Audit Report on the Accounts of Earthquake Reconstruction & Rehabilitation Authority Audit Year 2015-16

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Dasu Hydropower Project

Public Disclosure Authorized PAKISTAN WATER AND POWER DEVELOPMENT AUTHORITY (WAPDA) Public Disclosure Authorized Dasu Hydropower Project ENVIRONMENTAL AND SOCIAL ASSESSMENT Public Disclosure Authorized EXECUTIVE SUMMARY Report by Independent Environment and Social Consultants Public Disclosure Authorized April 2014 Contents List of Acronyms .................................................................................................................iv 1. Introduction ...................................................................................................................1 1.1. Background ............................................................................................................. 1 1.2. The Proposed Project ............................................................................................... 1 1.3. The Environmental and Social Assessment ............................................................... 3 1.4. Composition of Study Team..................................................................................... 3 2. Policy, Legal and Administrative Framework ...............................................................4 2.1. Applicable Legislation and Policies in Pakistan ........................................................ 4 2.2. Environmental Procedures ....................................................................................... 5 2.3. World Bank Safeguard Policies................................................................................ 6 2.4. Compliance Status with -

Languages of Kohistan. Sociolinguistic Survey of Northern

SOCIOLINGUISTIC SURVEY OF NORTHERN PAKISTAN VOLUME 1 LANGUAGES OF KOHISTAN Sociolinguistic Survey of Northern Pakistan Volume 1 Languages of Kohistan Volume 2 Languages of Northern Areas Volume 3 Hindko and Gujari Volume 4 Pashto, Waneci, Ormuri Volume 5 Languages of Chitral Series Editor Clare F. O’Leary, Ph.D. Sociolinguistic Survey of Northern Pakistan Volume 1 Languages of Kohistan Calvin R. Rensch Sandra J. Decker Daniel G. Hallberg National Institute of Summer Institute Pakistani Studies of Quaid-i-Azam University Linguistics Copyright © 1992 NIPS and SIL Published by National Institute of Pakistan Studies, Quaid-i-Azam University, Islamabad, Pakistan and Summer Institute of Linguistics, West Eurasia Office Horsleys Green, High Wycombe, BUCKS HP14 3XL United Kingdom First published 1992 Reprinted 2002 ISBN 969-8023-11-9 Price, this volume: Rs.300/- Price, 5-volume set: Rs.1500/- To obtain copies of these volumes within Pakistan, contact: National Institute of Pakistan Studies Quaid-i-Azam University, Islamabad, Pakistan Phone: 92-51-2230791 Fax: 92-51-2230960 To obtain copies of these volumes outside of Pakistan, contact: International Academic Bookstore 7500 West Camp Wisdom Road Dallas, TX 75236, USA Phone: 1-972-708-7404 Fax: 1-972-708-7433 Internet: http://www.sil.org Email: [email protected] REFORMATTING FOR REPRINT BY R. CANDLIN. CONTENTS Preface............................................................................................................viii Maps................................................................................................................. -

Pak-Swiss INRMP (2010) Study on Timber Harvesting Ban in NWFP

2 Study on timber harvesting ban in NWFP, Pakistan Disclaimer This study was conducted in an independent manner. The views expressed in this study do not present the official position of the NWFP Forest Department and the funding agency (SDC) but those of the Study Team ISBN: 969-9082-02-x Parts of this publication may be copied with proper citation in favour of the Authors and the publishing organization Integrated Natural Resource Management Project 3 This publication is based on 15 months continuous engagement of the team in collecting data, analyses and documentation by the study team. Initiated by: Pak-Swiss Integrated Natural Resource Management Project (INRMP) on request of the NWFP Forest Department in the first yearly planning workshop of the project, to conduct an independent study The Study Team and Authors: Dr. Knut M. Fischer (Team Leader) Muhammad Hanif Khan Alamgir Khan Gandapur Abdul Latif Rao Raja Muhammad Zarif Hamid Marwat Publication editing: Arjumand Nizami Syed Nadeem Bukhari Fatima Daud Kamal Layout: Salman Beenish Printing: PanGraphics (Pvt) Ltd., Islamabad Available from: Swiss Agency for Development and Cooperation (SDC) Intercooperation Delegation Office Pakistan INRMP / NWFP Forest Department, Planning, Monitoring and Evaluation Circle, Peshawar Cover photographs: Aamir Rana Amina Ijaz Arjumand Nizami Irshad Ali Mian Roshan Ara Tahir Saleem Technical cooperation: Intercooperation Head Office Berne, Switzerland and Pakistan Pak-Swiss Integrated Natural Resource Management Project (INRMP) GIS lab of Forest Planning and Monitoring Circle, NWFP Forest Department Published by Intercooperation Pakistan through Pak-Swiss Integrated Natural Resource Management Project (INRMP). INRMP is funded by Swiss Agency for Development and Cooperation (SDC) 4 Study on timber harvesting ban in NWFP, Pakistan About Intercooperation Intercooperation (IC) in Pakistan and worldwide has been actively engaged in forestry sector right from its inception in 1982. -

