Rudi's View: Technologyone, CSL, Banks

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

2013 Annual Report

Transforming business, making life simple Technology One Limited Technology 2013 Annual Report Technology One Limited 2013 Annual Report cus & Fo t Po et men we rk it r a m of M m O o n C e n o i s i V e s i One One One r p r e t vision. vendor. experience. n E n n S io o i t t m lu C pl o o ici Ev m ty, of ple er xity Pow y t P i o x w e e l r p o , y f t m i E c o i v l C o p t l u m i o t S n i o n TechnologyOne is a leading supplier of powerful, integrated enterprise software solutions. We are also Australia’s largest publicly listed software company. Market focus Our core An enterprise vision and commitment Transforming business, beliefs The power of a single, Preconfi gured enterprise making life simple integrated enterprise solution software solutions reduce time, cost and risk Experience the power of a single, A deep understanding and integrated enterprise solution engagement with our seven key built on a single modern markets means we can deliver platform with a consistent to our customers integrated, look and feel. preconfi gured solutions that provide proven practice, streamline implementations and reduce time, cost and risk. 1 Technology One Limited 2013 Annual Report 2013 full year highlights $m Compound Growth 13% $m Compound Growth 20% 40 80 35 70 30 60 25 50 20 40 15 30 10 20 5 10 0 FY FY 0 04 05 06 07 08 09 10 11 12 13 04 05 06 07 08 09 10 11 12 13 0 FY 04 05 06 07 08 09 10 11 12 13 0 FY 04 05 06 07 08 09 10 11 12 13 5 Net Profi t Before Tax 10 Annual Licence Fees 10 up 16%, $35.1m 20 up 14%, $9.1m 15 30 Every day, more than 1,000 leading corporations, government departments and statutory authorities in Australia, New Zealand, Asia, the South Pacifi c and United Kingdom use our world class enterprise software solutions, which we develop, market, sell, implement, support and run. -

Australian Investment Strategy

2 November 2016 Asia Pacific/Australia Equity Research Investment Strategy Australian Investment Strategy Research Analysts STRATEGY Hasan Tevfik ,CFA 61 2 8205 4284 [email protected] Aussie darlings Peter Liu 61 2 8205 4071 ■ Aussies love their darlings: Australia currently has the most expensive [email protected] equity market "Darlings" in the world. Our darlings trade on a forward P/E Damien Boey of 38x. The other commodity-focused market, Canada, has the second 61 2 8205 4615 [email protected] most expensive darlings. Darlings in Australia have been more expensive only during the Nasdaq bubble when they touched 45x. ■ Darling derating: Buying Australian darlings at these valuations has been a poor strategy in the past. Also, the current high valuation for Australia's darlings suggest they are especially vulnerable to rising bond yields and the coming end of the Australian profits recession. A rising discount rate and a lower premium for growth suggest investors should focus on stocks that could be future darlings. ■ Hello Daaarling: Future market darlings have shared many similar characteristics over the last 20 years. They are generally well managed, have strong balance sheets and operate on high margins. Our "Hello Daaarling" strategy highlights potential future darlings and they currently trade on just 17x P/E and include Caltex, Eclipx, Mayne Pharma, Nufarm, Star Entertainment and South 32. We add Eclipx to our long Portfolio. Figure 1: Australia has the most expensive darlings in the world Median 12-month forward P/E of "market darlings" around the world* 40 35 30 25 20 15 10 Australia Canada Cont. -

