Accelerators

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Map of Funding Sources for EU XR Technologies

This project has received funding from the European Union’s Horizon 2020 Research and Innovation Programme under Grant Agreement N° 825545. XR4ALL (Grant Agreement 825545) “eXtended Reality for All” Coordination and Support Action D5.1: Map of funding sources for XR technologies Issued by: LucidWeb Issue date: 30/08/2019 Due date: 31/08/2019 Work Package Leader: Europe Unlimited Start date of project: 01 December 2018 Duration: 30 months Document History Version Date Changes 0.1 05/08/2019 First draft 0.2 26/08/2019 First version submitted for partners review 1.0 30/08/2019 Final version incorporating partners input Dissemination Level PU Public Restricted to other programme participants (including the EC PP Services) Restricted to a group specified by the consortium (including the EC RE Services) CO Confidential, only for members of the consortium (including the EC) This project has received funding from the European Union’s Horizon 2020 Research and Innovation Programme under Grant Agreement N° 825545. Main authors Name Organisation Leen Segers, Diana del Olmo LCWB Quality reviewers Name Organisation Youssef Sabbah, Tanja Baltus EUN Jacques Verly, Alain Gallez I3D LEGAL NOTICE The information and views set out in this report are those of the authors and do not necessarily reflect the official opinion of the European Union. Neither the European Union institutions and bodies nor any person acting on their behalf may be held responsible for the use which may be made of the information contained therein. © XR4ALL Consortium, 2019 Reproduction is authorised provided the source is acknowledged. D5.1 Map of funding sources for XR technologies - 30/08/2019 Page 1 Table of Contents INTRODUCTION ................................................................................................................ -

2020 Diverse Founder Report 2021

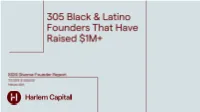

First Last Company Valuation Raise Status City Founded Race Gender ($mm) ($mm) 1 Robert Reffkin Compass $4,400 $1,500 Series G NYC 2012 African American Men 2 Daniel Perez Hinge Health $3,000 $426 Series D SF 2015 Latino Men 3 Tope Awontona Calendly $3,000 $351 Series A ATL 2013 African American Men 4 Pedro Franceschi Brex $2,600 $732 Series C SF 2017 Latino Men 5 Julia Collins Zume Pizza $2,250 $423 PE SF 2015 African American Women 6 Isabel Aznarez Stoke Therapeutics $2,160 $272 IPO BOS 2014 Latino Women 7 Jessie Woolley-Wilson Dreambox Learning $2,000 $176 Series C Seattle 2006 African American Women 8 Eugenio Pace Auth0 $1,920 $332 Series F Seattle 2013 Latino Men 9 Louis Von Ahn DuoLingo $1,650 $183 Series H Pittsburg 2011 Latino Men 10 Manny Medina Outreach $1,330 $289 Series F Seattle 2014 Latino Men 11 Jessica Alba Honest Company $1,000 $503 PE LA 2012 Latino Women 12 Toyin Ajayi City Block $1,000 $299 Series C NYC 2017 African American Women 13 Rihanna Fenty Savage x Fenty $1,000 $165 Series B LA 2017 African American Women 14 Michael Siebel Twitch $1,000 $35 M&A SF 2007 African American Men Total $28,310 $5,686 Investor Investments Investor Investments 1 Y Combinator 37 28 Rethink Education 6 2 Techstars 34 29 Salesforce Ventures 6 3 500 Startups 23 30 Sinai Ventures 6 4 Kapor Capital 19 31 AltaIR Capital 5 5 Harlem Capital Partners 16 32 Data Collective 5 6 Precursor Ventures 14 33 Founders Fund 5 7 Backstage Capital 12 34 Thrive Capital 5 8 Andreessen Horowitz 11 35 Village Global 5 9 Comcast Ventures 11 36 43North 4 10 Cross -

