Update of the Space and Launch Insurance Industry

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

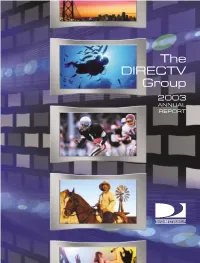

The DIRECTV Group 2003 ANNUAL REPORT

The DIRECTV Group 2003 ANNUAL REPORT THEDIRECTVGROUP DIRECTV U.S. (100% owned by The DIRECTV Group, Inc.) • Largest digital multi-channel service provider in the U.S. DIRECTV U.S. Cumulative Subscribers with 12.2 million customers as of year-end 2003 ()(Total Platform) 12.2M • Increased revenues 19% to $7.7 billion and operating 11.2M 10.3M profit before depreciation and amortization improved 9.1M 59% to $970 million in 2003 7.7M • Increased owned and operated customer base approximately 13% by adding approximately 1.2 million net new owned and operated customers in 2003 1999 2000 2001 2002 2003 - Added over 3 million gross owned and operated sub- scribers in 2003, an all-time record for a single year DIRECTV U.S. Average Monthly Revenue per Customer (ARPU) • Generates the highest average monthly video revenue (Owned and Operated Subscribers) in the U.S. multi-channel entertainment industry with $63.90 $63.90 per customer in 2003, an increase of 7% over 2002 $59.80 $58.70 $57.70 • Broadcasts all of the local channels in 64 top markets, $55.80 representing 72% of U.S. television households as of year-end 2003 - Expects to expand local channel coverage to at least 1999 2000 2001 2002 2003 130 top markets representing 92% of U.S. television households during 2004 DIRECTV U.S. Monthly Customer Churn (Owned and Operated Subscribers) • Ranked “#1 in Customer Satisfaction Among Satellite 2.0% 1.8% and Cable TV Subscribers Two Years in a Row” by J.D. 1.7% 1.6% 1.6% Power and Associates 1.5% 1.5% • Distributes over 850 digital video and audio channels, expanding significantly with the expected successful 1.0% launch of the DIRECTV 7S satellite in 2004 1999 2000 2001 2002 2003 DIRECTV Latin America (86% owned by The DIRECTV Group, Inc.) • A leading digital multi-channel service provider in Latin THEDIRECTVGROUP America with 1.5 million customers in 28 countries as of year- end 2003 • Emerged from Chapter 11 bankruptcy process in February 2004 as a more competitive and financially stronger company The DIRECTV Group, Inc. -

Quarterly Launch Report

Commercial Space Transportation QUARTERLY LAUNCH REPORT Featuring the launch results from the previous quarter and forecasts for the next two quarters. 4th Quarter 1996 U n i t e d S t a t e s D e p a r t m e n t o f T r a n s p o r t a t i o n • F e d e r a l A v i a t i o n A d m i n i s t r a t i o n A s s o c i a t e A d m i n i s t r a t o r f o r C o m m e r c i a l S p a c e T r a n s p o r t a t i o n QUARTERLY LAUNCH REPORT 1 4TH QUARTER REPORT Objectives This report summarizes recent and scheduled worldwide commercial, civil, and military orbital space launch events. Scheduled launches listed in this report are vehicle/payload combinations that have been identified in open sources, including industry references, company manifests, periodicals, and government documents. Note that such dates are subject to change. This report highlights commercial launch activities, classifying commercial launches as one or more of the following: • Internationally competed launch events (i.e., launch opportunities considered available in principle to competitors in the international launch services market), • Any launches licensed by the Office of the Associate Administrator for Commercial Space Transportation of the Federal Aviation Administration under U.S. -

