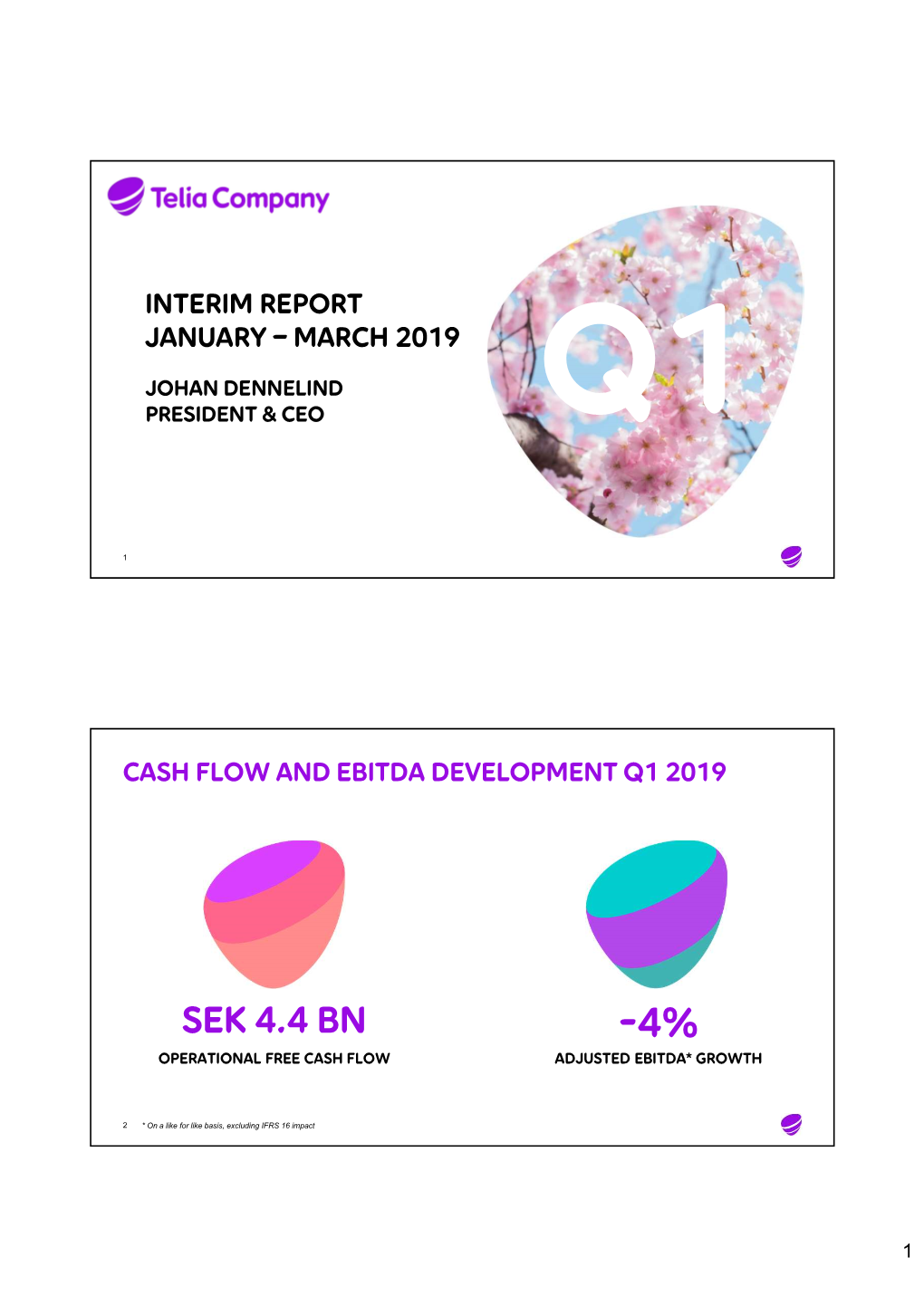

SEK 4.4 Bn -4% Operational Free Cash Flow Adjusted EBITDA* Growth

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Telia Company 4 På En Minut

BRINGING THE WORLD CLOSER ÅRS- OCH HÅLLBARHETS- REDOVISNING 2018 VÅRT FÖRETAG TELIA COMPANY 4 PÅ EN MINUT HÅLLBARHET VI STÅR FAST VID ETT ETISKT, ANSVARS- 8 FULLT FÖRETAGANDE VD 2018 VAR ETT 10 HÄNDELSERIKT ÅR TRENDER ETT KONSTANT ÖKANDE BEHOV 12 AV UPPKOPPLING Den reviderade årsredovisnin- Den av revisorerna översiktligt gen och koncernredovisningen granskade hållbarhetsinforma- INNEHÅLL omfattar sidorna 16–207 och tionen (som också utgör den 224. Den granskade bolagsstyr- lagstadgade hållbarhetsrap- ningsrapporten ingår på sidorna porten) omfattar sidorna 40–62 71–86. och 208–223. VÅRT FÖRETAG RÄKENSKAPER Telia Company på en minut ................................................... 4 Koncernens totalresultatrapporter ...................................... 87 2018 i korthet ......................................................................... 6 Koncernens balansrapporter ............................................... 88 Skapat värde .......................................................................... 7 Koncernens kassaflödesrapporter ...................................... 89 Hållbarhet – höjdpunkter ........................................................ 8 Koncernens rapporter över förändringar i eget kapital ....... 90 Styrelseordförandens kommentar .......................................... 9 Koncernens noter ................................................................ 91 Koncernchefens kommentar ................................................ 10 Moderbolagets resultaträkningar ..................................... -

Turkcell Annual Report 2010

TURKCELL ANNUAL REPORT 2010 GET MoRE oUT of LIfE WITh TURKCELL CoNTENTS PAGE our Vision / our Values / our Strategic Priorities 4 Turkcell Group in Numbers 6 Turkcell: Leading Communication and Technology Company 8 Letter from the Chairman 10 Board Members 12 Letter from the CEo 14 Executive officers 16 Superior Technologies 22 More Advantages 32 Best Quality Service 40 More Social Responsibility 46 Awards 53 Managers of Turkcell Affiliates 54 Subsidiaries 56 human Resources 62 Mobile Telecommunication Sector 66 International Ratings 72 Investor Relations 74 Corporate Governance 78 Turkcell offices 95 Consolidated financial Statement and Independent Audit Report 96 Dematerialization of The Share Certificates of The Companies That Are Traded on The Stock Exchange 204 The Board’s Dividend Distribution Proposal 