District Name Department DDO Description Detail Object

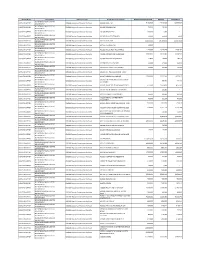

District Name Department DDO Description Detail Object Description Budget Estimates 2017-18 Releases Expenditure KD21C09 REVENUE & ESTATE KOHISTAN UPPER KD6108 Deputy Commisioner Kohistan A01101 BASIC PAY 9,184,500 12,316,580 10,833,687 DEPARTMENT KD21C09 REVENUE & ESTATE KOHISTAN UPPER KD6108 Deputy Commisioner Kohistan A01102 PERSONAL PAY 50,000 50,000 - DEPARTMENT KD21C09 REVENUE & ESTATE KOHISTAN UPPER KD6108 Deputy Commisioner Kohistan A01103 SPECIAL PAY 100,000 5,000 - DEPARTMENT KD21C09 REVENUE & ESTATE KOHISTAN UPPER KD6108 Deputy Commisioner Kohistan A01105 QUALIFICATION PAY 50,000 22,250 2,250 DEPARTMENT KD21C09 REVENUE & ESTATE KOHISTAN UPPER KD6108 Deputy Commisioner Kohistan A01151 BASIC PAY 15,629,500 16,706,650 15,067,318 DEPARTMENT KD21C09 REVENUE & ESTATE KOHISTAN UPPER KD6108 Deputy Commisioner Kohistan A01152 PERSONAL PAY 15,000 - - DEPARTMENT KD21C09 REVENUE & ESTATE KOHISTAN UPPER KD6108 Deputy Commisioner Kohistan A01202 HOUSE RENT ALLOWANCE 1,475,000 1,618,520 1,269,132 DEPARTMENT KD21C09 REVENUE & ESTATE KOHISTAN UPPER KD6108 Deputy Commisioner Kohistan A01203 CONVEYANCE ALLOWANCE 3,382,000 3,813,790 3,058,502 DEPARTMENT KD21C09 REVENUE & ESTATE KOHISTAN UPPER KD6108 Deputy Commisioner Kohistan A01207 WASHING ALLOWANCE 19,800 70,800 18,450 DEPARTMENT KD21C09 REVENUE & ESTATE KOHISTAN UPPER KD6108 Deputy Commisioner Kohistan A01208 DRESS ALLOWANCE 12,000 19,600 12,150 DEPARTMENT KD21C09 REVENUE & ESTATE KOHISTAN UPPER KD6108 Deputy Commisioner Kohistan A0120D INTEGRATED ALLOWANCE 92,000 92,000 70,200 DEPARTMENT -