PUBLIC NOTICE FEDERAL COMMUNICATIONS COMMISSION 445 12Th STREET S.W

PUBLIC NOTICE FEDERAL COMMUNICATIONS COMMISSION 445 12th STREET S.W. WASHINGTON D.C. 20554 News media information 202-418-0500 Fax-On-Demand 202-418-2830; Internet: http://www.fcc.gov (or ftp.fcc.gov) TTY (202) 418-2555 Report No. SES-00933 Wednesday June 6, 2007 SATELLITE COMMUNICATIONS SERVICES RE: SATELLITE RADIO APPLICATIONS ACCEPTED FOR FILING The applications listed herein have been found, upon initial review, to be acceptable for filing. The Commission reserves the right to return any of the applications if, upon further examination, it is determined they are defective and not in conformance with the Commission's Rules and Regulations and its Policies. Final action will not be taken on any of these applications earlier than 30 days following the date of this notice. 47 U.S.C. § 309(b). All applications accepted for filing will be assigned call signs, or other unique station identifiers. However, these assignments are for administrative purposes only and do not in any way prejudice Commission action. SES-ASG-20070504-00554 E E000731 CLEAR CHANNEL BROADCASTING LICENSES, INC. Application for Consent to Assignment Current Licensee: CLEAR CHANNEL BROADCASTING LICENSES, INC. FROM: CLEAR CHANNEL BROADCASTING LICENSES, INC. TO: TV Acquisition LLC No. of Station(s) listed: 6 SES-ASG-20070504-00555 E E980346 Citicasters Co. Application for Consent to Assignment Current Licensee: Citicasters Co. FROM: CITICASTERS CO. TO: TV Acquisition LLC No. of Station(s) listed: 1 SES-ASG-20070504-00557 E E030135 Central NY News Inc Application for Consent to Assignment Current Licensee: Central NY News Inc FROM: CENTRAL NY NEWS, INC. -

PUBLIC NOTICE FEDERAL COMMUNICATIONS COMMISSION 445 12Th STREET S.W

PUBLIC NOTICE FEDERAL COMMUNICATIONS COMMISSION 445 12th STREET S.W. WASHINGTON D.C. 20554 News media information 202-418-0500 Internet: http://www.fcc.gov (or ftp.fcc.gov) TTY (202) 418-2555 Report No. SES-02228 Monday December 30, 2019 Satellite Communications Services re: Satellite Radio Applications Accepted For Filing The applications listed herein have been found, upon initial review, to be acceptable for filing. The Commission reserves the right to return any of the applications if, upon further examination, it is determined they are defective and not in conformance with the Commission's Rules and Regulations and its Policies. Final action will not be taken on any of these applications earlier than 30 days following the date of this notice. 47 U.S.C. § 309(b). All applications accepted for filing will be assigned call signs, or other unique station identifiers. However, these assignments are for administrative purposes only and do not in any way prejudice Commission action. SES-AMD-20191129-01548 E E190724 SpaceX Services, Inc. Amendment Class of Station: Fixed Earth Stations Nature of Service: Fixed Satellite Service See IBFS File No.SES-LIC-20190906-01170 for a description of application. SITE ID: 1 LOCATION: 1020 Methodist Road, Mercer, Greenville, PA 41 ° 26 ' 0.80 " N LAT. 80 ° 19 ' 59.60 " W LONG. ANTENNA ID: 1 1.47 meters SpaceX 1.47M 29500.0000 - 30000.0000 MHz 480MD7W 60.50 dBW BPSK up to 64QAM; Digital Data 27500.0000 - 29100.0000 MHz 480MD7W 60.50 dBW BPSK up to 64QAM; Digital Data 18800.0000 - 19300.0000 MHz 480MD7W 0.00 dBW BPSK up to 64QAM; Digital Data 17800.0000 - 18600.0000 MHz 480MD7W 0.00 dBW BPSK up to 64QAM; Digital Data Points of Communication: 1 - SPACEX (S2983/3018) - (NGSO) Page 1 of 34 SES-ASG-20191120-01531 E E890118 WITI License, LLC ( d/b/a C/O NEXSTAR MEDIA GROUP, INC. -

Trends in Space Commerce

Foreword from the Secretary of Commerce As the United States seeks opportunities to expand our economy, commercial use of space resources continues to increase in importance. The use of space as a platform for increasing the benefits of our technological evolution continues to increase in a way that profoundly affects us all. Whether we use these resources to synchronize communications networks, to improve agriculture through precision farming assisted by imagery and positioning data from satellites, or to receive entertainment from direct-to-home satellite transmissions, commercial space is an increasingly large and important part of our economy and our information infrastructure. Once dominated by government investment, commercial interests play an increasing role in the space industry. As the voice of industry within the U.S. Government, the Department of Commerce plays a critical role in commercial space. Through the National Oceanic and Atmospheric Administration, the Department of Commerce licenses the operation of commercial remote sensing satellites. Through the International Trade Administration, the Department of Commerce seeks to improve U.S. industrial exports in the global space market. Through the National Telecommunications and Information Administration, the Department of Commerce assists in the coordination of the radio spectrum used by satellites. And, through the Technology Administration's Office of Space Commercialization, the Department of Commerce plays a central role in the management of the Global Positioning System and advocates the views of industry within U.S. Government policy making processes. I am pleased to commend for your review the Office of Space Commercialization's most recent publication, Trends in Space Commerce. The report presents a snapshot of U.S. -

