Annual Report 2015

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Silks Bistro & Champagne Bar Menu

Silks Bistro & Champagne Bar Menu A selection of breads from the basket Appetizers- Tapas Hummus served with Warmed Pitta £3.50 (v) Marinated Olives £3.75 (v) Chorizo with Roasted Shallots in a Red Wine Reduction £3.95 Shellfish Bisque Espresso with Shellfish Foam £4.25 Tempura of Seafood with Lemon & Sweet Chilli £6.50 3 Oysters Served on Crushed Ice & Red Wine Vinaigrette £8.50* Moules Mariniere Local Mussels cooked in Onions, Garlic & Lemon with a Splash of White Wine, Cream & Parsley (Moules available as Starter or Main Course) Starter: £7.95* Main: £14.50 Starters Homemade Soup of the Day £5.50 Goats Cheese Mousse with Pickled Blackberries and Brown Bread Crisps £5.95 Cayenne Floured Squid with Saffron Aioli & Fine Leaf £6.25 Ham Hock Terrine with Crispy Poached Egg, Straw Fries, Balsamic Reduction & Rocket £6.25 Newlyn Crab Cakes, Lemon & Sweet Chilli Mayonnaise £7.50 Seared Scallops with Pork Rillettes & a Smoked Carrot and Coral Puree £7.95* Silk’s Chicken Caesar Salad with Parmesan, Anchovy, Home Baked Croutons & Crispy Pancetta (Caesar Salads available as Starter or Main Course) Starter £7.50 Main £10.50 Vegetarian £6.50 Mains Roasted Vegetable, Tomato & Goat’s Cheese Linguini (v) £10.50 (Please ask us for other vegetarian or vegan options of the day) Chicken Supreme stuffed with Sage Mousse and wrapped in Serrano Ham, Fondant Potato & Buttered Chard £11.95 Battered Cod with Hand Cut Chips, Garden peas & Homemade Tartare Sauce £12.50 Trio of Pork Loin; Mushroom Rolled Pork Fillet, Braised Pork Daube & Crackling with Butternut -

World Cheese Awards 2018 Results As of 07/11/2018 12:00 Version 2

World Cheese Awards 2018 Version 2. Subject to change. Awards may be added. Results as of 07/11/2018 12:00 Entry Entry Class No Award Cheese Company Name Country* Company Website 5001 4 Bronze Traditional Halloumi Cheese (one type of milk) Charalambides Christis Ltd Cyprus www.charalambideschristis.com.cy 5001 5 Bronze Meze Chevin Meze Foods South Africa https://www.mezefoods.co.za 5001 6 Silver Goat Curd Harvey & Brockless UK www.harveyandbrockless.co.uk 5001 7 Silver Tegulàt Lavialattea srl Italy www.caseificiolavialattea.it 5001 8 Bronze Classic Fresh Goat Cheese Vermont Creamery USA www.vermontcreamery.com 5001 13 Bronze Woolwich Chevrai soft unripened cheese Saputo Dairy Products Canada G.P Canada http://saputo.ca/ 5001 18 Bronze Cerney Ash Cheese Cerney Cheese Limited UK www.cerneycheese.co.uk 5001 20 Silver goats`milk cheese " SUDAO" Doña Fancisca. queseria doña francisca s.l. Spain www.queseriadonafrancisca.com 5001 21 Bronze Kecskevilág Krémsajt Kecskevilág Hungary www.kecskevilag.hu 5001 22 Bronze Fresco Cabra San Vicente Industrias Lácteas San Vicente, S.A. Spain www.lsanvicente.com 5001 24 Gold Abergavenny British Soft Goats Cheese The Abergavenny Fine Foods Co. UK http://www.abergavenny.uk.com/ 5001 26 Super Gold Fromage Blanc Cypress Grove USA www.cypressgrovecheese.com 5001 27 Silver Ms. Natural Cypress Grove USA www.cypressgrovecheese.com 5001 30 Silver QUESOCREMA ELVIRA GARCÍA Spain www.quesoselviragarcia.com 5001 31 Silver Capridor Argiolas Formaggi S.r.l. Italy www.argiolasformaggi.com Agrupación de Ganaderos de los Montes de 5001 34 Bronze Queso Fresco Montes de Málaga Málaga Spain www.agamma.es 5001 49 Bronze EPIROS KATSIKISIO (GREEK GOAT CHEESE) Epirus S.A. -