Current Budget Estimates 2016-17

District Name Department DDO Description Detail Object Description Budget Estimates 2016-17 KD6108 DEPUTY COMMISSIONER KOHISTAN UPPERKD21C09 REVENUE & ESTATE DEPARTMENT A01101 BASIC PAY OF OFFICER 10,246,500 KOHISTAN KD6108 DEPUTY COMMISSIONER KOHISTAN UPPERKD21C09 REVENUE & ESTATE DEPARTMENT A01102 PERSONAL PAY 50,000 KOHISTAN KD6108 DEPUTY COMMISSIONER KOHISTAN UPPERKD21C09 REVENUE & ESTATE DEPARTMENT A01103 SPECIAL PAY 100,000 KOHISTAN KD6108 DEPUTY COMMISSIONER KOHISTAN UPPERKD21C09 REVENUE & ESTATE DEPARTMENT A01105 QUALIFICATION PAY 50,000 KOHISTAN KD6108 DEPUTY COMMISSIONER KOHISTAN UPPERKD21C09 REVENUE & ESTATE DEPARTMENT A01151 BASIC PAY OTHER STAFF 15,743,500 KOHISTAN KD6108 DEPUTY COMMISSIONER KOHISTAN UPPERKD21C09 REVENUE & ESTATE DEPARTMENT A01152 PERSONAL PAY 15,000 KOHISTAN KD6108 DEPUTY COMMISSIONER KOHISTAN UPPERKD21C09 REVENUE & ESTATE DEPARTMENT A01202 HOUSE RENT ALLOWANCE 4,623,000 KOHISTAN KD6108 DEPUTY COMMISSIONER KOHISTAN UPPERKD21C09 REVENUE & ESTATE DEPARTMENT A01203 CONVEYANCE ALLOWANCE 5,520,000 KOHISTAN KD6108 DEPUTY COMMISSIONER KOHISTAN UPPERKD21C09 REVENUE & ESTATE DEPARTMENT A01207 WASHING ALLOWANCE 34,500 KOHISTAN KD6108 DEPUTY COMMISSIONER KOHISTAN UPPERKD21C09 REVENUE & ESTATE DEPARTMENT A01208 DRESS ALLOWANCE 23,000 KOHISTAN KD6108 DEPUTY COMMISSIONER KOHISTAN UPPERKD21C09 REVENUE & ESTATE DEPARTMENT A0120D INTEGRATED ALLOWANCE 287,500 KOHISTAN KD6108 DEPUTY COMMISSIONER KOHISTAN UPPERKD21C09 REVENUE & ESTATE DEPARTMENT A0120X ADHOC ALLOWANCE - 2010 8,337,500 KOHISTAN KD6108 DEPUTY COMMISSIONER KOHISTAN -

Project Compilation Report on Two Weeks Campaig to Celebrate 16 Days of Acti

PROJECT COMPLETION REPORT DISABILITY UNIT DISTRICT KOHISTAN SALIK DEVELOPMENT FOUNDATION (SDF) KOHISTAN (Khyber Pukhtoonkhwa) 2 Table of Contents Topic Page Number 1. Table of Contents ………………………………………………….………………… 2-3 2. List of Acronyms ………………………………………………………….………….. 4 3. Project Identification Information............................................. 5 4. Training Objectives ……………………………………………………………. 6 5. Area Background ……………………………………………………………….. 6 6. Map of District Kohistan …………………………………………………….. 7 7. Union Council Wise Population of Kohistan ………………………….. 7 8. Rationale of the Project …………………………………………………… 8 9. Pre-Training Activities ………………………………………………………. 8 10. Dialogue between the SDF and Master Trainers (Tailoring) ….. 8 11. Signing of MOU ……………………………………………………………….. 9 12. Identification of Trainees …………………………………………………. 9 13. Training formally takes start (May 24, 2011) …………………….. 9 14. Tailoring Course ……………………………………………………………… 10 ______________________________________________________________________________ Salik Development Foundation Disability Program Kohistan 3 15. Opening Ceremony (May 24, 2011) ………………………………….. 11 16. Certificates Awarding Ceremony (June 22, 2011) ………………….. 13 17. Requisition for provision of Training Kits (Sewing Machine)……… 18 18. Distribution ceremony of Tailoring Kits ………………………………..…19 19. Graph of distribution of Tailoring Kits and Assistive Devices ……….20 20. Picture Gallary ………………………………………………………………………. 24 21. Community awareness regarding PWD……………………………………… 25 ______________________________________________________________________________ -