TPG Telecom Limited and Its Controlled Entities ABN 46 093 058 069

TPG Telecom Limited and its controlled entities ABN 46 093 058 069 Annual Report Year ended 31 July 2016 2 TPG Telecom Limited and its controlled entities Annual report For the year ended 31 July 2016 Contents Page Chairman’s letter 3 Directors’ report 5 Lead auditor’s independence declaration 34 Consolidated income statement 35 Consolidated statement of comprehensive income 36 Consolidated statement of financial position 37 Consolidated statement of changes in equity 38 Consolidated statement of cash flows 39 Notes to the consolidated financial statements 40 Directors’ declaration 91 Independent auditor’s report 92 ASX additional information 94 3 TPG Telecom Limited and its controlled entities Chairman’s letter For the year ended 31 July 2016 Dear Shareholders On behalf of the Board of Directors, I am pleased to present to you the TPG Telecom Limited Annual Report for the financial year ended 31 July 2016 (“FY16”). Financial Performance FY16 was another successful year for the Group. Continued organic growth and the integration of iiNet into the business have resulted in further increases in revenue, profits and dividends for shareholders. FY16 represents the eighth consecutive year that this has been the case. A detailed review of the Group’s operating and financial performance for the year is provided in the Operating and Financial Review section of the Directors’ Report starting on page 7 of this Annual Report, and set out below are some of the key financial highlights and earnings attributable to shareholders from the year. FY16 FY15 Movement Revenue ($m) 2,387.8 1,270.6 +88% EBITDA ($m) 849.4 484.5 +75% NPAT ($m) 379.6 224.1 +69% EPS (cents/share) 45.3 28.2 +61% Dividends (cents/share) 14.5 11.5 +26% iiNet Acquisition At the beginning of FY16 we completed the acquisition of iiNet and consequently there has been significant focus during the year on integrating the businesses to improve the efficiency of the combined organisation. -

Approved Securities List

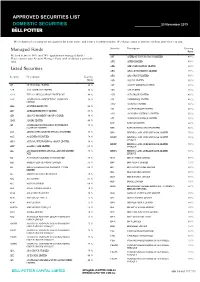

APPROVED SECURITIES LIST DOMESTIC SECURITIES 23 November 2019 The inclusion of a security on our approval list is not advice and is not a recommendation. We change ratios at any time without prior notice to you. Security Description Gearing Managed Funds Ratio We lend between 50% and 70% against most managed funds. APT AFTERPAY TOUCH GROUP LIMITED 40 % Please contact your Account Manager if you wish to discuss a particular fund. APX APPEN LIMITED 40 % Listed Securities ARB ARB CORPORATION LIMITED. 60 % ARG ARGO INVESTMENTS LIMITED 75 % Security Description Gearing ARQ ARQ GROUP LIMITED 50 % Ratio ASB AUSTAL LIMITED 50 % 3PL 3P LEARNING LIMITED.. 40 % AST AUSNET SERVICES LIMITED 65 % A2B A2B AUSTRALIA LIMITED 50 % ASX ASX LIMITED 70 % A2M THE A2 MILK COMPANY LIMITED NZ 40 % AUB AUB GROUP LIMITED 40 % AAC AUSTRALIAN AGRICULTURAL COMPANY 50 % AVJ AVJENNINGS LIMITED 40 % LIMITED. AWC ALUMINA LIMITED 70 % ABA AUSWIDE BANK LTD 40 % AX1 ACCENT GROUP LIMITED 50 % ABC ADELAIDE BRIGHTON LIMITED 65 % AYS AMAYSIM AUSTRALIA LIMITED 50 % ABP ABACUS PROPERTY GROUP STAPLED 50 % AZJ AURIZON HOLDINGS LIMITED 70 % ADH ADAIRS LIMITED 40 % BAP BAPCOR LIMITED 60 % AFI AUSTRALIAN FOUNDATION INVESTMENT 75 % COMPANY LIMITED BBN BABY BUNTING GROUP LIMITED 50 % AGI AINSWORTH GAME TECHNOLOGY LIMITED 55 % BEN BENDIGO AND ADELAIDE BANK LIMITED 70 % AGL AGL ENERGY LIMITED. 70 % BENPE BENDIGO AND ADELAIDE BANK LIMITED 70 % LPYR6UT AHG AUTOMOTIVE HOLDINGS GROUP LIMITED. 50 % BENPF BENDIGO AND ADELAIDE BANK LIMITED 70 % AHY ASALEO CARE LIMITED 65 % LPYR6UT AIA AUCKLAND INTERNATIONAL AIRPORT LIMITED 70 % BENPG BENDIGO AND ADELAIDE BANK LIMITED 70 % NZX LPYR3UT ALF AUSTRALIAN LEADERS FUND LIMITED 50 % BGA BEGA CHEESE LIMITED 60 % ALG ARDENT LEISURE GROUP LIMITED 55 % BHP BHP GROUP LIMITED 75 % ALI ARGO GLOBAL LISTED INFRASTRUCTURE 60 % BIN BINGO INDUSTRIES LIMITED 50 % LIMITED BKL BLACKMORES LIMITED 60 % ALL ARISTOCRAT LEISURE LIMITED 70 % BKW BRICKWORKS LIMITED 60 % ALQ ALS LIMITED 65 % BLD BORAL LIMITED. -

