Australian Equity Microcap Insights

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

TPG Telecom Limited and Its Controlled Entities ABN 46 093 058 069

TPG Telecom Limited and its controlled entities ABN 46 093 058 069 Annual Report Year ended 31 July 2016 2 TPG Telecom Limited and its controlled entities Annual report For the year ended 31 July 2016 Contents Page Chairman’s letter 3 Directors’ report 5 Lead auditor’s independence declaration 34 Consolidated income statement 35 Consolidated statement of comprehensive income 36 Consolidated statement of financial position 37 Consolidated statement of changes in equity 38 Consolidated statement of cash flows 39 Notes to the consolidated financial statements 40 Directors’ declaration 91 Independent auditor’s report 92 ASX additional information 94 3 TPG Telecom Limited and its controlled entities Chairman’s letter For the year ended 31 July 2016 Dear Shareholders On behalf of the Board of Directors, I am pleased to present to you the TPG Telecom Limited Annual Report for the financial year ended 31 July 2016 (“FY16”). Financial Performance FY16 was another successful year for the Group. Continued organic growth and the integration of iiNet into the business have resulted in further increases in revenue, profits and dividends for shareholders. FY16 represents the eighth consecutive year that this has been the case. A detailed review of the Group’s operating and financial performance for the year is provided in the Operating and Financial Review section of the Directors’ Report starting on page 7 of this Annual Report, and set out below are some of the key financial highlights and earnings attributable to shareholders from the year. FY16 FY15 Movement Revenue ($m) 2,387.8 1,270.6 +88% EBITDA ($m) 849.4 484.5 +75% NPAT ($m) 379.6 224.1 +69% EPS (cents/share) 45.3 28.2 +61% Dividends (cents/share) 14.5 11.5 +26% iiNet Acquisition At the beginning of FY16 we completed the acquisition of iiNet and consequently there has been significant focus during the year on integrating the businesses to improve the efficiency of the combined organisation. -

Approved Securities List

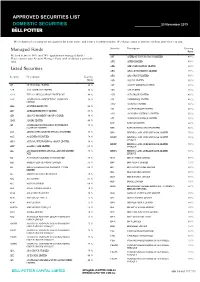

APPROVED SECURITIES LIST DOMESTIC SECURITIES 23 November 2019 The inclusion of a security on our approval list is not advice and is not a recommendation. We change ratios at any time without prior notice to you. Security Description Gearing Managed Funds Ratio We lend between 50% and 70% against most managed funds. APT AFTERPAY TOUCH GROUP LIMITED 40 % Please contact your Account Manager if you wish to discuss a particular fund. APX APPEN LIMITED 40 % Listed Securities ARB ARB CORPORATION LIMITED. 60 % ARG ARGO INVESTMENTS LIMITED 75 % Security Description Gearing ARQ ARQ GROUP LIMITED 50 % Ratio ASB AUSTAL LIMITED 50 % 3PL 3P LEARNING LIMITED.. 40 % AST AUSNET SERVICES LIMITED 65 % A2B A2B AUSTRALIA LIMITED 50 % ASX ASX LIMITED 70 % A2M THE A2 MILK COMPANY LIMITED NZ 40 % AUB AUB GROUP LIMITED 40 % AAC AUSTRALIAN AGRICULTURAL COMPANY 50 % AVJ AVJENNINGS LIMITED 40 % LIMITED. AWC ALUMINA LIMITED 70 % ABA AUSWIDE BANK LTD 40 % AX1 ACCENT GROUP LIMITED 50 % ABC ADELAIDE BRIGHTON LIMITED 65 % AYS AMAYSIM AUSTRALIA LIMITED 50 % ABP ABACUS PROPERTY GROUP STAPLED 50 % AZJ AURIZON HOLDINGS LIMITED 70 % ADH ADAIRS LIMITED 40 % BAP BAPCOR LIMITED 60 % AFI AUSTRALIAN FOUNDATION INVESTMENT 75 % COMPANY LIMITED BBN BABY BUNTING GROUP LIMITED 50 % AGI AINSWORTH GAME TECHNOLOGY LIMITED 55 % BEN BENDIGO AND ADELAIDE BANK LIMITED 70 % AGL AGL ENERGY LIMITED. 70 % BENPE BENDIGO AND ADELAIDE BANK LIMITED 70 % LPYR6UT AHG AUTOMOTIVE HOLDINGS GROUP LIMITED. 50 % BENPF BENDIGO AND ADELAIDE BANK LIMITED 70 % AHY ASALEO CARE LIMITED 65 % LPYR6UT AIA AUCKLAND INTERNATIONAL AIRPORT LIMITED 70 % BENPG BENDIGO AND ADELAIDE BANK LIMITED 70 % NZX LPYR3UT ALF AUSTRALIAN LEADERS FUND LIMITED 50 % BGA BEGA CHEESE LIMITED 60 % ALG ARDENT LEISURE GROUP LIMITED 55 % BHP BHP GROUP LIMITED 75 % ALI ARGO GLOBAL LISTED INFRASTRUCTURE 60 % BIN BINGO INDUSTRIES LIMITED 50 % LIMITED BKL BLACKMORES LIMITED 60 % ALL ARISTOCRAT LEISURE LIMITED 70 % BKW BRICKWORKS LIMITED 60 % ALQ ALS LIMITED 65 % BLD BORAL LIMITED. -