Roads &Bridges

“BUILD BACK BETTER” RECONSTRUCTION AND REHABILITATION STARTEGY TRANSPORT (ROADS &BRIDGES) SECTOR Government of Pakistan Earthquake Reconstruction and Rehabilitation Authority Prime Minister’s Secretariat (Public) 1 Abbreviations ADB Asian Development Bank AJK Azad Jammu and Kashmir DFID Department for International Development, UK DRU District Reconstruction Unit DRAC District Advisory Committee ERRA Earthquake Rehabilitation and Reconstruction Authority EIRR Economic Internal Rate of Return EIA Environmental Impact Assessment Est Estimated FHA Frontier Highway Authority IEE Initial Environmental Examination JBIC Japan Bank for International Cooperation JICA Japan International Cooperation Agency Km Kilometer LG&RD Local Government and Rural Development Department NGO Non-governmental Organization NHA National Highway Authority NWFP North West Frontier Province O & M Operation and Maintenance PERRA Provincial Reconstruction and Rehabilitation Authority PIU Project Implementation Unit PWD Public Works Department SERRA State Reconstruction and Rehabilitation Authority TMA Tehsil Municipal Administration W&S Works and Services Department 2 TABLE OF CONTENTS SR. NO CONTENTS PAGE EXECUTIVE SUMMARY 6 1. INTRODUCTION 9 1.1 Background 9 1.2 Summary of Damages and Needs 10 2. THE STRATEGY 12 2.1 Vision 12 2.2 Objectives 12 2.3 Scope 12 2.4 Guiding Principles 12 2.5 Errors or Omissions 14 2.6 Methodology 14 2.6.1 Reconstruction Approach 14 2.6.1.1 Improved disaster preparedness and service 14 delivery 2.6.1.2 Inter- sectoral Approach 15 2.6.1.3 Community Participation 15 2.6.1.4 Capacity Building: 15 2.6.1.5 Linkages & Partnership 15 2.6.1.6 Coordination 16 2.6.1.7 Management 16 2.6.1.8 Quality assurance 16 3. -

District Wise Details of De-Registered Npos / Ngos Registered Under the Societies Registration Act, 1860

DISTRICT WISE DETAILS OF DE-REGISTERED NPOS / NGOS REGISTERED UNDER THE SOCIETIES REGISTRATION ACT, 1860 District Chitral Upper S.No. Name of NPOs Address 1. Shoungush Youth Welfare Organization Ohoshush Owir Chitral (Upper) 2. Shami Welfare Society Village Chinar, Tehsil Mastuj, District Chitral (Upper) District Chitral Lower S.No. Name of NPOs Address 1. Nidaul Harmain Shar e faine Foundation Gool Door Near Old Zari Bank District Chitral (Lower) 2. Alian Foundation Village Alyian Near Chitral Scouts Cantt Teh & Dist Chitral (Lower) 3. Association for Sustainable Development (ASD) Chinar Inn Market Office No 26 Shahi Chitral (lower) 4. ANWAAZ Polo ground Main bazar Garam Chashma Chitral (Lower) KP District Dir Upper S.No. Name of NPOs Address 1. Socio Economic Advancement Society (SEAS) Main Bazar Wari Dir upper District Dir Lower S.No. Name of NPOs Address 1. Social Workers Awareness& Rural Development Naway Kalay Nasafa Talaah Tehsil Temergarah district Dir Lower (SWARD) 2. Social Awareness and Rural Development Temergarah district Dir Lower 3. Human Relief Trust Chakdara opposite to ID card office university road chakdara Dir lower 4. Organization for Human Development Program (CHDP) 3rd Floor Sanna Market China Plaza Chakdara The Adenzai district Dir Lower 5. Agency for Change & Transparency Timergara, district Dir Lower, Khyber Pakhtunkhwa, Pakistan. 6. Zoonoses Control Committee (ZCC) PCA Form Services Bypass Road Timergarah Dir Lower 7. Helping People Foundation (HPF) Gulabad Tehsil Adenzai District Lower Dir KP 8. Health Education Disaster Vulnerable Area Identification Dir Lower Tehsil Adenzai PO Chakdara Mandi program (MEDVAIP) NGO 9. Qalam Foundation Temergarah District Dir Lower. District Dera Ismail Khan S.No. -