205 2 3 oUR VISIoN oUR STRATEGIC PRIoRITIES To ease and enrich the lives of our customers with communication and As a Leading Communication and Technology Company, technology solutions. • to grow in our core mobile communication business through increased use of voice and data, • to grow our existing international subsidiaries with a focus on profitability, oUR VALUES • to grow in the fixed broadband business by creating synergy among Turkcell Group companies through our fiber optic infrastructure, • We believe that customers come first • to grow in the area of mobility, internet and convergence through new • We are an agile team business opportunities, • We promote open communication • to grow in domestic and international markets through communications, • We are passionate about making a difference technology and new business opportunities, • We value people • to develop new service platforms that will enrich our relationship with our customers through our technical capabilities. -

3 1 Jan. 2013

KvK Rotterdam/Rotterdam 3 1 JAN. 2013 FINTUR HOLDINGS B.V. CONSOLIDATED FINANCIAL STATEMENfS AT 31 DECEMBER 2011 TOGETHER WITH INDEPENDENf AUDITORS' REPORT adopted by the general meeting of shareholders by resolution passed on 29 Jamuary 2013 vastgesteld door de algemene vergadering van aandeelhouders bij besluit op 29 januari 2013 Prkt.'\\illl:rhou.sc(;oopers A<:countm11s N. \'. For idenlifirolion purpo~ouly lo pwc FINTUR HOLDINGS B.V. CONTENTS CONTENTS PAGES REPORT OF THE BOARD OF DIRECTORS .......................... 3-5 CONSOLIDATED FINANCIAL STATEMENTS................................................................... 6 - 58 CONSOLIDATED BALANCE SHEETS................................................................................. 7 CONSOLIDATED STATEMENTS OF INCOME.................................................................. 9 CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME............................. 10 CONSOLIDATED STATEMENTS OF CHANGES IN EQUITY......................................... 11 CONSOLIDATED STATEMENTS OF CASH FLOWS.......................................................... 12 NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS.................................... 13-58 NOTE I ORGANISATION AND NATURE OF OPERATIONS............................................................................... 7-8 NOTE 2 BASIS OF PREPARATION AND SUMMARY OF SIGNIFICANT RELEVANT ACCOUNTING POLICIES.......................................................................................................................... 9-33 NOTE 3 SEGMENT -

