courtesy of individuals whose articles appear in 52 An Uncensored Life - review, zehra bharucha the magazine or as 55 A Whirlwind Book Tour - farida master mentioned 57 Dolly Dastoor & Dinshaw Tamboly - recipients of recognition WZO WEBSITE 58 Delhi Parsis at the turn of the 19C - shernaz italia 62 The Everlasting Flame International Programme www.w-z-o.org 1 Sponsored by World Zoroastrian Trust Funds M e m b e r s o f t h e M a n a g i -

Diagnostic Centers'!A1 Laboratories!A1 Dental Centers'!A1 Ophthalmology Clinics'!A1 Medical Center'!A1 Diagnostic Centers

Diagnostic Centers'!A1 Laboratories!A1 Dental Centers'!A1 Ophthalmology Clinics'!A1 Medical Center'!A1 Diagnostic Centers L I S T O F A L L I A N Z E F U N E T W O R K D I S C O U N T D I A G N O S T I C C E N T R E S S.No Hospital Name Address Contact Contact Person Email Contact Number City Discount Category 021-35662052 Mr. Yousuf Poonawala 1 Burhani Diagnostic Centre Jaffer Plaza, Mansfield Street, Saddar, Karachi. 021-5661952 Karachi 10-15% Diagnostic Center 0336-0349355 (Administrator) [email protected] 02136626125-6 0334-3357471 [email protected] 2 Dr. Essa's Laboratory & Diagnostic Centre (Main Centre) B-122 (Blue Building) Block-H, Shahrah-e-Jahangir, Near Five Star, North Nazimabad. Mr. Shakeel / Ms. Shahida 021-36625149 Karachi 10-20% Diagnostic Center 0335-5755529 [email protected] 021-36312746 0335- 2.1 Ayesha Manzil Centre Ali Appartment, FB Area Karachi Karachi 10-20% Diagnostic Center 5755536 021-35862522 021- 2.2 Zamzama Centre Suite # 2, Plot 8-C (Beside Aijaz Boutique), 4th Zamzama Commercial Lane Karachi 10-20% Diagnostic Center 35376887 2.3 Medilink Centre Suite # 103, 1st Floor, The Plaza, 2 Talwar, Khayaban-e-Iqbal, Main Clifton Road, Karachi 021-35376071-74 Karachi 10-20% Diagnostic Center 2.4 Abdul Hassan Isphahani Centre A-1/3&4, Block-4, gulshan-e-Iqbal. Main Abdul Hassan Isphahani Road, Karachi 021-34968377-78 Karachi 10-20% Diagnostic Center 2.5 KPT Centre Karachi Port Trust Hospital Keemari, Karachi 021-34297786 Karachi 10-20% Diagnostic Center 021-34620176 021- 2.6 Gulistan-E-Johar Centre S -

Challenges and Solutionsin Building CPEC-A Flagship Of

Issue , Working paper CENTRE OF EXCELLENCE Challenges and CHINA-PAKISTAN ECONOMIC CORRIDORSolutionsIn Building CPEC-A Flagship of BRI Written by: Yasir Arrfat Research Coordinator CoE CPEC Minitry of Planning, Pakistan Institute Development Reform of Development Economics Challenges and Solutions in Building CPEC-A Flagship of BRI Yasir Arrfat Research Coordinator Centre of Excellence (CoE) for China Pakistan Economic Corridor (CPEC) Islamabad, Pakistan, [email protected] Abstract-One of the OBOR pilot corridors out of the six corridors is CPEC. The CPEC has been initiated in 2013 and due to its speedy progress, CPEC is now vastly considered as the “flagship” project among the OBOR projects. The CPEC initiatives include; development of Gwadar Port, road, rail and optical fiber connectivity, energy corridor and Special Economic Zones development for bilateral benefits to attain inclusive growth and regional harmonization. Before the inception of CPEC, the growth of Pakistan was curtailed by two major bottlenecks; acute energy shortages and weak local and regional connectivity infrastructures. In 2013, CPEC came with 59 billion USDs under OBOR and it has been eliminating all major economic bottlenecks. This paper sheds light on the BRI with deep focusing on CPEC. It further represents the Pakistan’s improving economic indicators through CPEC. This paper will also examine some key challenges and their solutions in building CPEC. Key Words-BRI, Challenges, Connectivity, Corridors, CPEC, Global Competitive Index (GCI), Investment, Infrastructure, OBOR I. INTRODUCTION The Globalization has brought vast changes in global economy and has directed the evolution to a boundary less development. This phenomenon has significantly amplified the maritime trade from 2.37 billion tons of freight to 5.88 billion tons of freight moving through maritime routes. -