2001 Commercial Space Transportation Forecasts

2001 Commercial Space Transportation Forecasts Federal Aviation Administration's Associate Administrator for Commercial Space Transportation (AST) and the Commercial Space Transportation Advisory Committee (COMSTAC) May 2001 ABOUT THE ASSOCIATE ADMINISTRATOR FOR COMMERCIAL SPACE TRANSPORTATION (AST) AND THE COMMERCIAL SPACE TRANSPORTATION ADVISORY COMMITTEE (COMSTAC) The Federal Aviation Administration’s senior executives from the U.S. commercial Associate Administrator for Commercial Space space transportation and satellite industries, Transportation (AST) licenses and regulates U.S. space-related state government officials, and commercial space launch activity as authorized other space professionals. by Executive Order 12465, Commercial Expendable Launch Vehicle Activities, and the The primary goals of COMSTAC are to: Commercial Space Launch Act of 1984, as amended. AST’s mission is to license and • Evaluate economic, technological and regulate commercial launch operations to ensure institutional issues relating to the U.S. public health and safety and the safety of commercial space transportation industry property, and to protect national security and foreign policy interests of the United States • Provide a forum for the discussion of issues during commercial launch operations. The involving the relationship between industry Commercial Space Launch Act of 1984 and the and government requirements 1996 National Space Policy also direct the Federal Aviation Administration to encourage, • Make recommendations to the Administrator facilitate, and promote commercial launches. on issues and approaches for Federal policies and programs regarding the industry. The Commercial Space Transportation Advisory Committee (COMSTAC) provides Additional information concerning AST and information, advice, and recommendations to the COMSTAC can be found on AST’s web site, at Administrator of the Federal Aviation http://ast.faa.gov. -

1 Before the Federal Communications Commission Washington, DC

Before the Federal Communications Commission Washington, DC 20554 In the Matter of Intelsat License LLC, as debtor in File No. SAT-RPL-___________ possession Application for Authority to Launch and Operate Galaxy 32, a Replacement Satellite with New Frequencies, at 91.0º W.L. APPLICATION FOR AUTHORITY TO LAUNCH AND OPERATE GALAXY 32, A REPLACEMENT SATELLITE WITH NEW FREQUENCIES, AT 91.0º W.L. Intelsat License LLC, as debtor in possession (“Intelsat”), pursuant to Section 25.114 of the Federal Communications Commission’s (“FCC” or “Commission”) rules,1 hereby applies to launch and operate a C/Ku-band replacement satellite with new frequencies, to be known as Galaxy 32, at the 91.0° W.L. orbital location.2 Galaxy 32 is scheduled for launch in mid-2022 1 47 C.F.R. § 25.114. 2 The Commission’s rules permit replacement satellite applications in the 3700-4200 MHz band and these applications are not subject to the FCC’s 2018 filing freeze on new fixed satellite service (“FSS”) space station applications. See 47 C.F.R. § 2.106 n. NG182 (“In the band 3700- 4200 MHz…[a]pplications for extension, cancellation, replacement, or modification of existing space station authorizations in the band will continue to be accepted and processed normally.”); International Bureau Announces Temporary Filing Freeze on New Fixed-Satellite Service Space Station Applications in the 3.7-4.2 GHz Band, Public Notice, DA 18-640, 33 FCC Rcd 6119 (2018) (“The freeze does not apply to applications for modification of existing authorizations, relocations of existing space stations pursuant to the Commission’s fleet management policy, or to applications for replacement space stations.”); see also Expanding Flexible Use of the 3.7 to 4.2 GHz Band, Report and Order and Order of Proposed Modification, FCC 20-22, 35 FCC Rcd 2343, ¶ 115 n. -