Ready for Upload GCD Wls Networks

LTE‐ Region Country Operator LTE 5G Advanced Eastern Europe 93 60 18 Albania Total 320 Albania ALBtelecom 100 ONE Telecommunications (formerly Albania Telekom Albania) 110 Albania Vodafone Albania 110 Armenia Total 330 Armenia MTS Armenia (Viva‐MTS) 110 Armenia Ucom 110 Armenia VEON Armenia (Beeline) 110 Azerbaijan Total 430 Azerbaijan Azercell 100 Azerbaijan Azerfon (Nar) 110 Azerbaijan Bakcell 110 Azerbaijan Naxtel (Nakhchivan) 110 Belarus Total 431 Belarus A1 Belarus 101 Belarus Belarusian Cloud Technologies (beCloud) 110 Belarusian Telecommunications Network Belarus (BeST, life:)) 110 Belarus MTS Belarus 110 Bosnia‐Herzegovina Total 310 Bosnia‐Herzegovina BH Telecom 110 Bosnia‐Herzegovina HT Mostar (HT Eronet) 100 Bosnia‐Herzegovina Telekom Srpske (m:tel) 100 Bulgaria Total 530 Bulgaria A1 Bulgaria (Mobiltel) 110 Bulgaria Bulsatcom 100 Bulgaria T.com (Bulgaria) 100 Bulgaria Telenor Bulgaria 110 Bulgaria Vivacom (BTC) 110 Croatia Total 331 Croatia A1 Hrvatska (formerly VIPnet/B.net) 110 Croatia Hrvatski Telekom (HT) 111 Croatia Tele2 Croatia 110 Czech Republic Total 433 Czech Republic Nordic Telecom 100 Czech Republic O2 Czech Republic (incl. CETIN) 111 Czech Republic T‐Mobile Czech Republic 111 Czech Republic Vodafone Czech Republic 111 Estonia Total 331 Estonia Elisa Eesti (incl. Starman) 110 Estonia Tele2 Eesti 110 Telia Eesti (formerly Eesti Telekom, EMT, Estonia Elion) 111 Georgia Total 630 Georgia A‐Mobile (Abkhazia) 100 Georgia Aquafon GSM (Abkhazia) 110 Georgia MagtiCom 110 Georgia Ostelecom (MegaFon) (South Ossetia) 100 Georgia -

Before the FEDERAL COMMUNICATIONS COMMISSION Washington, D.C

Before the FEDERAL COMMUNICATIONS COMMISSION Washington, D.C. 20554 In the Matter of ) ) Telia Company AB, Transferor ) WC Docket No. 20-___ ) Telia Carrier U.S. Inc., Licensee ) ) and Oura BidCo US, Inc., Transferee ) ITC-T/C-2020-_____ ) Joint Application for Consent to Transfer ) Control of International and Domestic Authority ) Pursuant to Section 214 of the ) Communications Act of 1934, as Amended ) JOINT APPLICATION FOR CONSENT TO TRANSFER CONTROL OF DOMESTIC AND INTERNATIONAL AUTHORITY PURSUANT TO SECTION 214 OF THE COMMUNICATIONS ACT OF 1934, AS AMENDED Pursuant to Section 214 of the Communications Act of 1934, as amended, ("the Act"), 47 U.S.C. § 214, and Sections 63.04 and 63.24 of the Commission's rules, 47 C.F.R. §§ 63.04 and 63.24, Telia Company AB (“Transferor” or “Telia Company”), Telia Carrier U.S. Inc. (“Licensee” or “Telia Carrier”), and Oura BidCo US, Inc. (“Transferee” or “BidCo US”) hereby request Commission consent to the transfer of control of domestic and international Section 214 authority held by Telia Carrier from Telia Company to Oura BidCo US, Inc., which is an indirect wholly owned U.S. subsidiary of Polhem Infra KB.1 This Joint Application is being filed simultaneously with the Wireline Competition Bureau and the International Bureau. I. Description of the Applicants A. Transferor and Licensee 1 Transferor, Licensee and Transferee may be collectively referred to as the “Applicants” herein. Licensee Telia Carrier has operated in the U.S. since 1996 and operates a nationwide fiber-optic communications network. Licensee historically has provided carrier-grade or “wholesale” services to carriers, content providers, operators and enterprises and offers a range of information services and telecommunications services. -