1 All Rights Reserved Do Not Reproduce in Any Form Or

ALL RIGHTS RESERVED DO NOT REPRODUCE IN ANY FORM OR QUOTE WITHOUT AUTHOR’S PERMISSION 1 2 Tactical Cities: Negotiating Violence in Karachi, Pakistan by Huma Yusuf A.B. English and American Literature and Language Harvard University, 2002 SUBMITTED TO THE DEPARTMENT OF COMPARATIVE MEDIA STUDIES IN PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR THE DEGREE OF MASTER OF SCIENCE IN COMPARATIVE MEDIA STUDIES AT THE MASSACHUSETTS INSTITUTE OF TECHNOLOGY JUNE 2008 © Huma Yusuf. All rights reserved. The author hereby grants to MIT permission to reproduce and to distribute publicly paper and electronic copies of this thesis document in whole or in part in any medium now known or hereafter created. Thesis Supervisor: ________________________________________________________ Henry Jenkins Peter de Florez Professor of Humanities Professor of Comparative Media Studies and Literature Thesis Supervisor: ________________________________________________________ Shankar Raman Associate Professor of Literature Thesis Supervisor: ________________________________________________________ William Charles Uricchio Professor of Comparative Media Studies 3 4 Tactical Cities: Negotiating Violence in Karachi, Pakistan by Huma Yusuf Submitted to the Department of Comparative Media Studies on May 9, 2008, in Partial Fulfillment of the Requirements for the Degree of Master in Science in Comparative Media Studies. ABSTRACT This thesis examines the relationship between violence and urbanity. Using Karachi, Pakistan, as a case study, it asks how violent cities are imagined and experienced by their residents. The thesis draws on a variety of theoretical and epistemological frameworks from urban studies to analyze the social and historical processes of urbanization that have led to the perception of Karachi as a city of violence. It then uses the distinction that Michel de Certeau draws between strategy and tactic in his seminal work The Practice of Everyday Life to analyze how Karachiites inhabit, imagine, and invent their city in the midst of – and in spite of – ongoing urban violence. -

Asia's Energy Security

the national bureau of asian research nbr special report #68 | november 2017 asia’s energy security and China’s Belt and Road Initiative By Erica Downs, Mikkal E. Herberg, Michael Kugelman, Christopher Len, and Kaho Yu cover 2 NBR Board of Directors Charles W. Brady Ryo Kubota Matt Salmon (Chairman) Chairman, President, and CEO Vice President of Government Affairs Chairman Emeritus Acucela Inc. Arizona State University Invesco LLC Quentin W. Kuhrau Gordon Smith John V. Rindlaub Chief Executive Officer Chief Operating Officer (Vice Chairman and Treasurer) Unico Properties LLC Exact Staff, Inc. President, Asia Pacific Wells Fargo Regina Mayor Scott Stoll Principal, Global Sector Head and U.S. Partner George Davidson National Sector Leader of Energy and Ernst & Young LLP (Vice Chairman) Natural Resources Vice Chairman, M&A, Asia-Pacific KPMG LLP David K.Y. Tang HSBC Holdings plc (Ret.) Managing Partner, Asia Melody Meyer K&L Gates LLP George F. Russell Jr. President (Chairman Emeritus) Melody Meyer Energy LLC Chairman Emeritus Honorary Directors Russell Investments Joseph M. Naylor Vice President of Policy, Government Lawrence W. Clarkson Dennis Blair and Public Affairs Senior Vice President Chairman Chevron Corporation The Boeing Company (Ret.) Sasakawa Peace Foundation USA U.S. Navy (Ret.) C. Michael Petters Thomas E. Fisher President and Chief Executive Officer Senior Vice President Maria Livanos Cattaui Huntington Ingalls Industries, Inc. Unocal Corporation (Ret.) Secretary General (Ret.) International Chamber of Commerce Kenneth B. Pyle Joachim Kempin Professor; Founding President Senior Vice President Norman D. Dicks University of Washington; NBR Microsoft Corporation (Ret.) Senior Policy Advisor Van Ness Feldman LLP Jonathan Roberts Clark S. -