Quarterly Investment Update Antares High Growth Shares Fund – June 2021

Quarterly Investment Update Antares High Growth Shares Fund – June 2021 For adviser use only Highlights for the quarter Performance: The Fund returned 9.6% (net of fees) for the June quarter, outperforming its benchmark by 1.3%. Contributors to performance: Positive contributors – Aristocrat Leisure, Telix Pharmaceuticals, Megaport, Boral, Woodside (not owned); Negative contributors – Incitec Pivot, Qantas, ANZ, Resmed (not owned) and Altium (not owned). Stock activity: Buys/additions – Ansell, Downer and TPG Telecom ; Sells/reductions – BlueScope Steel, Boral, Endeavour Group and Worley Fund snapshot Inception date 7 December 1999 Benchmark S&P/ASX 200 Total Return Index To outperform the benchmark (after fees) over rolling Investment objective 5-year periods Investment returns as at 30 June 20211 Period 3 months 1 year 3 years pa 5 years pa 10 years pa Since inception pa Net return2 % 9.6 39.9 9.2 12.6 10.0 11.0 Gross return3 % 9.9 41.9 10.5 13.9 11.2 12.5 Benchmark return % 8.3 27.8 9.6 11.2 9.3 8.5 Net excess return % 1.3 12.1 -0.4 1.4 0.7 2.5 Gross excess return % 1.6 14.1 0.9 2.7 1.9 4.0 1 Past performance is not a reliable indicator of future performance. Returns are not guaranteed and actual returns may vary from any target returns described in this document. 2 Investment returns are based on exit prices, and are net of management fees and assume reinvestment of all distributions. Contributors to performance Pleasingly the Fund enjoyed another strong quarter, returning 9.6% (net of fees) vs the benchmark return of 8.3%. -