Quarterly Investment Update Antares High Growth Shares Fund – June 2021

Quarterly Investment Update Antares High Growth Shares Fund – June 2021 For adviser use only Highlights for the quarter Performance: The Fund returned 9.6% (net of fees) for the June quarter, outperforming its benchmark by 1.3%. Contributors to performance: Positive contributors – Aristocrat Leisure, Telix Pharmaceuticals, Megaport, Boral, Woodside (not owned); Negative contributors – Incitec Pivot, Qantas, ANZ, Resmed (not owned) and Altium (not owned). Stock activity: Buys/additions – Ansell, Downer and TPG Telecom ; Sells/reductions – BlueScope Steel, Boral, Endeavour Group and Worley Fund snapshot Inception date 7 December 1999 Benchmark S&P/ASX 200 Total Return Index To outperform the benchmark (after fees) over rolling Investment objective 5-year periods Investment returns as at 30 June 20211 Period 3 months 1 year 3 years pa 5 years pa 10 years pa Since inception pa Net return2 % 9.6 39.9 9.2 12.6 10.0 11.0 Gross return3 % 9.9 41.9 10.5 13.9 11.2 12.5 Benchmark return % 8.3 27.8 9.6 11.2 9.3 8.5 Net excess return % 1.3 12.1 -0.4 1.4 0.7 2.5 Gross excess return % 1.6 14.1 0.9 2.7 1.9 4.0 1 Past performance is not a reliable indicator of future performance. Returns are not guaranteed and actual returns may vary from any target returns described in this document. 2 Investment returns are based on exit prices, and are net of management fees and assume reinvestment of all distributions. Contributors to performance Pleasingly the Fund enjoyed another strong quarter, returning 9.6% (net of fees) vs the benchmark return of 8.3%. -

Bringing the Future Faster

6mm hinge Bringing the future faster. Annual Report 2019 WorldReginfo - 7329578e-d26a-4187-bd38-e4ce747199c1 Bringing the future faster Spark New Zealand Annual Report 2019 Bringing the future faster Contents Build customer intimacy We need to understand BRINGING THE FUTURE FASTER and anticipate the needs of New Zealanders, and Spark performance snapshot 4 technology enables us Chair and CEO review 6 to apply these insights Our purpose and strategy 10 to every interaction, Our performance 12 helping us serve our Our customers 14 customers better. Our products and technology 18 Read more pages 7 and 14. Our people 20 Our environmental impact 22 Our community involvement 24 Our Board 26 Our Leadership Squad 30 Our governance and risk management 32 Our suppliers 33 Leadership and Board remuneration 34 FINANCIAL STATEMENTS Financial statements 38 Notes to the financial statements 44 Independent auditor’s report 90 OTHER INFORMATION Corporate governance disclosures 95 Managing risk framework roles and 106 responsibilities Materiality assessment 107 Stakeholder engagement 108 Global Reporting Initiative (GRI) content 109 index Glossary 112 Contact details 113 This report is dated 21 August 2019 and is signed on behalf of the Board of Spark New Zealand Limited by Justine Smyth, Chair and Charles Sitch, Chair, Audit and Risk Management Committee. Justine Smyth Key Dates Annual Meeting 7 November 2019 Chair FY20 half-year results announcement 19 February 2020 FY20 year-end results announcement 26 August 2020 Charles Sitch Chair Audit and Risk Management Committee WorldReginfo - 7329578e-d26a-4187-bd38-e4ce747199c1 Create New Zealand’s premier sports streaming business Spark Sport is revolutionising how New Zealanders watch their favourite sports events. -