Transshipment by Ministry of Maritime Affairs

GOVERNMENT OF PAKISTAN MINISTRY OF MARITIME AFFAIRS **** Draft Working Paper Transshipment INDEX S. No. Topic Page 01 Year 2020 declared as “Year of The Blue Economy” by Prime Minister 01 02 Concept of Transshipment for Pakistan 02 03 Potential for Growth in Transshipment at Karachi Port Terminals 02 04 Concepts of Transshipment 03 05 Transshipment Hubs 03 06 Forms of Transshipment 04 07 Ingredients of a successful model 05 08 Middle East – As A Successful Model 06 09 Consultations with major stakeholders 06 10 Pakistan’s Potential as Transshipment Hub - Graphic Illustrations 07 11 Establishing of a transshipment business friendly environment 11 12 Transshipment Business Model & Hub Selection - Phases 11 13 Proximity of Ports to Cities as a factor for Transshipment 12 14 Landlocked Countries & Arabian Sea Ports 12 15 Regional Ports & Shipping Routes 12 16 Gwadar Port Connectivity Potential 13 17 Barriers facing Pakistan vis-à-vis regional ports – Present Capacity & Utilization 13 18 Indian Ports Increasing Potential 14 19 Container Throughput – Comparison of Regions & Opportunities 14 20 Shipping Routes Transshipment Ports Wise Comparison 15 21 Chahbahar Port location – India attempting to benefit 15 22 Arabian Sea (Pakistan) Corridor 16 23 Comparative Analysis of Regional Ports for Transshipment Charges 16 24 Berthing/Charges Analysis Regional Comparison 18 25 Break up of Port Charges & their Comparison with Regional Ports 20 26 Port of Karachi Cargo & Container Capacity – Reduction of Volume 21 27 Transshipment Karachi Port Terminals -

Baloch Insurgency and Its Impact on CPEC Jaleel, Sabahat and Bibi, Nazia

Munich Personal RePEc Archive Baloch Insurgency and its impact on CPEC jaleel, Sabahat and Bibi, Nazia University of Engineering and technology, Taxila, Pakistan Institute of Development Economics, Islamabad 18 July 2017 Online at https://mpra.ub.uni-muenchen.de/90135/ MPRA Paper No. 90135, posted 24 Nov 2018 17:28 UTC Baloch Insurgency and its impact on CPEC Sabahat Jaleel (Lecturer UET Taxila) & Nazia Bibi (Assistant Professor PIDE) Abstract CPEC, a significant development project, aims to connect Pakistan and China through highways, oil and gas pipelines, railways and an optical fiber link all the way from Gwadar to Xinjiang. Being the biggest venture in the bilateral ties of China-Pakistan, the project faces certain undermining factors. The research explores the lingering security concerns that surfaced due to the destabilizing and separatist efforts of the Baloch Liberation Army (BLA) and Baloch Liberation Front (BLF). It also elaborates the Chinese concerns and Pakistan efforts to address these concerns while assuming the hypothesis that a secure and stable environment is necessary to reap the fruits of this mega project. The work also answers some innovative questions thus helpful for the students of Economics, Pakistan history, politics, Internal Relations, Foreign Policy and for those who intend to read about China-Pakistan and their joint ventures as CPEC. The main objective of the study to empirically analyses the response of Baloch community. Graphical and empirical methods have been adopted to describe and analyze the facts and figures related to the topic. The results clearly indicate that CPEC will face resistance from people of Balochistan, which will negatively affect the prospects of CPEC. -