Beverages Alcoholic Drinks

Home made Coleslaw £1.95 Boscastle Sauté Potatoes £2.95 or Marmalade Bowl of Olives £3.00 Two rounds with Trewithen butter and our own homemade Jam Garlic Bread with Davidstow Cheddar £3.50 TOAST £2.50 Garlic Bread £2.95 Extra Items with trewithan dairy natural yogurt HUGOS FRUIT & NUT GRANOLA £3.50 freshly baked bap. Extra item 70p each Raspberry Heaven £3.50 Our own farmhouse sausage or Cornish dry cured Bacon in a Pineapple Sunset £3.50 BACON/SAUSAGE BAP £3.75 Strawberry Delight £3.50 FRESH FRUIT SMOOTHIES free range eggs, sauteed Cornish potatoes and field mushrooms. Leek and Davidstow cheddar Rissoles, grilled vine tomatoes, Sam's CORNISH VEGETARIAN BREAKFAST £5.25 with Callestick Ice Cream. Chocolate, Strawberry and Vanilla, £3.50 Cornish potatoes and field mushrooms. MILKSHAKES bacon, grilled on the vine tomatoes, Sam's free range eggs, sautéed Our own farmhouse sausage, 2 rashers of Cornish dry cured CORNISH BREAKFAST £5.95 Non-alcoholic Ginger Beer £2.75 Orange & Lemon Sparkle £2.50 Breakfast - SERVED UNTIL 12.00 Coke/Diet Coke £1.70 Fresh Orange Juice £2.50 Glass of Milk £1.10 Cornish Orchard Lemonade £2.50 BEER from £3.20 per Bottle. Cornish Orchards Cranberry & Raspberry Sparkle £2.50 CORNISH CIDER, LAGER, ALE & GINGER A selection of Bottled Cornish Orchards Elderflower Presse £2.50 £11.95 Per Bottle or £4.00 Per Glass (175ml) Cornish Orchards Apple Juice £2.75 CORNISH HOUSE WHITE WINE Cornish Mineral Water. Still or Sparkling £1 60 CHILLED DRINKS £11.95 Per Bottle or £4.00 Per Glass (175ml) CORNISH HOUSE RED WINE Lemon Verberna £1.95 CAMEL PENOT NOIR SPARKLING ROSE £33.00 (Bottle Only) Peppermint £1.95 Earl Grey £1.95 flavours, perfect with for any occasion. -

UK National Report (WP 2 - Deliverable 2.2)

UK National report (WP 2 - Deliverable 2.2) Pictures: Inshore fishing boats, Cornwall & Dairy cow, Somerset Authors: Damian MAYE, James KIRWAN, Mauro VIGANI, Dilshaad BUNDHOO and Hannah CHISWELL Organisations April 2018 H2020-SFS-2014-2 SUFISA Grant agreement 635577 1 UK National report Contents EXECUTIVE SUMMARY ...................................................................................................... 12 1 Introduction and methods ........................................................................... 40 2 Media Content Analysis ............................................................................... 42 2.1 Introduction ............................................................................................................. 42 2.2 The predominance of price volatility in media discourses about UK agriculture .... 42 2.3 Inshore fisheries ...................................................................................................... 43 2.4 The dairy sector ....................................................................................................... 46 3 Brexit and the UK agri-food sector ................................................................ 50 3.1 Brexit: introduction ................................................................................................. 50 3.2 Brexit: fisheries, including inshore fisheries ............................................................ 53 3.2.1 Fisheries management ................................................................................... -