Bringing the Future Faster

6mm hinge Bringing the future faster. Annual Report 2019 WorldReginfo - 7329578e-d26a-4187-bd38-e4ce747199c1 Bringing the future faster Spark New Zealand Annual Report 2019 Bringing the future faster Contents Build customer intimacy We need to understand BRINGING THE FUTURE FASTER and anticipate the needs of New Zealanders, and Spark performance snapshot 4 technology enables us Chair and CEO review 6 to apply these insights Our purpose and strategy 10 to every interaction, Our performance 12 helping us serve our Our customers 14 customers better. Our products and technology 18 Read more pages 7 and 14. Our people 20 Our environmental impact 22 Our community involvement 24 Our Board 26 Our Leadership Squad 30 Our governance and risk management 32 Our suppliers 33 Leadership and Board remuneration 34 FINANCIAL STATEMENTS Financial statements 38 Notes to the financial statements 44 Independent auditor’s report 90 OTHER INFORMATION Corporate governance disclosures 95 Managing risk framework roles and 106 responsibilities Materiality assessment 107 Stakeholder engagement 108 Global Reporting Initiative (GRI) content 109 index Glossary 112 Contact details 113 This report is dated 21 August 2019 and is signed on behalf of the Board of Spark New Zealand Limited by Justine Smyth, Chair and Charles Sitch, Chair, Audit and Risk Management Committee. Justine Smyth Key Dates Annual Meeting 7 November 2019 Chair FY20 half-year results announcement 19 February 2020 FY20 year-end results announcement 26 August 2020 Charles Sitch Chair Audit and Risk Management Committee WorldReginfo - 7329578e-d26a-4187-bd38-e4ce747199c1 Create New Zealand’s premier sports streaming business Spark Sport is revolutionising how New Zealanders watch their favourite sports events. -

Ci Australian Equities Fund

CI AUSTRALIAN EQUITIES FUND QUARTERLY COMMENTARY REPORT Cooper Investors Pty Limited AFS Licence Number 221794 ABN 26 100 409 890 For current performance information please refer to the Monthly Performance Report. JUNE 2021 “Wise men speak because they have something to say: fools because they have to say something.” Plato “Faced with the choice between changing one’s mind and proving that there is no need to do so, almost everyone gets busy on the proof.” John Kenneth Galbraith **PORTFOLIO #BENCHMARK VALUE ADDED ROLLING 3 MONTH 9.13% 8.29% 0.84% ROLLING 1 YEAR 28.02% 27.80% 0.22% ROLLING 3 YEAR 10.82% 9.58% 1.24% ROLLING 5 YEAR 11.76% 11.16% 0.60% ROLLING 7 YEAR 11.32% 8.79% 2.53% ROLLING 10 YEAR 12.59% 9.26% 3.33% SINCE INCEPTION* 12.55% 8.98% 3.57% SINCE INCEPTION^ 844.84% 411.66% 433.18% *Annualised ^Cumulative (4 July 2002) **Before fees and expenses #S&P ASX 200 Accumulation Index Past performance is not necessarily a reliable indicator of future performance CI Australian Equities Fund - Gross of Fees $1,000 Invested Since Inception $9,800 $8,800 $7,800 $6,800 $5,800 $4,800 $3,800 $2,800 $1,800 $800 CI Australian Equities Fund S&P ASX 200 Accumulation Index Source: NAB Asset Servicing 1 CI AUSTRALIAN EQUITIES FUND QUARTERLY COMMENTARY REPORT Cooper Investors Pty Limited AFS Licence Number 221794 ABN 26 100 409 890 For current performance information please refer to the Monthly Performance Report. JUNE 2021 CI Australian Equities vs ASX200 (since inception to 30-Jun 2021) 16% CI Australian Equities 12% S&P 500 ASX 200 Acc. -