Makers-Of-Modern-Sindh-Feb-2020

Sindh Madressah’s Roll of Honor MAKERS OF MODERN SINDH Lives of 25 Luminaries Sindh Madressah’s Roll of Honor MAKERS OF MODERN SINDH Lives of 25 Luminaries Dr. Muhammad Ali Shaikh SMIU Press Karachi Alma-Mater of Quaid-e-Azam Mohammad Ali Jinnah Sindh Madressatul Islam University, Karachi Aiwan-e-Tijarat Road, Karachi-74000 Pakistan. This book under title Sindh Madressah’s Roll of Honour MAKERS OF MODERN SINDH Lives of 25 Luminaries Written by Professor Dr. Muhammad Ali Shaikh 1st Edition, Published under title Luminaries of the Land in November 1999 Present expanded edition, Published in March 2020 By Sindh Madressatul Islam University Price Rs. 1000/- SMIU Press Karachi Copyright with the author Published by SMIU Press, Karachi Aiwan-e-Tijarat Road, Karachi-74000, Pakistan All rights reserved. No part of this book may be reproduced in any from or by any electronic or mechanical means, including information storage and retrieval system, without written permission from the publisher, except by a reviewer, who may quote brief passage in a review Dedicated to loving memory of my parents Preface ‘It is said that Sindh produces two things – men and sands – great men and sandy deserts.’ These words were voiced at the floor of the Bombay’s Legislative Council in March 1936 by Sir Rafiuddin Ahmed, while bidding farewell to his colleagues from Sindh, who had won autonomy for their province and were to go back there. The four names of great men from Sindh that he gave, included three former students of Sindh Madressah. Today, in 21st century, it gives pleasure that Sindh Madressah has kept alive that tradition of producing great men to serve the humanity. -

The Rise of Dalit Peasants Kolhi Activism in Lower Sindh

The Rise of Dalit Peasants Kolhi Activism in Lower Sindh (Original Thesis Title) Kolhi-peasant Activism in Naon Dumbālo, Lower Sindh Creating Space for Marginalised through Multiple Channels Ghulam Hussain Mahesar Quaid-i-Azam University Department of Anthropology ii Islamabad - Pakistan Year 2014 Kolhi-Peasant Activism in Naon Dumbālo, Lower Sindh Creating Space for Marginalised through Multiple Channels Ghulam Hussain Thesis submitted to the Department of Anthropology, Quaid-i-Azam University Islamabad, in partial fulfillment of the degree of ‗Master of Philosophy in Anthropology‘ iii Quaid-i-Azam University Department of Anthropology Islamabad - Pakistan Year 2014 Formal declaration I hereby, declare that I have produced the present work by myself and without any aid other than those mentioned herein. Any ideas taken directly or indirectly from third party sources are indicated as such. This work has not been published or submitted to any other examination board in the same or a similar form. Islamabad, 25 March 2014 Mr. Ghulam Hussain Mahesar iv Final Approval of Thesis Quaid-i-Azam University Department of Anthropology Islamabad - Pakistan This is to certify that we have read the thesis submitted by Mr. Ghulam Hussain. It is our judgment that this thesis is of sufficient standard to warrant its acceptance by Quaid-i-Azam University, Islamabad for the award of the degree of ―MPhil in Anthropology‖. Committee Supervisor: Dr. Waheed Iqbal Chaudhry External Examiner: Full name of external examiner incl. title Incharge: Dr. Waheed Iqbal Chaudhry v ACKNOWLEDGEMENT This thesis is the product of cumulative effort of many teachers, scholars, and some institutions, that duly deserve to be acknowledged here. -

Gwadar: China's Potential Strategic Strongpoint in Pakistan

U.S. Naval War College U.S. Naval War College Digital Commons CMSI China Maritime Reports China Maritime Studies Institute 8-2020 China Maritime Report No. 7: Gwadar: China's Potential Strategic Strongpoint in Pakistan Isaac B. Kardon Conor M. Kennedy Peter A. Dutton Follow this and additional works at: https://digital-commons.usnwc.edu/cmsi-maritime-reports Recommended Citation Kardon, Isaac B.; Kennedy, Conor M.; and Dutton, Peter A., "China Maritime Report No. 7: Gwadar: China's Potential Strategic Strongpoint in Pakistan" (2020). CMSI China Maritime Reports. 7. https://digital-commons.usnwc.edu/cmsi-maritime-reports/7 This Book is brought to you for free and open access by the China Maritime Studies Institute at U.S. Naval War College Digital Commons. It has been accepted for inclusion in CMSI China Maritime Reports by an authorized administrator of U.S. Naval War College Digital Commons. For more information, please contact [email protected]. August 2020 iftChina Maritime 00 Studies ffij$i)f Institute �ffl China Maritime Report No. 7 Gwadar China's Potential Strategic Strongpoint in Pakistan Isaac B. Kardon, Conor M. Kennedy, and Peter A. Dutton Series Overview This China Maritime Report on Gwadar is the second in a series of case studies on China’s Indian Ocean “strategic strongpoints” (战略支点). People’s Republic of China (PRC) officials, military officers, and civilian analysts use the strategic strongpoint concept to describe certain strategically valuable foreign ports with terminals and commercial zones owned and operated by Chinese firms.1 Each case study analyzes a different port on the Indian Ocean, selected to capture geographic, commercial, and strategic variation.2 Each employs the same analytic method, drawing on Chinese official sources, scholarship, and industry reporting to present a descriptive account of the port, its transport infrastructure, the markets and resources it accesses, and its naval and military utility. -