Corporate Venturing Report 2019

Corporate Venturing 2019 Report SUMMIT@RSM All Rights Reserved. Copyright © 2019. Created by Joshua Eckblad, Academic Researcher at TiSEM in The Netherlands. 2 TABLE OF CONTENTS LEAD AUTHORS 03 Forewords Joshua G. Eckblad 06 All Investors In External Startups [email protected] 21 Corporate VC Investors https://www.corporateventuringresearch.org/ 38 Accelerator Investors CentER PhD Candidate, Department of Management 43 2018 Global Startup Fundraising Survey (Our Results) Tilburg School of Economics and Management (TiSEM) Tilburg University, The Netherlands 56 2019 Global Startup Fundraising Survey (Please Distribute) Dr. Tobias Gutmann [email protected] https://www.corporateventuringresearch.org/ LEGAL DISCLAIMER Post-Doctoral Researcher Dr. Ing. h.c. F. Porsche AG Chair of Strategic Management and Digital Entrepreneurship The information contained herein is for the prospects of specific companies. While HHL Leipzig Graduate School of Management, Germany general guidance on matters of interest, and every attempt has been made to ensure that intended for the personal use of the reader the information contained in this report has only. The analyses and conclusions are been obtained and arranged with due care, Christian Lindener based on publicly available information, Wayra is not responsible for any Pitchbook, CBInsights and information inaccuracies, errors or omissions contained [email protected] provided in the course of recent surveys in or relating to, this information. No Managing Director with a sample of startups and corporate information herein may be replicated Wayra Germany firms. without prior consent by Wayra. Wayra Germany GmbH (“Wayra”) accepts no Wayra Germany GmbH liability for any actions taken as response Kaufingerstraße 15 hereto. -

Read Dissertation

Doctoral Dissertation: The Journey towards a Growing Diffusion of Entrepreneurship Learning and Culture in Society Written by: Mirta Michilli Role DETAILS Author Name: Mirta Michilli, PhD Year: 2019 Title: The Journey towards a Growing Diffusion of Entrepreneurship Learning and Culture in Society Document type: Doctoral dissertation Institution: The International School of Management (ISM) URL: https://ism.edu/images/ismdocs/dissertations/michilli-phd- dissertation-2019.pdf International School of Management Ph.D. Program The Journey towards a Growing Diffusion of Entrepreneurship Learning and Culture in Society PhD Dissertation PhD candidate: Mirta Michilli 21st December 2019 Acknowledgments I wish to dedicate this work to Prof. Tullio De Mauro who many years ago believed in me and gave me the permission to add this challenge to the many I face every day as General Director of Fondazione Mondo Digitale. The effort I have sustained for many years has been first of all for myself, to satisfy my desire to learn and improve all the time, but it has also been for my fifteen year old son Rodrigo, who is building his life and to whom I wish the power of remaining always curious, hungry for knowledge, and capable of working hard and sacrificing for his dreams. I could have not been able to reach this doctorate without the support of my family: my mother, for having being present all the time I needed to be away, my sister, for showing me how to undertake continuous learning challenges and, above all, my beloved husband to whom I owe most of what I know and for dreaming with me endlessly. -

Tech Startup Ecosystem in West Bank and Gaza

Tech Startup Ecosystem in Public Disclosure Authorized West Bank and Gaza FINDINGS AND RECOMMENDATIONS Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized This map was designed over a map produced by the Map Design Unit of the World Bank. The boundaries, colors, denominations and any other information shown on this map do not imply, on the part of The World Bank Group, any judgment on the legal status of any territory, or any endorsement or acceptance of such boundaries. Content Authors and Acknowledgements 1 Executive Summary 2 Measuring and Analyzing the Tech Startup Ecosystem in the West Bank and Gaza 5 Measuring the Tech Startup Ecosystem 5 Analyzing the Tech Startup Ecosystem 6 The Tech Startup Ecosystem in the West Bank and Gaza 9 Skills 12 Supporting Infrastructure for Entrepreneurship 14 Investment 17 Community 20 Startup Success Factors 23 Gap Analysis and Policy Recommendations 24 Summary of Gap Analysis and Stage of Ecosystem 24 Policy Recommendations 25 Appendix: Survey Methodology and Analysis 28 Methodology 28 Short-Term Success 32 Long-Term Success 32 Notes 33 References 34 LIST OF TABLES Table 1.1 Networking Assets 7 Table 1.2 Categories of Ecosystems 8 Table 3.1 Development Stage of Ecosystem 24 Table 3.2 Policy Recommendations 25 LIST OF FIGURES Figure 2.1: Startup Growth in the West Bank and Gaza 9 Figure 2.2: Time to Complete Procedural Tasks in Life Cycle of a Startup Across Regions 10 Figure 2.3: Percentage of Female Founders Across Analyzed Ecosystems 10 Figure 2.4: Gender Distribution -