TJ's Traditional Christmas Pudding Lemon Posset Rich Chocolate Box

Tommy’s crab bisque Roasted cornish turkey with brandy cream & croutons Slow roasted cornish turkey Roast potatoes, parsnip puree, TJ’s traditional Christmas pudding Flash fried cold smoked chantenay carrots, roasted chestnuts, with brandy cream and sugar topping venison loin pigs in blanket & stuffing with honey roasted parsnip & orzo pasta Lemon posset Sous vide sirloin of beef Pressed chicken & artichoke Chateau potatoes, cornish pudding, Rich chocolate box terrine watercress, cauliflower & chantenay carrots Cornish cheese board Goats cheese pannacotta Cornish blue, cornish yarg and with beetroot carpaccio Chorizo encrusted monkfish davidstow cheddar Ratta potatoes, leek and samphire polenta & cherry vine tomatoes FINISH WITH COFFEE AND Quince and apple sorbet PETIT FOURS Homemade sautéed potato BOOK YOUR TABLE TODAY: gnocchi Celeriac & apple puree with baby turnip TO BOOK YOUR TABLE SIMPLY CALL 01288 356013 5th, 6th, 12th, 13th, 19th, 20th December TJ’s slow roasted tomato soup Roasted cornish turkey TJ’s Christmas pudding with Basil, crème fraiche & ciabatta croutons Roast potatoes, seasonal vegetables brandy sauce & roast gravy Homemade chicken liver pate Hazelnut parfait with shortbread Wrapped in prosciutto crudo, served Roasted cod fillet biscuit with port wine jelly & walnut bread Paella risotto, prawns, mussels & watercress Cornish cheese board - Melted red onion filo tart Cornish blue, yarg and davidstow Baked goats cheese, balsamic shallots Savoury pancakes cheddar served with celery, grapes Ratatouille, herbed cream cheese, and crackers tomato sauce FINISH WITH COFFEE AND PETIT FOURS Christmas Party - room rates £55 Standard Double/£62 Superior Double/£70 Luxury/Family. All rates based on 2 people sharing & include breakfast Tommy Jacks Beach Hotel, Crooklets Beach, Bude, Cornwall, EX23 8NF T. -