Turkcell the Digital Operator

Turkcell the Digital Operator Turkcell Annual Report 2018 About Turkcell Turkcell is a digital operator headquartered in Turkey, serving its customers with its unique portfolio of digital services along with voice, messaging, data and IPTV services on its mobile and fixed networks. Turkcell Group companies operate in 5 countries – Turkey, Ukraine, Belarus, Northern Cyprus, Germany. Turkcell launched LTE services in its home country on April 1st, 2016, employing LTE-Advanced and 3 carrier aggregation technologies in 81 cities. Turkcell offers up to 10 Gbps fiber internet speed with its FTTH services. Turkcell Group reported TRY 21.3 billion revenue in FY18 with total assets of TRY 42.8 billion as of December 31, 2018. It has been listed on the NYSE and the BIST since July 2000, and is the only NYSE-listed company in Turkey. Read more at www.turkcell.com.tr/english-support All financial results in this annual report are prepared in accordance with International Financial Reporting Standards (IFRS) and expressed in Turkish Lira (TRY or TL) unless otherwise stated. TABLE OF CONTENTS TRY Turkcell Group 16 Chairman’s Message 21.3 20 Board of Directors 22 Message from the CEO billion 26 Executive Officers 28 Top Management of Subsidiaries REVENUES 30 Turkcell Group 31 Our Vision, Target, Strategy and Approach 32 2018 at a Glance 34 2018 Highlights 36 The World’s 1st Digital Operator Brand: Lifecell 37 Turkcell’s Digital Services 2018 Operations 38 Exemplary Digital Operator 40 Our Superior Technology 41.3% 46 Our Consumer Business EBITDA 52 Our -

Annual and Sustainability Report 2020 Content

BETTER CONNECTED LIVING ANNUAL AND SUSTAINABILITY REPORT 2020 CONTENT OUR COMPANY Telia Company at a glance ...................................................... 4 2020 in brief ............................................................................ 6 Comments from the Chair ..................................................... 10 Comments from the CEO ...................................................... 12 Trends and strategy ............................................................... 14 DIRECTORS' REPORT Group development .............................................................. 20 Country development ........................................................... 38 Sustainability ........................................................................ 48 Risks and uncertainties ......................................................... 80 CORPORATE GOVERNANCE Corporate Governance Statement ......................................... 90 Board of Directors .............................................................. 104 Group Executive Management ............................................ 106 FINANCIAL STATEMENTS Consolidated statements of comprehensive income ........... 108 Consolidated statements of financial position ..................... 109 Consolidated statements of cash flows ............................... 110 Consolidated statements of changes in equity .................... 111 Notes to consolidated financial statements ......................... 112 Parent company income statements ................................... -

Kcell Is a Market Leader Again Mobile Network Antennas: Myths and Reality Dual Carrier: 3G Evolution in Progress Publisher: Apriori Communications LLP