The Bay Area Innovation System Science and the Impact of Public Investment

The Bay Area Innovation System Science and the Impact of Public Investment March 2019 Acknowledgments This report was prepared for the Bay Area Science and Jamie Lawrence, IBM Corporate Citizenship Manager – Innovation Consortium (BASIC) by Dr. Sean Randolph, California, Hawaii, Nevada, Utah, Washington Senior Director at the Bay Area Council Economic Daniel Lockney, Program Executive – Technology Transfer, Institute. Valuable assistance was provided by Dr. Dorothy NASA Miller, former Deputy Director of Innovation Alliances at Dr. Daniel Lowenstein, Executive Vice Chancellor and the University of California Office of the President and Provost, University of California San Francisco Naman Trivedi, a consultant to the Institute. Additional Dr. Kaspar Mossman, Director of Communications and support was provided by Estevan Lopez and Isabel Marketing, QB3 Monteleone, Research Analysts at the Institute. Dr. Patricia Olson, VP for Discovery & Translation, California Institute for Regenerative Medicine In addition to the members of BASIC’s board of Vanessa Sigurdson, Partnership Development, Autodesk directors, which provided review and commentary throughout the research process, the Economic Institute Dr. Aaron Tremaine, Department Head, Accelerator Technology Research, SLAC National Accelerator Laboratory particularly wishes to thank the following individuals whose expertise, input and advice made valuable Eric Verdin, President & CEO, Buck Institute for Research on Aging contributions to the analaysis: Dr. Jeffrey Welser, Vice President & Lab Director, IBM Dr. Arthur Bienenstock, Special Assistant to the President for Research – Almaden Federal Policy, Stanford University Jim Brase, Deputy Associate Director for Programs, Computation Directorate, Lawrence Livermore National Laboratory About BASIC Tim Brown, CEO, IDEO BASIC is the science and technology affiliate of the Doug Crawford, Managing Director, Mission Bay Capital Bay Area Council and the Bay Area Council Economic Dr. -

STARTUP ACCELERATOR PROGRAMMES a Practice Guide Acknowledgements

STARTUP ACCELERATOR PROGRAMMES A Practice Guide Acknowledgements This guide was produced by the Innovation Skills team in collaboration with the Policy and Research team. It draws on Nesta’s reports – specificallyThe Startup Factories written by Kirsten Bound and Paul Miller, and Good Incubation written by Jessica Stacey and Paul Miller – as well as Nesta’s practical experience supporting the startup and accelerator community in Europe. Thanks to Kate Walters, Jessica Stacey, Christopher Haley and Isobel Roberts, who all contributed to the content, and to Kirsten Bound, Brenton Caffin, Bas Leurs, Theo Keane, Sara Rizk and Simon Morrison who all provided valuable feedback along the way. Nesta’s Practice Guides This guide is part of a series of Practice Guides developed by Nesta’s Innovation Skills team. The guides have been designed to help you to learn about innovation methods and approaches and put them into practice in your work. For further information, contact [email protected] Nesta is an innovation charity with a mission to help people and organisations bring great ideas to life. We are dedicated to supporting ideas that can help improve all our lives, with activities ranging from early–stage investment to in–depth research and practical programmes. Nesta is a registered charity in England and Wales with company number 7706036 and charity number 1144091. Registered as a charity in Scotland number SCO42833. Registered office: 1 Plough Place, London, EC4A 1DE. www.nesta.org.uk ©Nesta 2014 STARTUP ACCELERATOR PROGRAMMES A Practice Guide CONTENTS INTRODUCTION 4 SECTION A: WHAT IS AN ACCELERATOR PROGRAMME? 6 SECTION B: WHY CONSIDER AN ACCELERATOR PROGRAMME? 12 SECTION C: SETTING UP AND RUNNING AN ACCELERATOR PROGRAMME 15 1. -