Pakistan, 2001

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized i Environmental Assessment and Review Framework (EARF) for Dasu-Islamabad TL Project TOC TABLE OF CONTENTS LIST OF ABBREVIATION ........................................................................................................ vii EXECUTIVE SUMMARY ...................................................................................................... ES-1 CHAPTER 1: INTRODUCTION ...............................................................................................1-1 1.1 RATIONALE ..............................................................................................................1-1 1.2 AN OVERVIEW OF THE PROJECT .............................................................................1-1 1.3 NEED FOR PREPARATION OF ENVIRONMENTAL ASSESSMENT AND REVIEW FRAMEWORK (EARF) DOCUMENT ...........................................................................1-2 1.4 SCOPE OF SERVICES AND APPROACH TO CARRY OUT THE STUDY ..................1-2 1.4.1 Specific Tasks for the Study Team ....................................................................1-3 1.5 THE STUDY TEAM ......................................................................................................1-4 1.6 STRUCTURE OF THE REPORT ..................................................................................1-5 CHAPTER 2: POLICY, LEGAL AND ADMINISTRATIVE FRAMEWORK ...............................2-1 2.1 GENERAL ..............................................................................................................2-1 -

Population and Household Detail from Block to District Level

POPULATION AND HOUSEHOLD DETAIL FROM BLOCK TO DISTRICT LEVEL KHYBER PAKHTUNKHWA (KOHISTAN DISTRICT) ADMIN UNIT POPULATION NO OF HH KOHISTAN DISTRICT 784,711 101,921 DASSU SUB-DIVISION 222,282 28,880 DASSU TEHSIL 222,282 28880 BARIYAR U.C 36,744 5333 AKRO BAK 130 18 014050406 130 18 ASHOI BACK 1,860 253 014050101 588 85 014050102 598 84 014050103 674 84 ASLAN 512 82 014050905 512 82 ATHLOK 513 73 014050603 513 73 BAIK 138 19 014050805 138 19 BAJA 602 83 014050706 602 83 BANDLO BELA 1,609 222 014050207 582 83 014050208 587 79 014050209 440 60 BAR MUSLIM KOT 1,375 217 014050401 382 65 014050402 432 62 014050403 308 54 014050404 253 36 BARI YAR 1,681 288 014050201 745 132 014050202 466 71 014050203 470 85 BARKAR 138 18 014050801 138 18 BARKHAIL BAK 529 71 014050407 529 71 BASH 574 79 014050701 574 79 CHONDO 63 11 014050305 63 11 DAD 1,268 194 014050109 227 37 014050110 1,041 157 Page 1 of 84 POPULATION AND HOUSEHOLD DETAIL FROM BLOCK TO DISTRICT LEVEL KHYBER PAKHTUNKHWA (KOHISTAN DISTRICT) ADMIN UNIT POPULATION NO OF HH DADAIR SAIDAN 608 81 014050903 608 81 DADBOON 1,729 229 014050512 656 85 014050513 536 70 014050514 537 74 DAKI DO 1,044 163 014050204 536 74 014050205 508 89 DAR 601 74 014051002 601 74 DOKRO 674 125 014050507 466 77 014050508 208 48 DOOLI 609 83 014050904 609 83 GAIDER KEEHRO 395 56 014050901 395 56 JAKH 55 12 014050306 55 12 JARTOSER 1,560 242 014050501 504 76 014050502 453 82 014050503 603 84 JHAMRA 1,765 233 014050408 630 82 014050409 523 69 014050410 612 82 JOKE 584 79 014050705 584 79 JONO 290 48 014051003 290 48 KANDAIR -