Specialized telecommunication magazine of Kazakhstan september — november / №3 [27] Kcell is a Market Leader Again Mobile Network Antennas: Myths and Reality Dual Carrier: 3G Evolution in Progress Publisher: Apriori Communications LLP Editor-in-chief: Aida Dossayeva Editorial Director: Natalia Yeskova Director: Dinara Sherieva Design: David Djubayev [www.vkartinke.com] Authors of Publications: Natalya Yeskova Ivan Glushchenko Aisha Arynova Sanzhar Bimamirov Dmitriy Paramonov Photographs: Saken Nigmashev Valeriy Ayapov Translation into the Kazakh and English languages: InterBridge-A Translation Bureau Read VOX.com on your mobile phone Address of the Editorial Office: 118 Makatayev str., 6 apt. 050000, Almaty, Republic of Kazakhstan tel.: 8 [727] 232-71-40 mobile.: +7 701 211 31 77 e-mail: [email protected] Printed in Gerona Print House 30a/3 Satpayev str., office 124 Tel.: 7 (727) 250-47-40, 398-94-59, 398-94-60 The magazine is re-registered with the Ministry of Communications and Information of the RoK as of 19.10.2011 under No.12052-Ж CONTENTS NEWS 4 TeliaSonera News 8 Kcell News ANALYTICS 6 Kcell is a Market Leader Again 22 Mobile Network Antennas: Myths and Reality INTERVIEW 26 The Road Project: What Matters Is There's Almost Always a Connection MARKET 12 Kcell Cloud: Taming Clouds 14 Dual Carrier: 3G Evolution in Progress 16 How to Maximize Your Smartphone's Potential 18 Roaming: Make Yourself At Home! 20 A Pretty Number Is Quick and Convenient 34 Smartphones with Dual Carrier Support PHOTO REPORTAGE 30 TEDxAlmaty. Extra is New Rationality 4 5 news TeliaSonera International the interconnection services. The net sales Net sales in the Eurasian branch of Carrier Presents Anywhereization Trend figures remained stable in the local currency, TeliaSonera (BA Eurasia) increased by 11.1 excluding acquisitions and divestments. -

Telia Company – Annual and Sustainability Report 2019

BRINGING THE WORLD CLOSER ANNUAL AND SUSTAINABILITY REPORT 2019 CONTENT OUR COMPANY Telia Company in one minute ................................................ 4 2019 in brief ............................................................................ 6 How we create value ............................................................. 8 Comments from the CEO ..................................................... 10 Trends and strategy .............................................................. 12 DIRECTORS' REPORT Group development ............................................................. 16 Country development .......................................................... 32 Sustainability ....................................................................... 41 Risks and uncertainties ....................................................... 62 CORPORATE GOVERNANCE Corporate Governance Statement ....................................... 70 Board of Directors ............................................................... 82 Group Executive Management ............................................ 84 FINANCIAL STATEMENTS Consolidated statements of comprehensive income .......... 86 Consolidated statements of financial position .................... 87 Consolidated statements of cash flows .............................. 88 Consolidated statements of changes in equity ................... 89 Notes to consolidated financial statements ........................ 90 Parent company income statements.................................. 182 Parent company -

Prepared for Upload GCD Wls Networks

LTE‐ LTE‐ Region Country Operator LTE Advanced 5G Advanced Pro Eastern Europe 92 57 4 3 Albania Total 32 0 0 Albania ALBtelecom 10 0 0 Albania Telekom Albania 11 0 0 Albania Vodafone Albania 11 0 0 Armenia Total 31 0 0 Armenia MTS Armenia (VivaCell‐MTS) 10 0 0 Armenia Ucom (formerly Orange Armenia) 11 0 0 Armenia VEON Armenia (Beeline) 10 0 0 Azerbaijan Total 43 0 0 Azerbaijan Azercell 10 0 0 Azerbaijan Azerfon (Nar) 11 0 0 Azerbaijan Bakcell 11 0 0 Azerbaijan Naxtel (Nakhchivan) 11 0 0 Belarus Total 42 0 0 Belarus A1 Belarus (formerly VELCOM) 10 0 0 Belarus Belarusian Cloud Technologies (beCloud) 11 0 0 Belarus Belarusian Telecommunications Network (BeST, life:)) 10 0 0 Belarus MTS Belarus 11 0 0 Bosnia and Total Herzegovina 31 0 0 Bosnia and Herzegovina BH Telecom 11 0 0 Bosnia and Herzegovina HT Mostar (HT Eronet) 10 0 0 Bosnia and Herzegovina Telekom Srpske (m:tel) 10 0 0 Bulgaria Total 53 0 0 Bulgaria A1 Bulgaria (Mobiltel) 11 0 0 Bulgaria Bulsatcom 10 0 0 Bulgaria T.com (Bulgaria) 10 0 0 Bulgaria Telenor Bulgaria 11 0 0 Bulgaria Vivacom (BTC) 11 0 0 Croatia Total 33 1 0 Croatia A1 Hrvatska (formerly VIPnet/B.net) 11 1 0 Croatia Hrvatski Telekom (HT) 11 0 0 Croatia Tele2 Croatia 11 0 0 Czechia Total 43 0 0 Czechia Nordic Telecom (formerly Air Telecom) 10 0 0 Czechia O2 Czech Republic (incl. CETIN) 11 0 0 Czechia T‐Mobile Czech Republic 11 0 0 Czechia Vodafone Czech Republic 11 0 0 Estonia Total 33 2 0 Estonia Elisa Eesti (incl. -