The Startup Factories. the Rise of Accelerator Programmes

Discussion paper: June 2011 The Startup Factories The rise of accelerator programmes to support new technology ventures Paul Miller and Kirsten Bound NESTA is the UK’s foremost independent expert on how innovation can solve some of the country’s major economic and social challenges. Its work is enabled by an endowment, funded by the National Lottery, and it operates at no cost to the government or taxpayer. NESTA is a world leader in its field and carries out its work through a blend of experimental programmes, analytical research and investment in early- stage companies. www.nesta.org.uk Executive summary Over the past six years, a new method of incubating technology startups has emerged, driven by investors and successful tech entrepreneurs: the accelerator programme. Despite growing interest in the model from the investment, business education and policy communities, there have been few attempts at formal analysis.1 This report is a first step towards a more informed critique of the phenomenon, as part of a broader effort among both public and private sectors to understand how to better support the growth of innovative startups. The accelerator programme model comprises five main features. The combination of these sets it apart from other approaches to investment or business incubation: • An application process that is open to all, yet highly competitive. • Provision of pre-seed investment, usually in exchange for equity. • A focus on small teams not individual founders. • Time-limited support comprising programmed events and intensive mentoring. • Cohorts or ‘classes’ of startups rather than individual companies. The number of accelerator programmes has grown rapidly in the US over the past few years and there are signs that more recently, the trend is being replicated in Europe. -

Creating LAIA Foreword

Creating LAIA Foreword The lack of capital and support has been a constant refrain a feasibility study on the potential of a women-focused heard from female entrepreneurs at every stage of growth. LA incubator and accelerator, hence this publication A recent report by JPMorgan Chase and The Initiative for of Creating LAIA: The Feasibility of a Women-Focused a Competitive Inner City (ICIC) found that women (and Incubator & Accelerator in Los Angeles. minorities) “are not participating in high-tech incubators and accelerators at the same rates as their white, male Creating LAIA is the definition of collaboration - what counterparts.” women do organically. Although it was ofcially and adroitly written by We Are Enough Executive Director and After I gave my 2015 TEDx Talk, “Why You Should be Sexist Co-founder, Delilah Panio, the final product was birthed by with Your Equity Capital,” I was surprised by how many many. Along with the women entrepreneurs and women- women entrepreneurs approached and requested to meet focused incubator and accelerator leadership listed in with me – each emotionally describing their reactions to the appendix, we have had conversations with or have what I thought was the unemotional subject of finance and listened to many female investors and entrepreneurs who money. The majority of these women were small business have informed the conclusions reached in Creating LAIA. owners who articulated stories of the difculty in growing To name a few – Monica Dodi, Kara Nortman, Efe Epstein, their businesses, specifically the lack of support and Dana Settle, Kesha Cash, Carman Palafox, Noramay capital. I soon learned that many women had an emotional Cadena, Adena Smith, Diane Manuel, Ana Quintana, Darya and insecure relationship with money. -

SILICON VALLEY Playbook

© 2017 | The official magazine for Published by the Consulate General of the Netherlands in San Francisco Dutch businesses visiting Silicon Valley SILICON VALLEY playbook René Bonvanie of Palo Alto Networks shares his insights for startups coming to Silicon Valley fix your cap table! WHAT INVESTORS Flyr founder Alexander Mans explains how he managed WANTto build a successful business inTO Silicon Valley KNOW Everything you have always wanted to know talk founder about moving to San Francisco to founder Super Evil Megacorp Co-founder Tommy Krul on his adventures as a Dutch Game Coder in Silicon Valley taking the big plunge super evil megacorp Plus: Plus: Plus: Plus: prepare your go build that work hard, read about the journey with a killer pitch play hard: the other side of visual toolbox deck best spots at night silicon valley Foreword You are in charge of 02 your own success! The Inside Silicon Valley Playbook Thank you to the following people was published by the Consulate (without you this magazine could General of the Netherlands in San never have been created!): Silicon Valley is a unique place. The buzz is palpable and infectious. Francisco Competition is relentless. Everyone is working on something big. The Consulate General of the More about Production, design, content and Netherlands in San Francisco : Everywhere you look there are people who can help enrich your interviews by 30X Amsterdam and Gerbert Kunst | Michiel Engelaar | experience. And everyone is willing to share in order to help Startup Delta Business Models Inc. San Francisco Jasper Smit | Alexander Kramer others succeed. For general information about this Investors, founders and experts: publication, please contact us. -