PUBLIC NOTICE FEDERAL COMMUNICATIONS COMMISSION 445 12Th STREET S.W

PUBLIC NOTICE FEDERAL COMMUNICATIONS COMMISSION 445 12th STREET S.W. WASHINGTON D.C. 20554 News media information 202-418-0500 Internet: http://www.fcc.gov (or ftp.fcc.gov) TTY (202) 418-2555 Report No. SES-01597 Wednesday November 13, 2013 Satellite Communications Services Information re: Actions Taken The Commission, by its International Bureau, took the following actions pursuant to delegated authority. The effective dates of the actions are the dates specified. SES-ASG-20130828-00767 E E060321 AMS Spectrum Holdings, LLC Application for Consent to Assignment Grant of Authority Date Effective: 11/07/2013 Current Licensee: COOK TELECOM INC. FROM: COOK TELECOM INC. TO: AMS Spectrum Holdings, LLC No. of Station(s) listed: 1 SES-ASG-20131108-00963 E E000003 Omnitracs, Inc. Application for Consent to Assignment Grant of Authority Date Effective: 11/12/2013 Current Licensee: Omnitracs, Inc. FROM: OMNITRACS, INC. TO: Omnitracs, LLC No. of Station(s) listed: 12 SES-LIC-20130813-00723 E E130153 IHLAS HABER AJANSI IHA Application for Authority 11/12/2013 - 11/12/2028 Grant of Authority Date Effective: 11/12/2013 Class of Station: Temporary Fixed Earth Station Nature of Service: Fixed Satellite Service SITE ID: 1 LOCATION: N/A, USA, Washington, DC ANTENNA ID: 1 1.35 meters General Dynamics C125M 14000.0000 - 14500.0000 MHz 8M00G7F 57.00 dBW Digital Compressed Video Points of Communication: 1 - ALSAT - (ALSAT) Page 1 of 36 1 - GALAXY 17 (S2715) - (91 W.L.) 1 - INTELSAT 14 (S2785) - (45.0 W.L.) 1 - TELSTAR 11N (S2357) - (37.5 W.L.) SES-MFS-20130604-00470 E E000696 SES Americom, Inc. -

China Dream, Space Dream: China's Progress in Space Technologies and Implications for the United States

China Dream, Space Dream 中国梦,航天梦China’s Progress in Space Technologies and Implications for the United States A report prepared for the U.S.-China Economic and Security Review Commission Kevin Pollpeter Eric Anderson Jordan Wilson Fan Yang Acknowledgements: The authors would like to thank Dr. Patrick Besha and Dr. Scott Pace for reviewing a previous draft of this report. They would also like to thank Lynne Bush and Bret Silvis for their master editing skills. Of course, any errors or omissions are the fault of authors. Disclaimer: This research report was prepared at the request of the Commission to support its deliberations. Posting of the report to the Commission's website is intended to promote greater public understanding of the issues addressed by the Commission in its ongoing assessment of U.S.-China economic relations and their implications for U.S. security, as mandated by Public Law 106-398 and Public Law 108-7. However, it does not necessarily imply an endorsement by the Commission or any individual Commissioner of the views or conclusions expressed in this commissioned research report. CONTENTS Acronyms ......................................................................................................................................... i Executive Summary ....................................................................................................................... iii Introduction ................................................................................................................................... 1 -

Space Business Review June 2006 Space Smart

Milbank Space Business Review June 2006 Space Smart - A monthly round-up of space industry developments for the information of our clients and friends - Intelsat-PanAmSat Merger Completed June Satellite & Launch Service Orders At our publication deadline on July 3, Intelsat Ltd. On June 6, EADS Astrium and ARABSAT signed a announced the completion of its merger with contract for the construction of the BADR-6 (“Full PanAmSat Holding Corporation. As part of the Moon”) satellite. The spacecraft, scheduled for delivery transaction, Intelsat acquired all of the outstanding in 2008, is based on the Eurostar 2000+ platform shares of PanAmSat for approximately $3.2 billion, and will be equipped with 24 C- and 20 Ku-band with each share of PanAmSat common stock converted transponders and offer payload power of about 6 kW into the right to receive $25 plus a $0.00927 pro rata for its 15-year service life. BADR-6 will be positioned at quarterly dividend per share without interest. The total 26º E.L. and provide direct-to-home, interactive TV value of the transaction, including PanAmSat debt that and Internet services to the Middle East, North Africa was assumed or refinanced, is approximately $6.4 and a large part of sub-Saharan Africa. On June 8, billion. In late June, Intelsat released details of its Space Systems/Loral announced its selection by acquisition financing package, including $750 million Sirius Satellite Radio Inc. to build the SIRIUS FM-5 9¼% Senior Notes due 2016, $260 million Floating geostationary satellite. The spacecraft, scheduled for Rate Senior Notes (LIBOR + 600 basis points) due delivery in 4Q 2008, will be based on SS/L’s FS 1300 2013 and $1.330 billion 11¼% Senior Notes due 2016 platform and include an X-band uplink and S-band issued by Intelsat (Bermuda) Ltd. -

Is There Space for My Satellite?