PERFORMANCE Cheese & Whey

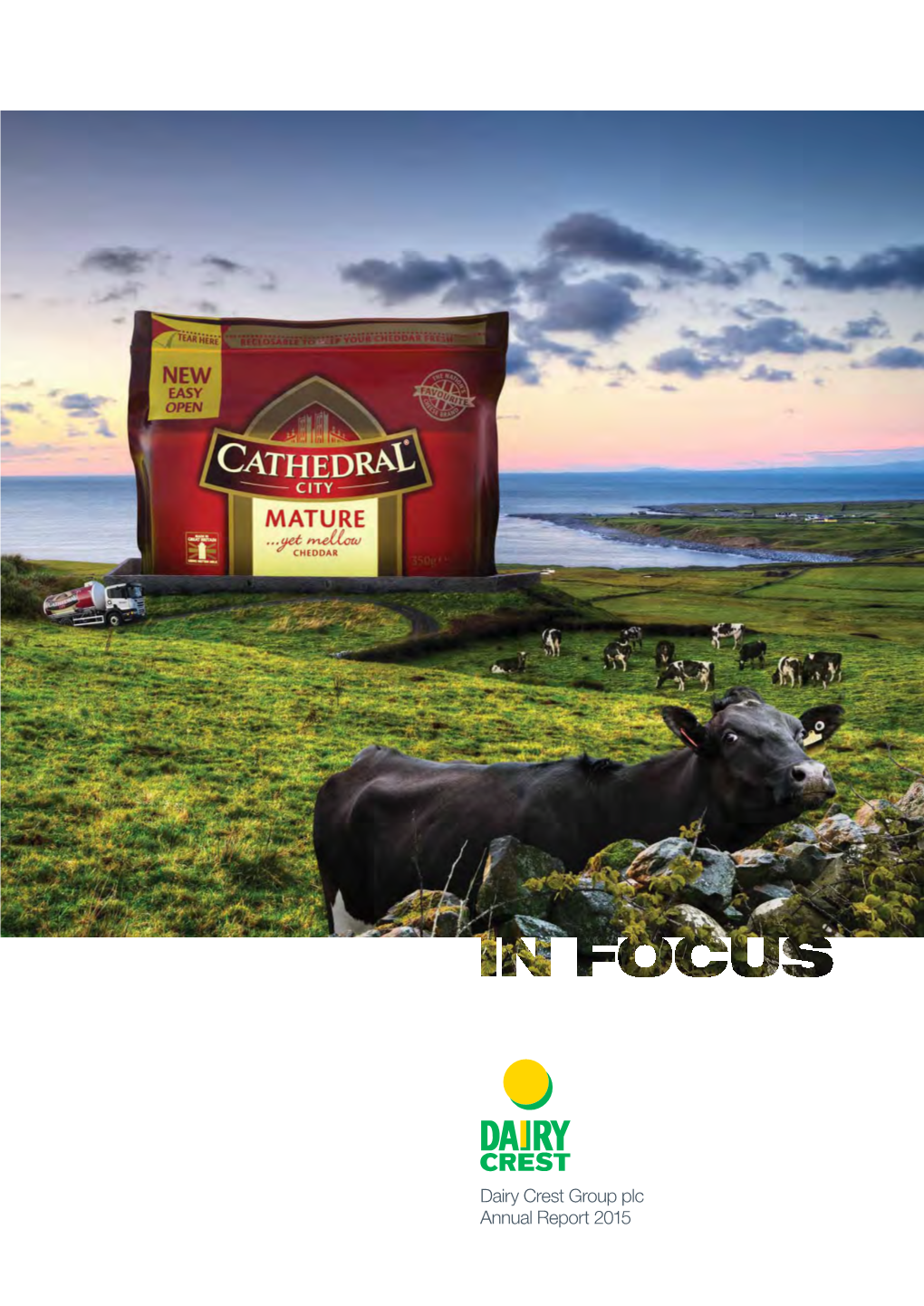

PERFORMANCE Cheese & whey March 2016 as stock made with less expensive milk is sold. Whey realisations have also fallen and this has contributed to lower reported £ million 2014/15 2013/14 margins in this business. In addition we Revenue 274.4 264.6 have adjusted our aged accruals in line Product group profit* 33.1 39.3 with the Grocery Supply Code of Practice. Margin 12.1% 14.9% * Before exceptional items and amortisation of Cathedral City continues to grow acquired intangibles market share Total retail cheese market sales were Share of the total retail unchanged over the year although cheese market by value volumes fell by 3%. Cheddar accounts for Cathedral more than half of all retail sales. Cathedral City City continued to grow market share, recording flat volumes and 5% sales growth. According to IRI, retail sales of 11% Cathedral City exceeded £280 million. Sales of competing cheddar brands have Other 89% continued to decline. Taken together the next three largest cheddar brands totalled Source: IRI 52 weeks ended 28 March 2015 £141 million, down over 20%. We continue to develop new products Dairy Crest produces and markets in the Cathedral City range. Products Cathedral City, the UK’s leading launched in earlier years such as cheese brand, as well as the Selections, Chedds, Spreadable Cathedral premium Davidstow cheddar brand. City and Baked Bites have all prospered. Milk from around 400 farmers in This year we have moved outside of Cornwall and Devon is made into cheddar for the first time and have selected cheddar cheese at our Davidstow Red Leicester and Double Gloucester for a creamery in Cornwall. -