1. Shareholdings in Public and Private Companies (Including Holding

Form A 3 March 2020 Surname: Mclachlan Other names: Andrew State/Territory: SA Date: 3/03/2020 1. Shareholdings in public and private companies (including holding companies) indicating the name of the company or companies (Note: It is NOT necessary to declare the size or value of the shareholding) Name of company – (including holding and subsidiary companies if applicable) OATMILL HOLDINGS PTY LTD AUSTOFIX GROUP LTD VITRO SOFTWARE HOLDINGS (Designated Activity Company) ALUMINA LIMITED ANTIPODES GLOBAL INVESTMENT COMPANY LTD ANZ BANKING GROUP LIMITED AP EAGERS LIMITED ARISTOCRAT LEISURE LIMITED BHP GROUP LIMITED BORAL LIMITED CLEANAWAY WASTE MANAGEMENT LTD COMMONWEALTH BANK OF AUSTRALIA CORPORATE TRAVEL MANAGEMENT LIMITED COSTA GROUP HOLDINGS LIMITED GRAINCORP LIMITED ILUKA RESOURCES LIMITED LI LONG SHORT FUND LIMITED MACQUARIE GROUP LIMITED MINERAL RESOURCES LIMITED Form A NAOS EMERG OPP CO LTD NINE ENTERTAINMENT co HLDGS LTD OOH!MEDIA LIMITED ORIGIN ENERGY LIMITED ORORA LIMITED QBE INSURANCE GROUP LIMITED QUBE HOLDINGS LIMITED RELIANCE WORLDWIDE CORPORATION LIMITED SIMS LIMITED SONIC HEALTHCARE LIMITED SOUTH32 LIMITED S32 THE STAR ENTERTAINMENT GROUP LTD TPG TELECOM LIMITED TPM WAM LEADERS LIMITED WAM MICROCAP LIMITED WESFARMERS LIMITED WESTPAC BANKING CORPORATION WOODSIDE PETROLEUM LIMITED WORLEY LIMITED NATIONAL STORAGE REIT STPLD SEC AMCOR PLC JANUS HENDERSON GROUP PLC SPARK NEW ZEALAND LIMITED VIRGIN MONEY UK PLC ANZ BANK UNSEC NON-CUM PARADICE GLOBAL SMALL CAP FUND PLATINUM EUROPEAN FUND WESTPAC CAPITAL NOTES 2. Family and business -

Ausbil Australian Emerging Leaders Fund (ARSN 089 995 442) (Fund)

Contactus@ ausbil.com.au Ausbil Investment Ausbil Australian Emerging Management Limited ABN 26 076 316 473 AFSL 229722 Leaders Fund Level 27 225 George Street Sydney NSW 2000 Monthly performance update GPO Box 2525 Sydney NSW 2001 July 2020 Phone 61 2 9259 0200 Fax 61 2 9259 0222 ‘We have now entered the FY 2020 reporting Fund Characteristics season in which companies will reveal the full Returns1 as at 31 July 2020 impact, so far, of Covid-19 on this year’s financial Period Fund Bench- Out/Under Return1 mark2 performance performance and balance sheets’ % % % 1 month 3.44 1.85 1.59 Performance Review 3 months 13.77 13.14 0.64 Fund performance for July 2020 was +3.44% (net of fees), versus the 6 months -9.97 -8.32 -1.65 benchmark return of +1.85%. The benchmark is represented by a FYTD 3.44 1.85 1.59 composite, 70% of the S&P/ASX MidCap 50 Accumulation Index, and CYTD -6.89 -4.39 -2.49 30% of the S&P/ASX Small Ordinaries Accumulation Index. 1 year -8.26 -4.05 -4.21 At a sector level, the overweight positions in the Materials, Financials 3 years pa 3.96 7.14 -3.18 and Information Technology sectors added to relative performance. The underweight positions in Industrials, Health Care and Real Estate also 5 years pa 6.03 9.36 -3.32 added to relative performance. Conversely, the overweight positions in 7 years pa 8.14 10.26 -2.13 the Consumer Staples and Communication Services sectors detracted 10 years pa 7.44 7.94 -0.51 from relative performance. -

Study of Mobile Telecommunications Markets in NZ Submission

Study of mobile telecommunications markets in NZ Submission | Commerce Commission 26 October 2018 Public Version Contents Executive Summary .............................................................................................................. 1 Introduction ........................................................................................................................... 4 1. Current market outcomes .................................................................................................. 5 Assessing competition and market outcomes .................................................................... 5 Price, quality and innovation .............................................................................................. 6 Data the paper seeks further information on ...................................................................... 7 2. Looking forward .............................................................................................................. 13 5G network deployment ................................................................................................... 15 Emerging trends .............................................................................................................. 17 Promoting 5G deployment ............................................................................................... 23 3. Industry structure ............................................................................................................ 24 MVNOs ........................................................................................................................... -