PRIVATE & CONFIDENTIAL Is There Space for my Satellite? Navigating the commercial satellite launch process This webinar presentation is brought to you by Avascent Analytics and the Satellite Industry Association AVASCENT ANALYTICS Analytic arm of Avascent, Analytics develops robust global market data forecasts built on state of the art visualizations. AVASCENT AVASCENT INTERNATIONAL Growth-oriented management A global network of consulting firm with deep senior level strategic market expertise and rigorous advisors from the highest analytical methods. levels of gov’t, business, intel, and int’l affairs A RECOGNIZED FOCAL POINT FOR WITH ESTABLISHED ACTIVE THE SATELLITE INDUSTRY WORKING GROUPS Representing & advocating industry positions with key involved with regulatory issues; government policy makers on Capitol Hill and with the White House, services, public safety, export control policy, FCC and most Executive Branch departments & agencies. and international trade issues. FORMED BY SEVERAL MAJOR SATELLITE COMPANIES as a forum to discuss issues and develop industry-wide positions on shared business, regulatory and policy interests. AVASCENT | 2 The discussion will be moderated by Avascent’s Jonathan Beland and Caitlin Kennedy, and will feature a discussion with special guest Sam Black from Satellite Industry Association (SIA) Jonathan Beland Senior Market Analyst, FCC Orbital Intelligence Product Manager Jonathan specializes in providing market analysis and subject matter expertise pertaining to the space and telecoms industry. Jonathan has extensive experience providing government and commercial clients with insight on global launch and satellite manufacturing capabilities. Caitlin Kennedy Senior Market Analyst, FCC Orbital Intelligence Product Manager Caitlin specializes in maintaining the FCC Orbital Intelligence database. She has been with Avascent since August 2012, and has since heavily contributed to maintaining and enhancing Avascent Analytics’ suite of U.S. -

PUBLIC NOTICE FEDERAL COMMUNICATIONS COMMISSION 445 12Th STREET S.W

PUBLIC NOTICE FEDERAL COMMUNICATIONS COMMISSION 445 12th STREET S.W. WASHINGTON D.C. 20554 News media information 202-418-0500 Fax-On-Demand 202-418-2830; Internet: http://www.fcc.gov (or ftp.fcc.gov) TTY (202) 418-2555 Report No. SES-00839 Wednesday July 19, 2006 SATELLITE COMMUNICATIONS SERVICES INFORMATION RE: ACTIONS TAKEN The Commission, by its International Bureau, took the following actions pursuant to delegated authority. The effective dates of the actions are the dates specified. SES-ASG-20060510-00778 E E5349 Autotote Communications Services, Inc. Application for Consent to Assignment Grant of Authority Date Effective: 07/18/2006 Current Licensee: Autotote Communications Services, Inc. FROM: AUTOTOTE COMMUNICATONS SERVICES, INC. TO: SCIENTIFIC GAMES RACING, L.L.C. No. of Station(s) listed: 25 SES-ASG-20060512-00796 E E010322 COMCAST OF NEW YORK, LLC Application for Consent to Assignment Consummated Date Effective: 07/17/2006 Current Licensee: CARMEL CABLE TELEVISION, INC. FROM: CARMEL CABLE TELEVISION, INC. TO: COMCAST OF NEW YORK, LLC No. of Station(s) listed: 3 SES-ASG-20060512-00799 E E040129 Emmis Television License, LLC Application for Consent to Assignment Grant of Authority Date Effective: 07/12/2006 Current Licensee: Emmis Television License, LLC FROM: EMMIS COMMUNICATIONS CORPORATION TO: ORLANDO HEARST-ARGYLE TELEVISION, INC. No. of Station(s) listed: 1 Page 1 of 27 SES-ASG-20060523-00867 E E010180 CEBRIDGE ACQUISITION, L.P. Application for Consent to Assignment Consummated Date Effective: 07/17/2006 Current Licensee: COXCOM, INC. FROM: COXCOM, INC. TO: CEBRIDGE ACQUISITION, L.P. No. of Station(s) listed: 29 SES-ASG-20060523-00869 E E010148 CEBRIDGE ACQUISITION, L.P.