Medal Winners by Producer

British Cheese Awards 2017 Medal Winners by Producer Abergavenny Fine Foods 622 Soft Goats Cheese with Honey & Ginger Blended - Sweet Gold 566 Soft Goats Cheese with Cranberries Dessert / Fruit / Sweet / Nuts / Seeds / Spices Silver Aillwee Cave Co Ltd 440 Burren Gold Plain Cow [over 12 months] Bronze 603 Burren Gold Garlic & Nettle Chives / Onions / Pepper / Chilli / Garlic Silver Arla Foods - Lockerbie Creamery 145 Mild White Cheddar Cheddar - Mild (open to traditional or block) Bronze 441 Extra Mature Coloured Cheddar Cow [over 12 months] Silver 427 Mature Coloured Cheddar Cow [7-12 months] Silver Arla Foods - Trevarrian Creamery 82 Character Brie Cow [with added cream] Gold 69 Character Brie Cow [over 500gm] Silver 83 Llawnroc Brie Cow [with added cream] Silver 72 Trevarrian Brie Cow [over 500gm] Silver Arla Foods -Taw Valley Creamery 307 Taw Valley The DuPont Danisco Grand Prix 3rd 241 Extra Mature Block Modern Cheddar - Extra Mature Block - Modern Bronze 192 Mature Block Modern Cheddar - Mature Block - Modern Bronze 147 Mild Cheddar Block Cheddar - Mild (open to traditional or block) Bronze 369 Double Gloucester Block The Gloucesters - Double Gloucester Block Gold 242 Extra Mature Block Modern Cheddar - Extra Mature Block - Modern Silver 146 Mild Cheddar Block Cheddar - Mild (open to traditional or block) Silver 686 Reduced Fat Hard [17-22%] Silver 275 Vintage Block Cheddar - Vintage Block [18+] Silver Arla Foods Tuxford & Tebbutt 766 Blue Stilton Blue - Stilton Bronze 768 Shropshire Blue Blue - Other Silver Arla Foods, Llandyrnog -

British Cheese Awards 2017 Champion and Special Winners

British Cheese Awards 2017 Champion and Special Winners Champion BCC1 Champion Retailer Marks and Spencer BCC1 Supreme Champion Pave Cobble White Lake Cheese BCC2 Reserve Champion Lancashire Crumbly Block Belton Cheese Limited Country Awards BCS1 Best English Cheese Pave Cobble White Lake Cheese BCS2 Best Scottish Cheese Seriously Mature Caledonian Cheese Company BCS3 Best Welsh Cheese Saval Rind Washed Caws Teifi Cheese BCS4 Best Irish Cheese Durrus Óg Durrus Cheese Main Category Awards BCS10 Best Flavour-Added Nortons Soft With Lavender Nortons Dairy BCS14 Best New Cheese Ashlynn Cheese Cellar Dairy BCS15 Best Export White Fox - Export Cheese - Belton Cheese Limited Modern British Cow BCS19 Best Dairy Product Yorkshire Yogurt Wensleydale Dairy Products BCS21 Best Packaging Award Heart-shaped Vintage Organic Godminster Cheddar BCS5 Best Fresh Cheese Pave Cobble White Lake Cheese BCS6 Best Soft White Ashlynn Cheese Cellar Dairy BCS7 Best Semi-Soft Saval Rind Washed Caws Teifi Cheese BCS8 Best Modern British Sheep Rustler White Lake Cheese BCS9 Best Blue Beauvale Cropwell Bishop Creamery Ltd Special Awards BCS12 Best Cheddar Westcombe Cheddar Westcombe Dairy BCS13 Best Territorial Lancashire Crumbly Block Belton Cheese Limited BCS16 Best Goat Cheese Cave Aged Goat Ashley Chase Estate Ltd BCS17 Best Organic Cheese Dumpling Wootton Organic Dairy BCS18 Best PDO /PGI Cheese Westcombe Cheddar Westcombe Dairy BCS20 Best Show Dressed Cheese Taw Valley Arla Foods -Taw Valley Creamery BCS22 Best Creamery Cheese Lancashire Crumbly Block Belton Cheese -