Reclaiming Prosperity in Khyber- Pakhtunkhwa

Working paper Reclaiming Prosperity in Khyber- Pakhtunkhwa A Medium Term Strategy for Inclusive Growth Full Report April 2015 When citing this paper, please use the title and the following reference number: F-37109-PAK-1 Reclaiming Prosperity in Khyber-Pakhtunkhwa A Medium Term Strategy for Inclusive Growth International Growth Centre, Pakistan Program The International Growth Centre (IGC) aims to promote sustainable growth in developing countries by providing demand-led policy advice informed by frontier research. Based at the London School of Economics and in partnership with Oxford University, the IGC is initiated and funded by DFID. The IGC has 15 country programs. This report has been prepared under the overall supervision of the management team of the IGC Pakistan program: Ijaz Nabi (Country Director), Naved Hamid (Resident Director) and Ali Cheema (Lead Academic). The coordinators for the report were Yasir Khan (IGC Country Economist) and Bilal Siddiqi (Stanford). Shaheen Malik estimated the provincial accounts, Sarah Khan (Columbia) edited the report and Khalid Ikram peer reviewed it. The authors include Anjum Nasim (IDEAS, Revenue Mobilization), Osama Siddique (LUMS, Rule of Law), Turab Hussain and Usman Khan (LUMS, Transport, Industry, Construction and Regional Trade), Sarah Saeed (PSDF, Skills Development), Munir Ahmed (Energy and Mining), Arif Nadeem (PAC, Agriculture and Livestock), Ahsan Rana (LUMS, Agriculture and Livestock), Yasir Khan and Hina Shaikh (IGC, Education and Health), Rashid Amjad (Lahore School of Economics, Remittances), GM Arif (PIDE, Remittances), Najm-ul-Sahr Ata-ullah and Ibrahim Murtaza (R. Ali Development Consultants, Urbanization). For further information please contact [email protected] , [email protected] , [email protected] . -

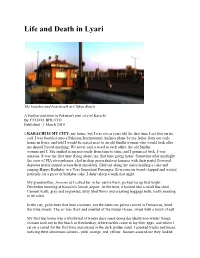

Life and Death in Lyari

Life and Death in Lyari The beaches and boardwalk at Clifton Beach A Further partition in Pakistan's port city of Karachi By FATIMA BHUTTO Published : 1 March 2010 1. KARACHI IS MY CITY, my home, but I was seven years old the first time I set foot on its soil. I was boarded onto a Pakistan International Airlines plane by my father from our exile home in Syria, and told I would be seated next to an old Sindhi woman who would look after me should I need anything. We never said a word to each other, the old Sindhi woman and I. She smiled at me nervously from time to time, and I grimaced back. I was anxious. It was my first time flying alone, my first time going home. Sometime after midnight the crew of PIA stewardesses, clad in deep green shalwar kameez with their pastel flowered dupattas neatly pinned across their shoulders, filed out along the aisles holding a cake and singing Happy Birthday to a Very Important Passenger. Everyone on board clapped and waited patiently for a piece of birthday cake. I didn't sleep a wink that night. My grandmother, Joonam as I called her in her native Farsi, picked me up that bright December morning at Karachi's Jinnah airport. At the time, it looked like a small bus shed. Cement walls, grey and unpainted, dirty tiled floors and creaking baggage belts, badly needing to be oiled. In the city, palm trees that bore coconuts, not the dates our palms carried in Damascus, lined the wide streets.