Australian Equity Microcap Insights

UBS Asset Management For professional / qualified / institutional investors only. May 2020 Australian Equity Microcap Insights Opportunities abound in Microcap space As the economy moves into the post COVID-19 recovery phase, UBS Microcap Fund Portfolio Manager Joel Fleming expects microcap companies to be an important contributor to the recovery, Joel Fleming with many smaller firms driving high levels Portfolio Manager Yarra Capital Management of growth as they take advantage of the lasting changes caused by the pandemic. There are a large number of common misconceptions Microcap recap about the contribution made by Australia’s smaller firms to Microcaps offer the largest investable universe by number the domestic economy. Some of Joels’s favourites include: on the ASX. With no ETF or passive products, a more constrained liquidity profile compared to large caps, and a • “Micro companies are largely in retail and service vast investable universe, Microcap investing is all about sectors and employ relatively few people in active management. comparison to larger firms” The index represents opportunity, with many examples of • “Micro and small companies tend to not be profitable. companies that have delivered on an idea and transitioned Profits in Australia are driven by large firms in the into the sphere of Australia’s Top 100 listed companies. mining, banks, supermarket and health care sectors” Think Afterpay, A2 Milk, Domino’s Pizza or TPG Telecom. • “Micro companies pay small dividends and have low While much of the universe will deliver poor returns, operating margins. Investing in the space is all about despite the hype and promise, the success stories can capital growth” deliver many multiples of an initial investment. -

2020 Annual Report About Nearmap

2020 ANNUAL REPORT ABOUT NEARMAP Nearmap Ltd (ABN 37 083 702 907) and its subsidiaries (Nearmap or Company) is a leading provider of cloud-based geospatial information services and an innovative location intelligence company. Nearmap captures a rich data set of the real world, providing high value insights to a diverse range of more than 10,000 businesses and government organisations. Using its own patented camera systems and processing software, Nearmap conducts aerial surveys capturing wide-scale urban areas in Australia, New Zealand, the United States of America and Canada multiple times each year, making fresh content instantly available in the cloud via web app or API integration. Every day, Nearmap helps tens of thousands of users conduct virtual site visits for deep, data driven insights – enabling businesses and government organisations to make informed decisions, streamline operations and bolster bottom lines. Founded in Australia in 2007, Nearmap is one of the ten largest aerial survey companies in the world by annual data collection volume and is publicly listed on the Australian Securities Exchange (ASX). Nearmap employs nearly 300 people globally, held a total annual subscription portfolio of $106.4m as at 30 June 2020 and was named as one of Fast Company’s 10 Most Innovative Enterprise Companies in 2020. United States Canada Australia New Zealand 71% population 64% population 89% population 73% population coverage coverage coverage coverage CAPTURED: 15 SEPTEMBER 2019 GOLD COAST QLD AUSTRALIA 2 ABOUT NEARMAP ABOUT NEARMAP -

Participating Organisations | June 2021 Aon Rewards Solutions Proprietary and Confidential