Telia Company – Års- Och Hållbarhetsredovisning 2019

BRINGING THE WORLD CLOSER ÅRS- OCH HÅLLBARHETS - REDOVISNING 2019 INNEHÅLL VÅRT FÖRETAG Telia Company på en minut ................................................... 4 2019 i korthet ......................................................................... 6 Hur vi skapar värde ............................................................... 8 Koncernchefens kommentar ................................................ 10 Trender och strategi ............................................................. 12 FÖRVALTNINGSBERÄTTELSE Koncernutveckling ............................................................... 16 Utveckling per land ............................................................. 32 Hållbarhet ............................................................................ 41 Risker och osäkerhetsfaktorer ............................................. 62 BOLAGSSTYRNING Bolagsstyrningsrapport ........................................................ 70 Styrelse ................................................................................ 82 Koncernledning ................................................................... 84 RÄKENSKAPER Koncernens totalresultatrapporter ...................................... 86 Koncernens balansrapporter ............................................... 87 Koncernens kassaflödesrapporter ...................................... 88 Koncernens rapporter över förändringar i eget kapital ....... 89 Koncernens noter ................................................................ 90 Moderbolagets resultaträkningar -

Ready for Upload GCD Wls Networks

LTE‐ LTE‐ REGION COUNTRY OPERATOR LTE Advanced Advanced Pro Eastern Europe 92 55 2 Albania Total 320 Albania ALBtelecom 100 Albania Telekom Albania 110 Albania Vodafone Albania 110 Armenia Total 310 Armenia MTS Armenia (VivaCell‐MTS) 100 Armenia Ucom (formerly Orange Armenia) 110 Armenia VEON Armenia (Beeline) 100 Azerbaijan Total 430 Azerbaijan Azercell 100 Azerbaijan Azerfon (Nar) 110 Azerbaijan Bakcell 110 Azerbaijan Naxtel (Nakhchivan) 110 Belarus Total 420 Belarus Belarusian Cloud Technologies (beCloud) 110 Belarusian Telecommunications Network Belarus (BeST, life:)) 100 Belarus MTS Belarus 110 Belarus VELCOM (A1 Belarus) 100 Bosnia and Herzegovina Total 300 Bosnia and Herzegovina BH Telecom 100 Bosnia and Herzegovina HT Mostar (HT Eronet) 100 Bosnia and Herzegovina Telekom Srpske (m:tel) 100 Bulgaria Total 530 Bulgaria A1 Bulgaria (Mobiltel) 110 Bulgaria Bulsatcom 100 Bulgaria T.com (Bulgaria) 100 Bulgaria Telenor Bulgaria 110 Bulgaria Vivacom (BTC) 110 Croatia Total 321 Croatia A1 Croatia (VIPnet incl. B.net) 111 Croatia Hrvatski Telekom (HT) 110 Croatia Tele2 Croatia 100 Czech Republic Total 430 Czech Republic Nordic Telecom (formerly Air Telecom) 100 Czech Republic O2 Czech Republic (incl. CETIN) 110 Czech Republic T‐Mobile Czech Republic 110 Czech Republic Vodafone Czech Republic 110 Estonia Total 330 Estonia Elisa Eesti (incl. Starman) 110 Estonia Tele2 Eesti 110 Telia Eesti (formerly Eesti Telekom, EMT, Estonia Elion) 110 Georgia Total 630 Georgia A‐Mobile (Abkhazia) 100 Georgia Aquafon GSM (Abkhazia) 110 Georgia MagtiCom