VOC.AX: Vocus/M2 Completes Fixed Telco 'Big Four'

8 April 2016 Asia Pacific/Australia Equity Research Alternative Carriers Vocus Communications (VOC.AX / VOC AU) Rating OUTPERFORM Price (08-Apr,A$) 8.58 INCREASE TARGET PRICE Target Price (A$) (from 8.0) 9.2 Target price ESG risk (%) 0.0 Market cap (A$mn) 4,565.9 Vocus/M2 completes fixed telco 'big four' Yr avg. mthly trading (A$mn) 204.8 Projected return: ■ Enlarged Vocus can become a major telco: Vocus has been transformed Capital gain (%) 7.2 following the recent mergers with Amcom and M2. The enlarged Vocus now Dividend yield (net %) 2.4 has national network capability, a strong data/internet product set, scale Total return (%) 9.6 presence in all key customer segments (medium/large corporate, wholesale, *Stock ratings are relative to the relevant country benchmark. ¹Target price is for 12 months. SME and consumer), and an enhanced national sales and dealer network to Research Analysts sell its products. The merged group has the footprint and capabilities that it Fraser McLeish needs to win share in all its key markets and to grow into a major telco over 61 2 8205 4069 [email protected] time. Execution will now be the main factor determining success. In this Lucas Goode report we undertake a detailed review of Vocus' operations and key drivers. 61 2 8205 4431 [email protected] ■ Market share gains to accelerate: The enlarged Vocus is expanding its sales force and investing in marketing, which we expect to drive continued growth in market share as corporate/business customers re-assess their telcom requirements as they transition to an IP/cloud environment. -

Small Talk Better, Cheaper, Faster… by Marcus Burns, Senior Portfolio Manager, Australian Smaller Companies

June 2013 For professional investors only Small Talk Better, cheaper, faster… by Marcus Burns, Senior Portfolio Manager, Australian Smaller Companies To a man with a hammer everything looks like a nail. Australia is a country blessed with a great climate, loads of natural resources, an abundance of land and the English legal System with the rule of law. You could stop there and logic alone would dictate these are conditions precedent for fostering a successful country. With these natural and cultural blessings in tow it would be unforgiveable, however, for us to become complacent. As the resources boom draws to an end and with it the vast investment in resources infrastructure, how well our country does will depend on our adaptability to new economic conditions. Conditions that will more likely favour companies whose managers are “fortunate because they are able” rather than those who are “fortunate and able”. By this I am referring to management teams whose capability to grow sales and profits faster than their industry average will likely become even more important as our economy subdues. Managers, in our opinion, likely to achieve this are those who can and have focused on innovation and who operate with lean and flexible work forces. Innovation can take many forms. It can involve making something better, faster, cheaper, more convenient. It can involve making something new – I didn’t know I needed an iPad until Steve Jobs and Apple invented one. Ditto the iPhone. Someone invented ABS brakes, LED lighting and solar power. Many of the longest lasting and better companies to work for are the most innovative. -