Aon Rewards Solutions Proprietary and Confidential Participating organisations | June 2021 Aon Rewards Solutions Proprietary and Confidential Participating organisations 1. .au Domain Administration 44. Alexion Pharmaceuticals Limited Australasia Pty Ltd 2. [24]7.ai 45. Alfa Financial Software 3. 10X Genomics* Limited 4. 4 Pines Brewing Company 46. Alibaba Group Inc 5. 8X8 47. Alida* 6. A.F. Gason Pty Ltd* 48. Align Technology Inc. 7. A10 Networks 49. Alkane Resources Limited 8. Abacus DX 50. Allianz Australia Ltd 9. AbbVie Pty Ltd 51. Allscripts 10. Ability Options Ltd 52. Alteryx 11. Abiomed* 53. Altium Ltd 12. AC3 54. Amazon.com 55. AMEC Foster Wheeler 13. ACCELA* Australia Pty Ltd 14. Accenture Australia Ltd 56. Amgen Australia Pty Ltd 15. AccorHotels 57. AMP Services Limited 16. Acer Computer Australia Pty Ltd* 58. AMSC 17. Achieve Australia Limited* 59. Analog Devices 18. Achmea Australia 60. Anaplan 19. ACI Worldwide 61. Ancestry.com 62. Anglo American Metallurgical 20. Acquia Coal Pty Ltd 21. Actian Corporation 63. AngloGold Ashanti Australia 22. Activision Blizzard Limited* 23. Adaman Resources 64. ANZ Banking Group Ltd 24. Adcolony 65. Aon Corporation Australia 25. A-dec Australia 66. APA Group 26. ADG Engineers* 67. Apollo Endosurgery Inc. 27. Adherium Limited 68. APPEN LTD 28. Administrative Services 69. Appian* 29. Adobe Systems Inc 70. Apple and Pear Australia Ltd* 30. ADP 71. Apple Pty Ltd 31. Adtran 72. Apptio 32. Advanced Micro Devices 73. APRA AMCOS 33. Advanced Sterlization 74. Aptean Products* 75. Aptos* 34. AECOM* 76. Apttus 35. AEMO 77. Aquila Resources 36. Aeris Resources Limited 78. Arcadis 37. -

National Asset Management Strategy Update NAMS Council

NAMS Council National Asset Management Strategy Update May 2019 Several NAMS Council items were reported at the meeting held on the 3rd May 2019. Of interest to readers and members are: 1 Projects Report 1.1 The National AM Congress The National AM Congress took place in August 2018. It was attended by 100 delegates and included presentations by many eminent speakers addressing a range of asset management issues. Outcomes from the Congress has allowed the IPWEA Board to endorse a “Public Infrastructure Action Plan” with the following key headings: 1. Increase competency in strategic infrastructure planning 2. Maintain funding at adequate levels for local government to deliver sustainable asset management plans 3. Promote effective knowledge sharing 4. Embrace emerging digital technology 5. Drive organisational cultural improvement 6. Build right place, right time projects 7. Provide investment and planning certainty 8. Integrate and coordinate national infrastructure planning It is anticipated that the broader NAMS and advocacy initiatives should be consistent with the relevant elements of the Action Plan. 1.2 Asset Management Basics Asset Management Basics (AMB) – Applying Infrastructure Asset Management Principles has been completed and is now available in hard copy or as part of the new E-Library. AMB is designed as a companion document to the IIMM and has been written to assist people and organizations that are new to asset management and need a grasp of the basic requirements of asset management planning. It is designed to be a resource that can be used by a variety of staff and elected members starting the journey of understanding the requirements of base and core level asset management planning. -