Winter 2018 £1

BOSCASTLE BLOWHOLE No 104 Winter 2018 £1 photo Jane Castling Community Chefs pictured above, left to right, are: David Lamond, Mike Stickney, Stephanie Key, Sue Viner, Rev Michael Parsons, Ruth Parsons, Mike Viner and Sue Stickney. To find out what they have been cooking up, see page 15 inside. Also inside: Boscastle Community Minibus page 3 The Reading Room page 16 News from School page 18 Boscastle Coastguard page 27 Crossword page 35 Foreword Festive Greetings to all our readers. We would like to thank all our readers, contributors, vendors and especially those unsung heroes who distribute the Blowhole each time; without your unstinting assistance, we would not have made it to issue 104. Thank You All We hope you will continue to support your village magazine. If There has been so much content to fit into this quarter’s edition anyone wants to get more that we have run out of space to include it all, have had to edit some articles and save others for the next edition. The team send condolences to involved, or has an idea the family and friends of Dave Not wanting to risk incurring the wrath of the witchy crew for a new feature or article, above, I’ve found room for their photo on this page...now I can from Easyprint. He was a star; please get in touch. eat garlic rather than dangle it from my computer monitor. always so helpful and cheery. All the best for 2019. We will all miss him. Boscastle Blowhole Team The editorial team reserves the right to accept, reject or edit any material submitted for publication. -

Grazing at Greens Bartender Breakfast

BREAKFAST AT GREENS Served until 11.30am FULL CORNISH (GF*) FRENCH TOAST (V) (GF*) Cornish pork sausage, bacon, choice of fried With Maple syrup, Greek yoghurt, berry BARTENDER or scrambled egg, mushroom, hogs pudding, compote & sliced banana – £7.50 tomato, baked beans & toast – £9.95 BREAKFAST BACON SANDWICH (GF*) Philip Warren smoked back bacon served VEGETARIAN BREAKFAST (GF*) (V) (VE*) BUCKS FIZZ in buttered sourdough – £6.00 Orange juice & Prosecco – £6.95 Buttery mushroom, wilted spinach, tomato, choice of fried or scrambled egg, beans HOMEMADE GRANOLA (V) BLOODY MARY & toast – £8.95 With Greek yoghurt, berry compote Black Cow vodka, tomato juice, & honey – £6.25 Tabasco, Worcester sauce EGGS ON TOAST (GF*) (V*) & celery salt – £7.95 choice of fried or scrambled eggs – £6.00 SOURDOUGH TOAST add bacon or sausage – £1.50 add mushroom or tomato – £1.00 (GF*) (V) With jam or marmalade – £3.50 LUNCH AT GREENS DESSERTS Served from 12pm to 3.30pm CHOCOLATE ORANGE BROWNIE (GF*) (V) With candied baby orange MAINS NIBBLES & vanilla ice cream – £6.95 CARAMELISED SHALLOT BAKED VANILLA RICE PUDDING ARTISAN BREAD (V) (VE*) (GF*) (V) (GF*) With toasted hazelnuts & & CORNISH BRIE TART (V) With olive oil and reduced balsamic – £4.00 With portobello mushrooms & a marinated miniature figs– £6.95 watercress & truffle oil salad– £12.95 MARINATED OLIVES (GF*) (V) (VE*) – £4.40 BLACKBERRY CHEESECAKE ROASTED NUTS (GF*) (V) (VE*) – £4.20 LOCAL FISH PIE (V) (GF*) Made with Cornish clotted cream, Mix of seasonal fish in a béchamel sauce, blackberry compote, -

Taste Hospitality Menu (Revised)