32840 SSNP02.Pdf

SOCIOLINGUISTIC SURVEY OF NORTHERN PAKISTAN VOLUME 2 LANGUAGES OF NORTHERN AREAS Sociolinguistic Survey of Northern Pakistan Volume 1 Languages of Kohistan Volume 2 Languages of Northern Areas Volume 3 Hindko and Gujari Volume 4 Pashto, Waneci, Ormuri Volume 5 Languages of Chitral Series Editor Clare F. O’Leary, Ph.D. Sociolinguistic Survey of Northern Pakistan Volume 2 Languages of Northern Areas Peter C. Backstrom Carla F. Radloff National Institute of Summer Institute Pakistani Studies of Quaid-i-Azam University Linguistics Copyright © 1992 NIPS and SIL Published by National Institute of Pakistan Studies, Quaid-i-Azam University, Islamabad, Pakistan and Summer Institute of Linguistics, West Eurasia Office Horsleys Green, High Wycombe, BUCKS HP14 3XL United Kingdom First published 1992 Reprinted 2002 ISBN 969-8023-12-7 Price, this volume: Rs.300/- Price, 5-volume set: Rs.1500/- To obtain copies of these volumes within Pakistan, contact: National Institute of Pakistan Studies Quaid-i-Azam University, Islamabad, Pakistan Phone: 92-51-2230791 Fax: 92-51-2230960 To obtain copies of these volumes outside of Pakistan, contact: International Academic Bookstore 7500 West Camp Wisdom Road Dallas, TX 75236, USA Phone: 1-972-708-7404 Fax: 1-972-708-7433 Internet: http://www.sil.org Email: [email protected] REFORMATTING FOR REPRINT BY R. CANDLIN. CONTENTS Preface..................................................................................................ix Maps .....................................................................................................xi -

Dassu Chilas Swat Disputed Area Bala Kot Athmuqam Allai Palas

73°0’0"E 73°30’0"E 74°0’0"E Karang Gilgit Darel/Tangir Thuti Sazin Karin Goshali 35°30’0"N 35°30’0"N Baryar Parwa Swat Siglo Dassu Seo Bar Jalkot Chilas Goshali Koz Jalkot Dassu Chawa Dara Dubair Bala Kamila Kayal Sagayon Pattan Jijal CRS, Army Dubair Khas SPO Kunshair CRS Dubair Pain Patan SPO, Army SPO, Army Peach Bela Shalkan Abod Bar Paro Pir Kana Ronolia SPO, Army Haran SPO Shareed Sheryal CRS, SPO Khota Kot Kuz Paro Kuz Kalle Albat SPO, Army Bazar SPO Sherakot SPO, Army SPO SPO CRS, SPO, Army Kolai Bankhad SPO, Army 35°0’0"N Lilunai SPO Palas Mada Khail 35°0’0"N SPO, Army Bar Kana SPO, Army Batera Pain Alpuri CRS, BEST SPO, Army Shahpur Sakargarh CARE, SCF, Sungi SPO, Army Kaghan Alpuri Kuz Kana Batyal WVI Damorai SPO, Army SPO, CWS Jambera Pir Abad SCF, BEST Pashto Kel SPO, Army PPAF, SCF, BEST Bisham Bateela Dherai Allai ACTED, Sungi, CARE SPO, Army Bana Bala Kot Dandai SCF, CWS, Sungi, BEST Malik Khel Chakisar Army ACTED, PPAF, SCF, Sungi, CARE Biari Shardi SPO, Army Rashang IR Puran Batkul SPO, Army Chakisar PPAF, CARE, CRS, ACTED Musa Khail Guresinakka Paimal Sharif PPAF, SDC, Sungi, FRC Athmuqam Alouch Thakot Sungi, BEST Batamori Puran SPO, Army SPO, CWS, Sungi Bunerwal Devli Jaberr Dudhnial Batagram SDC, SPO, Sungi, BEST PPAF, CRS, KP, BEST Shamlai Kewal IR Batagram SFL,PPAF, ACTED, CWS, Sungi, ILAP Peshora Nilam SPO, Army Bassi Khel PPAF, SPO, Sungi IOM, SPO, CWS, Sungi, SCF AC, Army IR Martoong Rajdhari Mohandri Gijbori Ajmera SPO, Sungi, BEST PPAF, KP,MC, CRS, BEST, ILAP HFH, SDC, CWS, Sungi Behlool Khail SPO, Sungi, BEST