Single Sector Funds Portfolio Holdings

! Mercer Funds Single Sector Funds Portfolio Holdings December 2020 welcome to brighter Mercer Australian Shares Fund Asset Name 4D MEDICAL LTD ECLIPX GROUP LIMITED OOH MEDIA LIMITED A2 MILK COMPANY ELDERS LTD OPTHEA LIMITED ABACUS PROPERTY GROUP ELECTRO OPTIC SYSTEMS HOLDINGS LTD ORICA LTD ACCENT GROUP LTD ELMO SOFTWARE LIMITED ORIGIN ENERGY LTD ADBRI LTD EMECO HOLDINGS LTD OROCOBRE LTD ADORE BEAUTY GROUP LTD EML PAYMENTS LTD ORORA LTD AFTERPAY LTD ESTIA HEALTH LIMITED OZ MINERALS LTD AGL ENERGY LTD EVENT HOSPITALITY AND ENTERTAINMENT PACT GROUP HOLDINGS LTD ALKANE RESOURCES LTD EVOLUTION MINING LTD PARADIGM BIOPHARMACEUTICALS LTD ALS LIMITED FISHER & PAYKEL HEALTHCARE CORP LTD PENDAL GROUP LTD ALTIUM LTD FLETCHER BUILDING LTD PERENTI GLOBAL LTD ALUMINA LTD FLIGHT CENTRE TRAVEL GROUP LTD PERPETUAL LTD AMA GROUP LTD FORTESCUE METALS GROUP LTD PERSEUS MINING LTD AMCOR PLC FREEDOM FOODS GROUP LIMITED PHOSLOCK ENVIRONMENTAL TECHNOLOGIES AMP LTD G8 EDUCATION LTD PILBARA MINERALS LTD AMPOL LTD GALAXY RESOURCES LTD PINNACLE INVESTMENT MANAGEMENT GRP LTD ANSELL LTD GDI PROPERTY GROUP PLATINUM INVESTMENT MANAGEMENT LTD APA GROUP GENWORTH MORTGAGE INSRNC AUSTRALIA LTD POINTSBET HOLDINGS LTD APPEN LIMITED GOLD ROAD RESOURCES LTD POLYNOVO LIMITED ARB CORPORATION GOODMAN GROUP PTY LTD PREMIER INVESTMENTS LTD ARDENT LEISURE GROUP GPT GROUP PRO MEDICUS LTD ARENA REIT GRAINCORP LTD QANTAS AIRWAYS LTD ARISTOCRAT LEISURE LTD GROWTHPOINT PROPERTIES AUSTRALIA LTD QBE INSURANCE GROUP LTD ASALEO CARE LIMITED GUD HOLDINGS LTD QUBE HOLDINGS LIMITED ASX LTD -

Ci Australian Equities Fund

CI AUSTRALIAN EQUITIES FUND QUARTERLY COMMENTARY REPORT Cooper Investors Pty Limited AFS Licence Number 221794 ABN 26 100 409 890 For current performance information please refer to the Monthly Performance Report. JUNE 2021 “Wise men speak because they have something to say: fools because they have to say something.” Plato “Faced with the choice between changing one’s mind and proving that there is no need to do so, almost everyone gets busy on the proof.” John Kenneth Galbraith **PORTFOLIO #BENCHMARK VALUE ADDED ROLLING 3 MONTH 9.13% 8.29% 0.84% ROLLING 1 YEAR 28.02% 27.80% 0.22% ROLLING 3 YEAR 10.82% 9.58% 1.24% ROLLING 5 YEAR 11.76% 11.16% 0.60% ROLLING 7 YEAR 11.32% 8.79% 2.53% ROLLING 10 YEAR 12.59% 9.26% 3.33% SINCE INCEPTION* 12.55% 8.98% 3.57% SINCE INCEPTION^ 844.84% 411.66% 433.18% *Annualised ^Cumulative (4 July 2002) **Before fees and expenses #S&P ASX 200 Accumulation Index Past performance is not necessarily a reliable indicator of future performance CI Australian Equities Fund - Gross of Fees $1,000 Invested Since Inception $9,800 $8,800 $7,800 $6,800 $5,800 $4,800 $3,800 $2,800 $1,800 $800 CI Australian Equities Fund S&P ASX 200 Accumulation Index Source: NAB Asset Servicing 1 CI AUSTRALIAN EQUITIES FUND QUARTERLY COMMENTARY REPORT Cooper Investors Pty Limited AFS Licence Number 221794 ABN 26 100 409 890 For current performance information please refer to the Monthly Performance Report. JUNE 2021 CI Australian Equities vs ASX200 (since inception to 30-Jun 2021) 16% CI Australian Equities 12% S&P 500 ASX 200 Acc.