TASTE HOSPITALITY MENU (REVISED) PENRYN CAMPUS 2020/21 Welcome to ‘Taste’ We are relaunching our Hospitality Service as ‘Taste’ with new menus and ideas from Cornwall together with some international flavours. Aim • To provide a high quality, value for money service to our customers • To be the hospitality supplier of choice, providing a comprehensive hospitality provision with efficient and friendly service at all times • To monitor performance and feedback to ensure we meet our Customer Promise Our Customer Promise • To make our customers the focus of everything we do • To be proactive and consistent and to offer a professional service • To act with integrity and respect at all times • To provide the best customer experience possible at every opportunity In Touch • Tag and share your event on Instagram • See our latest products and menus @Taste_penryn Contact us: Campus and Commercial Events, Falmouth Exeter Plus T: 01326-370-428 E: [email protected] CONTENTS 4 How to Order (overview) 5 Refreshments & Sweet Treats 6 Breakfast Working Lunches 7 • Sandwiches & Artisan Rolls • Taste of Cornwall Buffet • Taste of Vegan Buffet • Cornish Pasties • Packed Lunches 18 Cream Tea 19 Full Booking / Amendment / Cancellation Policies Suppliers 24 Allergens and Dietary Requirements 27 Environmental Information Hospitality Menu 03 Ordering Information To view our hospitality menus and download the order form please visit: http://www.fxplus.ac.uk/hospitality Contact & Opening Hours: The Hospitality Team The Penryn Campus, Penryn TR10 9FE Monday to Friday 0900 - 1700 hours T: 01326 370428 x1428 E: [email protected] W: www.fxplus.ac.uk/hospitality Delivery Times & Prices: Monday to Friday (0800 - 1700 hours): Free delivery Deliveries outside of these hours (before 0800, after 1700) incur a £30 delivery charge Weekends: The hospitality service is primarily a Monday to Friday service, please contact us if you have a weekend requirement and we will quote separately We can accommodate many dietary requirements, just let us know in advance of the event. -

Thinking Differently Differently

Dairy Crest Group plc Dairy Crest Group plc Claygate House Littleworth Road Esher Surrey KT10 9PN Company No: 3162897 Visit our website at www.dairycrest.co.uk Annual Report 2014 http://www.dairycrest.co.uk/investors/ THINKING DIFFERENTLY Dairy Crest Group plc Annual Report 2014 THINKING THINKING DIFFERENTLY DIFFERENTLY This report is printed on Hello Silk paper. This paper has been independently certified as meeting the standards of the Forest Stewardship Council® (FSC) Cows pictured with kind and was manufactured at a mill that is certified to the permission of their owners: ISO14001 and EMAS environmental standards. John S. Pile (Farms) Ltd, The inks used are all vegetable based. Middle Farm, Lewes, East Sussex and D.Goodwin Printed at Pureprint. & Sons, Hill House Farm, Lindfield, West Sussex; Designed and produced by Tor Pettersen & Partners. both of whom supply their Photographic direction by Hudson Wright Associates. milk to Dairy Crest. Board photography by Ed Hill. CONTENTS Dairy Crest is the largest UK-owned dairy food 2 At a glance company. We process and market nutritious fresh Strategic report 4 Our business model milk and branded dairy products. The Company 6 Our strategy has a well-established strategy, a clear vision, 8 Our people 11 Acting Chairman’s statement robust values and good people. 12 Chief Executive’s review 14 Principal risks and uncertainties The year ended 31 March 2014 was one 17 Performance Strategic report of consolidation for Dairy Crest. Following the 17 – Spreads & butters 18 – Cheese & whey transformational sale of our French spreads 20 – Dairies 22 – Milk Procurement business, St Hubert, last year we have continued 23 – Corporate Responsibility to execute our long term strategy of growing our 28 – Financial review key brands and other added value sales and Governance 32 Board of Directors and Advisers reducing our costs.