Local Connectedness

Global Startup Ecosystem Report 2018 Article: Local Connectedness Copyright © 2018 Startup Genome LLC. All Rights Reserved. 1 About About the Global Startup Genome Entrepreneurship Network Startup Genome works to increase the success rate The Global Entrepreneurship Network (GEN) operates of startups and improve the performance of startup a platform of projects and programs in 170 countries ecosystems globally. In a collaborative effort with hun- aimed at making it easier for anyone, anywhere to start dreds of public and private organizations in more than 30 countries and scale a business. By fostering deeper cross border collabora- we built the world’s largest primary research on startups, the Voice tion and initiatives between entrepreneurs, investors, researchers, of the Entrepreneur, with +10,000 founders participating each year. policymakers and entrepreneurial support organizations, GEN This allowed us to develop rigorous models that are considered work to fuel healthier start and scale ecosystems that create more the new science of startup ecosystem assessment. jobs, educate individuals, accelerate innovation, and strengthen economic growth. We advise leaders of innovation ministries, agencies, and organi- zations supporting startups, bringing data-driven insights, clarity, Our extensive footprint of national operations and global ver- and focus to actions that produce more scaleups, job creation, ticals in policy, research and programs ensures members have and economic growth. With our partners Global Entrepreneurship uncommon access to the most relevant knowledge, networks, Network and Tech Nation (formerly Tech City UK), and thanks to the communities and programs relative to size of economy, maturity generous support of the Kauffman Foundation, we deliver holistic, of ecosystem, language, culture, geography and more. -

Alberta Innovates Meta-Analysis of Accelerators

Meta-Analysis of ACCELERATORS Report submitted to Alberta Innovates February 9, 2021 Geoff Gregson TABLE OF CONTENTS EXECUTIVE SUMMARY 3 1 INTRODUCTION 7 2 BACKGROUND TO STUDY 10 3 LATEST THINKING ON ACCELERATORS 16 4 INVESTOR-LED ACCELERATORS 22 5 MATCHMAKER & SCALE-UP ACCELERATORS 40 6 DISCUSSION AND SUMMARY 48 REFERENCES 59 APPENDIX A: COMPARATIVE PROFILE OF ACCELERATORS 64 APPENDIX B: ACCELERATOR DESCRIPTIVE DATA 65 2 EXECUTIVE SUMMARY This report presents a meta-analysis of business accelerators and draws out relevant insights to inform on the Alberta entrepreneurial ecosystem. A summary of key insights are presented below; ordered under three questions that guide the study. A more detailed discussion of findings can be found in Section 6. Key Insights What are the benefits & challenges of adopting branded globally recognized business accelerators versus developing regional & local accelerator programs? Participation in leading accelerator programs may have a strong ‘positive’ signaling effect distinct from program content. Signaling effects reveal to investors that a founder has undergone a rigorous selection process and may assist founders in recruiting talent & securing other resources. Leading accelerators possess established & repeatable processes that have proven successful. Costs of learning by trial & error to create a home-grown program are difficult to forecast but could be substantial and include direct costs (funding) & indirect costs (reputation). Leading accelerators may provide access to resources that would be difficult to access otherwise. This includes access to seed funding & follow-on investment, extensive mentor & alumni networks, domain experts & peer-to-peer learning with highly qualified founders in the cohort. Seed accelerators may help founders learn when & how to fail & aid in more efficient development decisions.