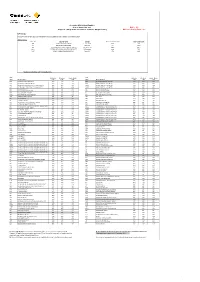

Commsec Margin Lending Approved Securities List

Accepted ASX Listed Equities as at 21 September 2021 Buffer - 5% Subject to change at the discretion of CommSec Margin Lending Maximum Gearing Ratio - 90% LVR Changes Changes since the last Approved Securities List was published are outlined in the below table: ASX Securities ASX Code Security Name Change Previous Portfolio LVR New Portfolio LVR AST AUSNET SERVICES LIMITED Capped LVR 75% 75% BGL BELLEVUE GOLD LIMITED New LVR 0% 40%* SXL SOUTHERN CROSS MEDIA GROUP LIMITED Uncapped LVR 40%* 40%* QLTY BETASHARES GLOBAL QUALITY LEADERS ETF LVR Increase 65% 70% CLNE VANECK GLOBAL CLEAN ENERGY ETF New LVR 0% 65% *Available via facilities with PLVR enabled only ASX Portfolio Standard Single Stock ASX Portfolio Standard Single Stock Code Security Name LVR LVR LVR Code Security Name LVR LVR LVR A200 BETASHARES AUSTRALIA 200 ETF 80% 75% 70% BNKS BETASHARES GLOBAL BANKS ETF 70% 65% 60% A2M THE A2 MILK COMPANY LIMITED 55% 50% 45% BOQ BANK OF QUEENSLAND LIMITED 70% 65% 60% AAA BETASHARES AUSTRALIAN HIGH INTEREST CASH ETF 90% 85% 80% BOQPE BANK OF QUEENSLAND LIMITED 70% 65% 60% AAC AUSTRALIAN AGRICULTURAL COMPANY LIMITED 50% 45% 40% BOQPF BANK OF QUEENSLAND LIMITED 70% 65% 60% ABA AUSWIDE BANK LTD 50% 45% 40% BPT BEACH ENERGY LIMITED 50% 45% 40% ABC ADELAIDE BRIGHTON LIMITED 60% 55% 50% BRG BREVILLE GROUP LIMITED 65% 60% 55% ABP ABACUS PROPERTY GROUP 65% 60% 55% BSL BLUESCOPE STEEL LIMITED 70% 65% 60% ACDC ETFS BATTERY TECH & LITHIUM ETF 60% 55% 50% BVS BRAVURA SOLUTIONS LIMITED 45% 40% 35% AD8 AUDINATE GROUP LIMITED 40% 0% 0% BWP BWP TRUST 70% 65% 60% ADH ADAIRS LIMITED 45% 40% 35% BWX BWX LIMITED 45% 40% 35% ADI APN INDUSTRIA REIT 60% 55% 50% BXB BRAMBLES LIMITED 80% 75% 70% AEF AUSTRALIAN ETHICAL INVESTMENT LIMITED 40% 35% 30% CAJ CAPITOL HEALTH LIMITED 40% 0% 0% AFG AUSTRALIAN FINANCE GROUP LTD 40% 35% 30% CAR CARSALES.COM LIMITED. -

TPG Telecom Limited (Formerly the Details of Our 2020 Achievements Across Our Family of Brands, We Named VHA) and a Contribution of and Our 2021 Priorities

Annual Report 2020 Contents Chairman and CEO’s letter 2 Strategy and Performance 6 Key Risks 12 Operating and Financial Review 15 Directors’ Report 23 Remuneration Report 30 Auditor’s Independence Declaration 60 Financial Report 61 Consolidated Income Statement 62 Consolidated Statement of Comprehensive Income 63 Consolidated Statement of Financial Position 64 Consolidated Statement of Changes in Equity 65 Consolidated Statement of Cash Flows 66 Notes to the Consolidated Financial Statements 67 Directors’ Declaration 122 Independent Auditor’s Report 123 ASX Additional Information 132 Annual Report 2020 1 Highlights REVENUE EBITDA $4.35b $1.39b 24 per cent from 2019 18 per cent from 2019 NPAT NET CASH FLOW $734m $342m First six months post-merger 2 Chairman and CEO’s letter Dear Shareholders, 2020 highlights will begin offering 5G fixed wireless services to customers. 2020 was a year in which Australian Following the implementation of society and the economy was the merger between the companies We are pleased with the progress subjected to significant unexpected formerly named Vodafone we have made, and we thank our shocks but also showed remarkable Hutchison Australia (‘VHA’) and employees for their hard work to resilience. TPG Telecom on 13 July 2020, we deliver more every day for our set upon the important work of customers. Telecommunications services played delivering the benefits to customers an essential part in the everyday lives and shareholders. Financial performance of Australians, with the COVID-19 pandemic and the bushfire crisis Customers began benefiting from the Our results demonstrate that highlighting the critical role that integration of our complementary despite the impact of COVID, the sector plays in our society.